BRMK - Broadmark Realty Capital: Things Are Ugly But I'm A Buyer

Summary

- Broadmark Realty Capital has seen its share price decline 60% year-to-date as the US residential real estate market has gone from hot to cold.

- Broadmark has many issues including: high level of non-performing loans, management turnover, and most recently a dividend cut.

- However, with minimal debt, limited exposure to structurally challenged assets, and a price to adjusted tangible book value of just 0.53x, I see a favorable risk-reward.

2022 has been a nightmare for mortgage REIT Broadmark Realty Capital ( BRMK ) shareholders. The dramatic downturn in the US housing market has led to a spike in non-performing loans as small homebuilder clients have faced a multitude of challenges (discussed below). In addition, the company's CEO recently departed and to make matters even worse, the dividend was recently cut.

Despite these very real negatives, I see a favorable risk/reward given that BRMK has little exposure to troubled asset classes (such as office real estate), little debt (sub 10% debt to equity ratio), and trades at just 0.53x tangible book value.

Background & Overview

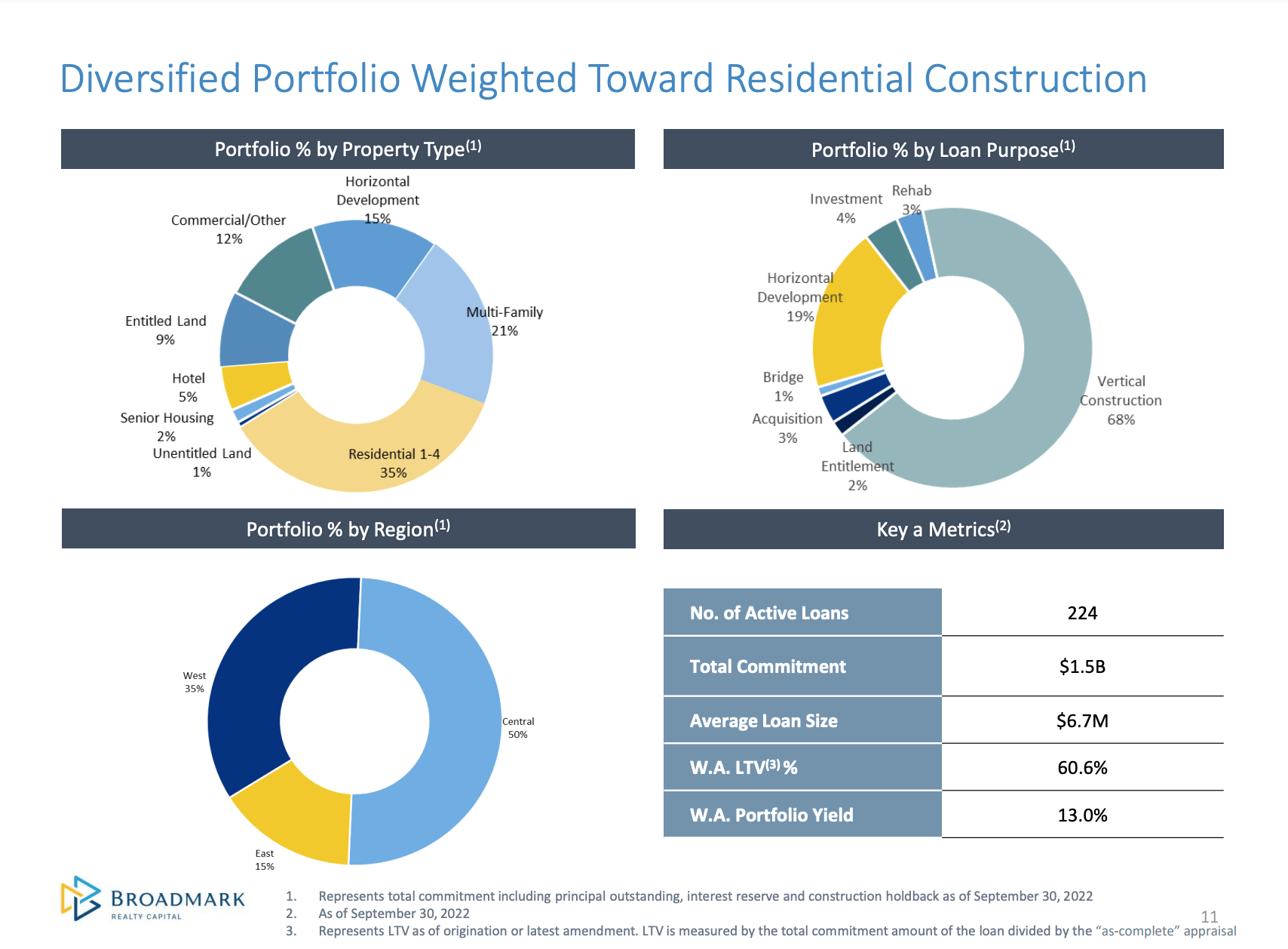

Founded in 2010, BRMK came public in 2019 through a SPAC transaction. While categorized as a 'mortgage REIT' BRMK is really what is known in the industry as a 'hard money lender' - it makes small ($6.7 million average size) short-term loans secured by property to developers (mainly small condo/townhome buildings) at relatively high interest rates (10%+; nearly double what mortgage REITs earn on assets).

{kind=link}

Historically BRMK had focused on lending to residential developers in the state of Washington but had broadened its portfolio to $800 million across a dozen states (with meaningful exposure to Washington, Utah, and Colorado) by 2019. Today the company has a just under $1 billion portfolio (across 20 states) with ~80% of its loan exposure to residential real estate assets.

Current Results/ Problems

To put it mildly, things have not gone well for BRMK in 2022. Coming into the year, the company was doing fine as the US residential real estate market was on fire - homes were frequently selling within a week of listing, often above list price. Fast forward to today and mortgage rates have soared from 3% at the beginning of the year to over 6%. This has caused a dramatic slowdown in housing transaction activity and as higher mortgage payments have priced many buyers out of the market.

{kind=link}

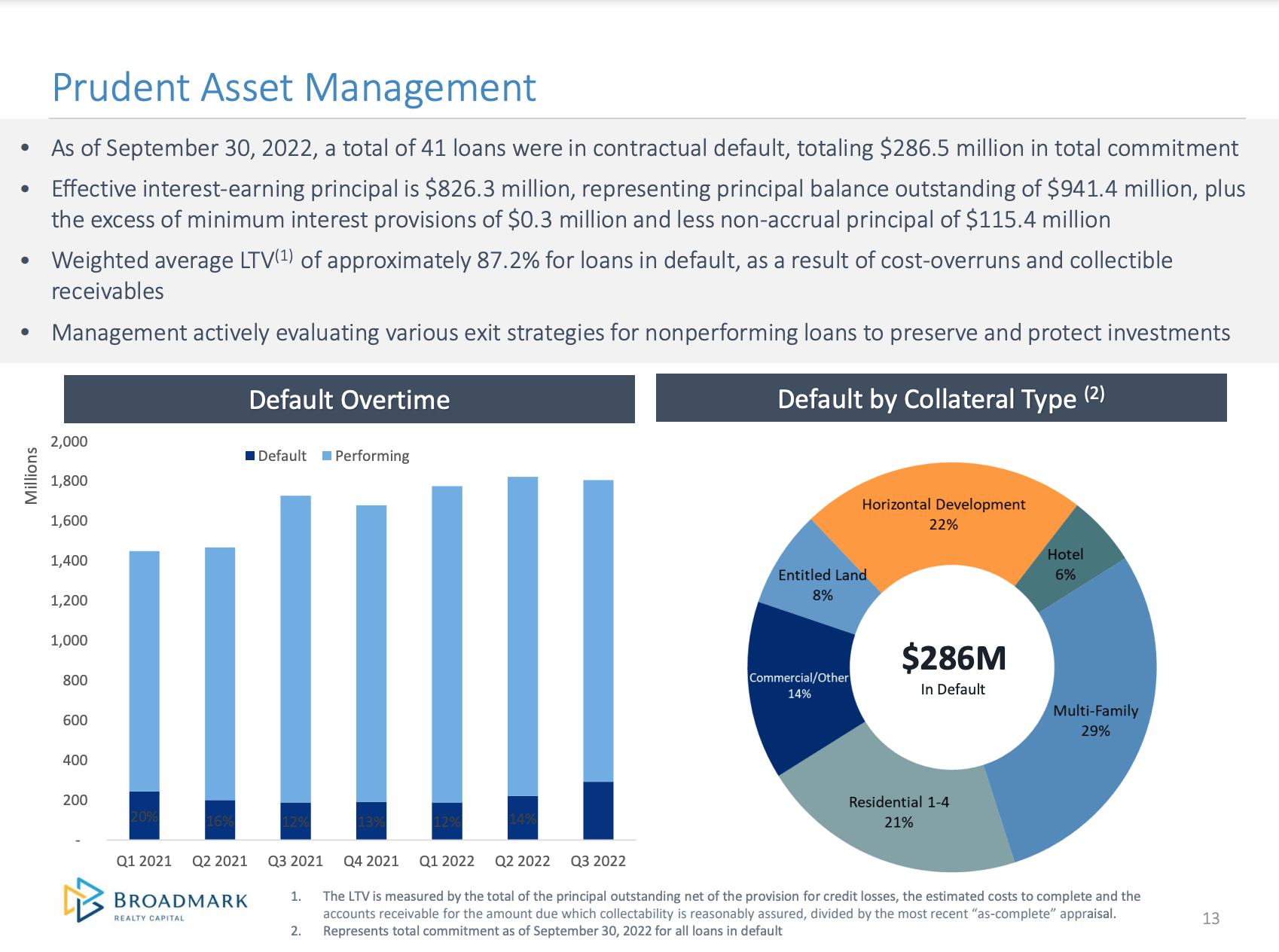

This has had several impacts, most notably a dramatic rise in defaulted assets as shown above. At the time BRMK came public, defaulted assets (borrower is not making interest/principal payments) represented less than 5% of its loan book. Today, however, defaulted loans represent ~30% of loans. While the macro environment certainly has played a large role in the spike in defaults, I suspect that BRMK's rapid expansion into new states (particularly in a hot market) also made a significant contribution to the spike in defaults.

Note that BRMK estimates that the current Loan to Value estimate for defaulted properties is 87%. Given that BRMK typically originates loans at no more than 65%, this shows how wrong things have gone for these loans (cost over-runs & property price declines).

As a result of poor performance it there was a 'mutual' decision for the CEO to step down (from the press release , it sounds like he was fired which makes sense given the terrible performance). On top of this, the CFO had announced his resignation just a month prior. Chairman of the Board (and former BRMK CEO) Jeff Pryatt assumed the role of interim CEO while the company searches for a new CEO.

Lastly, with over 25% its asset base (defaults) not contributing to earnings, BRMK has seen a significant decline in interest income. When coupled with increased loan loss provisions (for defaulted loans), this has caused the company to swing to a loss in 3Q22 and lead BRMK to cut its monthly dividend by 50% .

Reasons to own: Strong Balance Sheet & Valuation

While BRMK faces significant near term challenges as described above, I recently purchased a small position in the stock. I see the following investment positives:

- As shown in the Background & Overview, over 80% of BRMK's loan exposure is to residential real estate. Residential real estate is supported by demographic trends (growing population, millennials entering home buying years) and doesn't face structural concerns like office (due to work-from-home pressure).

- BRMK has a very strong balance sheet with debt to equity of less than 10%. It is very unusual to encounter a mortgage REIT or even a hard money lender that has so little debt. This greatly reduces the risk of financial distress and (for the time being at least) allows the company to continue to make dividend payments - even after the cut, the current yield is over 10%.

- BRMK trades at a very low valuation. The company trades at a stated Price-to-Book ratio of 0.46x and a Price-to-tangible book of just 0.53x (tangible book value at 9/30 was $7.24).

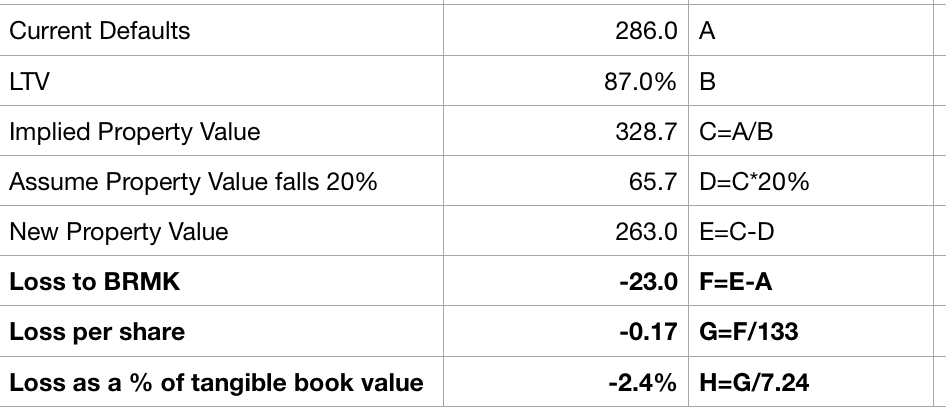

As shown on the Non-Performing Asset slide in the previous section, BRMK believes that its defaulted loans have a current loan to value of 87%. This implies that, in aggregate, it should not incur losses here even after cost over-runs and property price declines. While cost overruns should slow as labor becomes more available and the supply chain has largely normalized, I expect we could continue to see declines in home prices. Were the values of defaulted fall an additional 20% from BRMK's current estimate, as shown below, I calculate that this would only reduce BRMK's tangible book value by $0.17 or 2.4%.

Impact of Home Price Decline on Defaulted Loans (Company Filings; Author Estimates)

{kind=link}

While this is a rough guesstimate with some implicit assumptions, it illustrates that BRMK can weather a fairly significant hit to its defaulted portfolio without seeing a big decline in book value.

Risks

- US Home prices decline meaningfully in 2023 and beyond.

- Having performed very poorly thus far in 2022, we could see additional tax-loss selling in the near term which could further depress the share price.

- Another dividend cut would likely cause the share price to decline

Conclusion

Despite facing significant challenges, I don't see much downside at BRMK even if housing prices fall significantly. With shares trading at just over 50% of tangible book value I've purchased a small position in the stock.

For further details see:

Broadmark Realty Capital: Things Are Ugly But I'm A Buyer