BBUC - Brookfield Business Partners: Valuation Getting More Compelling

2023-11-20 11:00:00 ET

Summary

- Brookfield Business Partners has underperformed the S&P 500 and Industrial Select Sector SPDR by over 100%.

- We look at the Q3-2023 results which showed yet another successful exit.

- We tell you why the valuation is creating an asymmetrical payoff structure.

On our last coverage of Brookfield Business Partners L.P. ( BBU ) and its corporate entity version Brookfield Business Corporation ( BBUC ) we decided to stay out. The challenging business environment was in full display as the company's extremely leveraged holdings felt the full brunt of the interest rate hikes.

The performance since inception has been underwhelming and BBU has trailed the broader S&P 500 ( SPY ) and Industrial Select Sector SPDR ( XLI ) by more than 100%.

We don't expect BBU to repair this deficit any time soon. The stock might make sense for those that believe that the next rate cut cycle is about to begin and BBU's self-computed NAV is accurate. We don't buy either, and hence, we don't want to buy BBU.

Source: EAF Highlights The Challenging Environment

That was the correct decision and the stock has continued to be a poor performer.

Seeking Alpha

We are going to look at the Q3-2023 numbers today and tell you why we are having slight shift in stance.

A Little Background

Unlike the people who find everything Brookfield Asset Management ( BAM ) does as sacrosanct, we fall in the minority. We have repeatedly pointed out flaws in the Brookfield babies when prices detached from reality . We think Brookfield Property Partners L.P. 5.75 CL A PF SR3 ( BPYPN ) likely suspends its distribution . We have repeatedly criticized the BBU model as well putting a Sell rating on it in the past . So this is not the star-struck fan club that is telling you how "Brookfield will help you retire rich" for the thirtieth time.

Q3-2023

BBU is a hard company to analyze. The metrics you get every quarter are the EBITDA and the EFO, neither of which gets to the real owner equivalent earnings. But you have to use what you get and in this case, the adjusted EBITDA was higher by about 7%. Segmental EFO was mixed and corporate costs were way higher.

BBU Q3-2023 Presentation

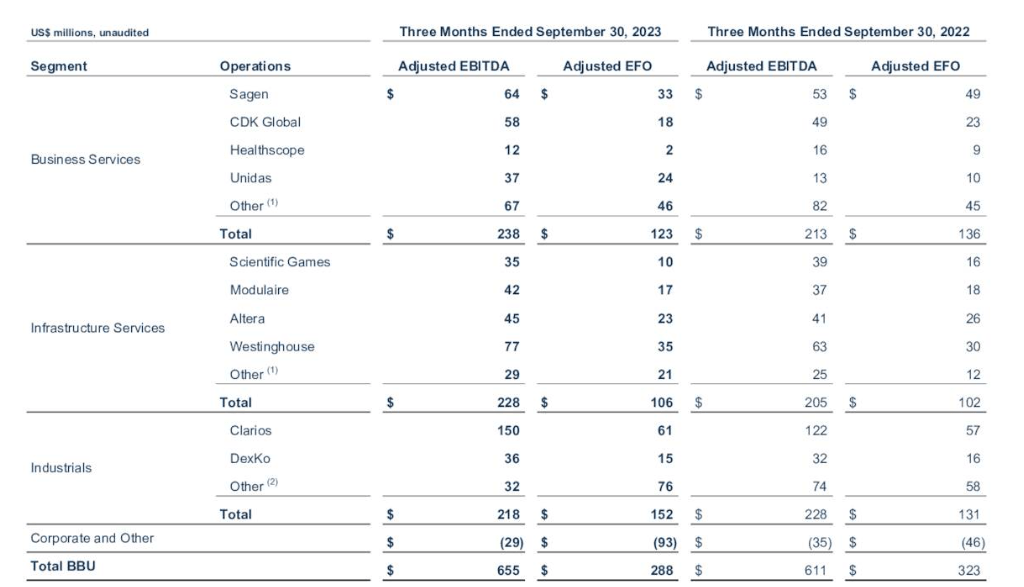

Looking at it on a segment level we can clearly see the star of the story. Clarios' EBITDA was up from $122 million to $150 million. Westinghouse was also doing well, but that unit sale is almost completed.

{kind=link}

Business services and infrastructure services are doing fine overall as you see the delta in the different components. Industrials had a big drop in the "other" category. Included here is the publicly traded entity GrafTech International Ltd.( EAF ).

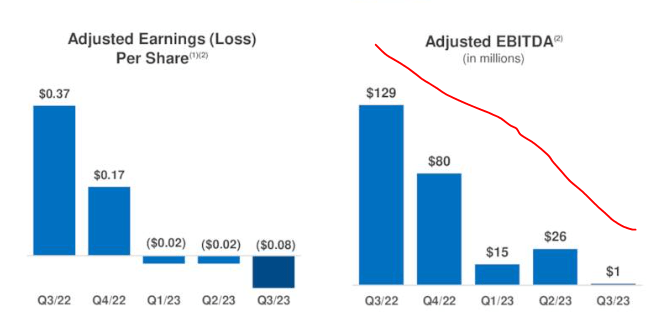

That performance has not been undeserved.

{kind=link}

Debt to EBITDA blew up from around 1.0X to almost 7.0X in one year. The company has the liquidity at present but it will be challenging for the equity until the next up-cycle starts.

{kind=link}

That is what happens to cyclical companies. So there are difficulties in individual business units and the only reason we can see this one, is because it is publicly traded. All that said, there was some good news for shareholders as BBU exited another business at a high multiple.

{kind=link}

BBU has shown a good deal of success on the investment side and this is yet another example.

Outlook

On a proportionate share basis, BBU carries an enterprise value of around $20.6 billion.

BBU Q3-2023 Presentation

This enterprise value is supported by $2.5 billion of proportionate adjusted EBITDA over the last 12 months. Collectively, this is growing quite nicely as you can see from the delta from the previous 12 months.

{kind=link}

This gets us to an implied valuation of 7.8X on EV to EBITDA. On a contextual basis The S&P 500 trades near 13X. We would have not thought about making that direct comparison, but BBU actually mentioned that on their conference call.

Stepping back, BBU is a very valuable business today. Despite the progress we’ve achieved, the trading performance of our units on any relevant metric is materially disconnected from value. To put this in context, today, we’re trading at less than 8 times annual EBITDA, and a significant discount to the broader S&P 500 that’s trading at 13 times. Businesses that generate similar margins to ours are trading closer to 15 times. The discount in the trading performance of our units and shares matters greatly to us, because we know it matters to each of you. We are committed to doing everything we can to continue enhancing the value of our business, including continuing our buyback program, which is highly accretive to value at current prices.

Source: BBU Q3-2023 Conference Call Transcript

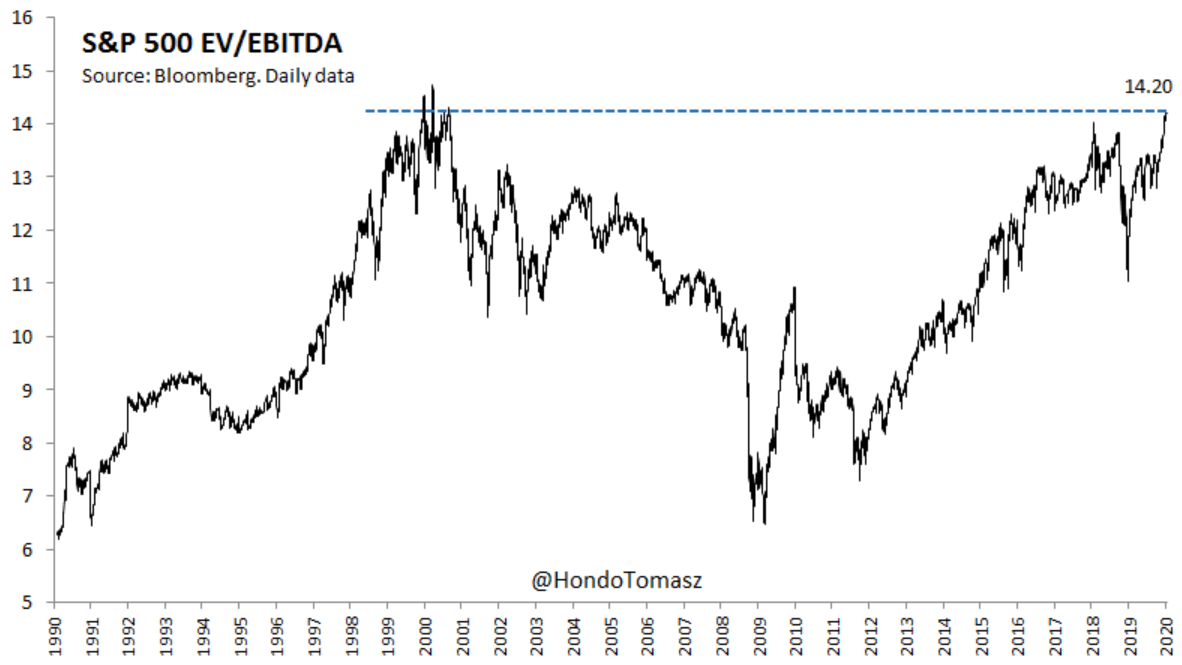

Of course 13X is at the very high end of what you pay for S&P 500. The legendary 2000 peak was near 14X.

{kind=link}

So while BBU may argue it is cheaper relative to S&P 500, it is an easy bar to jump over. Still 7.8X is on the unusually cheap side for businesses. If we had certainty that this collection of businesses could traverse the business cycle and the upcoming recession, it would be a rather clear buy. Of course, based on their leverage structure and the heavily loaded liability side, we have no idea which ones will make it. To be sure, there are some here that are thriving even today. Just see the context put on Clarios by management.

To put this in context. Clarios, our advanced energy storage operations is generating more than $500 million of free cash flow each year. And that’s after investing in new capacity to support the growth of its advanced battery operations. While this cash could be distributed to BBU and our partners, the business has been deleveraging. And during the quarter, it paid down an additional $700 million of debt. As a result, the net leverage of the business has come down to around 4.5 times EBITDA, compared to 6.5 times when we acquired it.

Source: BBU Q3-2023 Conference Call Transcript

BBU has also shown some enthusiasm in its own units, though arguably this has been restrained by the desire to keep dry powder to bail out challenged subsidiaries:

Jaspreet Dehl

Maybe just, Gary, if I can add, last year, we bought back about 2.5 million units. This quarter, we bought back an additional about 55,000 units under the NCIB. So, that program is active and we’ll continue to buy back.

Gary Ho

Okay. And then, Jaspreet, Well, I have you here. If you take the $1.5 billion proceeds, that reduces I think your debt roughly by 40%, 45% on the corporate debt side. Has your views changed on not carrying any corporate debt? And should we continue to see that balance grind down over time from future monetization or distributions?

Jaspreet Dehl

Yeah. So, look our long-term goal continues to be – to not have any permanent corporate debt at the BBU level. And you’ve seen over the last year we’ve sold a number of our smaller operations, the cash that’s being generated, we’re using it, we’re paying down the debt and that continues to be the focus. So that view hasn’t changed.

Source: BBU Q3-2023 Conference Call Transcript

Verdict

At 7.8X EV to EBITDA, BBU presents an unusual and asymmetric play. Remember this is a debt loaded to the max structure but the debt is all (or rather almost all) at the subsidiary level. If we get that rerating multiple down the line, it will really create a multiplier effect to the equity portion.

Source: BBU Q3-2023 Presentation

You could triple your equity portion pretty easily just by getting to a 10-11X EV to EBITDA. Sure, there will be some units which will be distressed, but BBU has the power to bail them out and extend liquidity where and when needed. The subsidiary level debt works like a secured mortgage. BBU can (though usually will not choose to) walk away from distressed cases. It can also get the full upside of those investments which do very well, one example of which was seen in the last quarter. At present, we think this offers an opportunity to dollar cost average into a position over the next 12-24 months. The next cycle which may be a good deal away, is where you are likely to triple your money from the trough. We don't own it at present as there are no longer term options on this one. Ideally we would like to start initiating covered calls here, but the lack of options makes it a less exciting prospect.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Brookfield Business Partners: Valuation Getting More Compelling