BIP - Brookfield Is Scaling Up - Q2 Earnings Calls And Investment Opportunities

- BAM and BAMR are attractive due to ongoing business development and the coming spin-off of the asset management business.

- BIP/BIPC are trading close to their fair value. The commissioning of the Heartland Petrochemical Complex late this year may become a catalyst for the stock.

- BEP/BEPC are priced high and appear unattractive due to mediocre distribution growth.

- BBU/BBUC may be held short-term as long as they are trading below their incentive distribution thresholds but are not suitable for buy and hold.

This is a review of recent developments within the Brookfield conglomerate that includes public Brookfield Asset Management (BAM), Brookfield Infrastructure (BIP) (BIPC), Brookfield Renewable (BEP) (BEPC), Brookfield Business (BBU) (BBUC), and Brookfield Reinsurance (BAMR). Due to the breadth of the topic, we will not go deep into details but try to mark the most attractive investment catalysts.

Brookfield Asset Management

Q2 was very successful for BAM but the stock started recovering even before the quarterly announcement. A year ago, I issued a warning about BAM ( Brookfield Is More Expensive Than Ever ) and sold a fraction of my holdings shortly after at $60+. In May and June, I published two bullish articles on BAM ( Brookfield Has Become A Screaming Buy and Brookfield And Other Asset Managers Are Trading As If There Were No Tomorrow ) and added to my position at $43-45. The strategy has been profitable and hopefully, my readers were able to do something similar.

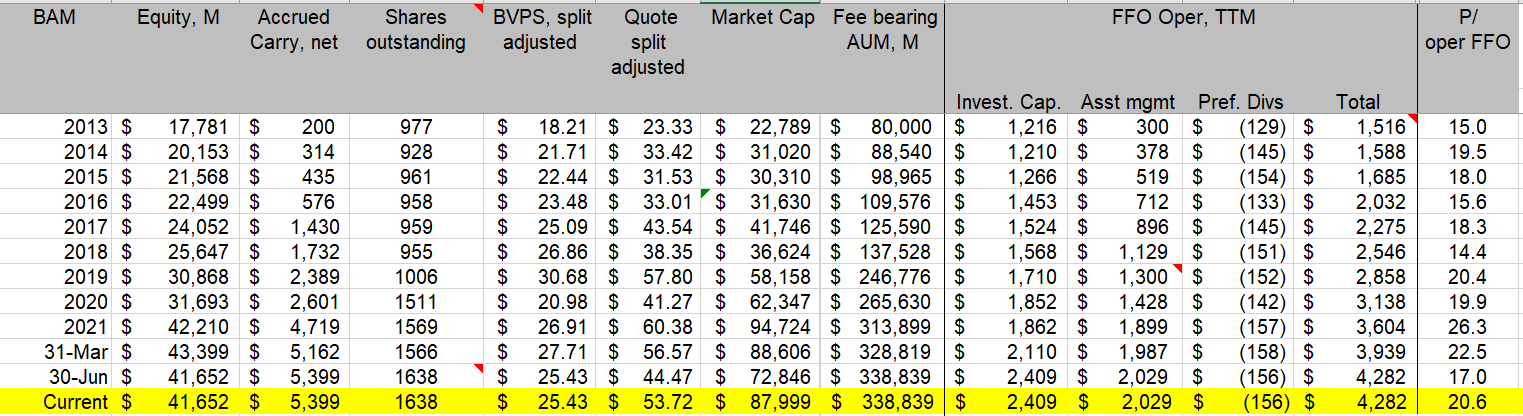

I will start with an update of my regular table (numbers are in millions of USD).

BAM's important metrics over years (Company's filings and author's calculations)

{kind=link}

A couple of footnotes to this table: a) from Q2, I started using diluted shares as opposed to basic before. It is related to the growing importance of BAMR as its shares are exchangeable into BAM; b) the AUM column indicates prorated shares as I exclude 38% of Oaktree assets. Since BAM stopped reporting Oaktree assets separately several quarters ago, it is an estimate.

Operating FFO, which I consider the most important metric of BAM's progress (together with fee-bearing AUM) jumped in the quarter which is noticeable even on a TTM basis. Surprisingly, it was due to Invested Capital as opposed to FRE (fee-related earnings) as is normally the case. All segments of the Brookfield empire contributed as is obvious from the second table that we will refer to in the subsequent sections.

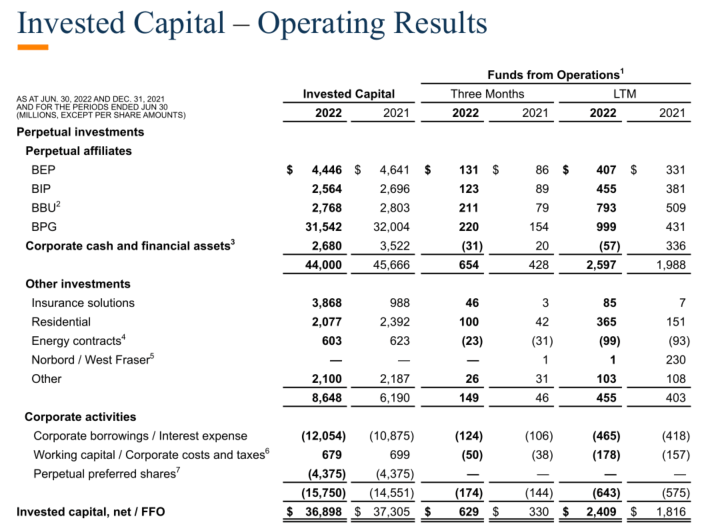

Invested Capital Operating FFO, Q2 22 (BAM's Q2 2022 filings)

{kind=link}

On the earnings call, Bruce Flatt updated us on preparations for the Asset Management spinoff (it will be called Brookfield Asset Management but we will call it Manager here; whatever is left will be called Brookfield Corporation). Excellent Q2 results require us to update our valuation of BAM on a proforma (after spin-off) basis (I am referring readers to my last two publications for details on FRE multiple and value of carry).

1. Manager is worth 25*FRE+Carry = 25*2.029+5 ~ $56B

2. Invested Capital produced Oper. FFO after preferred dividends of ~ $2.25B. If we value Invested Capital at its equity, it is equivalent to P/FFO = 41.65/2.25 ~ 18.5. This is a reasonable multiple, perhaps a bit elevated. I would roughly estimate Invested Capital at ~ $35-40B now which is significantly higher than a quarter ago.

The total value for BAM on a pro forma basis is 35-40+56 = $91-96B or ~$56-59 per share vs. $53 market price.

We should also emphasize that BAM is quickly increasing its fee-bearing AUM with several fund closings coming shortly. At the same time, insurance AUM are being deployed into Brookfield and Oaktree strategies and will start materially contributing to FRE soon. Both factors will increase Manager's valuations BEFORE the spin-off.

Summing up: despite the recent rise, BAM remains moderately attractive. Currently, the stock does not have a margin of safety as it had recently. However, save for a sharp market drop, I do not expect BAM to revisit the recent lows.

Brookfield Infrastructure

BIP is not supposed to be an outstanding investment as it pays big fees to BAM. But due to the extraordinary investment acumen of Sam Pollock and his team, its results are nothing short of outstanding. For me, BIP has delivered ~16% IRR over 9 years vs ~15% for BAM over 10 years. Relatively high yield adds to the stock allure.

Currently, BIP yields 3.5% vs 4% on average. I typically buy it at a 5+% yield (the last time it was 2 years ago). For this stock, yield is an acceptable valuation metric as it distributes almost everything left of its AFFO after paying preferred dividends and Incentive Distributions to BAM.

If we assume that the stock's return is equal to its yield plus the yield growth, BIP's expected return should be 3.5% (current yield) + 6% (current yield growth) = 9.5%. Since this result is lower than the 10% long-term return for the market, the stock may appear overvalued. However, it is not necessarily the case due to the coming commissioning of HPC ( Heartland Petrochemical Complex ).

In Q4 2021, after a prolonged battle, BIP acquired Canadian Inter Pipeline. In my opinion, it was a masterstroke. Besides various midstream assets, Inter Pipeline had been building HPC which was supposed to become its crown jewel. Now it will become a very important asset for Brookfield. Based on BIP's earnings call, HPC has already started shipments and will ramp up its capacity towards the end of 2022.

Here are some figures (all numbers are approximate): BIP, together with institutional investors from BAM's infrastructure fund, acquired Inter Pipeline for ~ CAD 8.6B paid in cash and BIPC shares. The capex required to build HPC is ~ CAD 4B.

I could not figure out what fraction of HPC is owned by BIP. It should be close to 50% but part of it might have been syndicated to institutional investors. Let us still assume it is 50%. HPC is supposed to produce ~ CAD 500M of EBITDA contracted on a long-term basis which is equal to CAD 250M at share for BIP. BIP's total EBITDA is ~ $2.5B. Hence, HPC alone should cause BIP's EBITDA to jump starting from Q1 2023 with similar consequences for FFO and AFFO. Thus, it is possible that HPC commissioning will allow BIP to raise its distributions by 7% in 2023. BIP's current stock price may already account for this coming catalyst.

Brookfield Reinsurance

This is where the action will be over the next several years. Brookfield Reinsurance will become a very important part (if not the most important part) of Brookfield Corporation. In this regard, Brookfield Corporation will be strikingly similar to Berkshire Hathaway ( BRK.A ) ( BRK.B ). Brookfield Reinsurance is supposed to be built following blueprints of Athene ( ATH ), now part of Apollo ( APO ).

Since BAMR is exchangeable into BAM, it does not have separate investment attributes. But to understand yet unexisting Brookfield Corporation, BAMR deserves detailed consideration. We may do it later in a separate post limiting ourselves to several points now.

Brookfield Reinsurance will be built using operating FFO from Manager and Invested Capital and proceeds from sales of properties currently owned by Brookfield Property Group (formerly Brookfield Property Partners ( BPY )). Currently, BAMR has $40B of insurance assets on its balance sheet and is expected to scale it up to $200-300B within several years. It will be done both organically and through M&A. BAMR closed its first big acquisition this May (American National) and as seen from our second table, started contributing to operating FFO. The required ~5.1B for this acquisition was supplied by issuing junior preferred shares to BAM (about $2.5B) and borrowing the balance.

BAMR will be contributing to operating FFO in 3 ways:

- dividends on preferred shares;

- spread between interest earned and benefits credited to policyholders and operating expenses;

- management fees on AUM

The targeted ROE is in the mid/high teens. It is surely achievable as Athene has generated ROE above 15% over many years solely from the spread. It is instructive to compare this figure with the return on real estate that we can estimate using our second table: FFO/Invested Capital = 999/31,542 ~ 3.2%. Without going into direct comparison (our estimates are too crude for that), one can imagine how profitable it will be for Brookfield to sell real estate and use the funds to scale up BAMR.

At this point, we do not have a quarterly report from BAMR to figure out important details, and the info in the previous paragraphs was deduced from press releases and the last earnings call.

Brookfield Renewable

BEP is structured similarly to BIP and is currently trading at a 3.2% yield, i.e. it is pricier than BIP. The word "renewable" appears to hold such weight that valuations do not matter any longer. The distribution growth rate for BEP is 5% over the last several years much lower than for BIP.

Those who are holding BEP today think that a) the yield is relatively high and b) renewable opportunities are enormous. From this angle, the stock seems attractive until one realizes that for retail investors all enormous opportunities are reflected in a single number - the yield growth rate which remains stubbornly mediocre. For Brookfield, on the contrary, the opportunities in renewable energy are truly enormous.

Having said that, the quarter was excellent. But it should take quite a few quarters like that to justify its current valuations.

Brookfield Business

BBU (which represents traditional private equity business) had an outstanding quarter and is scaling up quickly. The unit price jumped after the earnings release. Unfortunately, BBU, in my opinion, is not suitable for long-term holding due to the structure of its incentive distribution rights. Once the unit price exceeds its incentive distribution threshold (similar to the high watermark for hedge funds), BBU pays 20% of the market cap difference to BAM in cash. The current threshold is $31.53 while the unit trades at ~$26. So the unit still has room to rise until investors are penalized with the massive cash outlay.

Conclusion

Within the Brookfield universe, I see significant opportunities in the shares of BAM (or BAMR as it's paired to BAM) due to both ongoing business development and the coming spin-off. While these opportunities are smaller than in May-June, they are still moderately attractive.

My readers have already asked me how to trade Manager and Brookfield Corporation after the spin-off. I do not know and will not form an opinion until shortly before the spin-off. Stay tuned.

For further details see:

Brookfield Is Scaling Up - Q2 Earnings Calls And Investment Opportunities