BPYPN - Brookfield Property Preferreds: FFO Goes Negative

2023-05-08 06:00:00 ET

Summary

- We recently highlighted the potential issues for Brookfield Property preferred shares.

- They have come home to roost, and the shares are down 30%.

- We look at the Q1 2023 results and update our thesis.

BPY was long hailed as one of the powerhouses of the Brookfield Empire. It unfortunately exited the public market, leaving behind three fixed rate preferred issues that continue to trade on the NASDAQ.

- Brookfield Property Partners L.P. 6.50 PF UNIT (NASDAQ: BPYPP )

- Brookfield Property Partners L.P. 6.375 PF UNIT (NASDAQ: BPYPO )

- Brookfield Property Partners L.P. 5.75 CL A (NASDAQ: BPYPN ).

There are a lot more listed on the TSX and they are of the floating-reset variety.

Our most recent note on Brookfield Preferreds was not well received by the bulls.

Would we want to risk a near wipe-out for that little extra? Would we buy any company with a 16X debt to EBITDA for that little extra? Would we buy any company with a 16X debt to EBITDA when 62% of the debt is floating rate for that little extra? No way. The only reason this is even being debated here is because of the Brookfield Corporation ( BN ) and Brookfield Asset Management Ltd. ( BAM ) names attached to this. So sure, if that is your core logic, there is not much we can do about it.

Source: Time To Say Goodbye

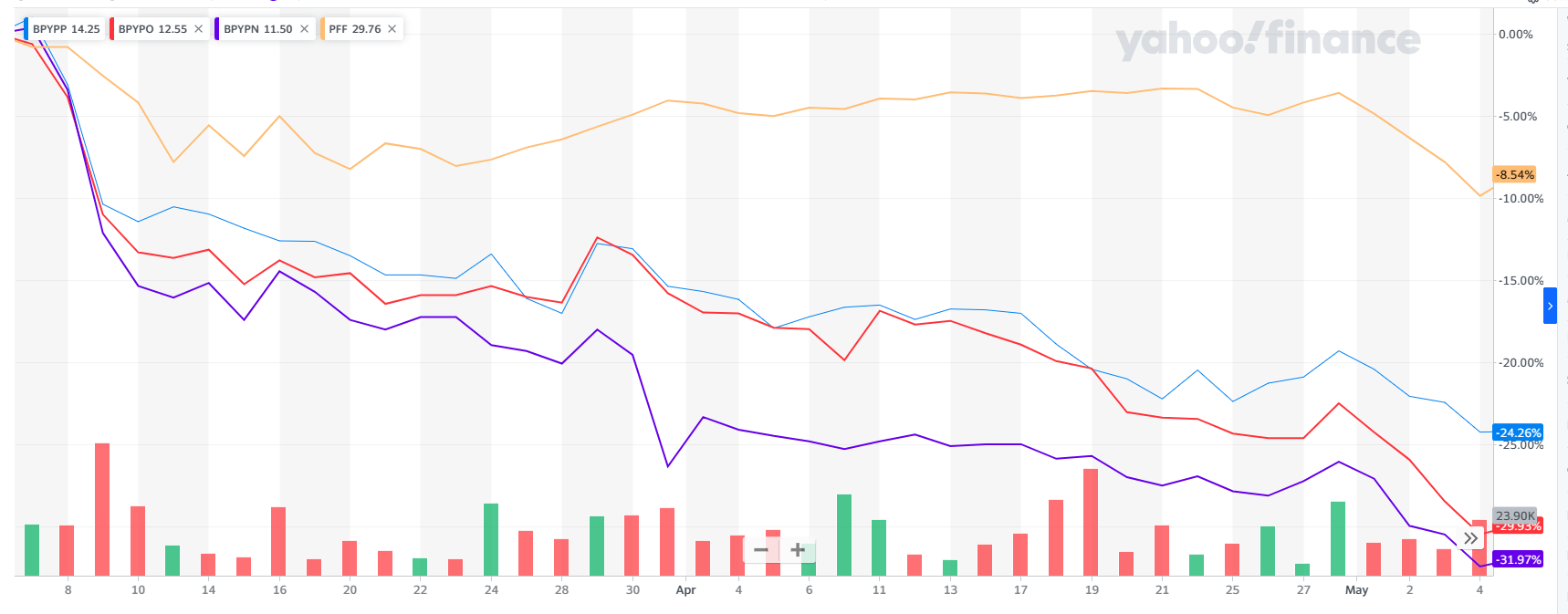

The 3 preferreds are down about 30% and have heavily underperformed iShares Preferred and Income Securities ETF ( PFF ) in the same time.

{kind=link}

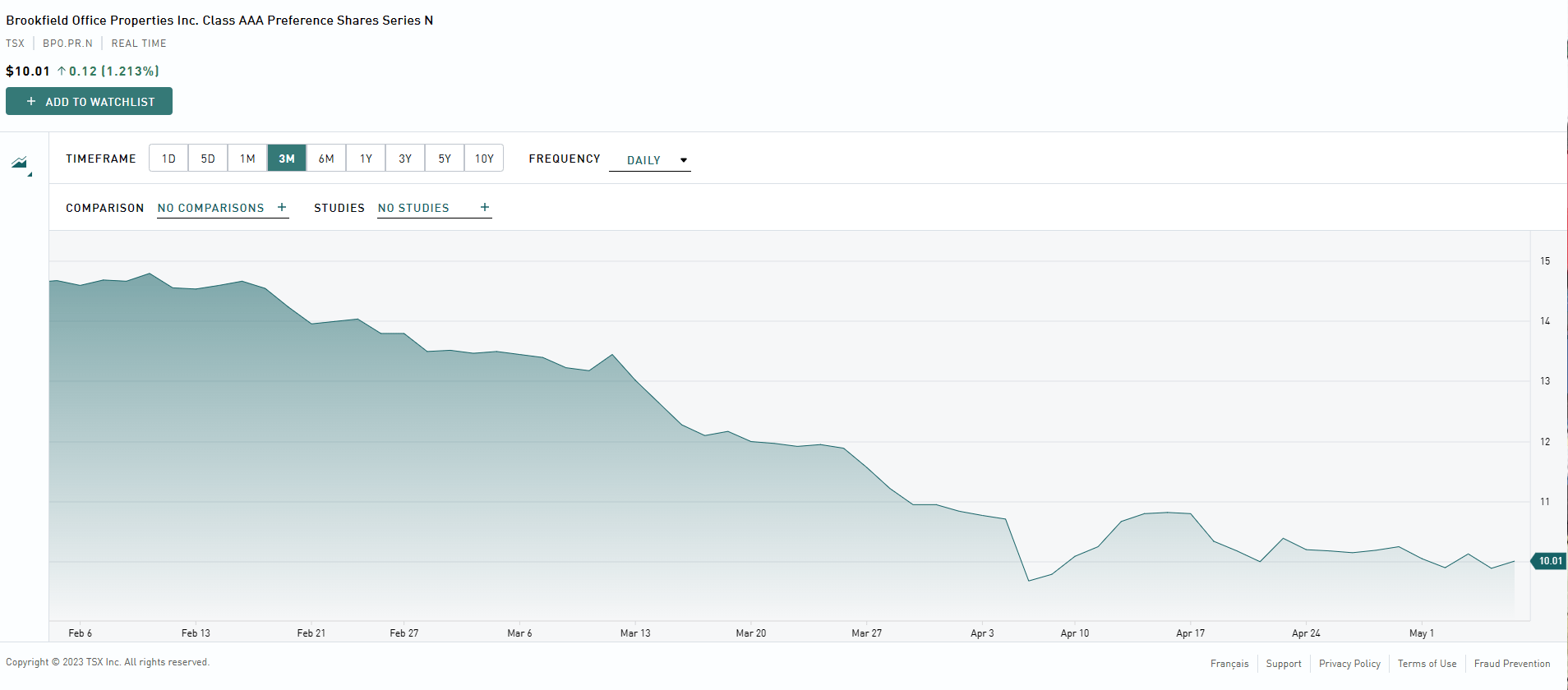

PFF has also suffered as it is filled with regional bank preferred shares. So the extreme underperformance here by these 3 is particularly notable. The TSX issues have performed in a similar manner. We are showing just one below for comparison.

{kind=link}

We look at the Q1-2023 results to update our thesis.

Q1-2023

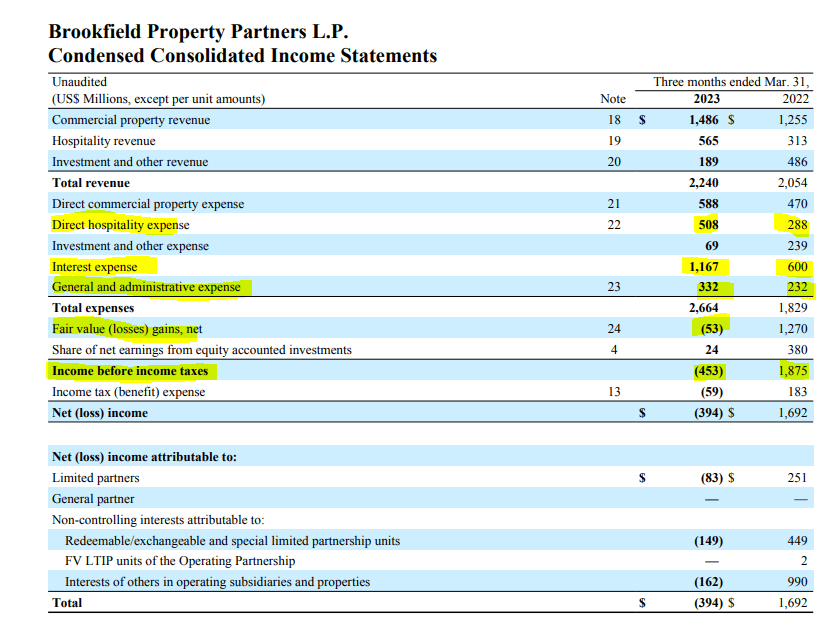

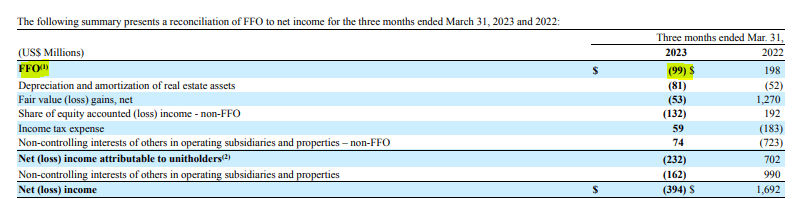

We saw the results posted just around end of day on May 4, 2023. On the income statement, you can observe that BPY posted a pretty chunky loss for Q1-2023. REIT investors might dismiss that as an accounting issue, and that logic generally holds for US REITs. But BPY, which reports under IFRS, is a different beast. Here, the loss means a lot of bad things. Let us walk you through that.

{kind=link}

You will notice above that there is no "depreciation" as we find in US REITs. Under IFRS, REITs won't post that regular real estate depreciation. In lieu of that, they will post a fair value gain or a fair value loss. This is done to keep the reported tangible book value per share as close to reality as possible. So what we saw this quarter was that even if you strip out this tiny fair value adjustment ($53 million above), BPY reported a solid loss of close to $400 million. There are 3 major drivers here. The first being the direct hospitality segment expense. In a way you can forgive them here as revenues for this segment went up smartly as well. General and administrative expenses were the second detractor, increasing by $100 million. But the key problem was the interest expense, which went up by a stunning $567 million. Of course, the main reason for this was that BPY was very heavily exposed to floating rate mortgages. But BPY also increased its borrowing by almost $10 billion in the last quarter.

{kind=link}

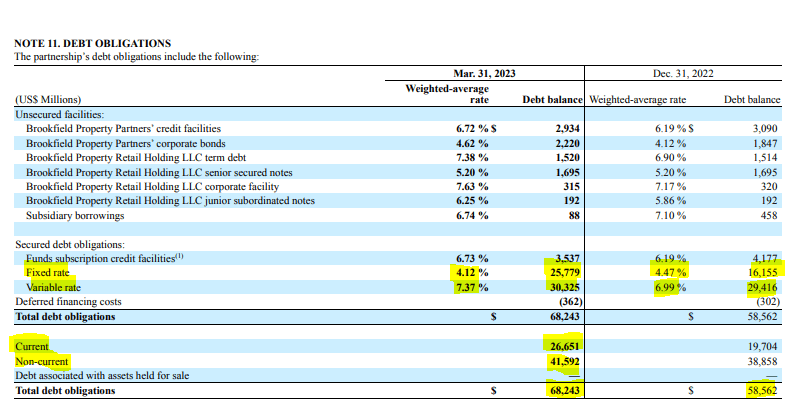

At present, $26.65 billion is owed back in one year or less and classified as "current". Last quarter this was a shade under $20 billion.

BPY 6-K

Ok so that is where the balance sheet stood? How are the properties doing? The bulk of their portfolio is office and that consolidated occupancy was down to 82.9%.

{kind=link}

You can see the drop from the March 2022 levels above. For additional comparison, note that it was at 84.7% last quarter.

BPY 6-K

Outlook & Verdict

BPY is easily the most leveraged structure we have seen in real estate. For years we have pointed this out and the bull response has been "yeah, it is all non-recourse." The bad news for the bulls is that it is not all non-recourse. The good news for the bulls is that they won't have to wait very long to find out whether that non-recourse portion will save the day or not. Current interest coverage is already under 1.0X. Funds from operations ((FFO)) is also negative.

{kind=link}

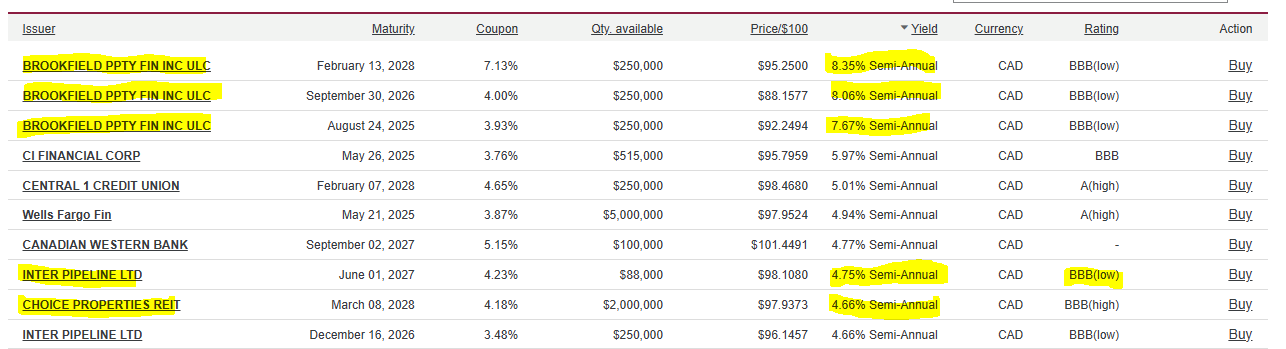

The variable interest expense is about to be jacked up in Q2-2023 as the additional hikes flow through. $26 billion needs to be refinanced within 1 year. Over $40 billion within two years. If these all sound doable because the mantra is "non-recourse", then we have to marvel at your optimism. The bond market is beginning to notice and even though bulk of the debt is non-recourse, there is still a lot of recourse debt. BPY's yield is the highest we could find on the Canadian markets for investment grade debt.

{kind=link}

Note the divergence from Inter-Pipeline which is rated the same BBB-LOW. Also note divergence form Choice Properties REIT ( CHP.UN:CA ), a REIT with about half the leverage as BPY. Market is clearly beginning to worry here as the debt roll approaches. The 12.5% plus yields on the fixed rate preferreds look fantastic to the investor seeking yield. On the TSX side, the nearest one to be reset will be Brookfield Office Properties Inc. CL AAA PF SER T ( BPO.PRT:CA ). With a Government of Canada 5-year bond rate plus 3.16%, the yield will reset in December to over 12% on the current price. Those are seriously tempting for the "income investor". They all also look like they are in the ICU at present as fundamentals are horrible. We think office occupancies will trend lower in 2023 and the negative FFO will persist. All refinancings completed in 2023 will be at a higher interest rate than what BPY is currently paying. We know that the preferred dividends are cumulative but in this case we see them going and never coming back.

DBRS still continues to rate them (BPY, not their preferreds) at BBB-Low with the hilarious notion that they might get an upgrade if they reach 13X Debt to EBITDA.

DBRS Morningstar would consider a negative rating action should BPY's operating environment fail to improve as expected such that total debt-to-EBITDA remains above 16.0x, on a sustained basis, all else equal, or if DBRS Morningstar changes its views on the level and strength of implicit support provided by BAM. On the other hand, DBRS Morningstar would consider a positive rating action should DBRS Morningstar's outlook for BPY's total debt-to-EBITDA improve to 13.0x or better.

Source: DBRS

Our take is that we are probably looking at an 20X debt to EBITDA by the fourth quarter of this year. We are taking our Strong Sell Rating and upgrading it here to just a "Sell" to account for more appropriate pricing for the risks.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Brookfield Property Preferreds: FFO Goes Negative