ARGO - Brookfield Reinsurance: Smart Capital Raise To Fuel Growth But Skepticism Warranted

2023-12-04 17:47:55 ET

Summary

- Brookfield Reinsurance operates a capital solutions business providing insurance and reinsurance services with $47bn in assets under management.

- The company is part of the highly successful Brookfield Corporation.

- It is growing fast, and raising capital from its parent very efficiently.

- Business strategy is not clear and valuation compared to peers is not compelling.

The company

Brookfield Reinsurance Ltd. ( BNRE ) operates a leading capital solutions business providing insurance and reinsurance services to individuals and institutions. Through its operating subsidiaries, Brookfield Reinsurance offers a broad range of insurance products and services, including life insurance and annuities, and personal and commercial property and casualty insurance.

BNRE has grown fast, and now has assets under management of $47bn, housed in companies and subsidiaries with an A- rating or better.

Brookfield Re is a 100% subsidiary of Brookfield Corporation ( BN ) and it's important for investors to understand how BNRE fits into the overall Brookfield landscape.

Brookfield Group Structure

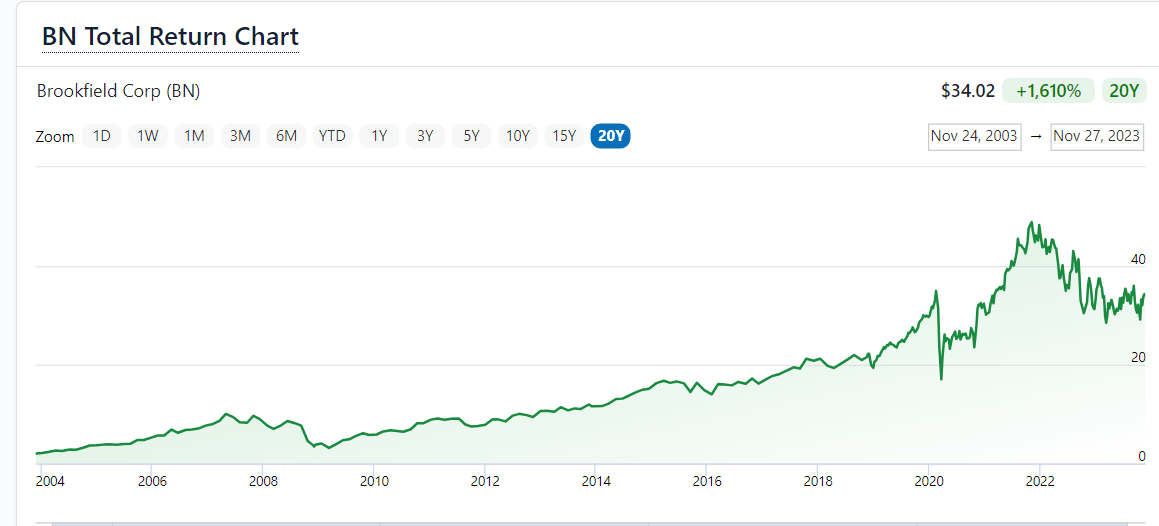

Brookfield Corporation is a much revered Asset Management and Alternative Asset company, helmed by legendary Canadian investor, Bruce Flatt. Long terms performance for investors has been strong, with a 20-year return of 1600%.

{kind=link}

The peak return at the end of 2021 was as much as 2200%. The steep drop-off in the chart above highlights one of the challenges for investors in Brookfield. The group is quite complex in structure, and the management team is very active in capital management and corporate restructuring. It's not easy to access like for like share price performance.

In 2021, Brookfield took Brookfield Property Partners ( BPY ) private, which significantly reduced the disclosure requirements of that part of the business. This proved timely, as the commercial real estate market has been under significant stress, resulting this year in some reported $1bn of property loan defaults from Brookfield.

Beginning of 2023, Brookfield trading under the ticker ( BAM ) spun off 25% of its asset management business, with the asset management business taking up the BAM ticker, and the remaining 'hard' assets under the ownership of the new 'Brookfield Corporation' brand ((BN)) which owns the interests in property, infrastructure, renewables and the insurance business. This restructuring and asset disposals need to be factored into evaluating the group performance over time.

It's not easy to piece together the new structure from the various Brookfield Group reports. I have compiled the overview below.

Author from BN reporting

Brookfield Re

Brookfield Re is 100% owned by Brookfield corporation, and the shares are exchangeable for BN shares on a 1-1 basis. The details of that arrangement are shown on the Brookfield website.

Brookfield Insurance solutions is one of the three core business areas in the first tier of the new Brookfield Structure.

The business is described on the Brookfield website. Brookfield Re is positioned as a capital solutions provider and asset manager, active in Life Insurance and Annuities, Personal and Commercial Property/Casualty Insurance and Reinsurance solutions with $46 bn of assets under management.

The company is domiciled in Bermuda, and organises its activities between Direct Insurance, Reinsurance and Pensions Risk Transfer [PRT].

BNRE Performance.

Shareholders to date have not been rewarded, with a reduction in share price of about 60% since launch.

The business is showing rapid growth, both organically and via acquisitions.

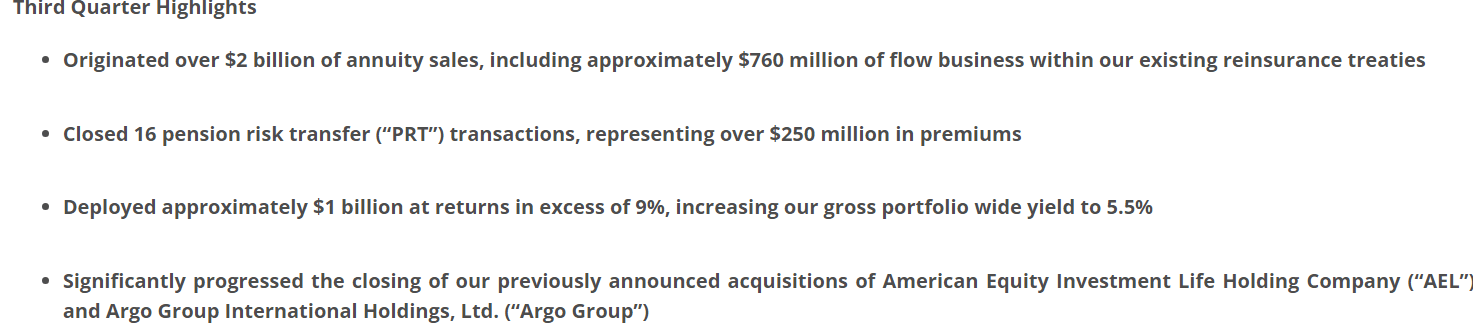

Third quarter results were released on November 9th, and show strong growth in assets.

{kind=link}

The business highlights were dominated by the acquisition of American National, a Texas based Property Casualty Insurer, but also rapid growth in the Annuity and PRT business, and a significant tailwind from repositioning of the asset portfolio. Net income however was lower, which is attributed to mark to market losses on the investment.

{kind=link}

Interestingly, the accounting basis was changed from IFRS to US GAAP, presumably to allow easier consolidation of American National which will make peer comparison with other players in the PRT and annuity space, like Legal & General ( LGGNY ) and Manulife ( MFC ) more difficult going forward.

As reported in Reuters , Brookfield agreed to acquire Argo Insurance, ( ARGO ) a NYSE listed Property/Casualty Insurer for $1.1bn in a transaction expected to close in the 4th Quarter.

As shown by Y charts, ARGO has been a poor performer, producing negative net income and suffered a peak to trough share price decline of 66%.

Yes, ARGO was acquired at a low valuation compared to mid 2021 levels, but it is not clear how Brookfield will return this business to profitability. It is possible that BNRE sees the ARGO assets that support their insurance liabilities as good value. The offer is only a slight premium to ARGO market cap, and ARGO is trading slightly below book value. Book value however requires the liabilities to be adequately reserved, and I for one am skeptical about the reserving levels of poorly performing US P&C Insurers. 10% arbitrage seems a poor risk/return trade to me.

All this growth required capital, and Brookfield Corporation has stepped up, by offloading $2.1 bn of real estate and other assets to BNRE in exchange for newly issued class C shares. My interpretation is that BN has pumped the BNRE balance sheet by $2.1 bn of commercial real assets from the privately held Brookfield Real Estate at current book value, diluting BNRE shareholders by issuing new shares in exchange. The BN ownership of these assets drops from 100% to their retained BNRE share count as a % of total BNRE shares. True, BN and BNRE are 'paired' listings, so theoretically BNRE shareholders can convert back, and BN state that as a result the BNRE shareholders are not diluted - I, for one, am left scratching my head to put it all together.

For BNRE, under US GAAP accounting, the mark to market value of their asset base will stabilise, as BN has control of the book value of the real estate assets, and solvency will increase to enable them to fund new insurance liabilities.

Next up, Brookfield launched an Exchange offer, which invited BN shareholders to exchange their BN shares for BNRE shares. The results of this offer were just published. 32.5m shares will be exchanged, with new class A shares in BNRE issued, raising a further $1.2bn of capital for BNRE, at zero cost to BN.

All in all, I am reminded of the old shell game in which sleight of hand confuses gamblers. It is clever capital management for sure, but is it in the long term interests of BNRE shareholders?

Corporate Shell Game (familyllb.com)

Brookfield Re future outlook.

Other than the closing of the Argo transaction, BNRE do not clearly articulate much of a business strategy. Investors are left with the following statement .

"Upon closing of the Argo Group and AEL transactions, we will have over $100 billion of assets across a diversified platform of life, annuities and P&C. With the strong, complementary distribution channels between the companies and our existing platform, we have a credible path to meaningfully grow our insurance assets organically, and by leveraging Brookfield's investment capabilities, these assets will be redeployed at attractive risk-adjusted returns, driving increased spread earnings and delivering significant returns to our shareholders.

This focus on Assets Under Management rather than underwriting profitable business is reminiscent of the 'Total Return Reinsurer' model which has been operated by Bermudian Reinsurers like Greenlight Capital ( GLRE ) which have not proved to create shareholder value. Other total return reinsurers like Third Point Re and Watford Re no longer exist as standalone entities."

Data by YCharts

Valuation.

Given the generally opaque reporting, and complex business model, it seems hard to value BNRE. Seeking Alpha Quant doesn't offer coverage, nor does Morningstar. It is quite hard to find any in depth analysis of the company.

I think price to book value is a good way to look at this, and as can be seen, BNRE does not offer compelling valuation compared to peers. I chose Manulife ((MFC)) as a peer in the Canadian Life and Annuities space, and GLRE as a Bermudian total return peer.

As you can see, BNRE trades at around book value, at a significant premium to GLRE, and a slight discount to MFC. Given that MFC has a long track record of profitable growth, and provides detailed disclosure of its strategy, I see a 10% premium in price to BNRE as entirely justified. Readers might be interested in my recent article on MFC. All in all, I don't know enough to invest in, or against BNRE. My position is to avoid BNRE for now. I am however long both BN and BAM.

Risks to my thesis.

My overall position on BNRE is one of skepticism. I do not like to invest in a business that I don't understand, and while I understand the Insurance and Reinsurance business very well, BNRE business strategy and disclosure is not clear enough for me to form a confident view. The risk to me is that BNRE manages to dramatically outperform companies that I do invest in. As the valuation gap is not compelling - I am prepared to take that risk.

Summary

Brookfield is a great value creator, but value creation is not even between all the entities.

The group is managed with great cleverness, but with complexity and opacity.

BNRE has been smartly capitalised, but I question the strategy and their focus on managing assets rather than underwriting quality.

My position is to follow BNRE progress, but to avoid the stock for now.

For further details see:

Brookfield Reinsurance: Smart Capital Raise To Fuel Growth But Skepticism Warranted