BRW - BRW: Top Performing Credit Hedge Fund In A CEF Structure

Summary

- BRW is managed by Saba Capital Management, one of the best credit managers in the world.

- The fund was able to navigate a tough 2022 with a 0.3% total return, vastly outperforming peers.

- Although I have concerns about the fund's 12% managed distribution rate, it could simply be Saba arbitraging the fund's discount to NAV.

- I would keep the BRW on my radar as the fund looks like one of the best positioned to take advantage of any credit distress if the economy falls into a recession.

The Saba Capital Income & Opportunities Fund (BRW) is a credit hedge fund managed by Saba Capital Management wrapped up in a closed-end fund structure. It pays an attractive 11.9% trailing 12 month distribution. However, I have concerns the distribution rate may be depleting NAV, although that could be the manager's goal all along.

BRW has managed 2022 superbly, returning 0.3% in total returns while other credit CEFs suffer double digit losses. I believe the fund is definitely worth monitoring, as Saba Capital Management is one of the best credit managers in the world.

Fund Overview

The Saba Capital Income & Opportunities Fund is a closed-end fund ("CEF") that aims to provide high current income and capital appreciation. The BRW fund has $367 million in net assets.

The BRW fund was formerly known as the Voya Prime Rate Trust ("PPR"), but after a lengthy proxy battle with activist investor Saba Capital, the fund changed its name to the Saba Capital Income & Opportunities Fund and installed Saba Capital Management as the fund's investment advisor as of June 2021. Other authors have written about the proxy battle, so I will not rehash all the details in this article.

Who Is Saba Capital

Saba Capital Management is an Investment Advisor/Hedge Fund Manager launched in 2009 as a spin-out of Deutsche Bank's proprietary credit trading group. It is led by Boaz Weinstein , one of the most well-known hedge fund managers in the past decade. Mr. Weinstein was the youngest ever managing director at Deutsche Bank, and Saba Capital was famously on the other side of J.P. Morgan's huge 'London Whale' trading losses in 2012. Saba Capital was named Risk.net's hedge fund of the year in 2021 for successfully navigating the COVID crisis and its aftermath.

Strategy

While Saba maintained BRW's primary focus on credit investments, the fund also made important changes to its investment mandate, allowing greater flexibility for the investment manager. Notably, the new mandate allows the BRW fund to invest in warrants, engage in short-selling, and invest in other investments where Saba believes the risk/reward is favorable. In effect, the BRW fund is now a credit focused 'hedge fund' wrapped in a CEF vehicle.

Portfolio Holdings

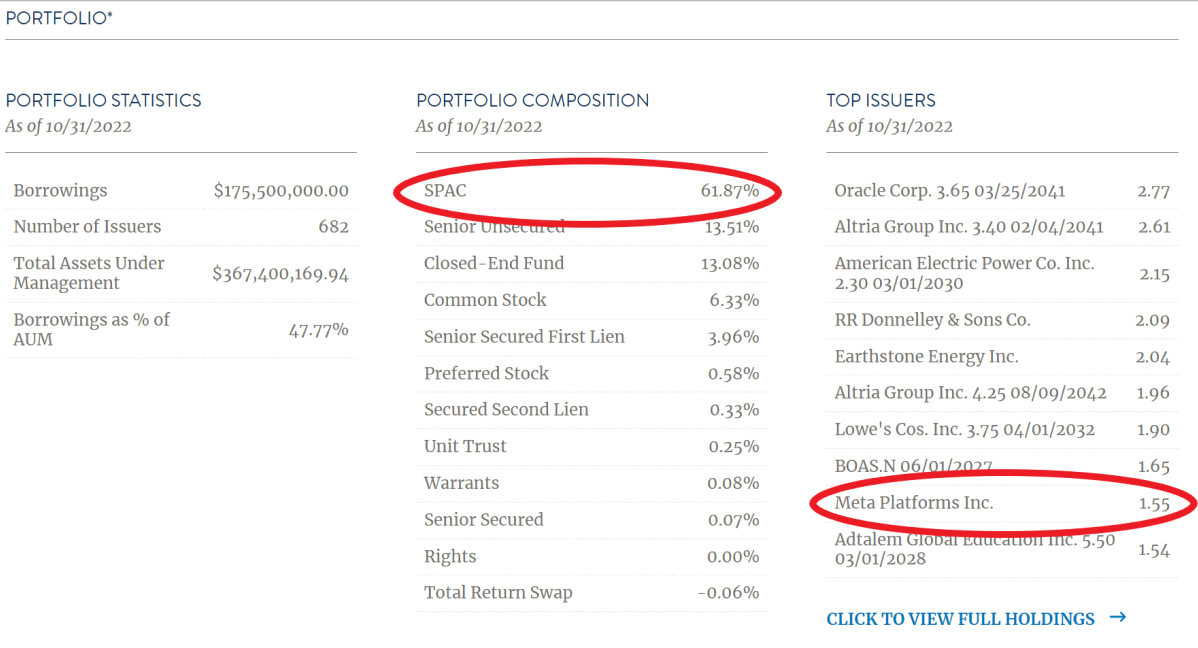

The change in BRW's investment mandate is most noticeable when we look at the fund's portfolio composition as of October 31, 2022 (Figure 1).

Figure 1 - BRW portfolio allocation (sabacef.com)

{kind=link}

From figure 1 above, we can see the BRW fund was 62% invested in SPACs as of October 31, 2022. It also held notable equity investments like Meta Platforms that are typically not found in credit CEFs.

Importantly, Saba's investment in SPACs appears to be a calculated arbitrage bet, providing gains with limited downside. In contrast to aggressive SPAC investment strategies pursued by some managers that buy 'disruptive companies' out of the de-SPAC process, BRW appears to be buying pre-deal SPACs that are trading at a discount to their cash redemption values as they near the end of their 2-year search mandates.

If the SPAC finds a merger candidate, investors like BRW have the opportunity to get a 'free look' at the deal and either vote for the deal or choose to receive their cash redemption value. If the SPAC cannot find a merger candidate, it winds up and cash is returned to shareholders. Typically, the yield to 'maturity' on these SPAC opportunities is better than cash yields and is a safe haven when markets are tough.

Returns

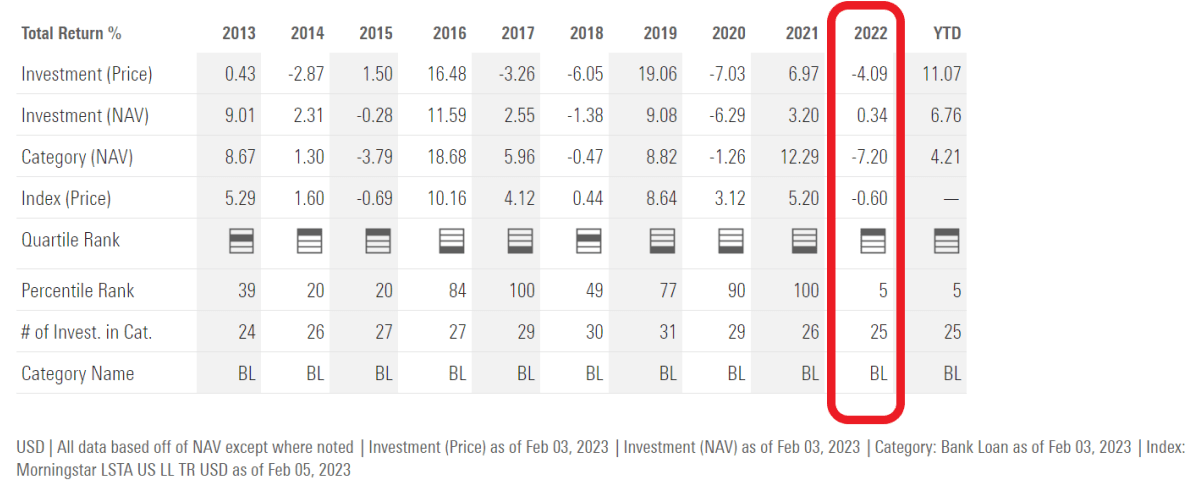

It is hard to argue with Saba's investment process, as the BRW fund ended 2022 with a 0.3% gain, outperforming 95% of its peers, as many credit-focused funds lost substantial sums during the Fed's interest rate hikes in 2022 (Figure 2).

Figure 2 - BRW annual returns (morningstar.com)

{kind=link}

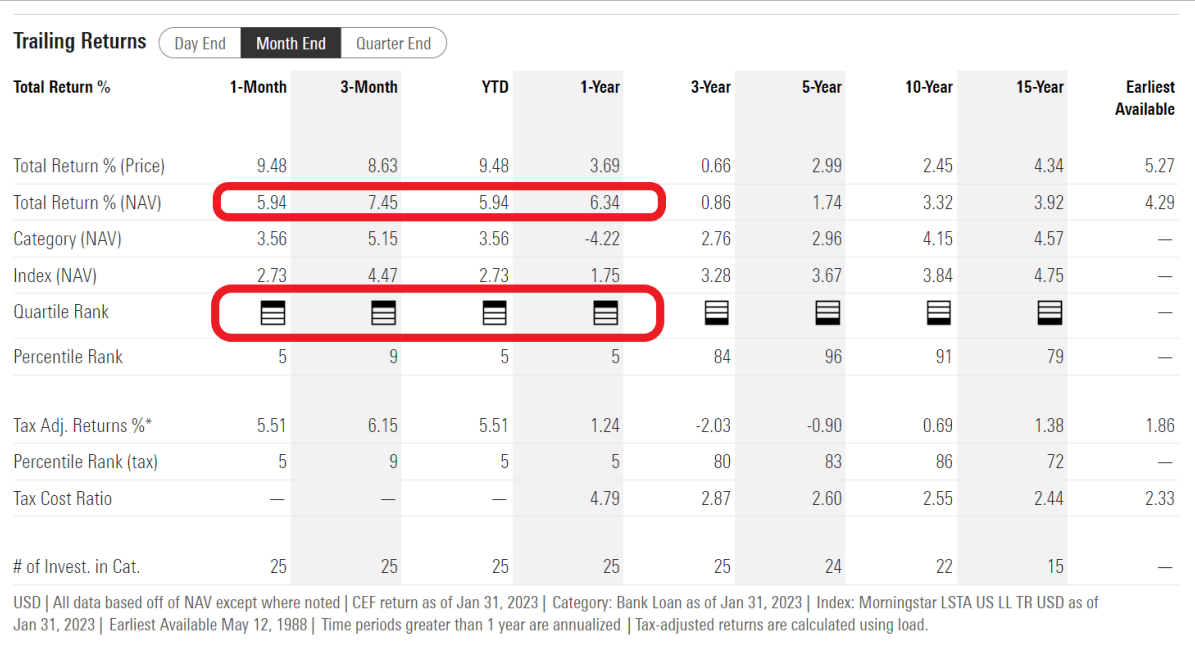

While it has only been 18 months since Saba took over management of the fund, early indications are that the fund's investment results have been dramatically improved as the fund is ranked 1st quartile on the 1Yr and YTD time frame, a steep improvement from 4th quartile on 3/5/10/15 Yr time frames (Figure 3).

Figure 3 - BRW historical returns (morningstar.com)

{kind=link}

Distribution & Yield

When Saba took over management of the BRW fund, it also implemented a 12% managed distribution yield, based on an average NAV of the prior month. In the past twelve months, BRW's distribution has amounted to $1.00 or a 11.9% distribution yield (Figure 4).

Figure 4 - BRW distribution (Seeking Alpha)

{kind=link}

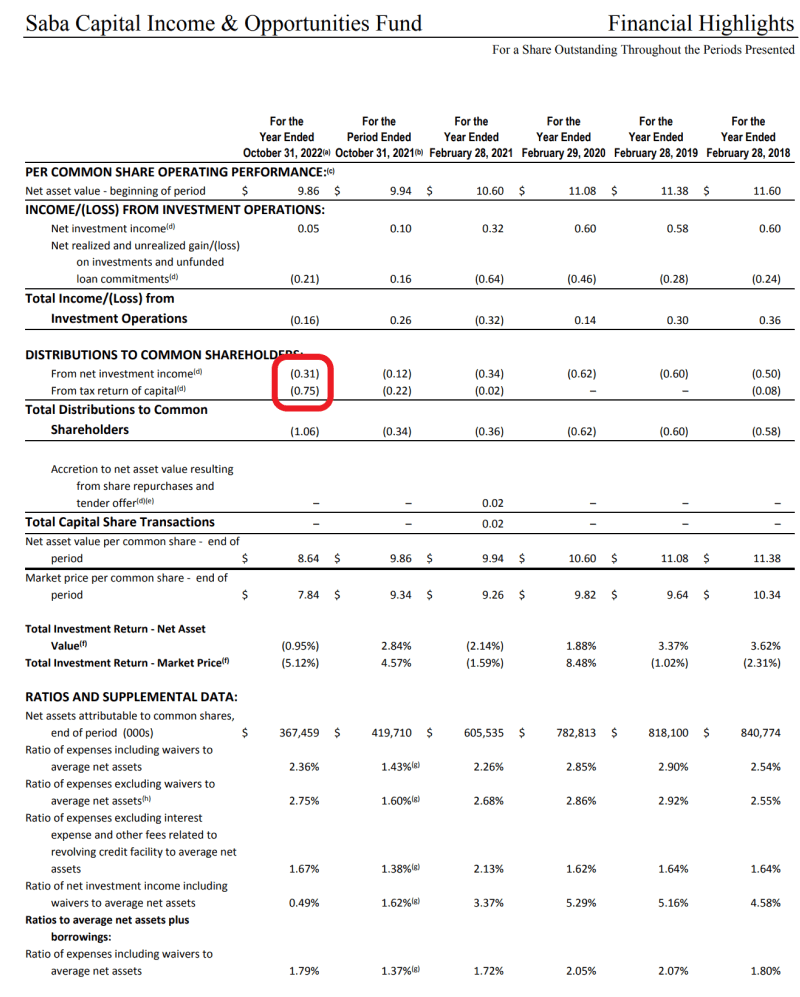

Investors should note that BRW's average annual total returns have been below its distribution rate, so it has not 'earned' its distribution. Instead, the distribution is funded out of NAV as return-of-capital ("ROC"). In fiscal 2022, 71% of the fund's $1.06 in distributions was funded out of ROC (Figure 5).

Figure 5 - BRW financial summary (BRW 2022 annual report)

{kind=link}

Regular readers know that I am usually critical of funds that cannot fund their distributions from earnings - I call these 'return of principal' funds as they give off the mirage of paying a high distribution, but they are simply funding the distribution by liquidating the fund's NAV. I believe this criticism is appropriate in BRW's case, at least until proven otherwise.

Distribution Arbitraging NAV Discount

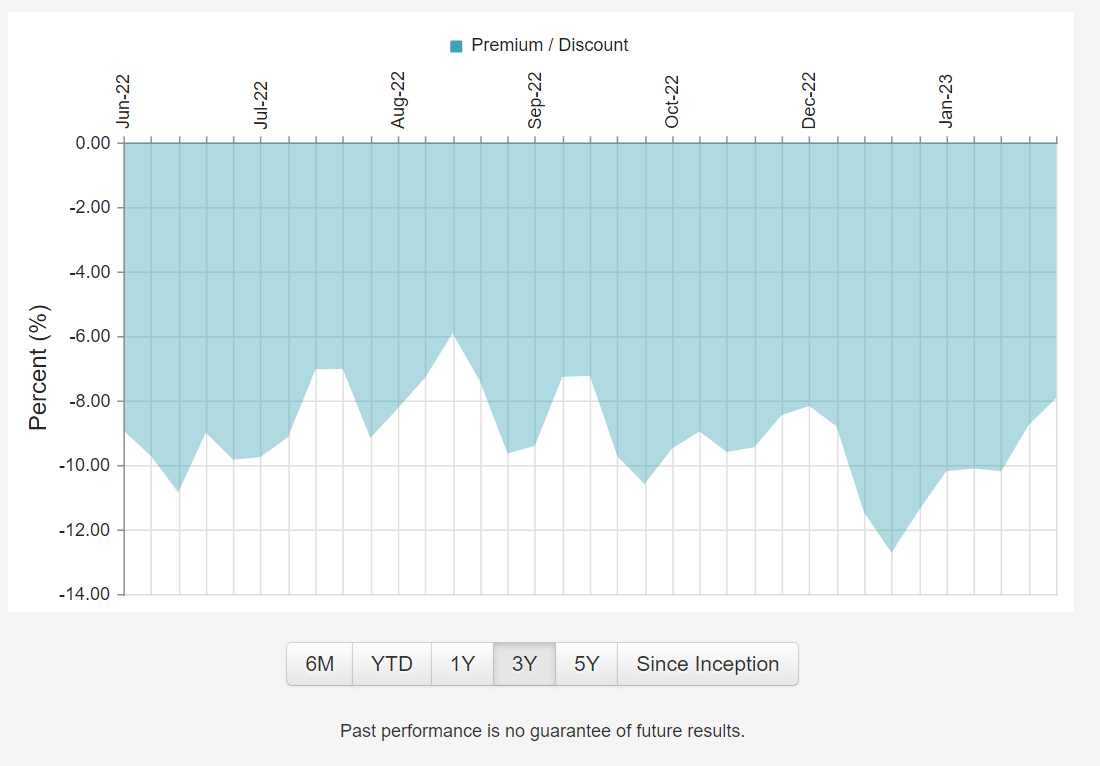

However, it must be mentioned that BRW is a non-traditional CEF run by an activist investor group. So another way to think about BRW's distribution is that the fund is arbitraging the steep discount to NAV of the fund's units through paying a distribution that is mostly funded out of ROC (Figure 6).

Figure 6 - BRW trades at a discount to NAV (cefconnect.com)

{kind=link}

In effect, investors can buy $1 of assets for $0.92, and have that $1 returned through the high distribution rate (provided the $1 in assets does not get turned into $0.80 by poor investment performance).

Fees

The BRW fund charged a relatively high total expenses of 2.36% of net assets in fiscal 2022. This is inclusive of fee waivers. Excluding fee waivers, the total expense ratio would have been 2.75%.

Conclusion

The BRW fund is a credit hedge fund managed by Saba Capital Management wrapped up in a CEF structure. It pays an attractive 12% of NAV managed distribution that has yielded 11.9% in the past twelve months.

I have concerns regarding the high distribution rate relative to the earnings power of the fund. However, viewed another way, the high distribution rate funded by ROC could simply be the manager arbitraging the significant discount to NAV of the fund's shares.

BRW has managed 2022 superbly, returning 0.3% in total returns while other credit CEFs suffer double digit losses. I believe the fund is definitely worth monitoring, since the manager, Saba Capital, is one of the best credit managers in the world.

For further details see:

BRW: Top Performing Credit Hedge Fund In A CEF Structure