BRW - BRW: Unique CEF With Some Good Qualities But Distribution Looks Unsustainable

2023-04-24 17:07:49 ET

Summary

- Investors today are desperately in need of additional sources of income simply to maintain their lifestyles in the face of the highest inflation that we have seen in forty years.

- Saba Capital Income & Opportunities Fund invests in a portfolio of SPACs, CEFs, and other things that are intended to provide a very high yield.

- The BRW closed-end fund's portfolio is surprisingly conservative and should hold up better in a recession than the portfolios of most other funds.

- The fund pays out 12% of its NAV, which is nice but does not appear sustainable.

- The fund is trading at a discount to its net asset value.

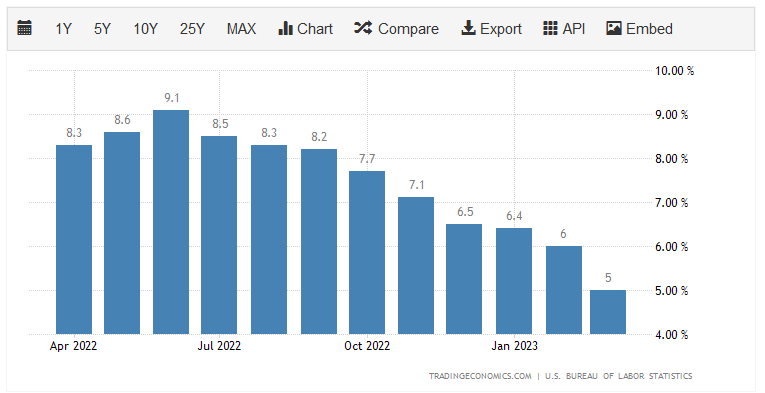

It seems essentially certain that one of the biggest problems facing the average American today is the incredibly high rate of inflation that has been dominating the economy. The cost of living has been rising at the highest rate that we have seen in more than four decades, as evidenced by the consumer price index. This index has posted at least a 6% year-over-year increase in eleven of the past twelve months:

{kind=link}

The decline in the index in recent months has largely been caused by falling oil prices, which could mean that inflation will begin to increase in the near future. As I discussed in a recent blog post , energy prices are positioned to climb over the summer, which will result in rising shipping costs and start pushing up the price of everything that we buy. This will have a major impact on consumers that have already suffered from 24 straight months of declining real wages and have in some cases been forced to take on second jobs or enter the gig economy just to obtain the money that they need to pay their bills or finance their lifestyles. In short, everyone may soon be in need of more income just to keep their standard of living stable.

As investors, we are certainly not immune to this as we also have bills to pay and a desire for fun "spending" money. We do not necessarily have to resort to second jobs in order to obtain this money, though. This is because we can put the cash that we already have to work for us as a way to earn an income. One of the best ways to do this is to purchase shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are admittedly not particularly well followed in the investment media or by financial professionals, which is unfortunate as this limits our ability to obtain information about them. That is unfortunate, as these funds have some advantages over open-end mutual funds and exchange-traded funds ("ETFs"), as they are capable of using certain strategies that boost their effective yields well beyond that of any of the underlying assets.

In this article, we will discuss the Saba Capital Income & Opportunities Fund ( BRW ), which is a closed-end fund that can be used to earn an income. This fund is fairly good at this task, as its 12.73% yield is one of the highest available in the market. However, any time a yield reaches this level, it is a sign that the market expects that there will be a near-term cut, so this is something that we should certainly keep in mind as we analyze the fund. Let us investigate and see if this fund could be a good addition to your portfolio today.

About The Fund

According to the fund's webpage, the Saba Capital Income & Opportunities Fund has the stated objective of providing its investors with a high level of current income. This is somewhat surprising considering that this is primarily a common stock fund, although it also includes fixed-income securities. We can clearly see this in the fact that 86.98% of the fund is invested in common stock:

CEF Connect

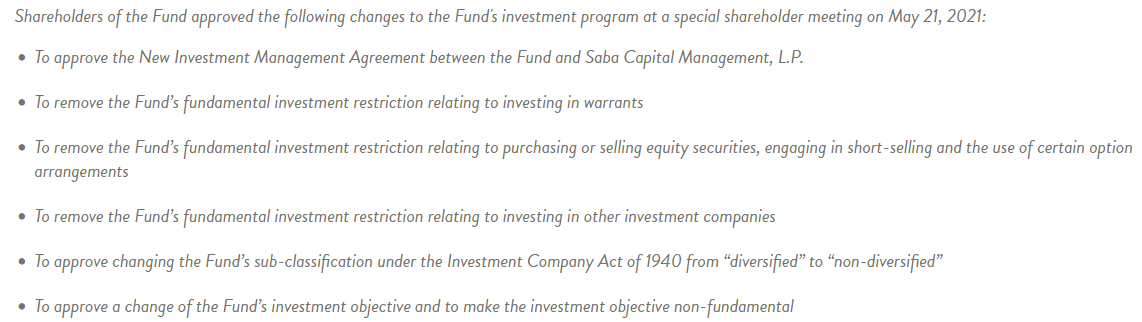

This is very different from what we would expect, as the name of the fund would ordinarily imply that the fund would invest in debt securities. That was, in fact, originally the case as this fund used to be the Voya Prime Rate Trust until Saba Capital Management took over the fund's management in 2021. The fund was, at that time, a floating-rate debt fund that invested in senior secured loans. However, a number of changes were made to the fund at a shareholder meeting in 2021:

{kind=link}

These changes almost completely changed the fund from a floating-rate debt fund into a hybrid stock and bond fund. The fund states this on its webpage thusly:

"The fund will invest in debt and equity securities of public and private companies, which includes, but is not limited to, closed-end funds and special acquisition companies."

Thus, the fund was transformed into an almost brand-new fund from its previous incarnation. There are some advantages to the new strategy though, as being able to invest in common stock can provide the fund with much higher potential total returns. However, common stock is also a bit riskier as we saw over the past year. This was especially true when we compare common stock to senior floating-rate loans, as the latter security was almost flat over the past year. Thus, the fund's former strategy probably would have done much better than its new one over the past year or so. We are long-term investors though, and common stocks are almost always the place to be for long-term investment.

With that said though, this fund does not invest in the same common stocks as most equity closed-end funds do. Rather, a sizable portion of the common stocks in the portfolio is actually special acquisition companies or other closed-end funds. The fund hints that it will invest in these entities in the description that was provided earlier, but its actual position in such companies is much larger than we would expect:

Saba Capital

The fact that 40.75% of the fund's assets are invested in special acquisition companies is particularly surprising. These companies became incredibly popular during the free-money bubble peak of 2021 as a way for private companies to lose their luster. However, now that the Federal Reserve has started raising interest rates and made it much easier to obtain a reasonable yield from a portfolio. This caused special-purpose acquisition companies to lose much of their former luster. They are still capable of delivering solid long-term returns by purchasing the right private company though, but I will admit that I would rather see the allocation to these entities be much lower and the weightings to everything else in this portfolio be much higher. That would help with the fund's income as well since special-purpose acquisition companies do not typically offer much in the way of yield.

The fund does appear to have a marked preference for high-yielding assets. We can see this by looking at its sector weightings. Here they are, excluding the closed-end funds and special-purpose acquisition companies that may not have a specific sector:

Saba Capital

As we can see here, the fund is more exposed to tobacco and utility companies than anything else. This confirms my statement about a focus on high-yielding assets, as companies in these two sectors do tend to have higher yields than most others. The other sector that tends to have very high yields is oil & gas, so the fund's relatively insignificant weighting to that sector is a bit disappointing. This is doubly true as the traditional energy sector significantly outperformed every other sector during 2022. Thus, if the fund had a higher weighting to this sector, it probably would have had a better return over the past year as well as more income. However, it is possible that this weighting has started increasing again now that oil prices are beginning to rebound following the fall that we saw in the second half of last year.

The emphasis on tobacco and utilities is also nice to see because these are defensive sectors. Generally speaking, people prioritize utility bills ahead of discretionary spending, so utilities tend to be stable regardless of conditions in the macroeconomic environment. Tobacco is an addictive product that addicts will normally purchase even if they cannot really afford it, so these companies tend to deliver a relatively stable performance regardless of economic conditions as well. This could be quite nice today considering that there are a growing number of signs that the United States will enter a recession during the second half of this year. Even if that does not happen, the rising cost of living has been straining the budgets of many average Americans, as I pointed out in a recent blog post . Thus, people are probably going to be prioritizing spending and it is likely that they will prioritize spending on products from these companies ahead of things like purchasing a new car or smartphone. Thus, the fund is probably reasonably well invested given the current environment.

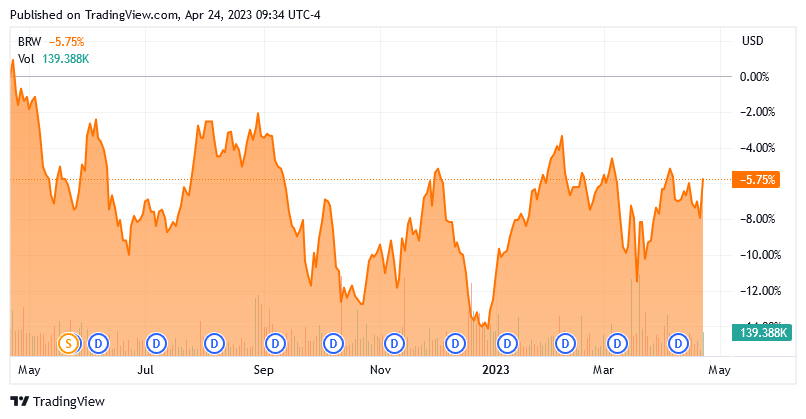

The Saba Capital Income & Opportunities Fund actually has held up pretty well over the past year. As we can see here, the fund's market price is only down 5.75% over the past year:

{kind=link}

When we add the fund's distribution yield to this, it actually delivered a positive total return over the period:

{kind=link}

This was much better than the S&P 500 Index (SP500), which was down 5.90% over the same period. Thus, the fund's strategy does appear to be working. It remains to be seen how well it will do over the long term though since the fund has only been using its current strategy since 2021. Thus, we will have to wait and see how well it does in the long term. I will admit that I am remaining cautious about it because special-purpose acquisition companies, or SPACs, have not been tested during regimes in which money is more difficult to come by, and these entities account for the majority of the fund's holdings.

Leverage

In the introduction to this article, I stated that closed-end funds like the Saba Capital Income & Opportunities Fund have the ability to employ certain strategies that have the effect of boosting their yields beyond that of any of the underlying assets. One of the strategies that the fund employs is the use of leverage. Basically, the fund borrows money and then uses this borrowed money to purchase shares of special-purpose acquisition companies, closed-end funds, and other assets. As long as the yield that it obtains from the purchased assets is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably higher than retail rates, that will usually be the case.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to an excessive amount of risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason. The Saba Capital Income & Opportunities Fund, fortunately, fulfills that requirement as its levered assets only account for 32.12% of its assets under management. Thus, the fund seems to be running with a reasonable balance between risk and reward.

Distribution Analysis

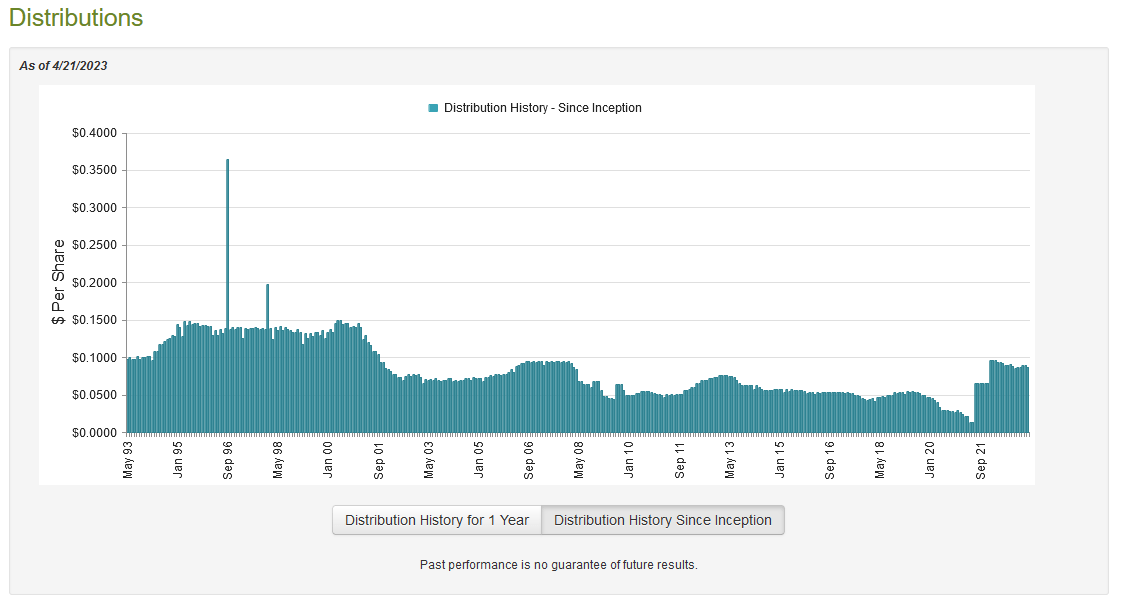

As mentioned earlier in the article, the primary objective of the Saba Capital Income & Opportunities Fund is to provide its investors with a high level of current income. In order to achieve this, it invests in closed-end funds that have remarkably high yields along with special purpose acquisition companies that typically deliver very high total returns after they complete the purchase of a company, which can then be paid out to the fund's shareholders. In addition to this, the fund employs leverage to boost the effective yield of the portfolio. We might therefore assume that this fund has an impressive yield, which is certainly the case. The fund pays a monthly distribution of $0.0870 per share ($1.044 per share annually), which gives it a 12.73% yield at the current price. The fund's distribution tends to vary considerably from month to month:

{kind=link}

This variable distribution may be concerning to those investors that are seeking a stable and secure source of income to use to pay their bills or otherwise finance their expenses. It is not particularly surprising though as this fund has a managed distribution policy, which is discussed on its webpage :

"As part of the managed distribution plan, the fund will make monthly distributions to shareholders at an initial annual minimum fixed rate of 12.00%, based on the average monthly NAV of the fund's common shares. The fund will calculate the average NAV from the previous month based on the number of business days in that month on which the NAV is calculated. The distribution will be calculated as 12.00% of the previous month's average NAV, divided by twelve."

Thus, the fund's distribution will vary considerably based on the fund's performance and average assets during any given month. As such, investors that are seeking a stable source of income probably will not find it here. However, the fund's policy also ensures that any investor should receive a very high yield on a consistent basis. As is always the case, though, it is critical that we ensure that the fund can actually afford this distribution, as we do not want to be the victims of a distribution cut that both reduces our incomes and almost certainly causes the fund's share price to decline.

Unfortunately, we do not have an especially recent document to consult for this purpose. The fund's most recent financial report corresponds to the full-year period that ended on October 31, 2022. As such, it will not include any information from the past several months. This is unfortunate since that was a period of time that included a great deal of market volatility. However, the report should still give us a good idea of how well the fund performed during the worst of the challenging market last year, so that is certainly something that is helpful to see.

During the full-year period, the Saba Capital Income & Opportunities Fund received a total of $8,809,392 in interest along with $2,429,675 in dividends from the assets in its portfolio. This gives the fund a total income of $11,239,067 during the period. The fund paid its expenses from this amount, which left it with $1,944,996 available for shareholders. As might be expected, this was nowhere close to enough to cover the $44,996,624 that the fund actually paid out in distributions during the period. At first glance, this is likely to be concerning as the fund was unable to cover its distribution solely out of net investment income.

However, the fund does have other methods through which it can obtain the money that is needed to cover the distribution. For example, it might have capital gains during the period that can be paid out to investors. This is, in fact, the fund's goal as there is no conceivable way that it can earn a 12% return solely from interest and dividends. Unfortunately, the fund met with mixed results in getting capital gains during the period. It did manage to achieve net realized gains of $9,130,329 during the period, but this was more than offset by $18,329,380 net unrealized losses. Overall, the fund's assets under management declined by $52,250,679 after accounting for all inflows and outflows. This comes on the heels of steady declines to the fund's assets under management:

| FY Ending 10/31/2022 |

| Period Ending 10/31/2021 |

| FY Ending 2/28/2021 |

| Beginning Balance |

| $419,709,890 |

| $605,535,284 |

| $782,813,237 |

| Ending Balance |

| $367,459,211 |

| $419,709,890 |

| $605,535,284 |

As we can see, the fund's assets under management have been rapidly declining. I will admit that I am concerned about the fund's ability to maintain its distribution, as this is not a good sign. The fact that the fund was not able to cover the distribution during the eight-month period that ended on October 31, 2021, is especially concerning. It probably will have to change its managed distribution policy at some point to achieve sustainable finances.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Saba Capital Income & Opportunities Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of April 21, 2023 (the most recent date for which data is currently available), the Saba Capital Income & Opportunities Fund had a net asset value of $8.72 per share but the shares currently trade for $8.08 per share. This gives the fund's shares a discount of 7.34% at the current price. This is a reasonable price that is relatively in line with the 7.39% discount that the shares have averaged over the past month. Thus, the price certainly appears to be reasonable today.

Conclusion

In conclusion, the Saba Capital Income & Opportunities Fund offers a somewhat unique strategy that provides investors with exposure to several asset classes that may be lacking in a typical portfolio. However, the current emphasis on special-purpose acquisition companies may have worked a bit better during the heights of the bubble in 2021 than today. The fund has been outperforming the S&P 500 Index, though, so there are still reasons to like it.

The big problem here is that it appears that the fund is being too aggressive with its distribution. Saba Capital Income & Opportunities Fund will probably have to resort to either cutting the managed distribution to a level that is more reasonable based on its actual performance or selling shares to get money to distribute to the existing shareholders like the Cornerstone Funds. Neither of those is a particularly good option, so the best move here may be to wait for something to change. Saba Capital Income & Opportunities Fund is trading at a reasonable valuation, though.

For further details see:

BRW: Unique CEF With Some Good Qualities, But Distribution Looks Unsustainable