BTZ - BTZ: Good Debt Allocation Fund But Fixed-Rate Bonds Might Be Overpriced

2023-12-18 06:22:54 ET

Summary

- The BlackRock Credit Allocation Income Trust offers a current yield of 9.68%, lower than other debt funds in the market.

- The fund's shares have increased by 7.19% since October 12, 2023, outperforming the Bloomberg U.S. Aggregate Bond Index.

- BTZ's performance history suggests competent management, but it favors fixed-rate securities over floating-rate securities, which may impact performance.

- The market could be wrong about the magnitude of interest-rate cuts next year, and we may see a correction in bond prices over the next six months.

- The fund appears to be fully covering its distribution and trades at a discount on net asset value.

The BlackRock Credit Allocation Income Trust ( BTZ ) is a closed-end fund that specializes in providing a high level of current income for those investors seeking it. The fund's current yield is a bit lower than many of the other options available in today's market however, as it is only at 9.68% as of the time of writing. That would have been a very attractive yield two or three years ago when interest rates were near zero, but it is not really that great in a market in which the best debt funds are yielding 11% to 13%. Then again, BlackRock funds frequently do have lower yields than other options available in the market.

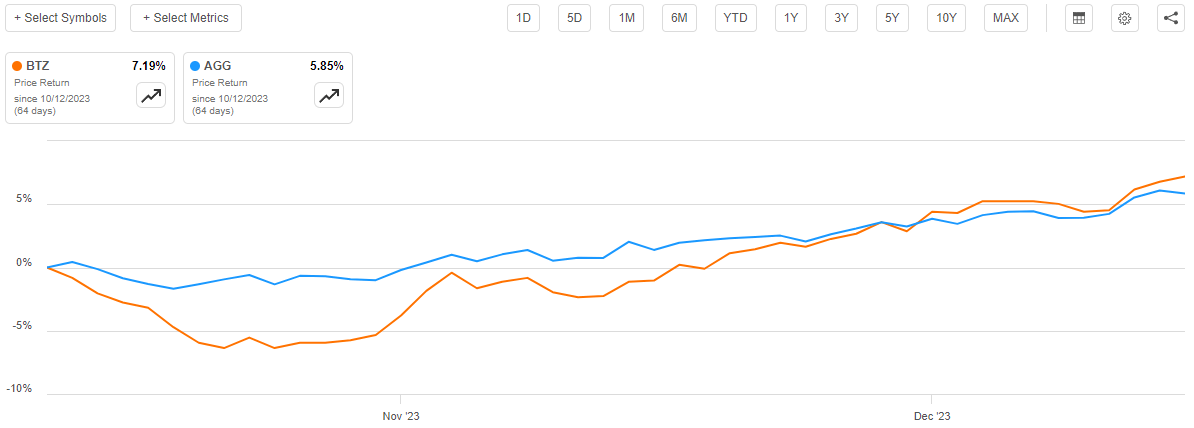

As regular readers may remember, we last discussed the BlackRock Credit Allocation Income Trust in mid-October. This article was published about a week before the market turned in earnest in anticipation of the Federal Reserve's 2024 interest rate cuts. As such, we might expect the fund's shares to have been going up during most of the period between that date and today. That is indeed the case, as shares of the fund are up 7.19% since October 12, 2023. This is better than the 5.85% gain of the Bloomberg U.S. Aggregate Bond Index ( AGG ):

{kind=link}

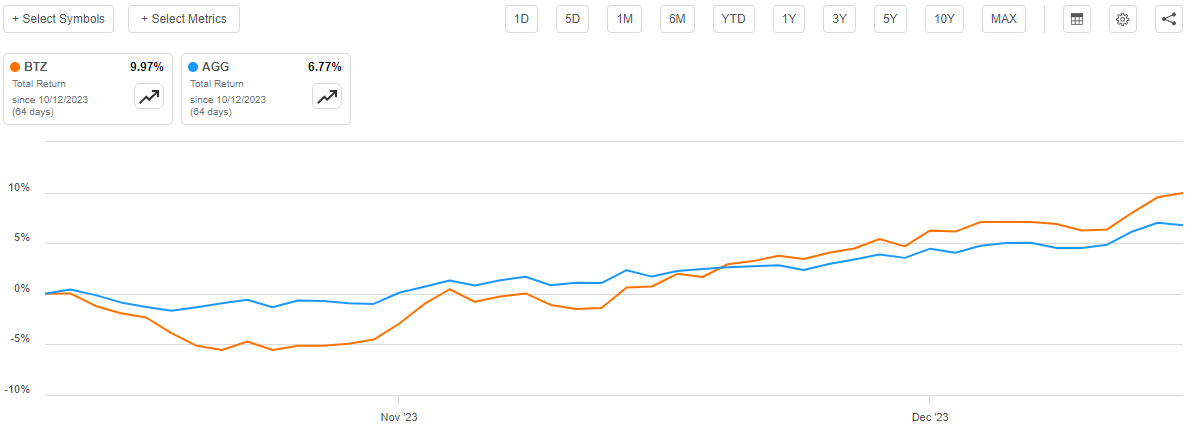

The fund's performance was even better when we included the distributions that it paid out during the period in its total returns. As we can see here, investors who purchased the BlackRock Credit Allocation Income Trust on the date that my prior article was published are up an impressive 9.97% over the past two months:

{kind=link}

As is the case with many fixed-income funds though, there could be some reasons to believe that the shares have got ahead of themselves. The market is pricing in more interest rate cuts than the Federal Reserve is likely to deliver, and when the market realizes this, it will probably reverse, and bonds will give up some of their near-term gains. As such, anyone buying the fund today may have to deal with some near-term losses. The distribution is large enough to offset at least some of the damage from this though, and long-term investors will almost certainly make money regardless. As such, the best strategy may be to simply slowly accumulate shares as opposed to building an entire position with one large purchase.

About The Fund

According to the fund's website , the BlackRock Credit Allocation Income Trust has the stated objective of providing its investors with current income, current gains, and capital appreciation. Specifically, the website states:

BlackRock Credit Allocation Income Trust's investment objective is to provide current income, current gains, and capital appreciation. The Trust seeks to achieve its investment objective by investing, under normal market conditions, at least 80% of its assets in credit-related securities, including, but not limited to, investment grade corporate bonds, high yield bonds (commonly referred to as 'junk' bonds), bank loans, preferred securities or convertible bonds or derivatives with economic characteristics similar to these credit-related securities. The Trust may invest directly in such securities or synthetically through the use of derivatives.

As I have pointed out in numerous previous articles, it is not unusual for a debt fund to have the generation of income as one of its primary objectives. After all, these investment vehicles are, at their core, income vehicles since the only net returns provided to their investors are the regular coupon payments that they pay out. The security is initially issued and ultimately redeemed at face value, after all.

The current gains objective also makes a certain amount of sense. It is possible to earn capital gains from debt securities because their price typically varies with interest rates. As such, the fund could buy when yields are high and then sell once long-term interest rates have come down and net itself a profit on the difference. This is actually a very typical strategy employed by bond funds because very few of them buy bonds and then hold them until maturity.

However, long-term capital appreciation, which this fund lists as its third investment objective, is very hard to achieve with bonds or other debt securities. As I pointed out in a recent article :

Bonds do not deliver capital appreciation indefinitely. Bond prices do go up when interest rates go down, but that is about it. There is a limit to how low interest rates can decline since nobody will ever lend money at a negative nominal rate. In fact, after the problems that have been caused by the easy money of the past two decades, it seems rather unlikely that the central bank will ever let the real interest rate drop below zero percent.

As such, the only real way to achieve long-term growth of capital by investing in bonds or other debt securities is to use coupon payments to purchase more bonds. Most closed-end funds do not do this and will instead opt to pay out all of the investment profits to the shareholders. That makes it very difficult to achieve any sort of long-term capital gains with a fund like this. However, as an investor, you could simply opt to use the distributions to purchase more shares of the fund to grow your personal position without any injection of new money.

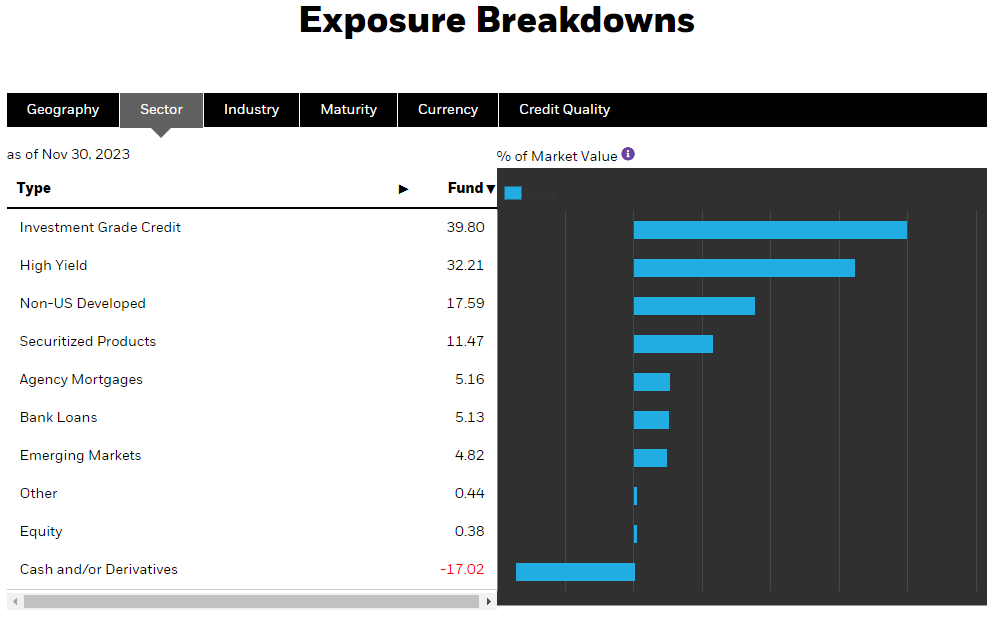

As I mentioned in my previous article on the BlackRock Credit Allocation Income Trust, this fund has generally favored investment in fixed-rate securities as opposed to floating-rate securities, despite the description stating that it will invest in both. As of the time of writing, only 5.13% of the fund is invested in bank loans, which are most commonly floating-rate loans:

{kind=link}

The majority of the rest of these securities are generally going to be fixed-rate investments. The exception could be the 11.47% allocation to Securitized Products. If these are collateralized loan obligations or something similar, then they might also be floating-rate securities. Unfortunately, the fund's most recent fact sheet does not provide a breakdown of fixed-rate securities compared to floating-rate securities and neither does the fund's webpage. The fund's semi-annual report also does not explicitly state this information, but a review of the fund's schedule of investments clearly shows that at least 16% of the fund is invested into floating-rate securities and probably more. However, that report is dated earlier in 2023 than the information on either the web page or the fact sheet. The takeaway though is that the fund appears to greatly favor investment in fixed-rate securities rather than floating-rate securities.

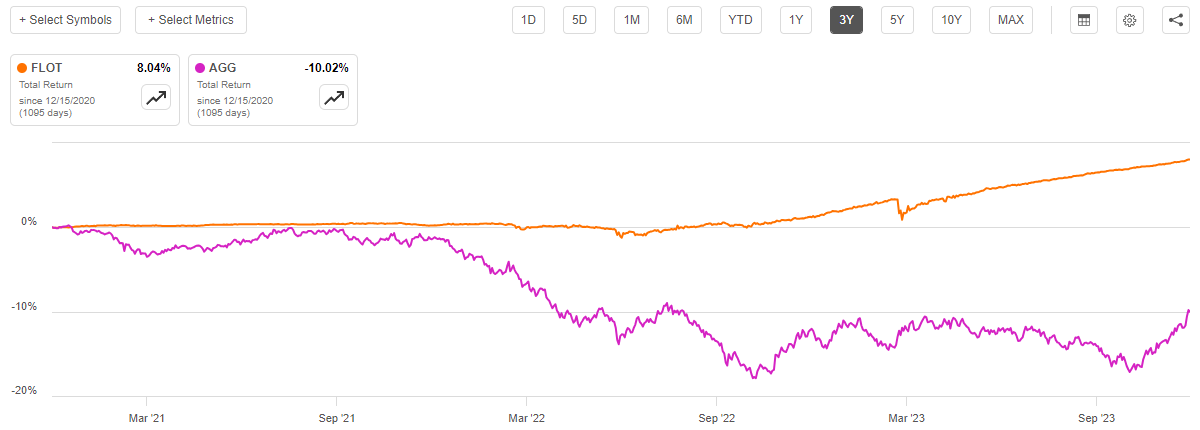

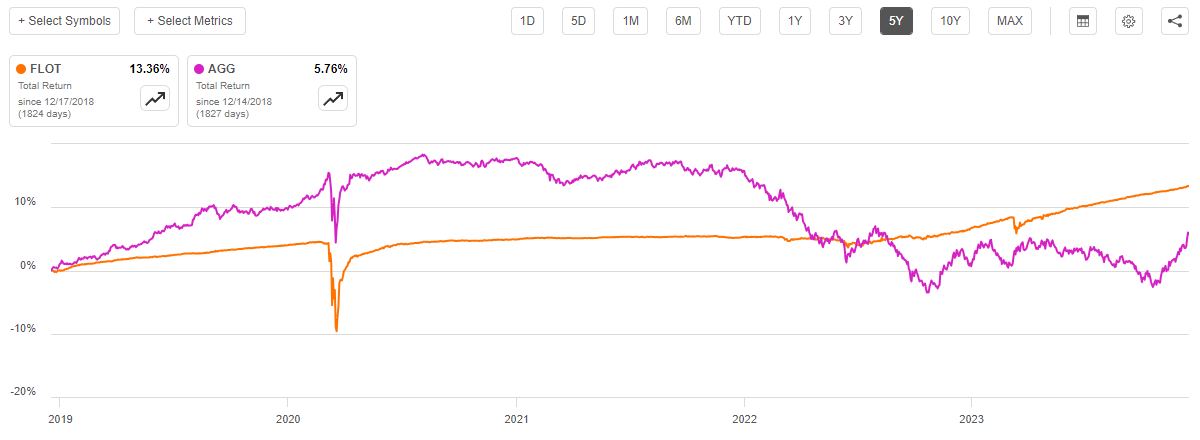

This has proven to be a negative factor in the fund's performance over the past few years. This is because floating-rate securities tend to outperform fixed-rate bonds during periods of rising interest rates. We can see this by comparing the total returns of the iShares Floating Rate ETF ( FLOT ), which invests in a portfolio of floating-rate loans, against the Bloomberg U.S. Aggregate Bond Index ETF over the past three years:

{kind=link}

As we can see, the floating-rate securities drastically outperformed the broader bond market index over the three-year period. This is true over the past five years as well:

{kind=link}

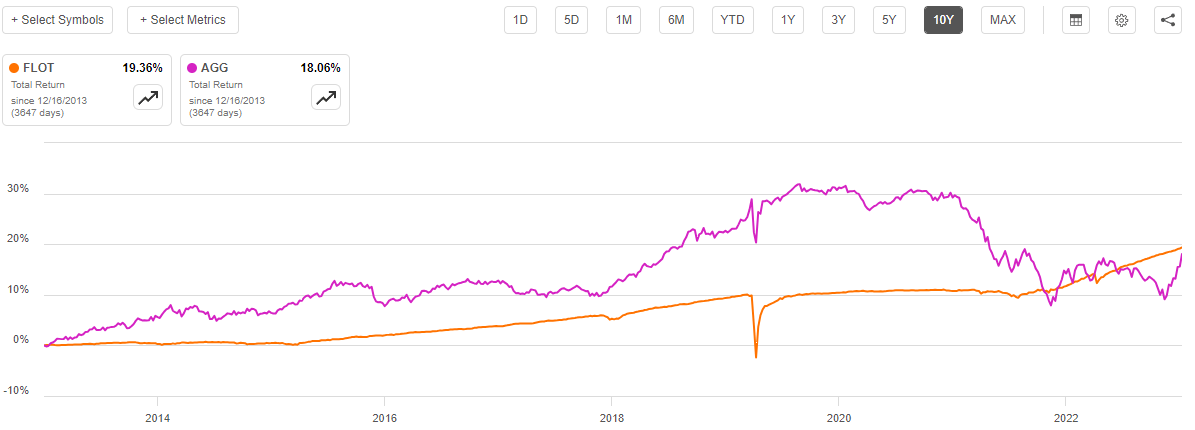

It is even true over the past ten years:

{kind=link}

The two longer periods did have some instances when fixed-rate bonds were outperforming, however. The biggest reason for this is mostly that floating-rate securities are not adversely affected by rising interest rates. In fact, they benefit because the payments made to investors increase. The reverse is true when interest rates decline, although floating-rate securities usually have a high enough coupon yield that they can provide at least some return. Ideally, the fund would be switching its allocation between fixed-rate and floating-rate securities in order to best take advantage of long-term interest rate trends. After all, the Federal Reserve does not tend to just randomly change rates up or down, its policy tends to be long-term, so it is not that difficult to follow the overall trend.

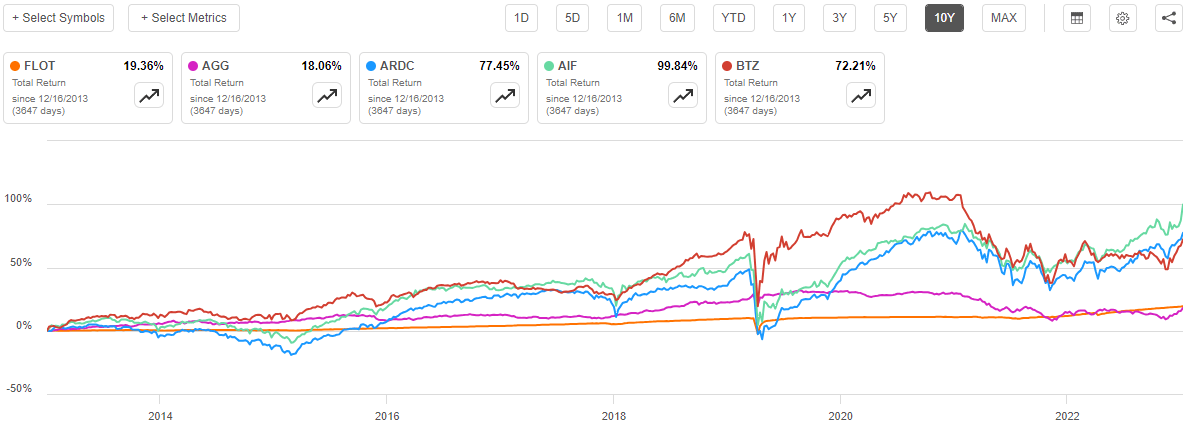

As I have mentioned in a few previous articles, there are some peer funds that have done this task quite admirably over the years. For example, both the Apollo Tactical Income Fund ( AIF ) and the Ares Dynamic Credit Allocation Fund ( ARDC ) have delivered very substantial returns to their investors over the years by altering their portfolio allocations between senior loans and traditional fixed-income securities to take advantage of interest-rate trends. The BlackRock Credit Allocation Income Trust has actually not done that poorly at this task either. As we can see here, over the past ten years, this fund has delivered comparable total returns to either of those:

{kind=link}

Over the past ten years, the BlackRock Credit Allocation Income Trust delivered a 72.21% total return to its shareholders. This is just a bit below the total return provided by the Ares Dynamic Credit Allocation Fund. The fund did underperform the Apollo Tactical Income Fund by quite a lot, but this was mostly caused by that fund's much larger allocation to floating-rate securities over the past year or two. The BlackRock fund was outperforming both of these peers during certain time periods though, especially back in 2021. While past performance is no guarantee of future results, this performance history certainly suggests that the fund's management has a great deal of competence in managing a debt fund across the interest rate cycle and this should be attractive to most risk-averse income-seekers who desire a fund that can simply be added to a portfolio and not require a high degree of micromanagement.

This is important considering that there is a lot of confusion right now with respect to the Federal Reserve's policies over the next year. As I have mentioned in various previous articles, the market is currently pricing in six interest rate cuts by the end of December 2024. That is pretty unlikely to occur unless we have a very severe recession within the next few months. The central bank itself currently suggests that there will be three rate cuts by the end of 2024, with one of the cuts being one that was originally planned for 2025. Thus, the long-term trajectory for interest rates remains the same as before Wednesday's announcement, it is just that 2024 is now expected to see an additional rate cut or two, and 2025 will see fewer than previously expected. On Friday, however, the Federal Reserve walked back on these comments and suggested that interest rate cuts are not currently being considered.

As such, there is still some uncertainty as to the Federal Reserve's policy, and this creates risk for investors today. In particular, the fact that the market is expecting more interest rate cuts in 2024 than even the most dovish voices at the Federal Reserve suggests that bonds are substantially overvalued right now and vulnerable to a short-term correction when the Federal Reserve does not cooperate with the market's expectations. As such, it is probably not the time to go all-in on bonds, but long-term investors will probably still want some exposure to these securities as the outlook over the next few years does provide some room for optimism. As such, a mixture of fixed-rate and floating-rate bonds is probably appropriate and that is what this fund delivers. It is not as aggressive as its peers though with respect to the floating rate securities so it might underperform both the Apollo and Ares funds in the near term, assuming that the United States avoids a recession. It could still be worth slowly building a position in this fund, though.

Leverage

As is the case with most closed-end funds, the BlackRock Credit Allocation Fund employs leverage as a method of boosting the effective yield and overall returns from its portfolio. I explained how this works in my last article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase bonds or other debt securities. As long as the interest rate that the fund pays on the borrowed money is less than the yield that the fund receives from the purchased securities, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. It is important to note though that this strategy is not as effective today with borrowing rates at 6% as it was two years ago when the borrowing rate was basically 0%.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that a fund is not employing too much leverage because that would expose us to an excessive amount of risk. I do not typically like a closed-end fund's leveraged assets to exceed a third of its portfolio for this reason.

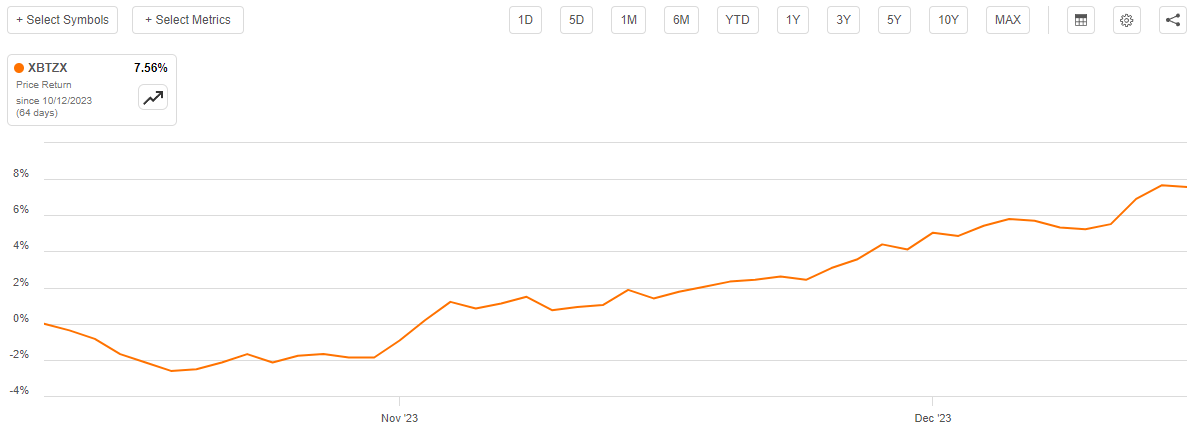

As of the time of writing, the BlackRock Credit Allocation Trust has leveraged assets comprising 36.46% of its overall portfolio. This is considerably less than the 38.01% leverage that the fund had the last time that we discussed it, which is a good sign.

As has been the case with several fixed-income funds in recent weeks, the fund's leverage ratio has gone down due to its portfolio increasing in overall size. As we can see here, the fund's net asset value per share is up 7.56% since the date that the previous article was published:

{kind=link}

This will naturally reduce the fund's leverage ratio as a percentage of the portfolio. After all, the increase in assets means that the outstanding debt is now a smaller percentage of the total assets assuming that the outstanding debt did not increase. It is a good sign that the fund is not borrowing more money just because its portfolio size is going up. After all, that action would increase our risks and given the real possibility that the market is wrong about its 2024 interest rate projections, we do not want the fund to be taking on excessive amounts of risk.

With that said, the fund's leverage is still higher than that one-third of assets maximum level that we would normally prefer to see. It is hardly alone in this though, as many fixed-income closed-end funds are above that level today. Fortunately, fixed-income funds can carry a somewhat higher level of leverage than equity funds because their assets are less volatile. This fund is probably okay, but we do want to watch it and make sure that it does not significantly increase the leverage from the current level.

Distribution Analysis

As mentioned earlier in this article, the BlackRock Credit Allocation Income Fund has the primary investment objective of providing its shareholders with a high level of current income. In order to achieve this objective, the fund purchases a variety of debt instruments including junk bonds, ordinary investment-grade bonds, floating-rate securities, and other things. It then borrows money to purchase more bonds than it could with just its own shareholder capital. The fund collects all of the money that it receives in coupon payments from these securities and combines it with any profits that it manages to earn by selling appreciated bonds in a favorable market. Finally, the fund pays all of this money out to its shareholders, net of its expenses. When we consider that bond yields are more attractive than they have been in over a decade, we can quickly see how this should give the fund a very attractive current yield.

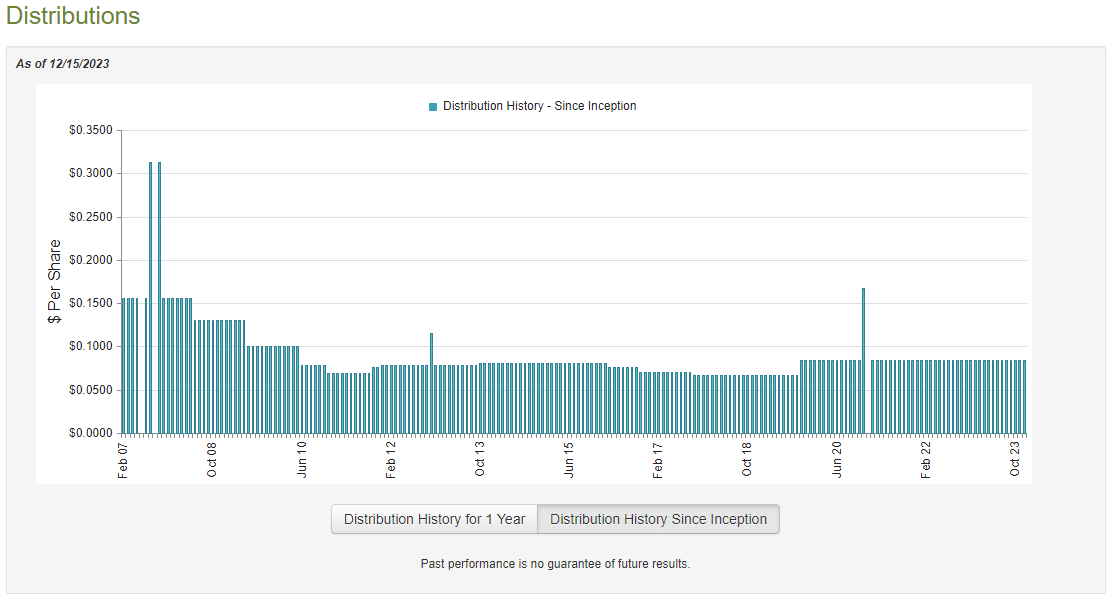

That is certainly the case, as the BlackRock Credit Allocation Trust currently pays a monthly distribution of $0.0839 per share ($1.0068 per share annually), which gives the shares a 9.68% yield at the current share price. This is not as high as some other fixed-income funds manage to achieve, but this fund also includes a higher proportion of investment-grade debt than most of the funds yielding 11% or higher so it should be slightly less exposed to the expected increase in corporate defaults next year. Unfortunately, though, the BlackRock Credit Allocation Trust has not been especially consistent with respect to its distributions over an extended period:

{kind=link}

As we can see, the fund's distribution has been raised and reduced numerous times over its history, although it has been quite stable since the pandemic. This fluctuating distribution could reduce the fund's appeal somewhat in the eyes of those investors who are seeking to receive a safe and stable income from the assets in its portfolio. The recent consistency is likely to be attractive though, assuming that the fund can sustain the payout. Most fixed-income funds had to cut their distributions over the past twelve to eighteen months in response to the Federal Reserve's monetary tightening efforts, so the fact that this one has not had to do that should be investigated. Of course, this fund did not increase its distribution during the incredibly loose monetary environment of late 2020 and early 2021 either so today's distribution could be partially covered by outsized trading profits during those years. This is why we need to pay close attention to the fund's financial statements.

Fortunately, we do have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on June 30, 2023. A link to this document was provided earlier in this article. This is a good time period to look at, as the first half of 2023 was characterized by a loosening monetary environment that kept long-term yields relatively suppressed and should have provided the fund with some opportunities to make trading profits. Unfortunately, this report will not cover the July to October period, which could have caused it to lose any capital gains that were not realized. We will need to wait for the fund to release its annual report in order to see how well it handled that event, but this report is not expected to be released for another few months.

During the six-month period, the BlackRock Credit Allocation Income Trust received $1,292,909 in dividends along with $49,732,746 in interest from the investments in its portfolio. When we combine this with a small amount of income from other sources, we can see that the fund reported a total investment income of $51,194,440 during the period. It paid its expenses out of this amount, which left it with $31,344,782 available for shareholders. That was, unfortunately, nowhere close to enough to cover the distributions that the fund paid out to its investors during the period. The fund's distributions totaled $47,071,475 over the course of six months, which might be concerning. After all, with a fixed-income fund, we would normally prefer to see the fund completely cover all of its distributions with net investment income.

However, there are other methods through which a closed-end fund like this can obtain the money that it needs to cover the distributions. For example, the fund might be able to earn some trading profits by exploiting bond price fluctuations. These trading profits are not considered to be investment income, but obviously, they do represent money coming into the fund that can be distributed to investors. The fund had mixed results at this task during the period, as it reported net realized losses of $45,590,272 but managed to fully offset this with $63,944,106 net unrealized gains. Overall, the fund's net assets increased by $2,627,141 after accounting for all inflows and outflows during the period. As such, the fund did technically manage to cover its distributions, although it had to rely on unrealized gains to accomplish this.

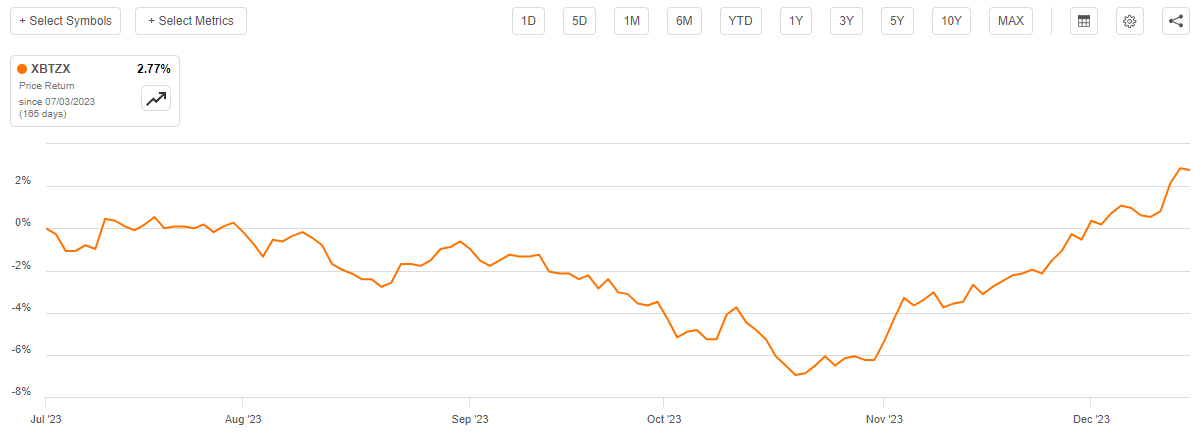

The problem with unrealized gains is that they can be easily erased in a market correction, such as the one that occurred when long-term interest rates shot up over the summer. This fund still appears to be okay though, as its net asset value per share is up 2.77% since July 1, 2023:

{kind=link}

This strongly suggests that the BlackRock Credit Allocation Income Trust has thus far managed to fully cover all of the distributions that it has made during the second half of its fiscal year. The fund's net asset value per share is up year-to-date as well:

{kind=link}

Thus, it appears that the fund has managed to fully cover its distributions year-to-date, even though it may have had to rely on unrealized capital gains to accomplish the task. The important thing to look for is that the fund's distributions are not destructive to its net asset value per share. It appears that this is not the case here so we should not need to worry about a near-term distribution cut.

Valuation

As of December 14, 2023 (the most recent date for which data is currently available), the BlackRock Credit Allocation Income Trust has a net asset value of $11.53 per share but the shares currently trade for $10.44 each. This gives the fund's shares a 9.45% yield at the current price. This is not quite as attractive as the 10.13% discount that the shares have traded for on average over the past month, but it is not really a bad price either.

Conclusion

In conclusion, the BlackRock Credit Allocation Income Trust looks like a reasonably decent debt fund in the current environment. The fund's ability to invest in both floating and fixed-rate securities is quite attractive considering the overall uncertainty in the monetary environment right now, although this fund does not seem to be quite as skilled at exploiting market swings as its peers. The fund does appear to be fully covering its distribution and trades at a reasonable discount on net asset value. The real risk here seems to be that bonds are looking overpriced and may be due for a correction at some point, which would punish anyone purchasing the fund today.

For further details see:

BTZ: Good Debt Allocation Fund, But Fixed-Rate Bonds Might Be Overpriced