BBRYF - Burberry: Historically Cheap Amid Macro Headwinds (Rating Upgrade)

2024-01-09 02:31:51 ET

Summary

- Burberry stock has sold off sharply since I last covered it in the summer, with the firm seeing a sharp slowdown in sales growth in its fiscal Q2.

- Management pinned the blame on a broader slowdown in the global luxury market. While fair, recent results also highlight the brand's relatively weaker position compared to peers like Hermès.

- While earnings will fall this year, the stock now trades for just 14x my fresh FY2023/24 EPS estimate.

- Burberry has rarely traded at that kind of valuation over the past decade. When it has, forward returns have been very attractive.

Shares of luxury fashion retailer Burberry ( BURBY )( BBRYF ) have fallen sharply since I last covered the company back in the summer, with the ADSs delivering a stinging negative 32% total return in that time amid a sharp deceleration in sales growth.

Downgrading to Hold at the time, I felt that macro factors might weigh on the company in the near term. Furthermore, Burberry's relative position in the sector means it is likely to underperform certain higher price-point peers such as Hermès in that kind of environment. This appears to be playing out, with management indeed blaming a soft global macro environment for its sales slump even though peers like Hermès ( HESAY )( HESAF ) are reporting comparatively better figures.

While flagging sales growth will lead to a drop in fiscal 2023/24 earnings versus my initial expectations, these shares now look historically cheap at circa 14x EPS, and I upgrade the stock to Buy.

Why Has BURBY Stock Fallen?

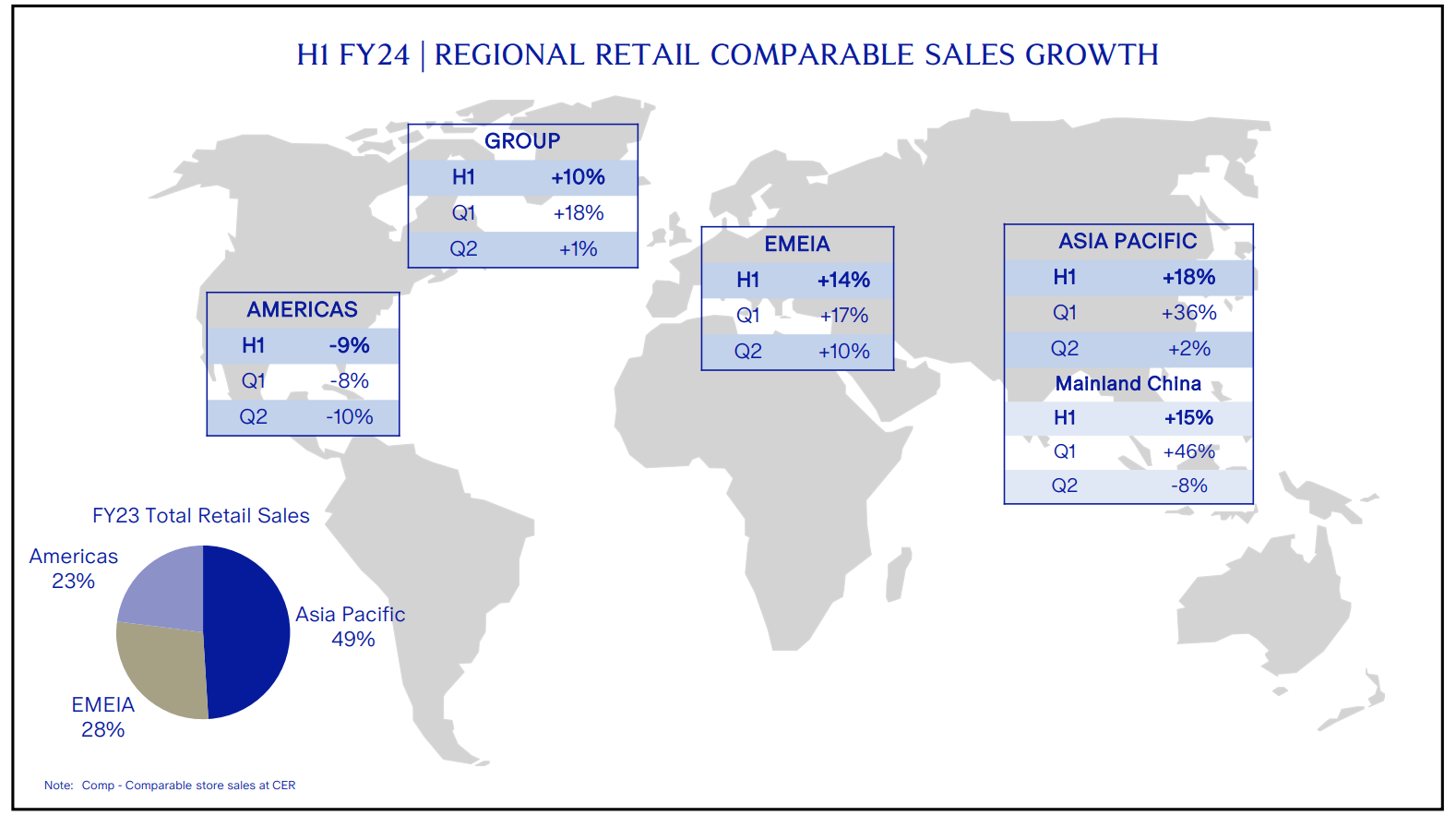

Burberry shares have been falling amid a slowdown in sales growth. In its fiscal 2023/24 second quarter (which roughly maps to the calendar Q3), the company reported Retail comparable sales growth of just 1% year-on-year, a sharp deceleration on the 18% growth posted in Q1. Although all regions reported a deceleration in sales growth, performance was particularly weak in the Americas, where Retail comparable sales fell 10% YoY in Q2.

Source: Burberry H1 FY2023/24 Results Presentation

{kind=link}

Management blamed the drop in sales growth on a weaker macro environment rather than any brand-specific issues, including anything related to new Chief Creative Officer Daniel Lee's first products:

We’ve really only launched Daniel’s products in September, so this performance is absolutely nothing to do with that. We’ve been really pleased with the response to the collections. Obviously, you know, we’re now live. I think the positive thing is that we are now live with Daniel’s products. This gives us a lot more visibility on what’s working and what’s not working and we’re very mindful about that, and we will adapt and adjust to that. But, overall, no, I think this is really down to the macro.

Jonathan Akeroyd, Chief Executive Officer, FY2023/24 H1 Results Call

This is entirely plausible given the wider global luxury industry has been staring at a slowdown in recent months . Part of this is due to the normalization of consumer behavior post-COVID, with the Americas particularly weak as pandemic stimulus savings continue to dissipate alongside other headwinds such as the resumption of student loan repayments.

While macro conditions are driving its performance, recent results nonetheless highlight Burberry's relative weakness versus certain peers like Hermès, with the latter reporting constant currency sales growth of 16% in its fiscal Q3 (which roughly maps to Burberry's fiscal Q2).

In past coverage , I have mentioned that Burberry's corporate strategy includes a goal to elevate its brand so that it can capture a higher price point. Results relative to Hermès highlight the value of such a strategy, with the latter's more prestige brand attracting a customer base that is clearly more immune to macro factors.

Source: Burberry H1 FY2023/24 Results Presentation

{kind=link}

I would note, too, that in business lines where Burberry's brand resonates strongest, such as its iconic trench coats, performance has remained relatively resilient. Outerwear, for example, delivered 21% YoY growth in H1, outperforming group sales by 11ppt.

Guidance Cut, But Buybacks Will Support EPS

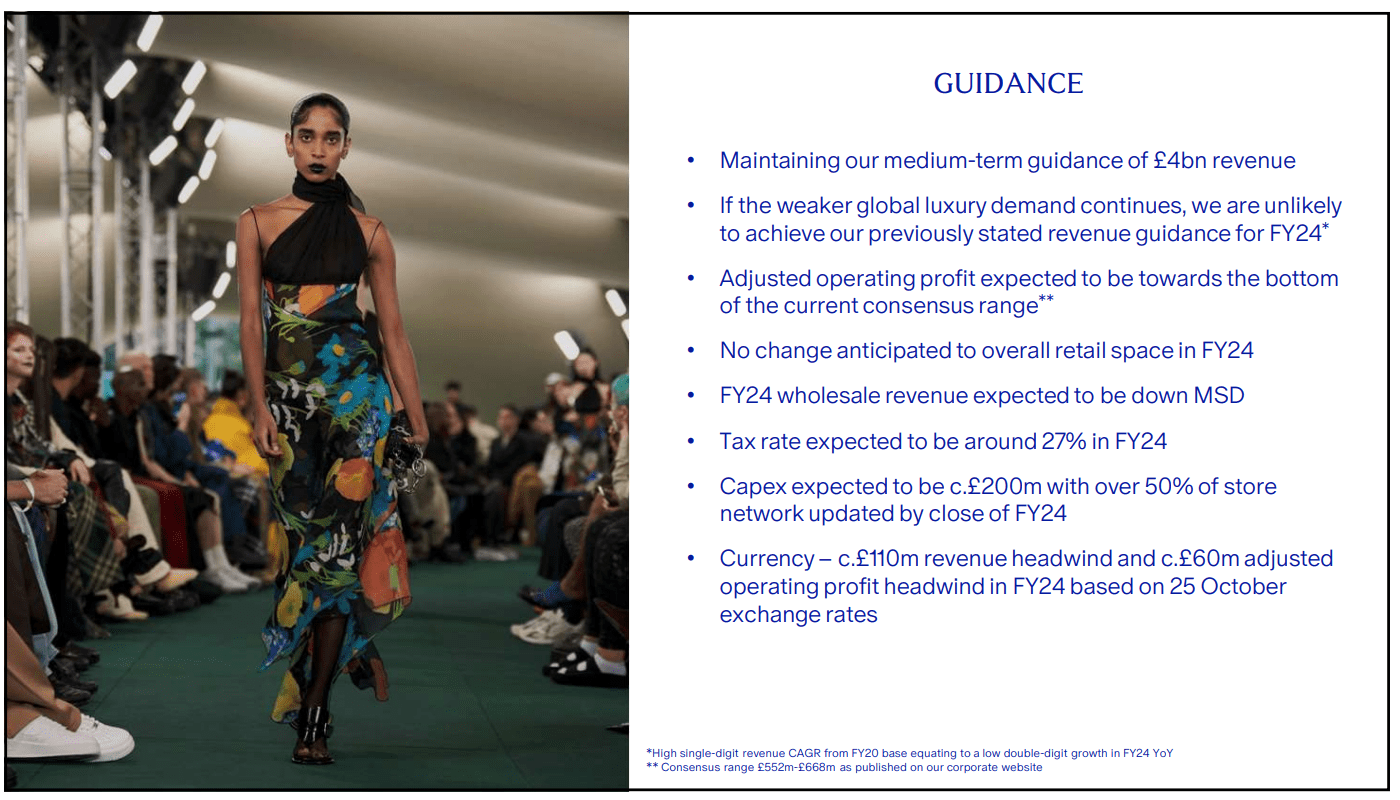

As per my last article, management was initially guiding for circa 11-12% YoY sales growth in FY2023/24 at constant exchange rates. Including a £70 million headwind from currency, that would have put revenue at around £3.36 billion for the full year. It further guided for 50bps YoY in operating profit margin expansion, again at constant exchange rates, implying a 20% EBIT margin. Including a £40 million headwind from currency, that would have pointed to around £645 million in annual EBIT.

Management has since downgraded EBIT guidance to the low-end of consensus , implying around £550 million in EBIT, including a steeper headwind from currency. This would imply a circa 13% YoY fall in EBIT, with net income dropping even more as the tax rate is seen at 27% this year versus 22.2% in FY2022/23.

Source: Burberry 1H FY2023/24 Results Presentation

{kind=link}

Now, one of the features of Burberry's business is that it displays significant fixed-cost leverage. It operates 409 stores worldwide, and this retail network accounts for around 80% of sales. Store-level expenses like rent, utilities, staff wages and so on need to be paid regardless of the ups and downs of sales. This means changes to earnings are typically much more volatile than revenue, hence the steep EBIT revision and share price decline.

One offsetting point to note, however, is that Burberry has been heavily buying back its stock. Debt is fairly modest here at 0.9x EBITDA, while cash conversion is typically excellent (i.e. the company converts most of its accounting net income into free cash flow), so there is plenty of cash to return to investors via dividends and buybacks.

Burberry reported weighted average shares outstanding of 376.1 million in H1, down from 394.4 million in the year-before period. Importantly, management commented that only £200 million of its most recent £400 million buyback program was completed in the period. The rest was completed by October, with the company reporting 358.5 million shares outstanding following the completion of its buyback program on October 31. This will provide some support to EPS, at least helping to cushion the blow of the higher tax rate.

Valuation Now Compelling

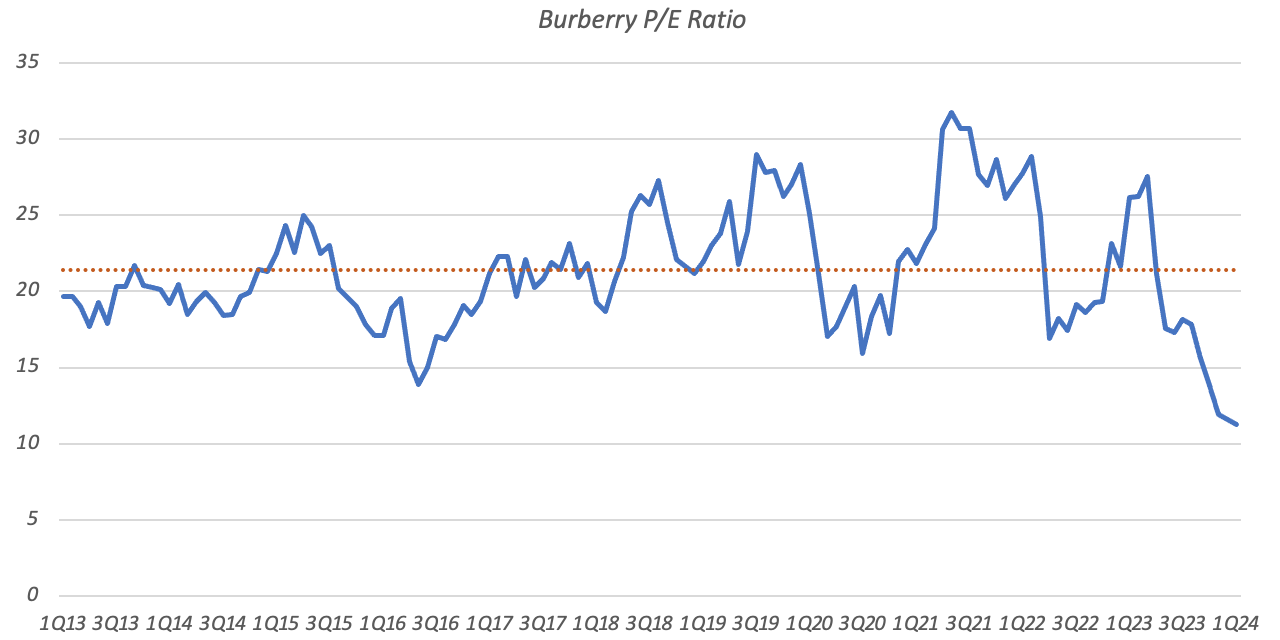

At the low-end of consensus , annual EPS would fall around 12% YoY to £1.06 (~$1.35 per ADS), but Burberry's share price is down by 32% since prior coverage. As a result, its P/E ratio has de-rated significantly, with the current $17.83 ADS price mapping to a P/E of just 13x.

Data Source: Yahoo Finance, Burberry Annual Reports, Author Calculation

{kind=link}

Looking over the past ten years of data, Burberry's P/E has averaged around 21x in that time. The current share price represents a circa 40% discount to this, and is based on forward EPS which already factors in a double-digit year-on-year decline. The stock has only been this cheap one other time in the past decade. That was in the second quarter of 2016, and it delivered a 60% total return over the following two years:

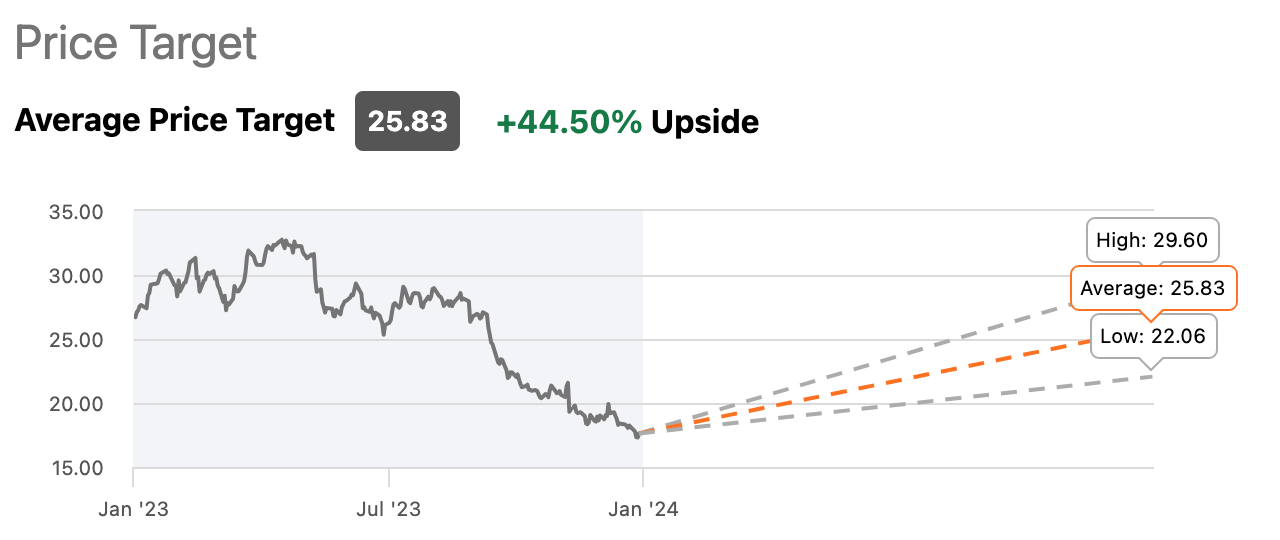

Wall Street analysts see a similar level of undervaluation, with 12-24 price targets pointing to 45% upside as per Seeking Alpha .

{kind=link}

Management has also kept medium-term guidance of £4 billion in annual sales and a 20% EBIT margin in place. I view that as a reasonable given the current slowdown is macro related rather than company-specific. If we apply a reasonable five-year timeframe to these goals, it would represent a top line CAGR of around 4.4% compared to FY2022/23 (when sales were £3.09 billion). That is about in line with the expected market growth rate. A 20% EBIT margin is only 50bps of expansion versus last year's figure, which also looks reasonable given the significant fixed cost leverage in the business.

After finance costs and taxes, EBIT of £1 billion would map to EPS of around £1.95 ($2.50 per ADS) based on the current share count. On a 16x EPS multiple, that would deliver a share price of $40 in five years. That doesn't include dividends, nor the impact of buybacks, yet it still represents over 100% upside from the current share price.

Risks

The two main risks to the above are macro and brand risk. A deeper than expected slowdown would hurt Burberry's near-term earnings more than anticipated and could also lead management to lower or scrap medium-term targets. Similarly, Burberry's brand could fall out of favor with consumers, which would have a similar impact on earnings. However, with Burberry's valuation running at a steep discount to its historical average I would argue these risks are more than compensated for. As a result, I upgrade Burberry to Buy.

For further details see:

Burberry: Historically Cheap Amid Macro Headwinds (Rating Upgrade)