BHRB - Burke & Herbert: First Underperformance Then Recovery (2024E Outlook)

2024-01-15 07:15:00 ET

Summary

- Burke & Herbert has seen outperformance compared to the S&P 500 since its merger with Summit Financial Group.

- The bank has a strong history and structure, with increased assets and offices following the merger.

- 3Q23 results showed strong balance sheet quality, increased loan volume, and adequate capital reserves, but net income was impacted by merger-related costs.

Dear readers/followers,

I've only written a single article on Burke & Herbert ( BHRB ), which you can find here . When I last wrote about it, the company had just merged with the Summit Financial Group, which overall enhanced its position and overall appeal - at least how I saw it, resulting in a bank with over $8B in assets and is expected to have a 2024E ROATCE of 22% and ROAA of 1.4%.

This is by no means a sector-leading bank even in the regional subsector, but it's far better than the bank was on its own as a regional player. However, I didn't invest in the bank - there were far better and safer alternatives out there than Burke & Herbert.

In this article, I mean to review the company once again because as a matter of fact, it has delivered outperformance more than 2x of the S&P500 when it climbed in pattern with the rest of the overall market.

What I like about the bank is its history, its structure, and the resulting assets and offices following the merger. It used to be just D.C., and now it's added to the surrounding areas as well.

Let's look at where the latest couple of quarters have left this bank and what we can expect here.

Burke & Herbert - What to expect from the bank going into 2024E

With over 150 years of history and an operational focus on D.C., it's easy to like Burke & Herbert's legacy operations. The merger with Summit will result in an added focus on the surrounding areas and towns, resulting in a scale advantage and diversified bank that has the potential to deliver some overall impressive cost savings.

The combined structure comes with significant deposits and is now the #3rd largest bank in the area. It also expected and forecasted a better return metric than most regional banks can expect, with an annual EPS of over $7.5 for the first year, which is something we can determine the likelihood of at this particular time.

The logic behind the M&A was a good one. Scale and efficiency are always a big one. Underlying quality in both banks is another one, though perhaps more so in Burke than in Summit, given Burke's 150+ year underlying history. But Summit, on the other hand, has managed to already consolidate operations through M&A several times since 2015, including successful ones of PSB holdings in 2023, and managed to include many of those qualitative operations into its banking business with a resulting, positive ROATCE. A regional bank is never going to have the same sort of operational scale and efficiency as a large global one.

However, regional banks can bring local expertise to the table, which is exactly what some local Swedish banks do, and why I am positive about operations such as these here. I'm familiar with this characteristic and consider it important.

BHRB IR (BHRB IR)

The latest set of operational results we have to look at are 3Q23 results - so let's see what we have here, and if the company is likely to deliver on the previously forecasted earnings.

And indeed, 3Q23 came in with plenty of impressive qualities. The company saw a continued strong balance sheet quality with very ample amounts of overall liquidity, totaling over $920 at the end of 3Q23. The company also managed to increase the loan volume by over 13.5% YoY, with total loans now at $2.1B and deposits totaling $3B, leading to a loan-to-deposit ratio of sub-70%.

The bank continues to present adequate capital reserves and safeties, a CET1 ratio of 16.4% to risk-weighted assets, and a leverage ratio of less than 12%. The aforementioned merger with Summit isn't yet done but will be done as follows.

There will be an all-stock merger of equals structure, creating a financial holding company with over $8B in total assets across more than 75 branches in Virginia, West Virginia, Maryland, Delaware, and Kentucky, and also consolidating more than 800 total employees.

On a net income basis, the company's net income was lower - but mostly due to merger-related costs, increased funding costs, and changes for credit loss provisions. The company recorded a non-trivial increase in NIE, offsetting the company's gain in NII. This is because the ongoing rate environment has, for a smaller player like this, resulted in a far higher increase in borrowing costs than in income, which is to be expected in the short term.

However, the company's asset and credit quality remain high. The company recorded credit loss provisions for only $200k - which while not zero, is still quite good, as I see it.

The ongoing plan for the company is to expand its market share, among other things through the merger, become more digital-focused, and grow the fee-based parts of its overall business mix.

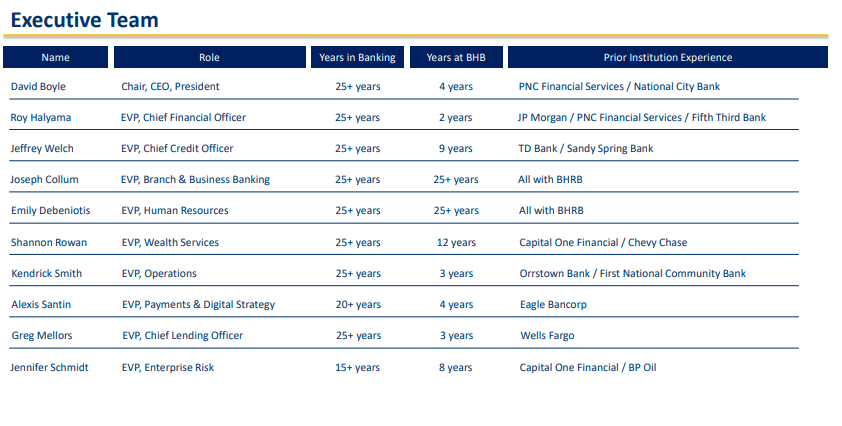

And I would also like to point out at this stage the sheer and impressive experience brought to bear by the management team for the bank. No one in the C-suite here has less than 15 years in banking, and most have over 25 years of banking experience to fall back on.

{kind=link}

This may be a comparatively undercovered and underappreciated little bank, similar to Bank OZK ( OZK ), but it's a good one for that, at least at the right price. There was a time when the company dropped after my article, where I would have viewed the company as a "BUY" - but this is no longer the case here, now that the bank has really bounced quite a bit.

Still, this is a very small company. And given the state of the market today, should this be a type of company that you should be investing in as things stand today?

After all, looking at margins and return metrics, this bank when compared to other banks is really quite average - the company's yield is less than 3.7%, and we're talking about this in an environment where it's possible for you to get 5% from an A-quality bank like Toronto-Dominion ( TD ), or even more from something like The Bank of Nova Scotia ( BNS ).

Why should you look at this particular one here?

Valuation for Burke & Herbert Financial

The valuation for this company remains very tricky to estimate. Given its small size, the lack of clarity for the upside following the merger, and the overall macro, where this company is certainly more impacted than a larger bank by higher funding costs, I would generally want to pay less than I would for a larger bank.

There's a clear limit to how much positivity we can actually give a company like this. Despite having traded at around 8-9x P/E since COVID-19, the company now trades at around 13-14x on a diluted basis. Is this a good price?

No, it's not a good price for this bank. When considering that the dividend yield is below 4%, that's even worse, and when considering the bank's size, that for me is the nail in the coffin here. The company is also currently at a premium to its book value, closer to 1.4 or 1.5x typically, now at 1.61x. Most relevant indicators for this company put Burke & Herbert at a not-inconsiderably high valuation at this time.

In my last article, I wrote the following.

The company has some things going for it. All of the valuation indicators are at 12-month or 24-month lows. There is also plenty of current insider buying. In this particular case, this is very good news, I obviously do not think people would be buying if they thought the deal was bad. And it's not meaningless sums either in terms of capital.

(Source: Burke & Herbert Article, Seeking Alpha )

However, those things have changed now that the company is up double digits. The company is now not at all-time lows or even really that much at a low, trading not that far from $60/share.

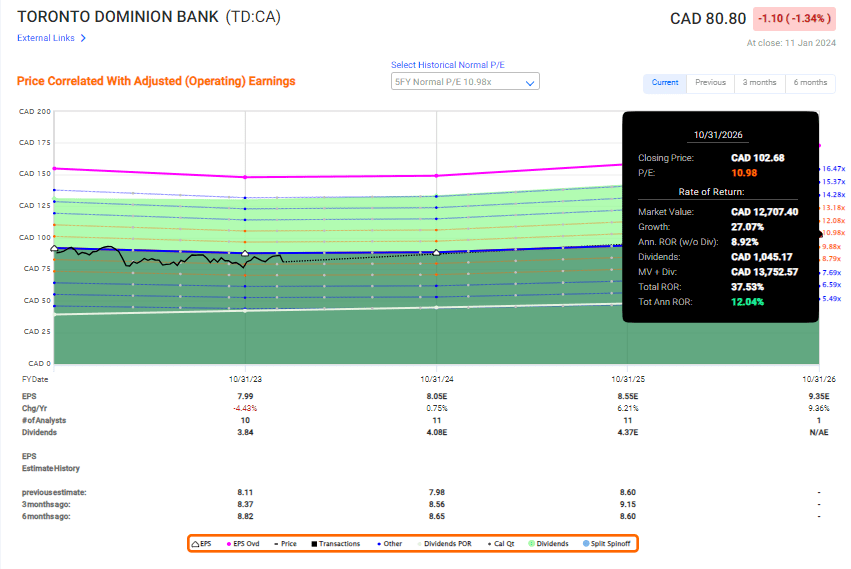

I don't believe this bank to be worth it, in the context of what other banks are available and the prices they're available at. For instance, a sub-$81 CAD Toronto Dominion bank even just forecasting that bank at 10.9x, gives us over 12% annualized of which 5% is dividend yield. That's not a high multiple, and it still has a very impressive upside, and with an AA-rated credit safety.

{kind=link}

When you can get that with ease and safety, I don't see a reason to invest in what I believe to be a somewhat overvalued regional bank with a limited scope and limited upside.

For that reason, I give you the following thesis on Burke & Herbert as we move into 2024E.

Thesis

- Burke & Herbert is an interesting regional banking play in a mostly attractive area of the United States. While this company lacks the appeal of any larger or global bank that I usually invest in, it does have meaningful potential upside to a normalized post-transaction P/E level of 10-12x. based on a $7-$8 EPS.

- However, even if such a valuation is possible, I would view it as a risky business to expect this out of a bank like this in an environment like this. This is one of those investments that I wish could be attractive, but the fact is that on a comparative basis, it is not.

- Put into context, I can buy BHRB - or I can buy a 5%+ yielding Toronto Dominion , with an A+ credit rating, and a significantly better conservatively-adjusted upside available than this one.

- In such a situation, my choice is obvious. This investment is contextually speaking, a "HOLD", even though upside is possible.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I can't give a higher rating or upside to a company in the midst of a merger and the associated uncertainty this brings, and now added to by the overall macro and uncertainty, which in my perspective really hasn't improved since I last covered the company.

This remains a "speculative investment", despite my current PT. I will revisit this where possible, but to those requesting coverage, I would look at non-regional and more "global" banks at this particular juncture.

For further details see:

Burke & Herbert: First Underperformance, Then Recovery (2024E Outlook)