BHRB - Burke & Herbert: Interesting But A 'Hold' Even With Potential M&A

2023-09-07 20:54:10 ET

Summary

- Burke & Herbert Financial Services is a small regional bank with a market cap just above $370M.

- The bank recently merged with Summit Financial Group, making it a larger and more interesting institution.

- The combined bank will have over $8B in assets and is expected to have a 2024E ROATCE of 22% and ROAA of 1.4%.

- However, given the market and what else is available, i recommend caution at this juncture.

Dear readers/followers,

In this article, I'm going to take a look at one of the regional banks - a small one with a market cap just north of $370M. These sorts of companies and banks aren't the easiest nor safest to invest in. Burke Herbert Financial Services ( BHRB ) is however a request I've gotten twice now, and that's usually my bar for starting coverage on a company. In this case, we're talking about an actual relatively small institution, with around a 4% yield, and it does have an upside.

However, the entire segment comes with an upside - so this company is in no way unique. A company being cheap isn't enough justification for a "BUY" rating in this environment - we need more fundamentals and upside.

Does BHRB fulfill this?

Let's see.

Burke & Herbert - a Regional bank with a storied history

Burke & Herbert has a lot of history. The bank has over 150 years under its belt and focuses on one of the more interesting and wealthy areas on the entire eastern Seaboard and eastern USA, centered around Washington D.C.

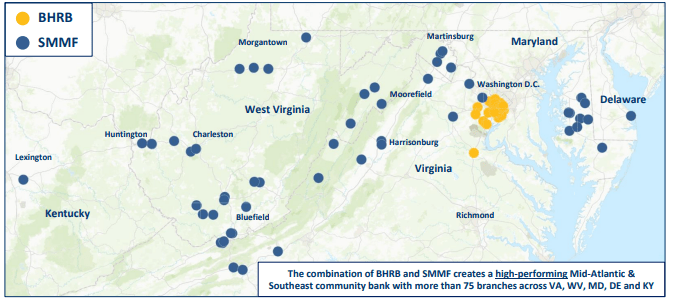

The company also very recently merged with Summit Financial Group, which effectively makes this bank much larger than before, and perhaps far more interesting than BHRB has been on its own.

Through the BHRB portfolio, which was entirely (or close to it) focused on the D.C. area, and the Summit Financial portfolio, which focuses on the surrounding areas...

{kind=link}

...which, as the presentation notes, creates a scale-advantaged and diversified banking institution with branches around the surrounding areas and states. This is certainly not uninteresting, because the company's combined assets will come to over $8B, with $5.6B in Gross Loans, and $6.7B in deposits.

The company will be the #3 largest bank headquartered in Virginia by assets alone, and in the top 10 for the deposit market share, not only in Virginia but West Virginia.

The company's return metrics are better than you might expect from regional banks. With a 2024E ROATCE of 22% and ROAA of 1.4%, estimating an annual net income of over $115M (again, remember the market cap here - BHRB has less than $400M in an unmerged state) and an annual EPS for year 1 of $7.9.

So why is BHRB doing this?

A few reasons.

Scale is obvious. To remain competitive, companies need to scale up and offer efficiency. This certainly does that, becoming a 5-state location bank with a good footprint.

I also have no issues with the forecasts about profit. The numbers make sense to me, with $600M of market securities able to be converted to liquidity with zero negative capital implications. With annual earnings well above $100M per year, the company with this scale can invest significantly in its own operations and growth, to become a $10B+ asset banking and financial institution.

Summit is slightly larger than Burke - but Burke is by far the more qualitative, older, more storied, and more well-managed bank. However, what Summit lacks in CET-1, it makes up for in M&A history. Summit has managed several M&As since 2015, including PSB holdings back in 2023. The picture I get from viewing and looking at Summit is a company that's picked up the working operations of banks over several years, resulting in a Core ROATCE for Summit of almost 19%. its efficiency ratios are nowhere near where peak banks are on a global scale, but it's still solid "enough" for where things are now.

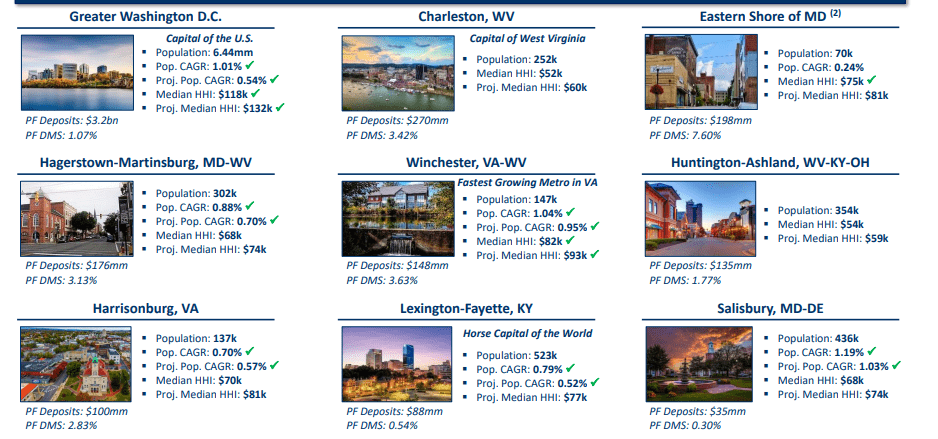

Also, this bank has a local presence - and knowing Swedish banks with a similar appeal and business model, I'm familiar with this characteristic and consider it important. With the combined operations, here are some examples of the locations that this combined set of operations can actually give us.

{kind=link}

I've been through the various loan and deposit compositions that will result as of this merger. The overall yield of the combined proforma loans will be around 5.82% - higher than Burke's 5.13% but lower than Summit's 6.13% - and this I believe is very indicative of the operational risks for these individual companies, with Summit being the "scrappier" bank here, but with higher risk (30%+ floating rate, 37% cycle beta, 95% Loan/deposits), while BHRB has all of the indications of a fundamentally and 150+-year-old banking house (26% floating, 22% cycle beta, Loan/Deposit of less than 67%). If BHRB can leverage Summit scale and geography, and apply some of the conservative policies clearly in place here, then this bank could see some significant outperformance.

And with a 4%+ yield, you're also getting a decent interest rate for your investment - not market-beating, but that's not the point either when you're investing in a "cheap" business - which at this valuation, this actually is.

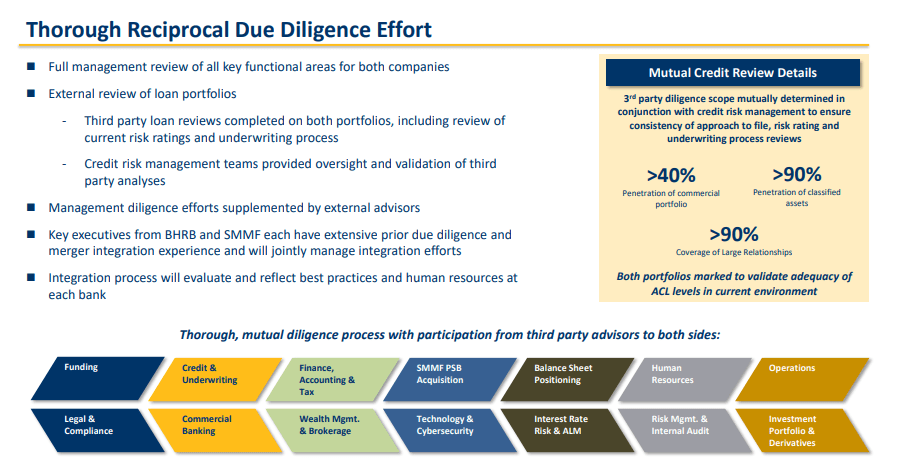

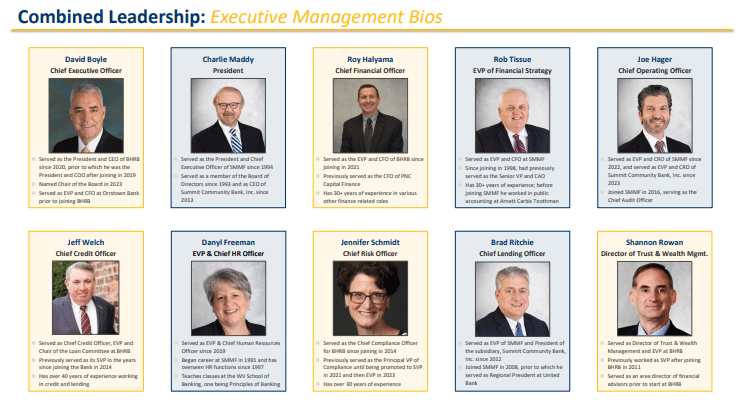

I haven't been able to find much concrete information of the combined leadership team - but from what I've read, the company, specifically Burke & Herbert, has one of the better teams in the area. The 50/50 split the company is doing both in terms of management and in terms of the board (8 from each), and added to by a very comprehensive due-diligence effort goes some way to add conviction to the case here.

{kind=link}

To those that haven't caught on - this is a merger of equals, but with Summit merging into Burke & Herbert, with BHRB as the survivor of the merger. Based on the company quality, this makes perfect sense to me, being considered the acquiring entity in legal and accounting terms. The bank charter will be BHRB's charter, but the ownership structure will be a straight 50/50 with a 100% stock consideration, with 0.5043x for a BHRB share for each SMM, with an implied share price of $25.20/share, coming to a total transaction volume $371M.

{kind=link}

The CEO of the combined bank will be David Boyle from BHRB, with the President being from Summit, the CFO being BHRB, and so forth. Headquarters will be in Alexandria, VA, with operations centers in Moorefield, West Virginia.

Closing for the transaction? 1Q24, though obviously subject to approval (though I do not forecast any challenges here).

On the earnings side, the company offers 95% 2025E EPS accretion on a GAAP basis, with a 1.2-year earnback, and a shareholder dilution of around 12.7% at the close. With 10.4% CET1 GAAP and 8.1% leverage, the resulting company will be again, not the best, but certainly good enough.

The only reason that I see investing in a regional bank or a smaller bank when there are banks that offer global scale and better yield is the home market and community advantage. The client advantage, so to speak. Does the resulting BHRB have this?

I say yes. BHRB as well as Summit does have a history of community involvement, zero actual footprint overlap historically, and obvious and clear synergies.

The combined bank will have a loan exposure that's relatively typical of a regional, client-focused bank. That means it has construction exposure, resi real estate, and various forms of commercial real estate, with small exposures to consumer and other sectors. Geographically, over 70% in West Virginia and Virginia respectively.

On a peer comparison, the pro-forma ROATCE, ROAA, and efficiency ratios outperform on nearly every basis, except in efficiency. That's where the company has perhaps most of its challenge - even pro-forma, it's sub-50%, with a peer median of 62% and a top quartile of over 53%.

Let's look at where this company comes in terms of valuation to see if you should actually invest here.

BHRB Valuation - a lot of uncertainty due to the merger

So, there's a limit to how positive I can be on the company given that it's in the midst of a merger, is a small regional bank in a global financial sector where opportunities aren't exactly rare at this time, and there's a bit of uncertainty baked into the numbers whenever you try and forecast the next 2 years in this sort of environment.

Burke & Herbert has typically traded, since COVID-19, at a normalized P/E of around 8-9x P/E. This is despite an impressive overall recovery between the years of 2020 until 2022, where we saw double-digit EPS growth for several years as the bank recovered from a 50% earnings decline during COVID-19. The bank hasn't been a dividend-paying stock for a very long time either.

While this merger announcement has caused the company's share price to normalize to a level where the merger is included, and there is an upside to the stock at this price, I would not necessarily put this investment at a high rate of attraction next to other companies available in the same, or ancillary sectors.

The company has some things going for it. All of the valuation indicators are at 12-month or 24-month lows. There is also plenty of current insider buying. In this particular case, this is very good news, I obviously do not think people would be buying if they thought the deal was bad. And it's not meaningless sums either in terms of capital.

After the company crashed, there was, and has been a flurry of activity from the director's side of things, with thousands of shares being purchased. Nothing extraordinary by any means, but nothing irrelevant for anyone with a six-figure salary either, and adding to an existing ownership in the millions.

When valuing the company, I would work with projected earnings, book valuations, and other multiples. The company currently trades at 1.3x to book, and depending on where you put the post-transactions earnings, an implied P/E of 8-12x P/E.

However, in the end, most of these discussions are moot.

The reason they are moot is that while BHRB is theoretically an attractive investment - and I do believe that this is the case - it ultimately fails the contextual test of looking at what else is available. There is a dozen banks and attractive names in the financial sector that offer a meaningful upside to an even more conservative future valuation, while also adding to this with twice the dividend yield, and A+ rated credit.

So while I can see a $70-$80/share price and consider this to be attractive in the context of regional banks on a post-transaction basis, it also comes with the caveat that there are better alternatives out there.

And unless you're Midas, your capital isn't limitless. You need to choose where to invest.

My stance is that BHRB isn't that, unfortunately, and for that reason I would stay careful here. I am going to give the company a "HOLD" here, and that's due to transactional uncertainty. I also go at a 30% discounted P/E to 10x of the pro-forma earnings, which comes to around $55/share.

And while this does, on a PT basis come to a "BUY", I still say "HOLD" until we know more about the merger.

That is my current stance on the business, and here is my thesis.

Thesis

- Burke & Herbert is an interesting regional banking play in a mostly attractive area of the United States. While this company lacks the appeal of any larger or global bank that I usually invest in, it does have meaningful potential upside to a normalized post-transaction P/E level of 10-12x. based on a $7-$8 EPS.

- However, even if such a valuation is possible, I would view it as a risky business to expect this out of a bank like this in an environment like this. This is one of those investments that I wish could be attractive, but the fact is that on a comparative basis, it is not.

- Put into context, I can buy BHRB - or I can buy a 9%+ yielding Credit Agricole ( CRARY ) , with an A+ credit rating, €33B in market cap, and over €320B in TEV with a realistic upside to a P/E of 8x of 22% per year or more.

- In such a situation, my choice is obvious. This investment is contextually speaking, a "HOLD", even though upside is possible.

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

This company is overall qualitative. This company is fundamentally safe/conservative & well-run. This company pays a well-covered dividend. This company is currently cheap. This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I can't given a higher rating or upside to a company in the midst of a merger and the associated uncertainty this brings. This remains a "speculative investment", despite my current PT. I will revisit this where possible, but to those requesting coverage, I would look at non-regional and more "global" banks at this particular juncture.

For further details see:

Burke & Herbert: Interesting, But A 'Hold' Even With Potential M&A