RBGPF - Buy The Turnaround In Reckitt Benckiser And Enjoy Its Recovery At A Discount

2023-04-28 05:24:29 ET

Summary

- Reckitt is a blue-chip large-cap consumer staple with roots going back over a century.

- After several missteps, signs are there that the long-awaited turnaround is taking place.

- The huge discount to peers is far too large, and the dividend yield of 3% is attractive.

- Help protect your portfolio during a recession and Buy Reckitt.

Consumer staple giant at a crazy discount

Reckitt Benckiser Group Plc ( RBGPF ) ( RBGLY ) (RKT lon) is a $56bn market cap consumer staple giant. They own brands across hygiene (41% of revenue), health (42% of revenue) and nutrition (17% of revenue) and, they are amongst the biggest brands on the planet.

Revenues as per Q1 are split as follows: USA 33.8%; Europe/ANZ 33.7% and Developing Markets 32.5% its remarkably balanced between the regions with an ever-larger presence in faster growth developing markets.

The brand reach is vast and include the likes of Dettol, Durex, Veet, Clearasil, Lysol, Vanish, Cillit Bang, Air Wick, Finish, Nurofen, Gaviscon and Enfamil. These are global brands that I'm sure many of us use daily, so many of us in fact that the company sells over thirty million products every single day !

reckitt brands (company website)

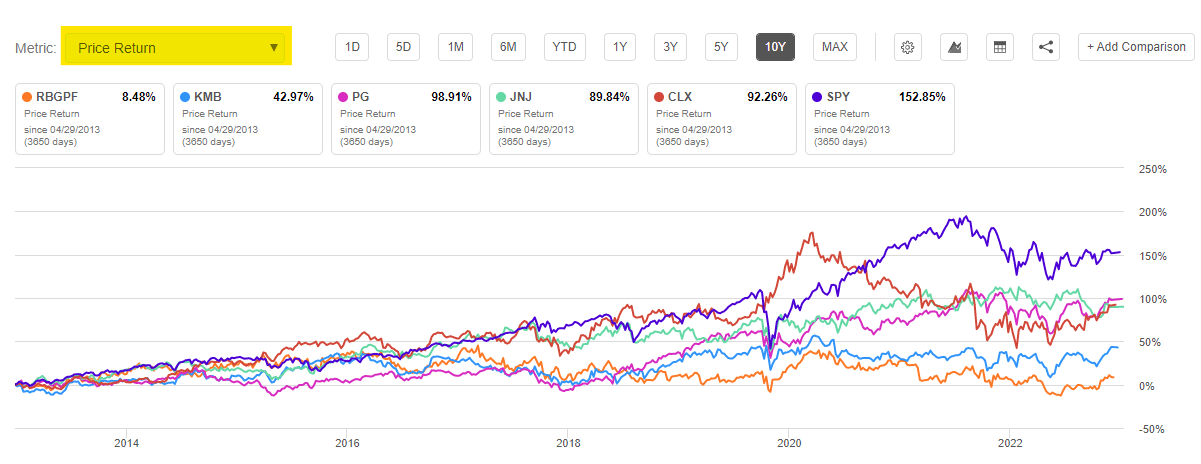

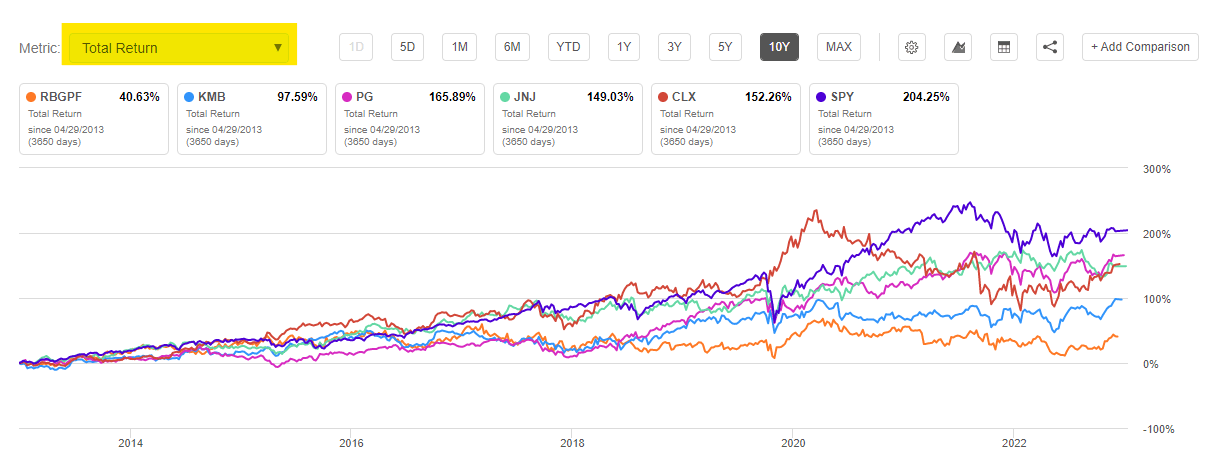

They compete in a fierce environment against other global giants like Johnson & Johnson (JNJ), Clorox ( CLX ) and Procter & Gamble (PG). This is a tough space where the biggest brands win, and customer loyalty is a hard-fought challenge. It might be surprising to learn then that going back over the last 10 years or so this global behemoth has been a poor investment. This is especially true when compared to both the market and its peer group. In both price and total return.

Price return vs peers over the last 10 years (Seeking Alpha)

{kind=link}

Total return vs peers over the last 10 years (Seeking Alpha)

{kind=link}

It sits last on the table when compared to the likes of Kimberly-Clark (KMB), PG, JNJ and CLX and by quite some margin too. Today though, I'm sticking my neck out and saying that this is about to change. Reckitt is amongst my favourite companies to hold for and after a potential recession.

The opportunity

For the last few years Reckitt has been struggling with a myriad of issues most of which have stemmed from a company that was accused of having lost touch with its markets and customers. Not enough time or money was being spent on brand awareness and customer service. On shelf availability and innovation were also seen as lacking. There were also concerns around a lack of control around certain costs which given its scale and reach should have been better managed. All this culminated in a business in need of some rejuvenation and an injection of purpose and sense of self.

It's taken some time, but the business has reshaped itself over the last few years and now after the appointment of a new CEO IS ready to prosper again, in my opinion.

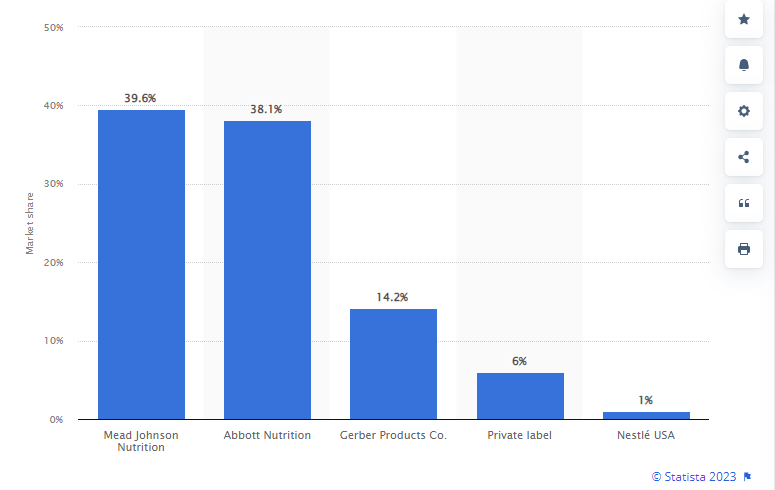

Its trading update published on 26 April is testament to the effort made over the last few years to reinvigorate the business and set it up for lasting success. The year has started well with group like for like sales growth of 7.9% vs expectations of 3.6%, volumes fell by 4.5% over the period. Don't let the decline in volumes put you off this is purely because of massive COVID and Baby Formula comparisons which are now being lapped in the Hygiene and Nutrition divisions respectively, with the latter seeing a surge in activity post the Abbott ( ABT ) baby formula scandal , which caused a massive shortage that Reckitt helped fill which boosted sales in that part of the business. Impressively however those market share gains haven't reversed with the Enfamil brand (Mead Johnson) holding on to roughly 40% of the US market .

US baby formula market shares (Statista)

{kind=link}

As has been the case with companies in this space price increases are being passed onto consumers, and the ability to raise prices helps offset higher input costs which in turn protects margins. This of course can't happen infinitely, so it needs to be watched, however price/mix gained a whopping 12.4% in the last period as supply chain disruptions eased and retail inventories were restocked (in baby formula especially).

Underneath it all we are seeing considerable progress being made. Over half of the company's core category market units held or gained share over the last three-month rolling period and this is a commendable achievement when such large one-off situations cause a spike in market share which can easily be reversed once things get back to normal.

Despite these large covid and baby formula comparisons the company is still guiding for overall growth of 3%-5% this year. This guide is especially important in my view - its suggesting that despite these 'one off' boosts the underlying business is firing on all cylinders. Growth on top of what could be construed as an artificially higher base is very impressive. To my mind it demonstrates how the company jumped on the baby formula opportunity for example and is still holding onto those market share gains even now that it passed. The investment in innovation and distribution is bearing fruit.

E-commerce sales are also growing above market and net revenue was up 9% in the quarter, it's now 13% of group revenue. The Chinese reopening is yet to be fully reflected in company performance too which adds to the view that management guidance is likely to be met and might prove to be a bit on the conservative side.

On top of this the 8-month search for a CEO is over. The internal promotion of Kris Licht (who was instrumental in both the transformation strategy and the significant turnaround of the health division) was announced on the 26th of April. Investors should feel comfortable with the company under his stewardship considering his role in turning the company around.

The turnaround in the business operations is a vital cog in the investment thesis that in my mind is over the hump and this leads us to the next piece of the puzzle.

Valuation

Consumer Staples are considered some of the safest, most reliable investments people can make. These are large well-run companies that have been around for years and in some cases even centuries (Reckitt's roots date back to 1823!) They sell products we as consumers enjoy, need, or want and that we purchase regularly repeatedly. (See my previous article here with a look at Maslow's hierarchy of needs and covers my first recession proof pick in the 'water' space). They've survived recessions, depressions and crises time and time again and come out stronger for the next set of challenges they face. This is reflected in the premium price investors are willing to pay for these quality companies.

Peer group valuation comparison (Seeking Alpha)

Every so often however these companies need to reinvent themselves in order to stay relevant and oftentimes during this process the business and share price can underperform. It's akin to a sports team rebuilding itself as its best players retire or move on. The period of reinvestment takes time to bear fruit at which point the next cycle of success begins. Some of course have proven more adept than others at getting this right, Nestle ( NSRGY ) (NESN switz) for example hardly ever put a foot wrong. Reckitt on the other hand had let it 'slip' and has been punished as a result. The share price now trades at an enormous discount to the peer group. Its dividend yield too is 10% higher than peers.

Is this justified? It may have been as the company grappled with its market position and painstakingly turned itself around but if they are in fact on the mend as recent trends show this discount is due to be narrowed.

What makes this company so attractive in my view is not only the demonstrable turnaround in the business but also the significant ground the share price must make up to achieve a market related valuation.

What's it worth?

Well again this is subjective, so we use this as a guide and try to find a range that makes sense to us. From a PE perspective you'd have say that the company needs to earn its way back up the ranks, but with such a solid slate of brands and a turnaround gaining traction a discount like we see below seems far too steep. Looking at a range of PE's we get the following.

{kind=link}

It's a wide range that's for sure but I'd argue RKT is not yet worthy of the premium valuation something like Nestle, Clorox, Coke or Pepsi has but even at a 20% discount to the average we still get to a target price of £83.86 vs the current price on the London market of £63.00.

What about a discounted cash flow [DCF]?

Looking at a DCF I'd use a risk-free rate of 7% which is almost twice the current UK 10-year Gilt yield, this adds an adequate margin of safety as its pretty much double the risk-free rate. 6.9% also happens to be the average annualised return of the FTSE100 in the UK over the last 20yrs so it is also a decent return hurdle to consider. Looking at growth I think 6% per annum for the next 5 years is possible as the company's efforts over the last few years begin to show up in company performance. New innovations and product lines are showing promising adoption and are resonating with customers. From there we take it down to the long-term inflation expectation of 2% per annum.

DCF valuation (Analyst)

Once again, it's quite interesting that both the PE relative and the DCF valuations line up quite closely. The average of the two valuations is £83.50 which is significantly higher than the current £63.00 level. This implies a potential return of 32%. Whether looking at PE or discounted cash flows upside is considerable for what is a 'bellwether' company.

The dividend is growing too and should continue to grow at or around the same rate of earnings, call it 4-6% per annum which off a starting yield of 3% is very attractive.

Risks

As always there are risks, we need to consider.

First off, I'd say is that of recessions. With roots going back over 100yrs we can say that existential risk is small but of course the impact this may have on the consumers of the company's products needs to be considered. Tougher times may mean consumers rein in spending and buy less.

Inflation too is something we need to watch. Although the company has successfully increased prices in this current inflation cycle this cannot happen infinitely. At some point consumers will refuse to pay more. Unless input costs decline, which allows for some price elasticity, especially if economies do go into recession, margins would come under pressure.

The firm reports its earnings in GBP however it derives just over a third of profits from the UK. The weaker pound over the last year has proven a nice tailwind to earnings. Should the pound strengthen, or dollar/euro/emerging markets currencies weaken this tailwind will reverse.

The turnaround strategy is clearly gaining momentum however if it falters, we may not see the rerating we hope will materialise because of the company getting back on track.

Although the new CEO is a familiar face and largely responsible for the company's successful turnaround so far, the market may have been hoping for an external candidate to take the role as was evidenced by the 3.5% decline in the stock price after the announcement was made. Faith in management is vital to the rerating thesis and Mr Licht will need to show he is the right person for the job.

Conclusion

After a long period of underperformance, Reckitt's turnaround efforts are starting to bear fruit. This is a large well-established company with a long history that is currently trading at a substantial discount to its peer group. Its valuation disconnect is also evidenced by the wide gap between its current price and a DCF value that does not have aggressive assumptions in it. This discount should narrow as the company demonstrates its investments in innovation, distribution and customer service are beginning to pay off.

A new CEO which played a large role in the successful turnaround is bringing new energy and purpose to the group too and at exactly the right time especially if a recession is around the corner. The consumer staples sector is considered one of the best sectors to invest in for defensive exposure during times of stress. Here we have a blue chip at a 40% discount to its peers with a 3% dividend yield that is forecast to grow faster than long term inflation expectations. In my opinion, this a low-risk high return opportunity that is worth considering for your portfolio.

I've added Reckitt to my portfolio and consider it a safe BUY.

For further details see:

Buy The Turnaround In Reckitt Benckiser And Enjoy Its Recovery At A Discount