BZFDW - BuzzFeed: Oversold Beyond Its Prospects

2023-04-08 09:00:00 ET

Summary

- BuzzFeed saw a revenue decline YoY but has still grown over the last 2 years, albeit in a choppy fashion.

- While consistently unprofitable, its cash burn rate is not so bad and it isn't set to go out of business any time soon.

- Additionally, I like how it remains a founder-led company with a relatively technical CEO.

- The stock is trading very cheaply, but overall I think there is more than meets the eye here, and I am willing to call it a buy based on alternative factors. Note there is significant risk here, however.

Overview

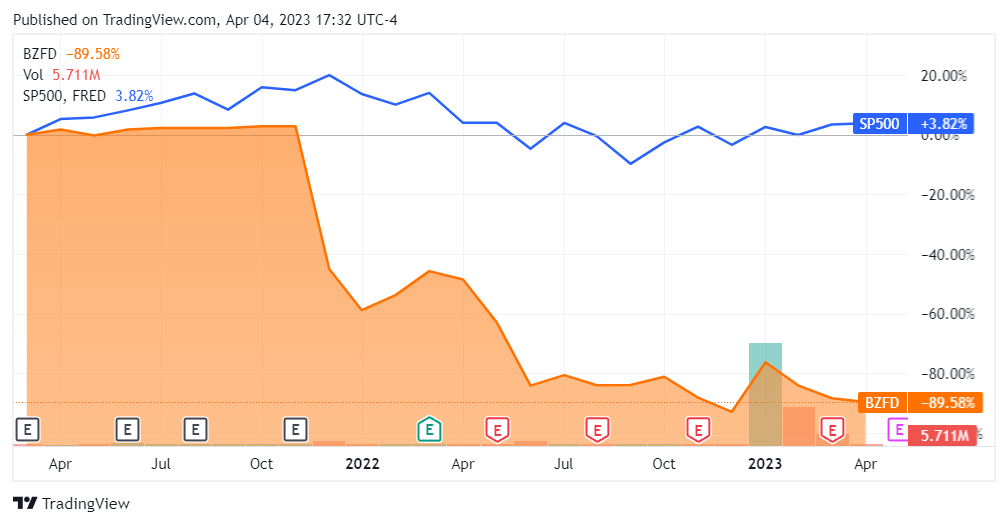

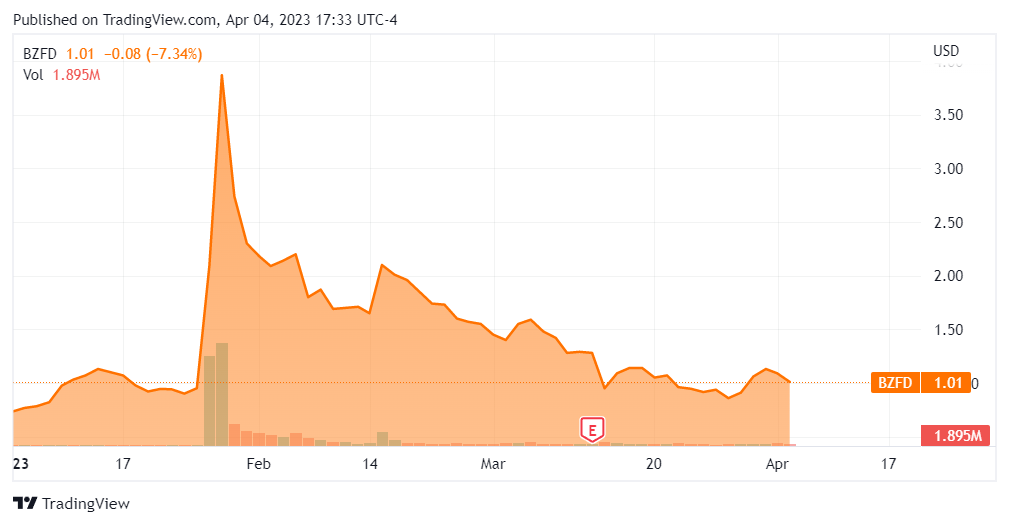

BuzzFeed (BZFD) is a decently well-known digital media company focused on short-form content that it distributes through its own website as well as other channels. It primarily generates revenues from advertisements sold against this content. It has been in the news cycle recently for inking a $10M ARR deal with Meta as well as embracing the use of ChatGPT for content creation. While the stock appreciated headily in light of that latter bit of news, it has since been sold off to levels at which it has traded previously, with the stock recently trading right near the $1.00 level.

{kind=link}

{kind=link}

This article will review the company's financials to see where things are headed and if the stock is deserving of its current valuation.

Financials

Revenue on the whole has been going up over the last 10 quarters. It is orth noting is that Q4 of each year seems to be a blockbuster quarter for the company and the one in which they earn the most revenue. The most recent print on this was unfavorable for the stock because BuzzFeed couldn't beat its previous years performance for Q4. Nonetheless we see that revenue growth overall has remained quite solid for the company. The down quarter is certainly bad, but I am less convinced that it's damning because of the overall volatility of revenues that this company regularly experiences. I also believe that the relatively weak Q4 for revenues was due to secularly weak advertising demand - something that may very well continue throughout this year.

{kind=link}

Gross profit is variable like revenues but overall growing much less steadily. This is due to the constantly changing expenditures for content creation; every piece is unique in terms of cost footprint. This is the area where AI could perhaps drive margin or at least create more stability.

{kind=link}

The profit picture isn't too pretty and is also highly volatile. In general BuzzFeed loses money, although it had 2 quarters where it did fairly well. The most recent quarter's seemingly dismal performance was driven by a one-off non-cash goodwill adjustment of $102.3M that wiped out more than half of the company's goodwill from previous acquisitions. While this looks bad, it's actually standard practice as far as accounting goes and is not something that indicates anything about the core business of the company. Without that adjustment net income was close to breakeven at -$3.01M. Not exactly good, but better than it's been all year.

{kind=link}

As for cash flow, we also find a variable picture but one that is noticeably less negative than what the firm posts across net income. Nonetheless, the performance here is spotty. The business model necessarily creates variability across this dimension as well.

{kind=link}

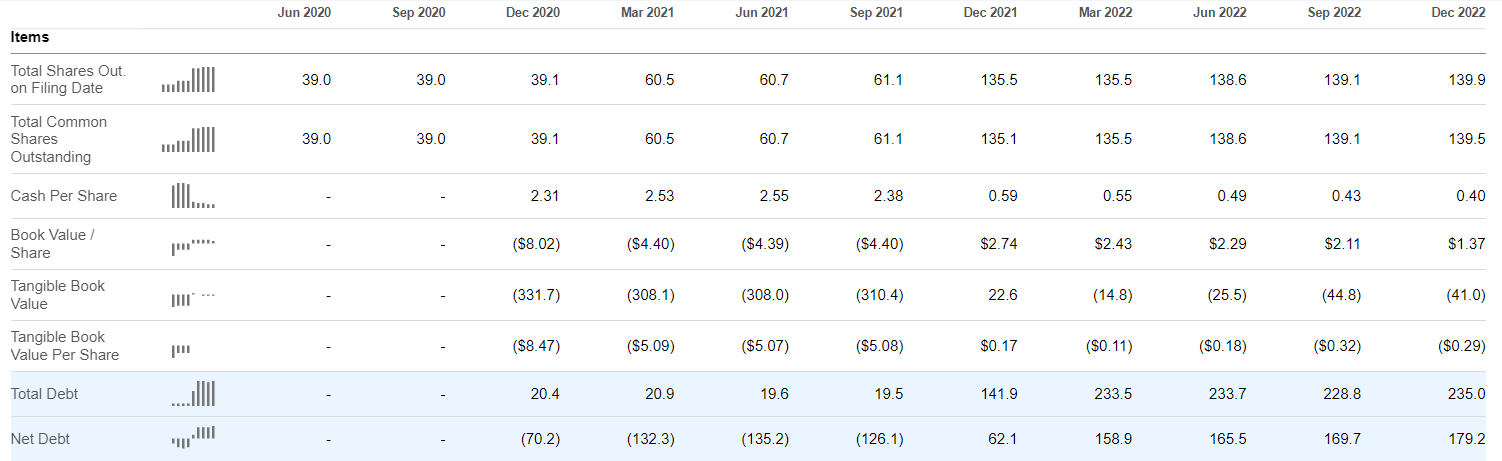

Given the lack of profitability and cash flows, we should evaluate the balance sheet to see how leveraged BuzzFeed may be. It is a net debtor and appears to have been so since going public.

{kind=link}

The firm's debt service appears to be structured semi-yearly but isn't an overly large portion of revenues.

{kind=link}

This past year has also seen management be significantly more conservative with cash, with the firm losing less than $10M of cash per quarter.

{kind=link}

Adding up the cash burn across the last 4 quarters, we can annualize this to $24.1M. At this burn rate and present cash levels the firm has roughly 2 years to go before it needs fresh capital. I consider that enough time to improve bottom line and cash metrics further, which is a must in the current market context.

{kind=link}

These financials are overall difficult to extrapolate given their variability. The bright spot to me here is the relatively strong QoQ revenue performance and the controlled cash burn. I believe that this company is still growing, albeit in a highly unsteady fashion. While Q4 was certainly a poor showing, it wasn't too large a drop-off to have warranted this kind of valuation at the moment.

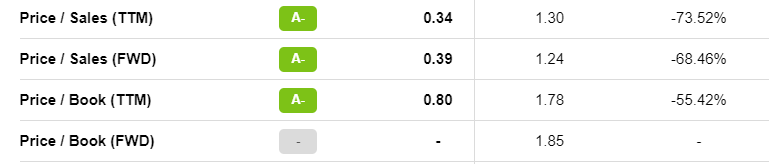

This stock is trading cheaply because of ongoing concern about the digital advertising environment - which is warranted. The discount, however, is quite steep on both a sales and book basis. This is of course due to the ongoing correction against non-cash generative companies; I think this will be the big question for BuzzFeed. AI could open the door for that.

{kind=link}

Since it doesn't look like BuzzFeed will go out of business soon, this valuation is cheap - if you believe they can hit break even on cash. At the burn rates cited above, they're actually not too far off.

The CEO Factor

Something that I consider interesting about BuzzFeed is that it remains a founder-led company. Throughout my career, I have found that these companies tend to outperform their peers. Founder-CEOs who stay on board are committed and are often willing to do what it takes to keep their company going.

Jonah Peretti also studied at the MIT Media Lab. For those in the know, this is an interdisciplinary facility in which the boundaries of technology and media are pushed. I believe this part of MIT provides a uniquely quality grounding for someone who is now trying to leverage artificial intelligence for content creation. Basically, I think this is the CEO for the moment for BuzzFeed. Luckily enough, he is also the founder.

{kind=link}

Conclusion

I'm going to take a leap of faith here and call this company a buy. While the financials haven't yet proven out profitability or cash flow generation, this company is trading very cheaply on a sales basis and has what I consider to be credible potential to wrangle its unit economics through artificial intelligence. It also has the cash on hand to sustain through this period of change and appears to be managing its burn rate quite well throughout recent quarters. Basically, it's quite cheap at the moment and I don't think it will go out of business; I believe revenues should also continue to grow in a volatile fashion over the long-term.

As to the top-most line for media businesses - attention - things are still going just fine for BuzzFeed. It generated 100M unique views this past December . It also has a very young base of users; marketers know that this is a valuable demographic to have access to.

Furthermore, I think BuzzFeed is uniquely positioned to leverage AI for content creation and customization for two reasons. The first is the CEO. The second is the business model itself. The company relies on short-form, quick-hit content - the kind that I would believe is most amenable to partial automation through AI. BuzzFeed is undoubtedly a leader in this kind of quick content; that has always been its bread and butter. I'm going to clear in saying that it's a risky play, but my gut tells me it's a buy due to these alternative factors.

For further details see:

BuzzFeed: Oversold Beyond Its Prospects