BWLLY - BW LPG: Still An Attractive Choice For The Income-Oriented Investor

2023-08-13 03:49:24 ET

Summary

- BW LPG, the largest owner and operator of VLGCs globally, has a strong balance sheet, fuel-efficient fleet, and excellent management, making it an attractive investment for income-oriented oil and gas investors.

- Despite a gloomy outlook at the start of the year, robust freight rates and increasing demand in China and India have supported BW LPG's ability to pay dividends consistently.

- Although a significant expansion of the global VLGC is expected in 2023, this is offset by a backlog of special surveys and fully booked shipyards, suggesting rates will likely remain high.

Editor's note: Seeking Alpha is proud to welcome Soroya Investments as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

BW LPG's ( BWLLF , BWLLY ) strong balance sheet, predictable dividend payout history, fuel-efficient fleet, and excellent management provide a great case for the income-oriented oil and gas investor. Its 15 LPG-powered self-owned enjoy a TCE premium over VLSFO-powered vessels. With a cash breakeven of $23,100 for FY2023, according to its latest quarterly report, BW LPG has great dividend potential, considering freight rates in 2023.

LPG is an essential part of the energy mix and is only becoming more relevant as large markets such as India seek to reduce their emissions. Significant producers such as the U.S. are forecasted to increase their exports over the following years.

The geographical distance between where LPG is produced and consumed will continue to drive shipping demand. In one of its latest reports, Oil 2023 , IEA forecasts that during 2022-2028 90 percent of global demand growth for oil products will be provided by Asia-Pacific. In contrast, North American demand is forecast to peak in 2023. LPG demand is forecast to be 1.2 mb/d over the forecast period. As North America is a large producer of LPG, increased Asia-Pacific consumption will further increase demand for LPG shipping.

BW LPG offers the lowest leverage ratio and, in my view, an excellent dividend track record; it has the largest LPG dual-fuel powered fleet and the most extensive fleet overall compared to its peers.

Consequently, an investor with a positive outlook on LPG shipping should consider BW LPG and carefully evaluate its risks.

Introduction

My investment philosophy is finding undervalued stocks with a proven dividend track record. In this analysis, I will show that BW LPG's current share price is undervalued relative to its peers and that the company is in good shape to continue its predictable dividend in the future. I have divided the analysis into two main parts:

- In the first part, I will look at market dynamics and outlook for LPG shipping.

- In the second part, I will do a peer comparison to show that, in my view, BW LPG is the better choice for an investor sharing my positive outlook on the future of LPG shipping.

Market Dynamics And Outlook

Demand Side: Despite The Gloomy Outlook At The Beginning Of The Year, Rates Have Remained High

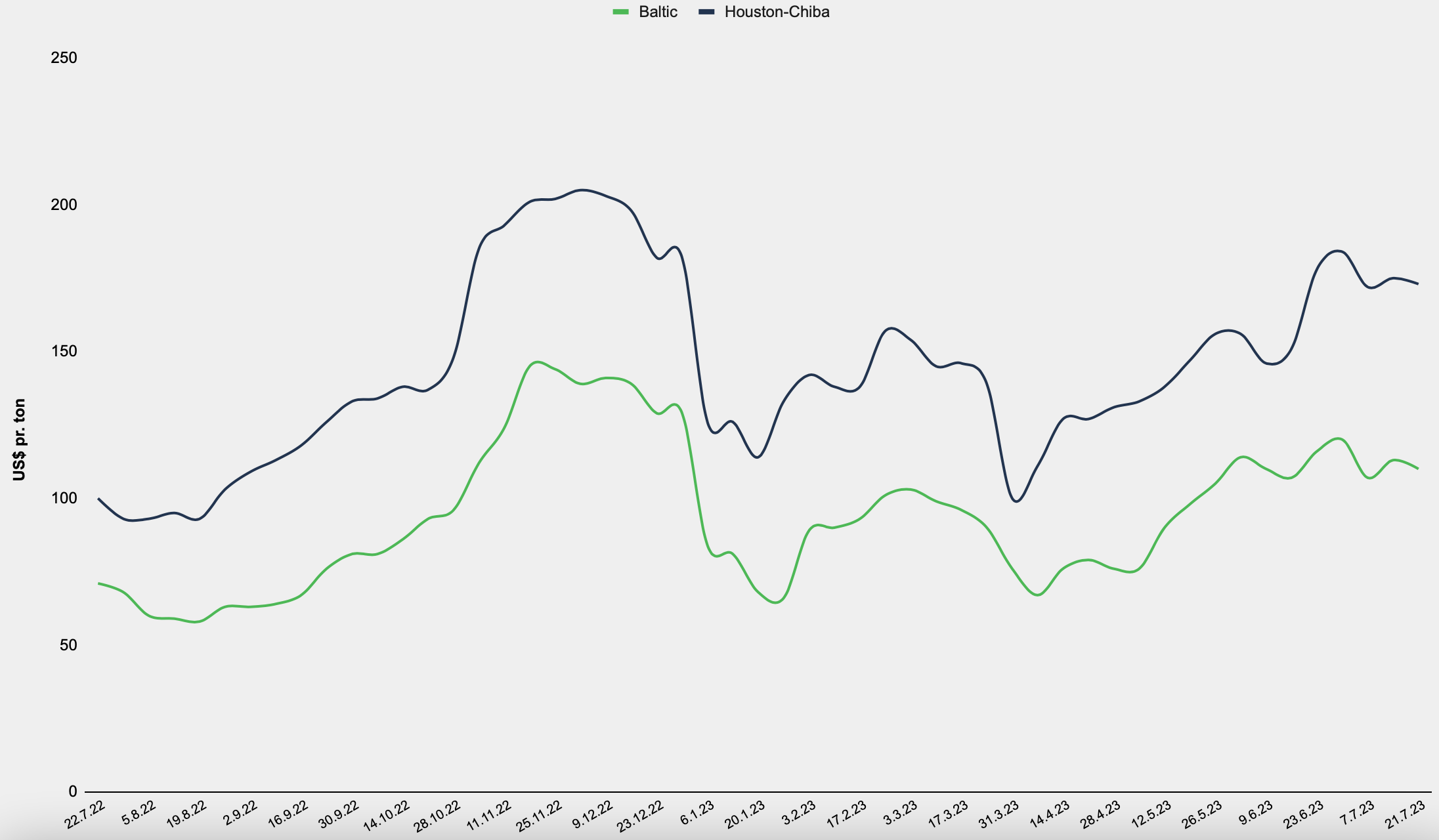

2022 concluded with robust freight rates, pushing the Houston-Chiba rate to $205 per metric ton. Banks collapsing in the U.S., a slow start in China, and a possible recession on the horizon contributed to a generally negative outlook for LPG stocks. However, to the extent those factors did contribute, their effects have not been reflected in BW LPG's share price, freight rates, and, ultimately, the company's ability to pay dividends to its shareholders. The share started the year at its lowest point, reaching NOK 66.25 on January 4. From then until late July, it's been a steady incline to its current share price of NOK 103.

Chinese demand is expected to increase as PDH plants come online, and Indian domestic demand is expected to continue its growth, buoyed by governmental subsidies. In its Oil 2023 report, referenced in the investment thesis above, IEA forecasts that global demand for LPG will grow in the Asia-Pacific region and remain flat or with modest growth in North America and Europe. These factors will likely support rates as this increases ton-mile demand.

Its peer Avance Gas provides this freight rate chart on its website , showing reference rates for the Baltic Exchange and Houston-Chiba transports:

Weekly freight rates, selected routes, last 52 weeks (Avance Gas website)

{kind=link}

After declining during the first quarter, rates continued upward during the second quarter. One month into Q3, rates have continued increasing. For the past three weeks, rates have been stable at about $172-175 per ton on the Houston-Chiba transport.

After BW LPG's stellar first quarter, this rate development bodes well for its ability to create shareholder value in the future.

Supply-side: Global Fleet Expansion Offset By The Backlog Of Drydocking And Special Surveys - And Shipyards Are Fully Booked Until H2 2026

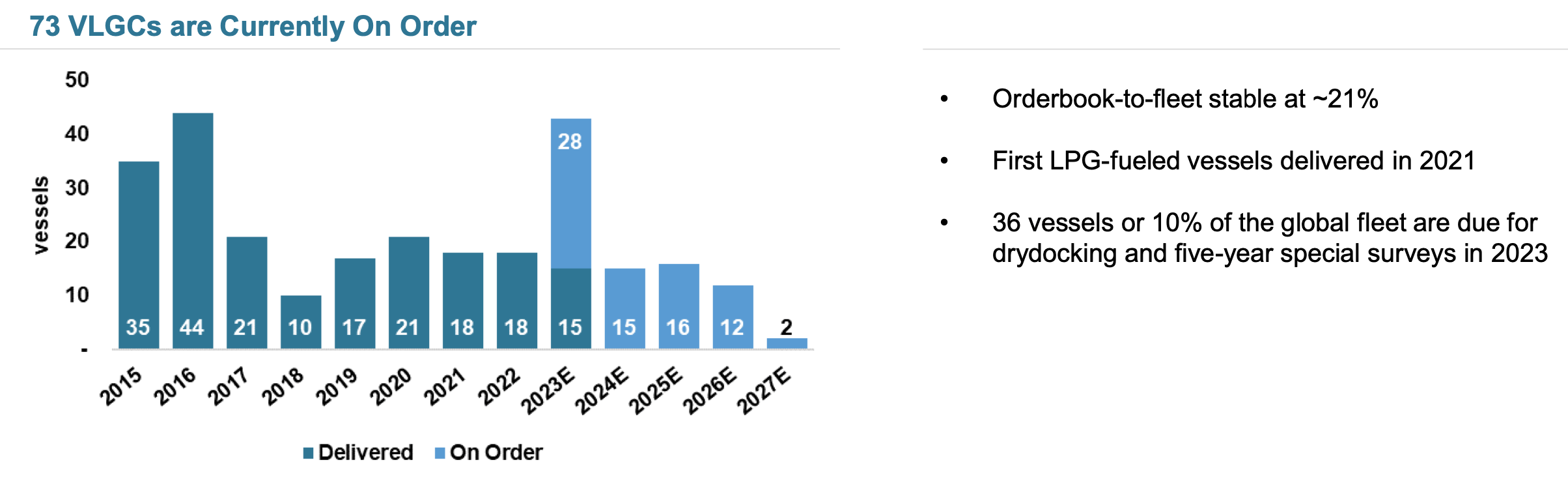

43 new builds are expected to enter the market this year. However, according to Dorian's investor presentation (June 2023), no less than 36 vessels are due for drydocking or special surveys, almost offsetting new carrier capacity entering the market. Dorian's investor presentation of June 2023 offers this illustration:

VLGC order book (Dorian LPG investor presentation of June 2023 (p. 24))

{kind=link}

In other words, 2023 is expected to be a year of unusually many new builds entering the market, while at the same time, a significant portion of that added capacity will be offset by drydock inspections. These are expensive and time-consuming, yet shipowners have no choice but to have their ships inspected, as class societies require them to be completed on time. A vessel must be in class to create revenues. According to the same investor presentation, more ships are expected to perform special surveys next year.

It is pertinent to add that shipyards are currently fully booked until 2026, according to BW LPG's Q1 presentation (p. 6) . Adding more vessels to the market will be more challenging during the next three years (2024-2026).

These two combined factors - sold-out shipyards and many ships due for inspection - mean that adding net VLGC capacity to the market will take much work for the next two years.

Market Risks

Ultimately, BW LPG's ability to drive dividends depends on the market rates it can secure. As we saw earlier, the company lost money and did not pay dividends for two years in 2017 and 2018. China, the U.S., and India are the world's top consumers of LPG. Since the USA is also the biggest producer, with about 40 percent market share, the important markets in terms of exports are China and India. Unfavorable economic developments in these two markets will negatively affect freight rates and BW LPG's earnings. There is also some political risk for India, considering domestic consumption is a significant demand driver. As India seeks to reduce its emissions footprint, LPG is a critical component in its drive to move away from wood as a source of heating and cooking. Governmental subsidies help this, and policy changes may have adverse effects on demand and, thus, freight rates. Also, supply shocks in the U.S. may affect rates negatively, as declining inventories might cause the U.S. to lower its exports.

BW LPG's stock trades on the Oslo Stock Exchange and is denominated in NOK. Depending on location, some investors may also find that trading stocks on the Oslo Stock Exchange come with prohibitive fees.

NOK, being the currency of a small economy, is a relatively illiquid currency. It has had a much more volatile three years than USD. The standard deviation of the USD/NOK index is 0.94, while the standard deviation of the USD/DXY index is 0.46. One can confirm that these are different by employing an F-test.

Please look at the following chart, which shows this difference in volatility graphically. The swings in USD/NOK (thick black line) are more significant, especially in periods of volatility (March 2020 being the most evident).

Exchange rate development, selected currency pairs, Jan 1, 2020 - July 14, 2023. Jan 1, 2020, = 100. (Author's calculations. USD/NOK rates are sourced from The Central Bank of Norway's data archive. USD/DXY sourced from Yahoo Finance.)

{kind=link}

Daily exchange rates were sourced from The Central Bank of Norway's data archive and Yahoo Finance to create the chart above. Jan 1, 2020 was indexed to 100 for both currencies, and the change in each subsequent observation was computed. Finally, the result was plotted as the line graph shown above.

Peer Comparison

The approach will be a peer comparison using the following multiples:

- EV/EBITDA and P/E

- Net debt to EBITDA

- Dividend payout ratio and yield

I have selected Avance Gas and Dorian LPG as peers I am comparing to BW LPG, as these companies have similar business models, and their main focus and source of income is VLGC shipping. According to its Investor Tools page , BW LPG considers Avance, Dorian, and Navigator Holdings its peers. In this analysis, I have excluded Navigator as it does not operate VLGC; instead, it uses a fleet of smaller gas carriers (<39,999 cbm) and does not pay dividends. According to fleet lists published on their websites, these three companies own or operate 86 vessels, comprising almost a quarter of the world's VLGC fleet.

BW LPG is, to my knowledge, the world's largest owner-operator of Very Large Gas Carriers (VLGCs), controlling a fleet of 45 vessels. According to Dorian LPG's investor presentation of June 2023 (p. 24), the world VLGC fleet currently has 353 ships, meaning that BW LPG controls more than 12 percent of the world fleet.

One final note before dividing into the peer comparison: Dorian LPG's fiscal year deviates from the calendar year. Its fiscal year runs from March through February next year. I will refer to quarters of the calendar year in this analysis. For example, Dorian reports Q1 2024, while BW LPG and Avance Gas report Q2 2023. When BW LPG and Avance report Q3 2023, Dorian says Q2 2024.

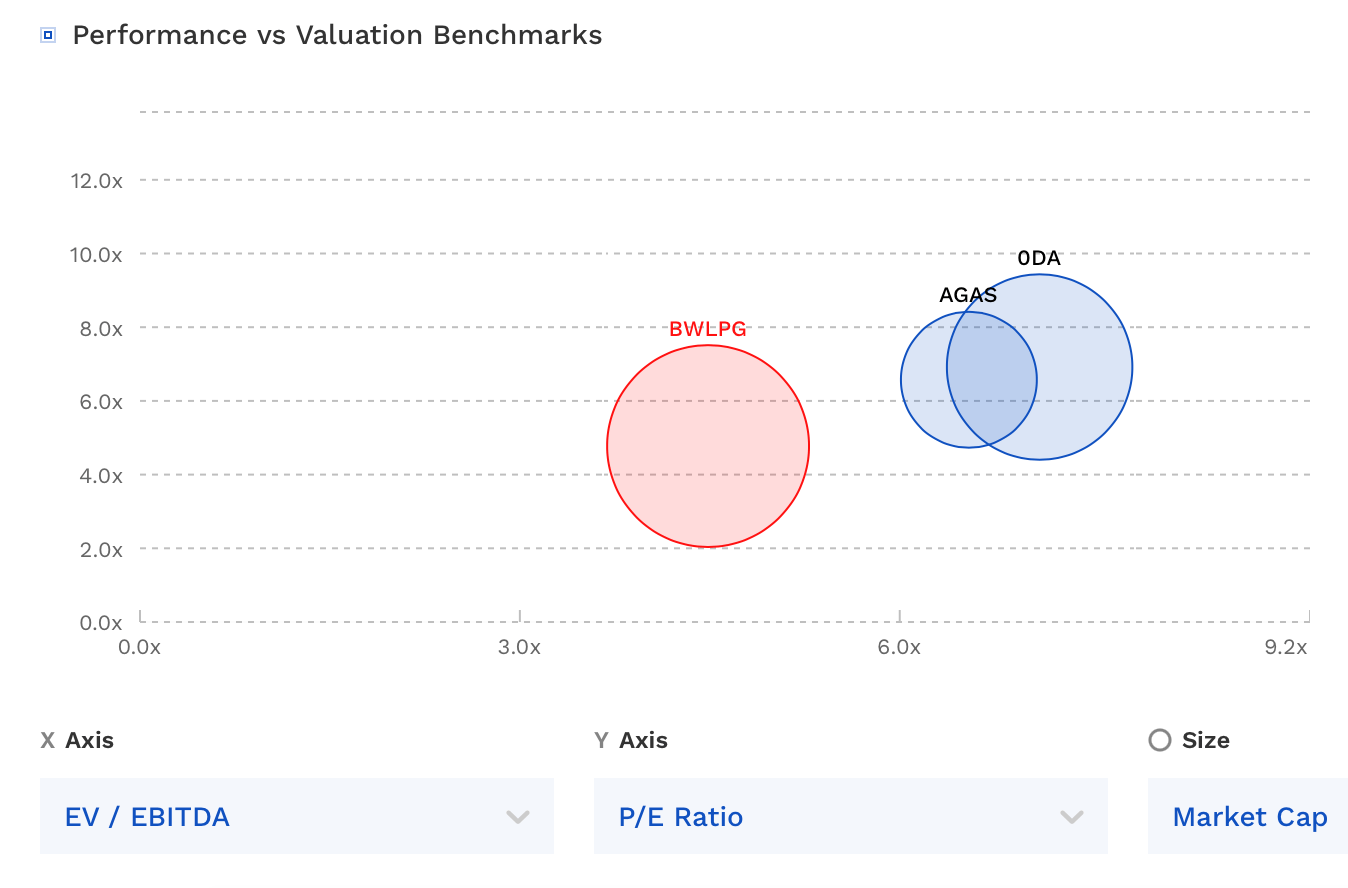

BW LPG Lower In Both EV/EBITDA And P/E

We'll begin by looking at the EV/EBITDA and P/E multiples. The chart below shows that BW LPG trades at an EV/EBITDA of 4.5, compared to Avance GAS and Dorian (0DA in the chart below) trades at 6.5 and 7.1, respectively.

The P/E ratio for BW LPG is 4.8, lower than Avance Gas' 6.6 and Dorian LPG's 6.9.

EV/EBITDA and P/E for BW LPG, Avance Gas, and Dorian LPG (Finbox)

{kind=link}

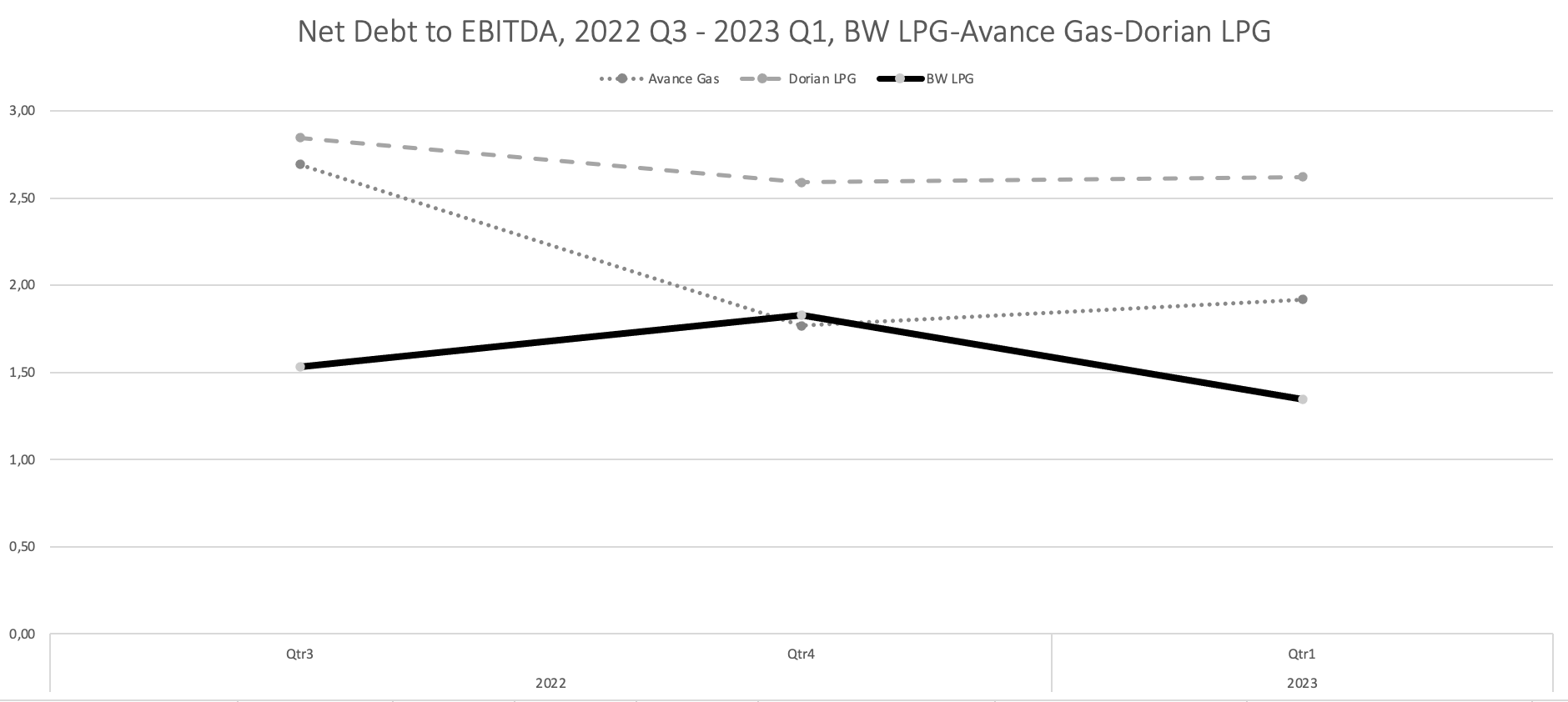

Net Debt To EBITDA: Lowest Leverage Ratio Among Its Peers

The company has maintained its net debt to EBITDA ratio at levels lower than, or the lowest level of, its peers. The following chart shows this ratio over recent quarters:

Net debt to EBITDA, 2022 Q3 - 2023 Q1. The ratio is calculated as (debt minus cash and cash equivalents) divided by the sum of EBITDA last four quarters. (Author's calculations, based on BW LPG quarterly financial reports)

{kind=link}

To arrive at these figures, data was pulled from each company's quarterly reports, found on their websites, and put into the following table (all figures in USD):

Figures used to arrive at Net debt to EBITDA calculation (Author's calculations by using figures from quarterly reports)

EBITDA, total debt, and cash and cash equivalents figures were pulled directly from the financial statements. Then, the last four quarters of reported EBITDA were computed. Finally, for each row in the table above, the Net Debt to EBITDA ratio was calculated by using the following formula:

- (Total debt - cash and cash equivalents) / (EBITDA (4 quarters))

If EBITDA 4 quarters was a blank cell, the ratio was set to N/A.

Dividend Policy

BW LPG's dividend policy on its Shares and Dividends page states that the company targets a payout of 75 percent of net profits after tax ((NPAT)) in dividends when the net leverage ratio is below 30 percent. Also, when the net leverage ratio is below 20 percent, the company targets a payout of 100 percent of NPAT in dividends.

Overall, BW LPG states that it aims for a payout of 50 percent of NPAT annually. In my opinion, this is a straightforward and easy-to-understand dividend policy.

BW LPG reported its net leverage ratio at 21 percent in Q1 2023. The board still decided, however, to declare a dividend of 100 percent of NPAT in dividends, which amounted to a DPS of $0.75.

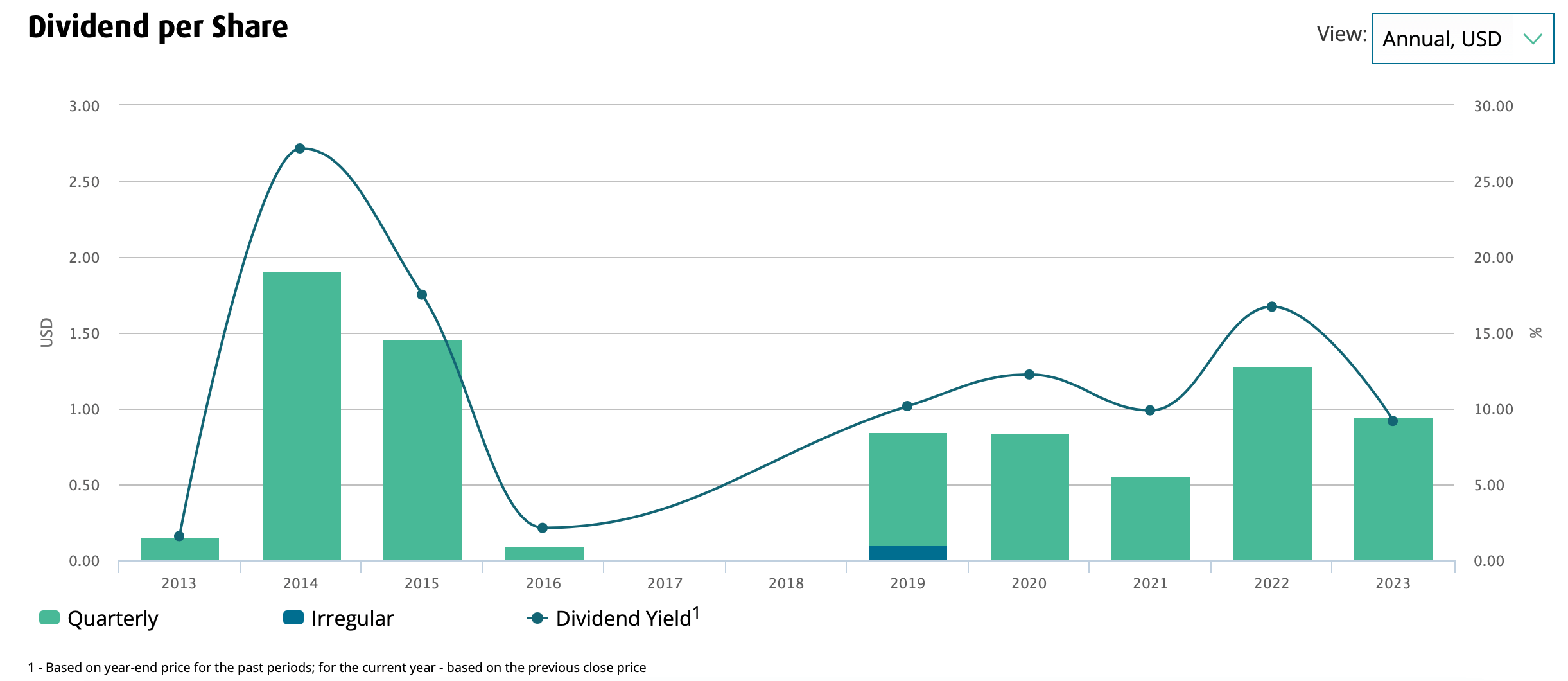

The following chart, borrowed from the Shares and Dividend page mentioned above, illustrates its dividend history over the past few years:

BW LPG dividend history since IPO (2013-2023) (BW LPG investor relations pages)

{kind=link}

After the lossmaking years of 2017 and 2018, the company bounced back in 2019. Since then, it has consistently been able to pay dividends.

Let's focus on how BW LPG's dividend compares to its peers by comparing its payout ratio and yields.

Dividend Payout Ratio: Showing The Dividend Policy At Work

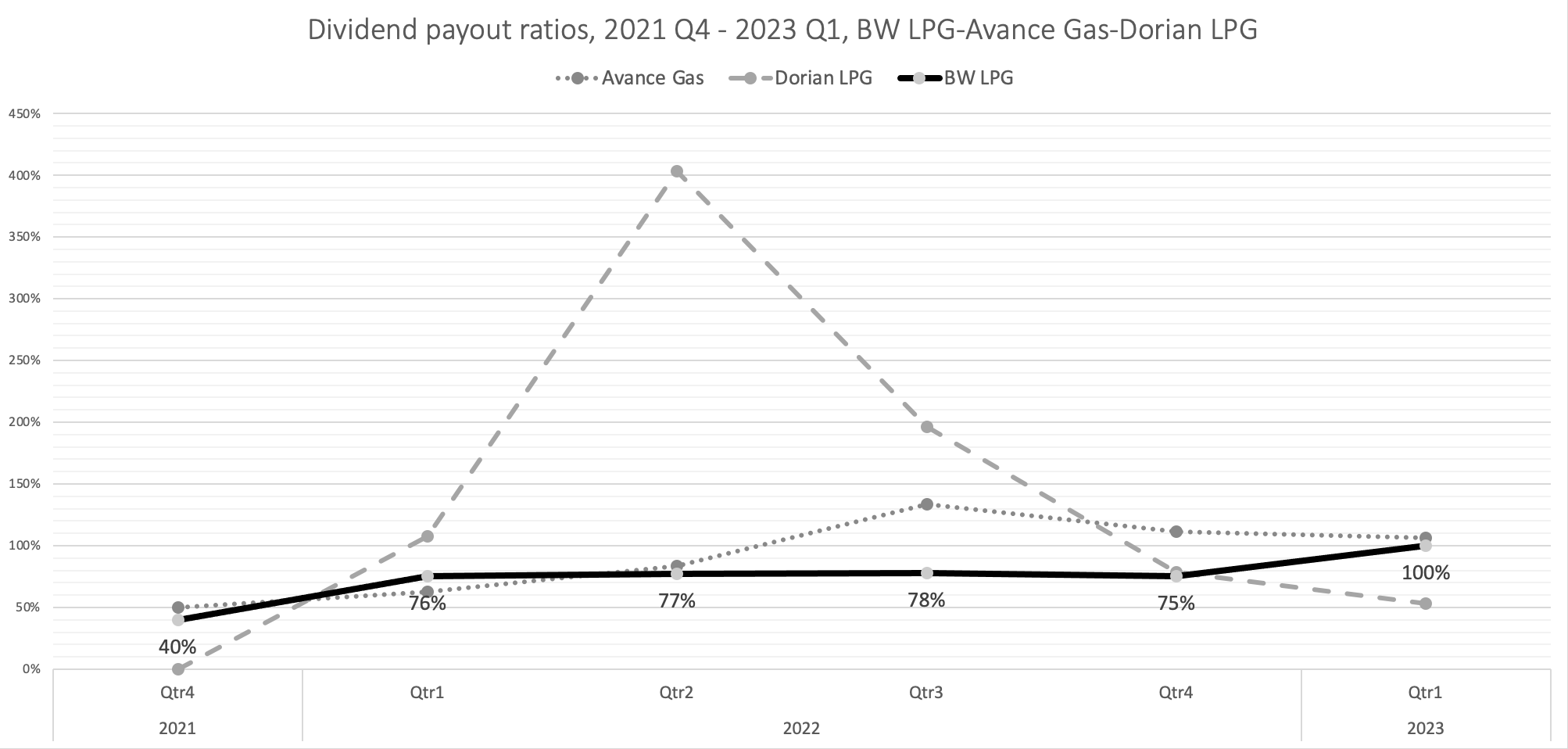

The following chart illustrates the dividend payout ratios of BW LPG and its peers over the last six quarters:

Dividend payout history Q4 2021 - Q1 2023. The dividend payout ratio is calculated as DPS divided by EPS for the quarter (Author's calculations based on quarterly reports)

{kind=link}

BW LPG has paid somewhat stable dividends quarterly. This contrasts with its peers Avance Gas and Dorian LPG, which have varied quite a lot in their dividend payout history. Compare BW to Avance Gas, which tracked BW's payout ratio closely during the first two quarters of 2022. In the latter half of 2022, however, Avance Gas' payout ratio exceeded 100 percent. Finally, Dorian paid massive dividends in 2022. As we can see from the chart has returned to more sustainable levels of 50-75% during Q4 2022 and Q1 2023.

Earnings per Share ((EPS)) and Dividend per Share ((DPS)) figures were pulled from each company's quarterly reports, available on their websites, to arrive at this result. The figures were then put into the following table:

Figures used to calculate dividend yields (Author's calculations based on figures pulled from quarterly reports)

The payout ratio was calculated for each row in the table by dividing DPS by EPS.

BW LPG Has Steadily Increased Its Dividend Yield

Turning our attention to dividend yields, the following picture emerges:

Dividend yield (trailing twelve months), 2022 Q3 - 2023 Q1. Yields are calculated as (the sum of dividends last four quarters) / share price at the end of the quarter (Author's calculations based on quarterly reports)

{kind=link}

BW LPG's dividend yield has steadily increased. Compare this to Dorian, whose massive dividends in the past year are reflected in yields exceeding 30 percent. The graph above gives off the impression of a declining yield.

To create the graph above, the following data was used:

Dividend yield calculations (Author's calculations using figures from quarterly reports)

- For each company, the share price at the end of the quarter was recorded and, for BW LPG and Avance Gas, converted to USD using the exchange rate at the same, sourced from the Central Bank of Norway's data archive referenced above.

- Then, each company's dividend per share figure was sourced from their respective quarterly reports on their websites.

- "DPS last four quarters" was calculated as a rolling sum last four quarters.

- Finally, the dividend yield was calculated by dividing DPS's last four quarters by the share price at the end of the quarter.

The table above also reveals Dorian LPG's somewhat hefty $2.50 dividend in Q2 2022.

Still Upside Potential In BW LPG Stock

On August 11, BW LPG closed at NOK 117.80 (USD 11.30). I believe NOK 150 (USD 14.45) is a reasonable target price based on a simple valuation using the dividend discount model:

Simple dividend discount model with growth valuation (Author's calculation)

{kind=link}

Let's review the basis for this calculation.

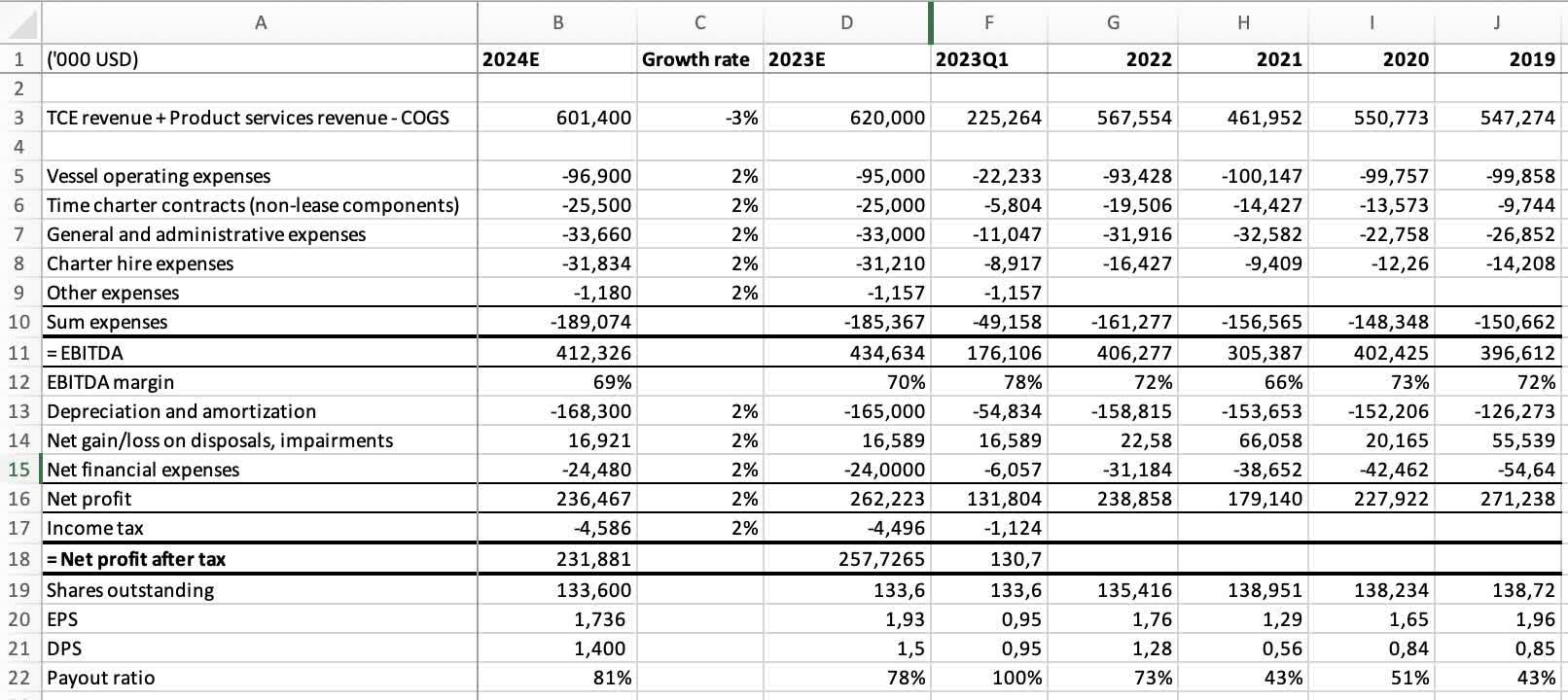

Next year's USD 1.40 dividend was calculated based on the following figures. Using 2019-2022 FY data, averages were established. Then, Q1 2023 figures were extrapolated to FY 2023 figures. Finally, FY 2023 figures were used to forecast 2024 figures. Ultimately, this exercise results in the USD 1.40 DPS figure in cell B21.

Valuation calculations (Author's calculations based on annual and quarterly reports)

{kind=link}

- Revenues : As can be deduced from the change in TCE revenues, I believe rates will cool somewhat but remain high. Rates seen in 2023 are relatively high, looking back five years, and due to the factors mentioned previously in this article, I expect that to continue.

- Expenses : I've extrapolated only minor changes from 2022 levels, resulting in an expected EBITDA margin of 69% for the 2024 estimate. This is a conservative estimation compared to previous years.

- Payout ratio : The company is currently (end of Q1 2023) reporting its net leverage ratio at 21 percent. Though with some cooling off in rates, I expect the favorable market to continue, enabling BW LPG to continue executing its returns-focused investor strategy.

- To achieve that, I assume that BW LPG will keep its fleet size more or less stable, as there are no meaningful commitments to expand the fleet.

As can be seen in cell B21, this results in a forecast DPS of USD 1.40 for 2024.

To arrive at the required rate of return, a simple CAPM calculation was used:

Estimation of the required rate of return (Author's calculations)

{kind=link}

I use a 5% risk-free return and estimated BW LPGs beta at 1.1. I used daily closing prices for BW LPG stock and the OSEBX (Oslo Stock Exchange Benchmark Index) for the past two years (Aug 10, 2021 - Aug 9, 2023) to calculate the beta (Oslo Stock Exc.

Finally, a world GDP growth of 3 percent is assumed for the dividend growth. We end up with the following variables that I plugged into the dividend discount formula above:

- Dividend next year: USD 1.40

- The required rate of return for BW LPG stock: 12.7%

- Long-term growth rate: 3%

In conclusion, this calculation yielded a target price of approximately NOK 150 (USD 11.30).

Company-specific Risks

During the summer, both the CEO and CFO of BW LPG announced their departures from the company.

- On July 6, the company announced the departure of its long-standing CEO, Anders Onarheim, effective September 30, 2023. Mr. Onarheim has been with the company since 2010 and its CEO since 2020. He will be succeeded by Kristian Sorensen, currently deputy CEO and Head of Strategy. Mr. Sorensen joined the company on September 1, 2022.

- On May 26, CFO Elaine Ong stepped down , effective immediately. However, just one week later, the company announced that Samantha Xu would join BW LPG as its new CFO.

What to make of this management shuffle?

According to its press release, Mr. Onarheim and Sorensen have worked closely together, which "will provide a seamless transition," according to chairman Andreas Sohmen-Pao. In addition, delaying his departure until September 30 gives off the impression of a planned CEO succession. Mr. Onarheim's next venture has yet to be discovered. He is, however, chairman and member of the board of several companies.

Ms. Ong's sudden departure could be a cause for concern. Ms. Ong had been with BW LPG for 12 years and had completed the Vilma LPG integration into BW Product Services. Perhaps she merely thought that her job at BW LPG was done and wanted to do something else, but wouldn't a more prolonged departure make for better optics if that was the case?

It's not unusual to see CFOs resigning in the wake of bad news, and a CFO suddenly leaving could indicate a worsening situation inside the company. I have yet to track down any concrete information as to why Ms. Ong left with immediate effect, so I will instead consider BW LPG's recent performance and press releases. As shown above, BW LPG has reduced its debt load and grown its dividend. Q1 2023 was a record quarter for the company.

The fact remains that two central executives, who have been with the company through the recent boom years of 2020-2023, have left in a short time.

Conclusion

After 2022 ended with record rates, VLGC owner-operators continued posting solid results in Q1 2023. Unfortunately, a looming banking crisis, recession fears, and a historically large order book were causes for concern in March and April, causing rates to decline. BW LPG's Q2 results will probably suffer slightly from the market dip in March and April, which caused the company to sell about 90 percent of available Q2 days at a TCE of $50,000/day. A pertinent decision, given the market outlook and the time, but since then, rates have again approached $100,000/day. However, the forward rates have increased since, and Q3 should be better.

The departures of the CEO and CFO during the summer warrant closer scrutiny of the company in the coming months to decode any underlying message. Were these departures merely coinciding in time, or were they signs of trouble ahead?

Still, with its large fleet, low capital expenditure, low net leverage ratio, and excellent dividend track record, BW LPG's fundamentals show that it still is a good candidate for the income-oriented investor.

For further details see:

BW LPG: Still An Attractive Choice For The Income-Oriented Investor