CIXPF - CaixaBank: Bankia Integration Should Boost ROTE To 12% By 2024

2023-03-18 11:35:00 ET

Summary

- CaixaBank is the largest bank in Spain, with the No. 1 position in several of its core divisions.

- The EPS in 2022 came in above 40 cents per share, and this should grow to in excess of 50 cents by 2024, indicating a forward P/E of 7.

- CaixaBank uses a 50%-60% payout ratio for its dividends. This results in a current yield of 6.5% (subject to the 19% Spanish dividend withholding tax).

- The entire European banking sector is cheap. But CaixaBank definitely belongs on my watch list while I wait to see how the current banking crisis plays out.

Introduction

Although CaixaBank (CAIXY) (CIXPF) isn't the largest Spanish bank, it's the largest bank in Spain. While Santander (SAN) and BBVA (BBVA) are larger, they mainly focus on their foreign operations in emerging markets while Caixa tends to focus on its domestic market . Earlier this decade, the bank merged with Bankia to create a large player on the Iberian peninsula.

{kind=link}

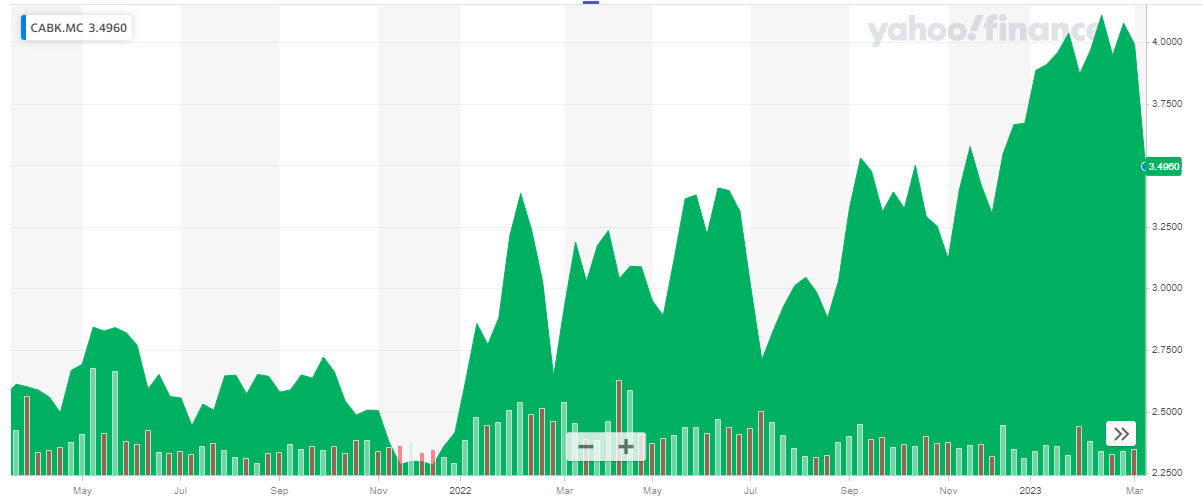

The main listing of CaixaBank is on the Madrid Stock Exchange where the bank is listed with CABK as its ticker symbol . The average daily volume in Madrid is approximately 12 million shares to the Spanish listing, which clearly is the most liquid trading venue. At 3.50 EUR per share, the current market capitalization is approximately 25B EUR.

2022 was generally a good year

Despite the recent 15% decrease, Caixa's share price is currently still trading more than 60% higher compared to the 2.24 EUR per share it was trading at when my previous article on this Spanish bank name was published.

{kind=link}

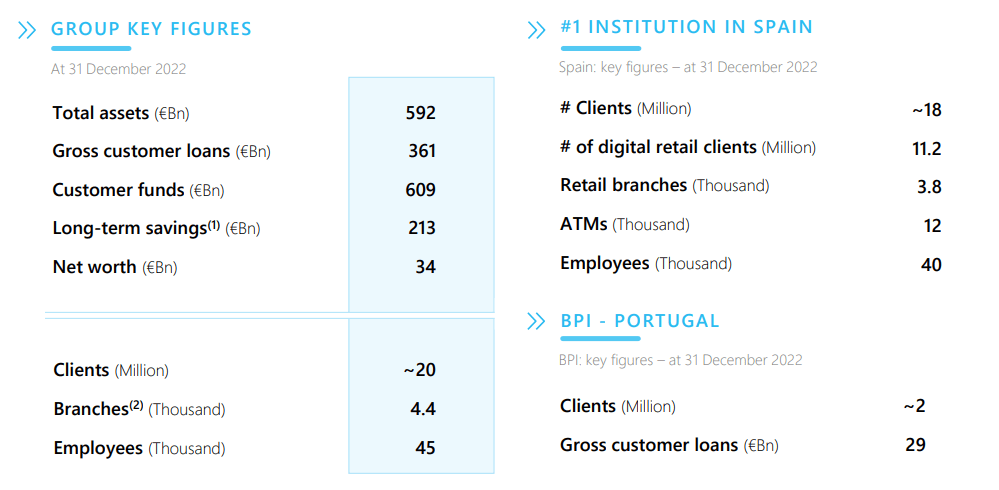

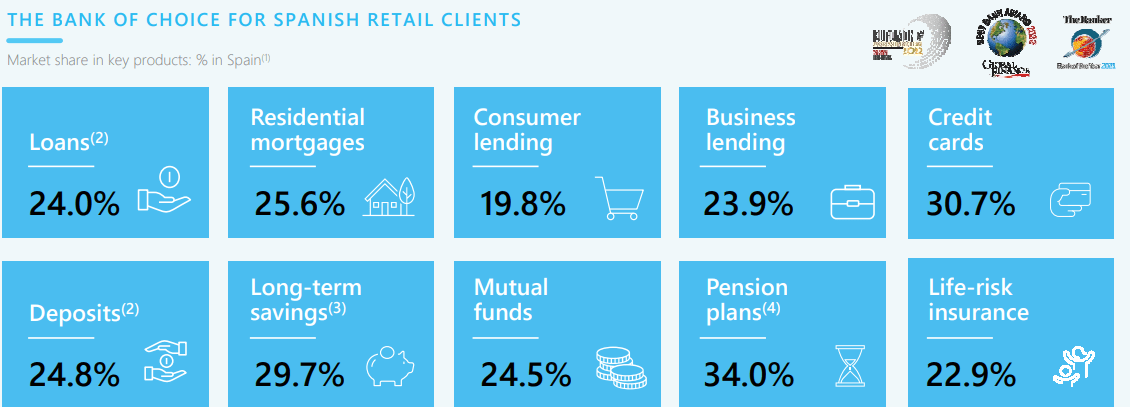

The bank has solid market shares in pretty much every domain of the banking system and is the undisputed leader in Spain. Perhaps surprising for investors from outside of Spain as not Santander or BBVA but CaixaBank is the number one in Spain .

{kind=link}

Despite shrinking its balance sheet in 2022 (the bank had too much cash and deposits that it couldn't put to work after the merger with Bankia), CaixaBank's "right-sized" operations saw the net interest income increase despite having a lower amount of interest-earning assets.

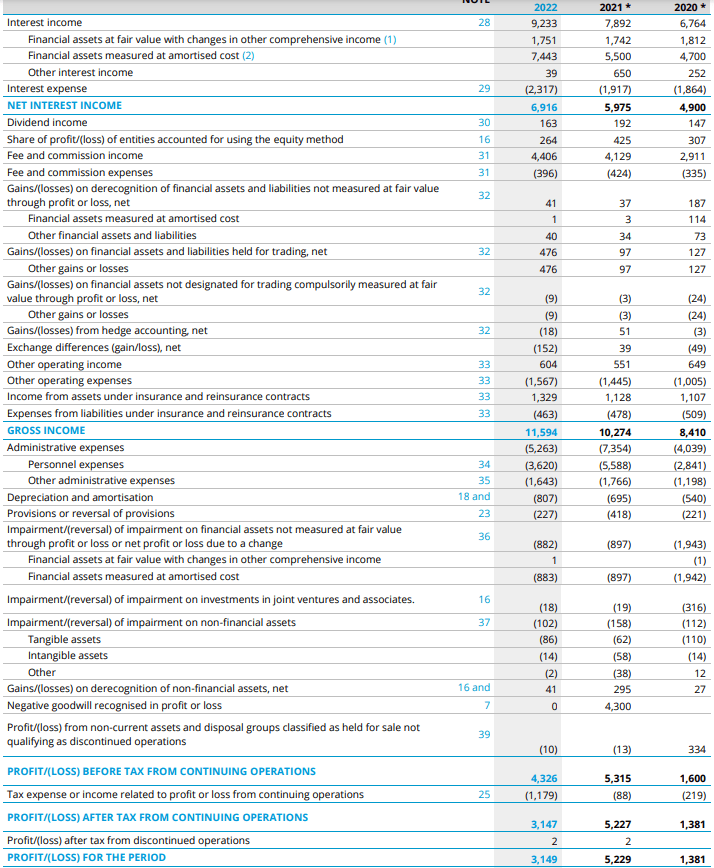

As you can see on the image below (you can click on it to expand), the net interest income increased from less than 6B EUR in 2021 to almost 7B EUR in 2022 and this fueled the total net revenue which came in at 11.6B EUR (the "gross income" mentioned in the income statement below). And while the pre-tax income decreased from 5.32B EUR to just 4.33B EUR , the income statement clearly explains what happened.

{kind=link}

During 2021, CaixaBank had to complete the integration of Bankia, the acquisition of the other Spanish bank. This resulted in two important elements: First of all the total amount of administrative expenses skyrocketed from 4B EUR in 2020 to 7.4B EUR in 2021. We see this came back down again to a more normalized 5.3B EUR in 2022. On the other hand, the 2021 result was boosted by a 4.3B EUR "negative goodwill" which basically is the reversal of an impairment charge. Excluding these two items, the pre-tax income in 2021 would not have been 5.3B EUR but somewhere in the 3-3.5B EUR region and that makes an exact comparison pretty difficult.

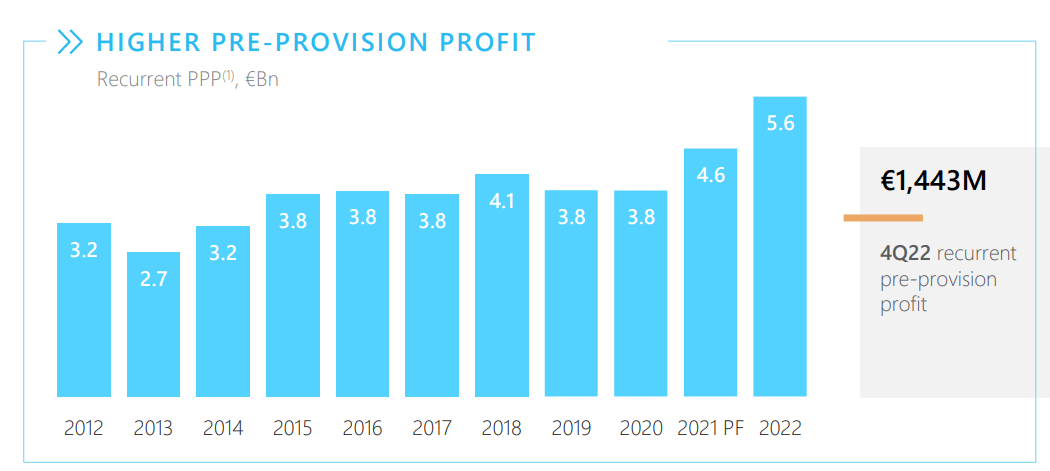

The bank did make an effort to filter out the non-recurring items, and the image below clearly shows the sharp increase in the pre-provision profit.

{kind=link}

In any case, the reported net income in 2022 was 3.15B EUR of which a few million Euro was attributable to non-controlling interests. The EPS was approximately 42 cents per share and the company will pay a 23.06 cent dividend which represents a payout ratio of 55% which is right in the middle of the anticipated payout ratio of 50%-60% (which was reconfirmed for this year). It also is a 58% increase compared to the dividend payment last year.

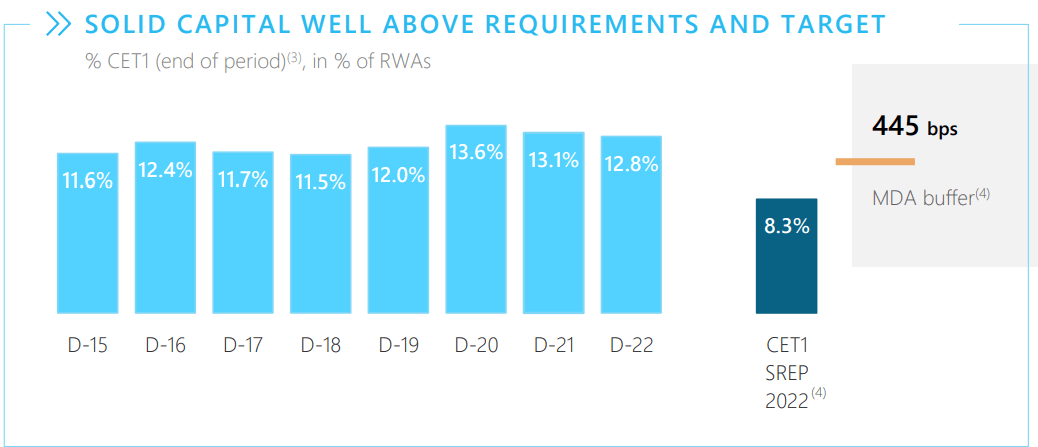

The Spanish banking sector does not really have the best reputation as the sector was hit hard in the Global Financial Crisis and had to deal with the sovereign debt crisis just a few years later. Fortunately Caixa's CET1 ratio is relatively high, and substantially higher than what's required by the regulators.

{kind=link}

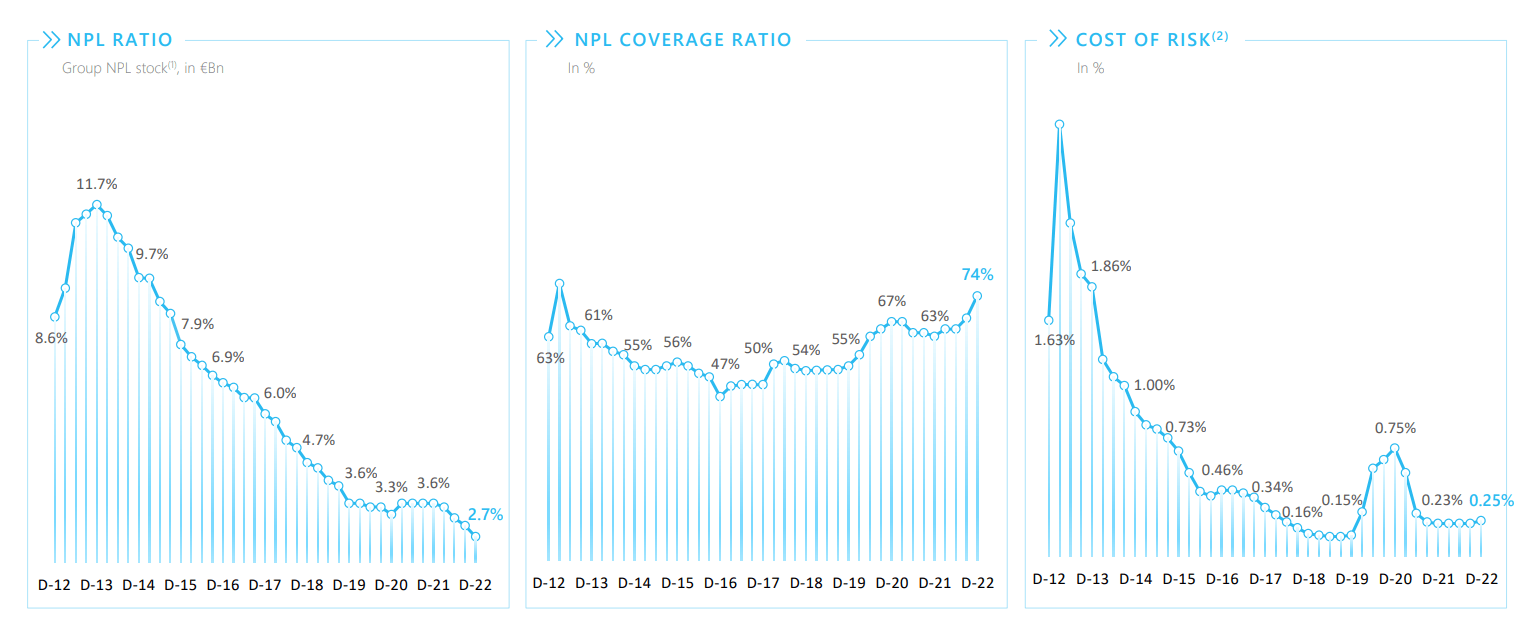

The strong capital ratio was helped by a substantial decrease in the NPL ratio and the cost of risk while the NPL coverage ratio increased in the past few years.

{kind=link}

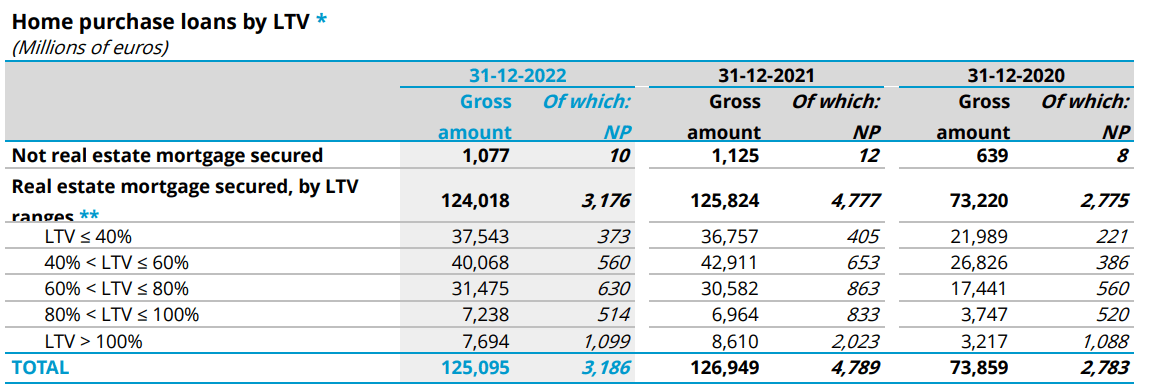

It's also interesting to see almost 40% of the loan book consists of residential mortgages.

{kind=link}

And while residential real estate hasn't always been a painless experience in the past few decades as the housing market has experienced large swings in the past two decades, the average LTV ratio of these mortgages is actually pretty low. About 60% of the mortgages have an LTV ratio of less than 60% and just over 10% have LTV ratios exceeding 80%. Some of those loans will definitely need more attention but it's encouraging the total amount of non-performing loans in those high-LTV categories has decreased on a YoY basis.

{kind=link}

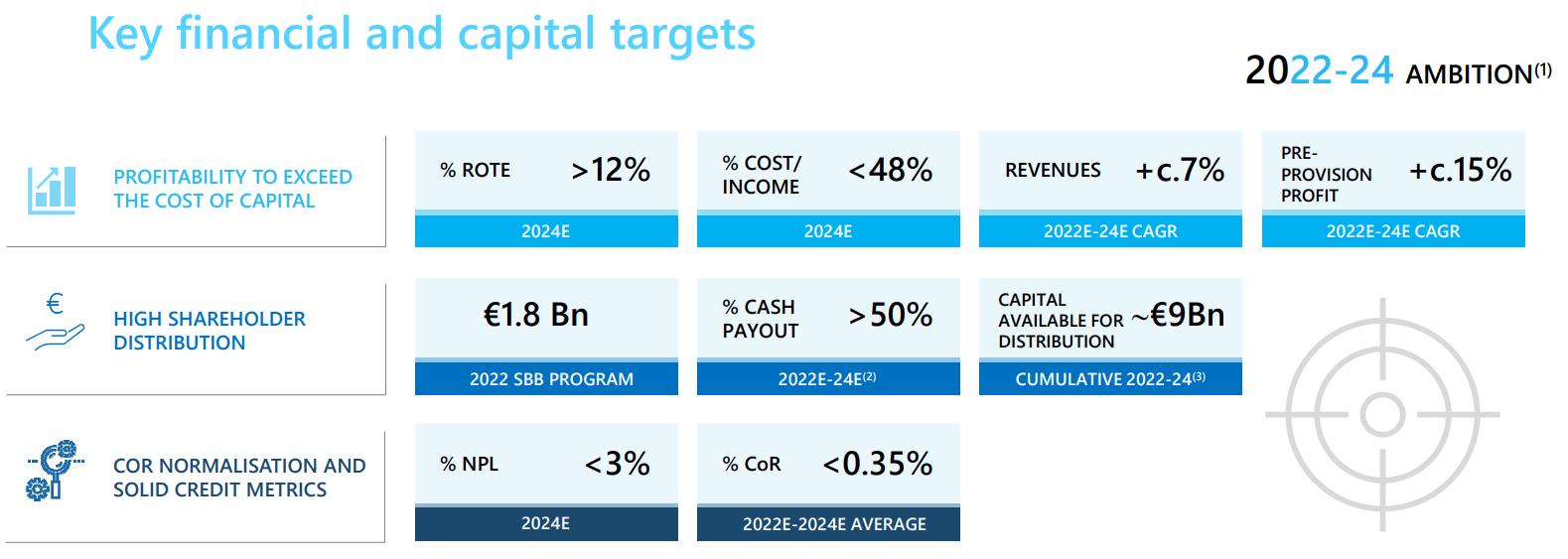

The bank expects to keep its loan loss provisions low as it targets a cost of risk of less than 0.35% in the 2022-2024 period. And as you can see below, Caixa expects to keep its payout ratio above 50% which should result in 9B EUR in cumulative dividends in the 2022-2024 era.

{kind=link}

And that's interesting guidance. There are currently approximately 7.05B shares outstanding, which means the cumulative capital available for distribution is almost 1.30 EUR per share. That's fueled by the anticipated 15% CAGR of the pre-provision profit. That's great, but given the recent turmoil on the markets this may now become a difficult target. The TBV is currently 3.82 EUR per share and if the bank retains 20 cents in earnings per share per year, the TBV will increase to approximately 4.20 EUR per share by the end of next year. Applying a 12% ROTE would subsequently mean the EPS will exceed 0.50 EUR per share towards the end of 2024.

Investment thesis

The entire banking sector is "on watch" after the Credit Suisse issues (the Silicon Valley and Signature Bank blowups should not have a major impact on the European banks but Credit Suisse is closer to home and is sending a ripple through the European market) but I'm quite impressed with how fast CaixaBank has been able to integrate the Bankia acquisition in its own corporate structure.

While I expect provisions for loan losses to increase, Caixa's net interest income will likely continue to increase albeit at a slower pace as the vast majority of its mortgages have a fixed interest rate. That's not really good news for the net interest margin but it also means its borrowers won't suddenly see their monthly payments spike which reduces the risk for defaults in the mortgage portfolio.

I currently have no position in CaixaBank anymore as I sold my position a little while ago. The stock looks attractive again at the current share price but the entire European financial sector is now attractive and trading at similar multiples. I will keep a close eye on CaixaBank as I'm hoping for a re-entry point but I will likely wait at least until the Q1 results are out so I can see how the bank's results are impacted by the current volatility.

For further details see:

CaixaBank: Bankia Integration Should Boost ROTE To 12% By 2024