CIXPF - CaixaBank: Cheap Despite A Sting From The Banking Levy

2023-06-03 02:04:11 ET

Summary

- Spanish player CaixaBank is benefiting from higher interest rates and strong asset quality, leading to a significant boost in near-term income and profitability.

- While the bank's net interest income and pre-provision profit are up significantly, the recently introduced banking levy is a drag on earnings growth and profitability.

- Despite this, CaixaBank shares look inexpensive, with a potential 25% upside to fair value.

A rising tide lifts all boats, and CaixaBank (CAIXY) (CIXPF) has certainly been getting a nice lift from higher interest rates and continuing strong asset quality.

Caixa's 2021 merger with Bankia now makes it the number one bank in Spain. Lacking the international diversification of peers means that the recently introduced banking levy will hit Caixa harder over the next couple of years - and possibly beyond that should the authorities decide to keep it on the statute book after 2024.

The banking levy is definitely a drag on an otherwise solid earnings growth story, but even so Caixa is still set for a big step-up in near-term profit. With that mapping into a double-digit return on tangible equity and a commensurate boost in capital returns to shareholders, these shares currently look inexpensive. Buy.

Interest Income Heads Higher

Caixa is now the largest domestic player in Spain following its merger with Bankia, sporting a circa 25% share in retail lending and deposit gathering. The bank does have some non-Spanish operations (~7% of FY22 income was from BPI, its Portuguese business) but for the most part this is a Spain-only player. That sets it apart from larger multinational Spanish banks Santander (NYSE: SAN ) and BBVA (NYSE: BBVA ), both of which have significant Latin American operations.

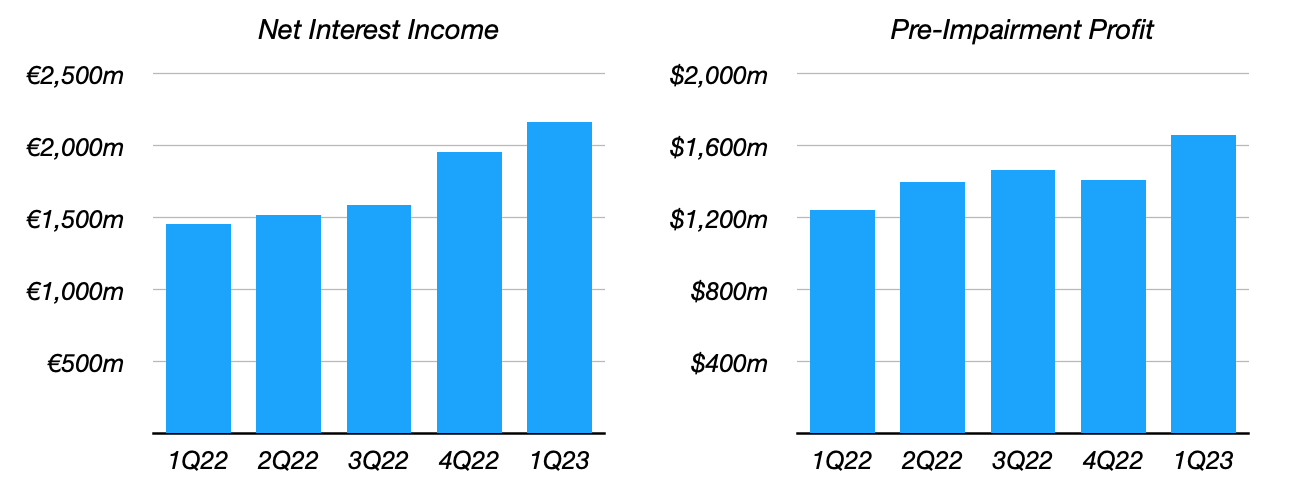

With interest rates headed higher in the Eurozone, Caixa has been seeing a nice boost to its net interest income ("NII") and pre-provision operating profit recently:

CaixaBank: Quarterly Net Interest Income & Pre-Impairment Profit

Data Source: CaixaBank Earnings Reports

{kind=link}

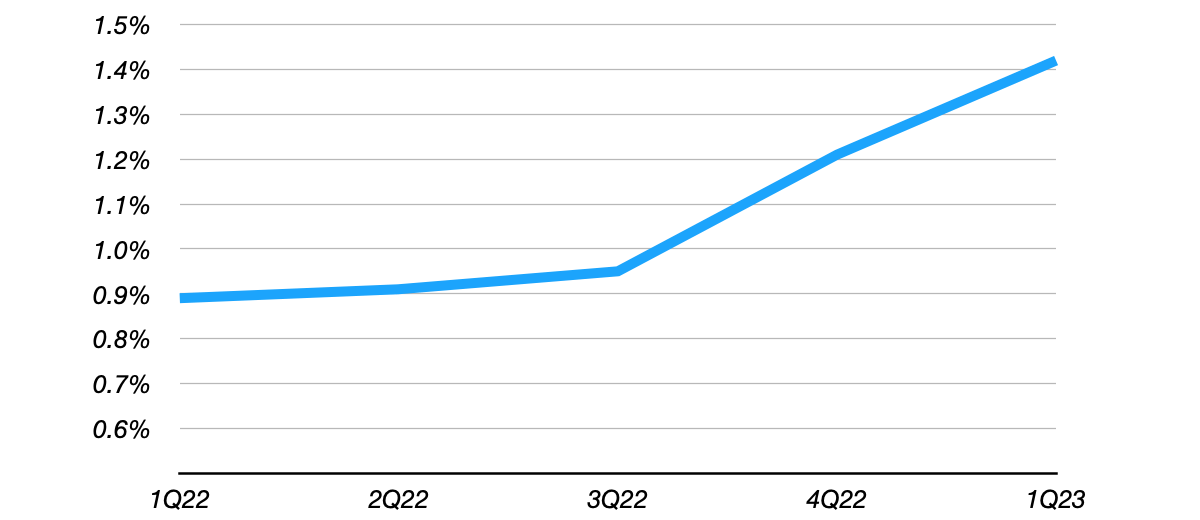

The bank does have some nice non-interest lines (it is a leading domestic composite insurer, for example), but NII still accounted for over 60% of core revenue as of Q1 2023. Higher rates have lifted the yield on its assets by around 117bps since Q1 2022, leading to a circa 59bps YoY rise in its net interest margin (to 142bps in Q1 2023):

CaixaBank: Quarterly Net Interest Margin

Data Source: CaixaBank 1Q23 Results Release

{kind=link}

Funding costs and deposit betas will rise going forward. Management expects it to end FY23 at circa 20%, rising to the "high 30s" in FY24, while the Q1 YoY rise in deposit costs was 34bps versus a circa 300bps rise in the Eurozone base rate over the same time. Worth noting, however, is that management hasn't seen the negative dynamics on deposits and funding costs that US regional banks have experienced recently. As per the Q1 2023 earnings call:

Basically, first of all, there has been no change in customer behavior as a result of the instability mainly in the US during the month of March and some of the recent news that's business as usual in terms of the behavior that's not having an impact.

Gonzalo Gortazar, CEO

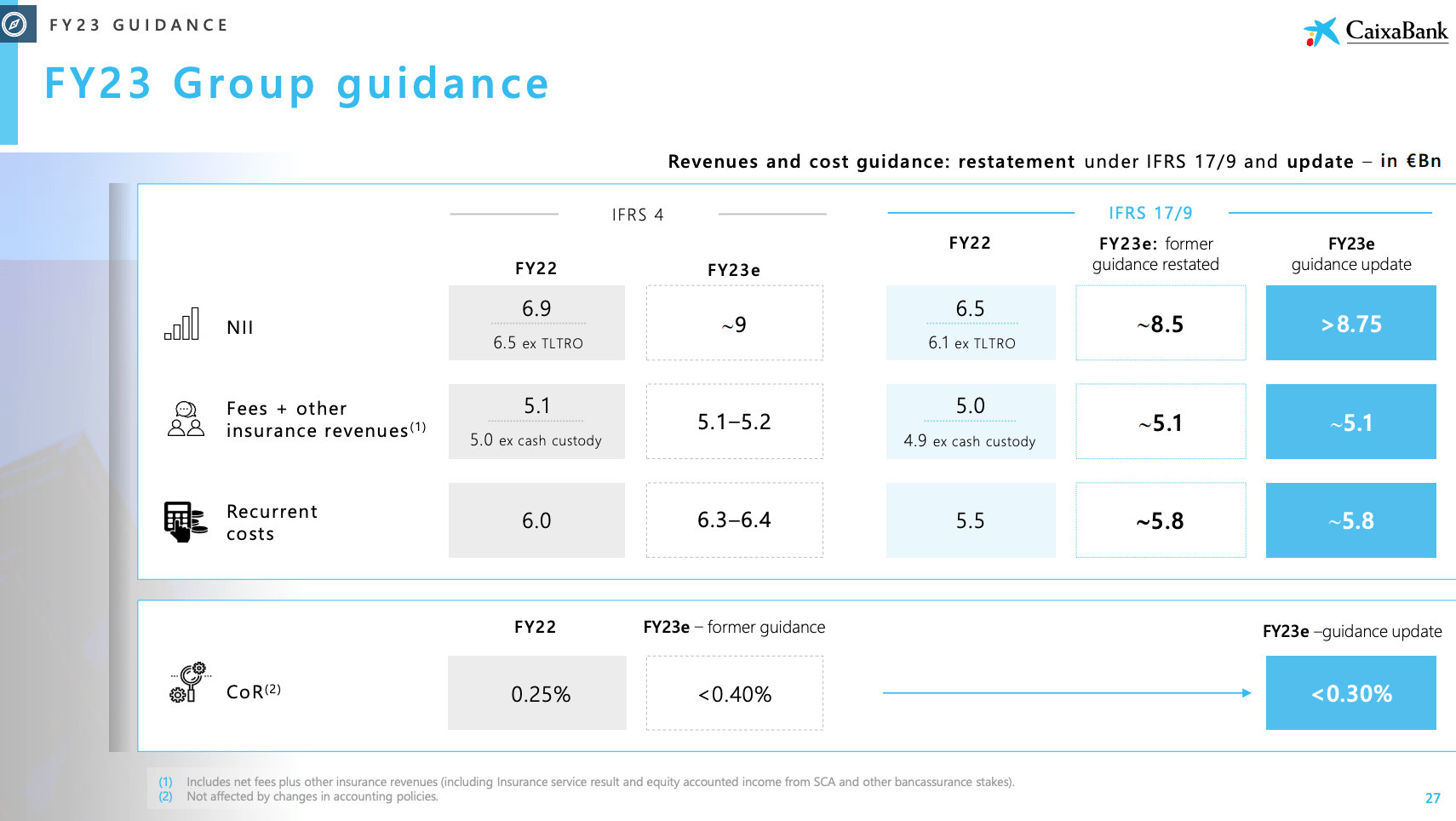

Indeed, management has actually upgraded group NII guidance by at least €250m to over €8.75B for FY23, which would represent circa 35% growth YoY (FY22 NII: €6.5B). On unchanged FY23 guidance of €5.1B in fees and insurance revenue and €5.8B in recurrent costs, I estimate this should be good for a circa 30% YoY rise in pre-impairment income (my FY23 estimate: €7.15-7.20B; FY22: €5.5B).

Asset Quality Holding Up Well

Asset quality is holding better than anticipated, and combined with higher operating income as per above this is pushing Caixa into double-digit return on tangible equity ("ROTE") territory.

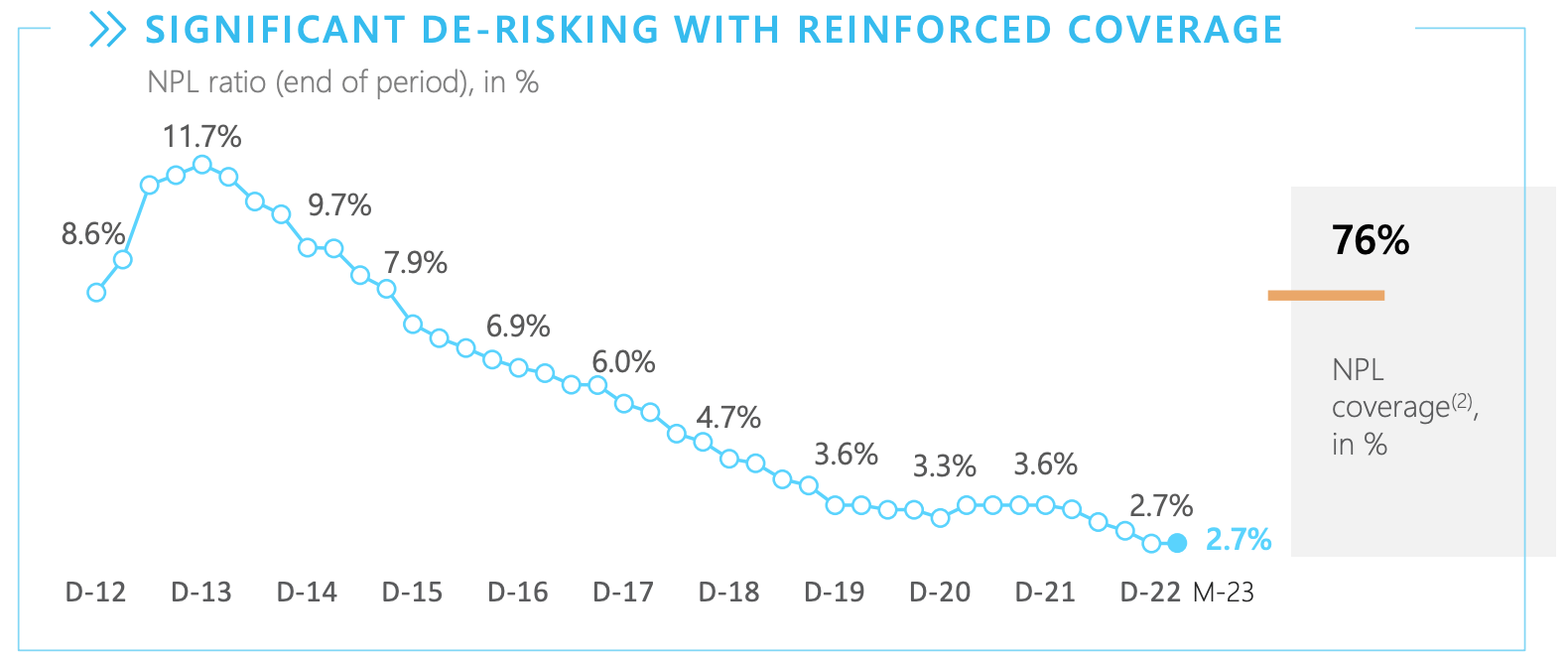

Q1 non-performing loans ("NPL") were actually down a touch sequentially to €10.5B (steady at 2.7% of total loans and contingent liabilities), and were down around €3B YoY (Q1 FY22 NPL ratio: 3.5%).

Source: CaixaBank 1Q23 Results Presentation

{kind=link}

Q1 cost of risk ("COR") did inch up 3bps sequentially, but at 26bps it remains relatively benign. Indeed, management also upgraded COR guidance, with FY23 COR now seen coming in below 30bps versus 40bps previously (FY22 and F21 COR: 25bps). Net income was strong in Q1 as a result, coming in at €855m, mapping to a trailing-twelve-month ROTE of 10.5%.

Asset quality has traditionally been a weak point at Caixa, but one thing I would note regarding that is that coverage levels are now also higher here. The Q1 FY23 NPL coverage ratio was 76%, up 2ppt sequentially and around 13ppt higher than it was at year-end FY21.

Earnings & Dividends To Head Higher, But Banking Levy A Drag

With management upgrading guidance on COR, net income will get a further boost this year. On €7.15-7.2B in estimated pre-impairment income I get to FY23 net profit of around €4B give or take (€0.53 per share).

Source: CaixaBank 1Q23 Results Presentation

{kind=link}

Management targets a 50-60% dividend payout ratio which, at the low-end, would result in a FY23 DPS of €0.265 per share. On a flat payout ratio (55% in FY22) the DPS would clock in at around €0.29 per share, or ~25% higher than the €0.2306 per share FY22 payout. Investors can expect strong dividend growth over the next year.

One thing I have yet to mention is the banking levy. The was passed by the Spanish parliament last year and basically levies a 4.8% tax on the sum of domestic NII and fee income of the large Spanish banks. Caixa is the most affected by this levy because it lacks the non-Spanish operations of bigger rivals Santander and BBVA.

At the moment, this levy applies temporarily in FY23 and FY24 (with tax based on results of the preceding year), however the government has pledged to look at whether to make this levy permanent in Q4 2024. It would be prudent to expect this to become a permanent feature of the Spanish banking landscape, but with Caixa challenging this in court there could be upside for investors if it wins.

Now, Caixa charged €373m to its pre-impairment income in Q1 in relation to the levy, which by my count represents a majority of the total due in 2023 (the remainder of which should be paid in Q3). Clearly this is a headwind for the firm, as the levy will rise significantly next year given the significantly higher NII guidance.

Some Upside To Fair Value

At €3.63 in Madrid trading at time of writing, CaixaBank shares trade for just under 1x tangible book value per share ("TBVPS"). The TTM dividend yield is 6.3%.

While the banking levy does depress ROTE versus what it otherwise would be, Caixa is still well on track to meet management's goal of 12%-plus ROTE in FY24 (indeed it should hit that this year). That would support a valuation closer to 1.2x TBVPS share in my view, implying a fair value of €4.43 per share ($1.58 per ADR) and around 25% higher than the prevailing price. This corresponds to an undemanding FY23 price-earnings ratio of 8.4 and a FY23 dividend yield of 6.5%, further lending support to the value case here. Buy.

For further details see:

CaixaBank: Cheap Despite A Sting From The Banking Levy