CM - Canadian Imperial Bank of Commerce: Grab The 6% Dividend Yield And Double-Digit Earnings Growth

2024-01-15 06:43:35 ET

Summary

- Canadian Imperial Bank of Commerce downgraded from Strong Buy to a Buy rating this time.

- Strong dividend case with a nearly 6% yield and proven growth over 10 years.

- Growth in revenue, earnings, and equity despite challenging environment for net interest margins.

- Risk impact of office loan exposure appears to be low, considering the size of overall loan portfolio.

Stock & Industry Snapshot

Since the Fed's last meeting in December, the banking sector has been getting added attention so today I'm revisiting a major Canada-based bank I rated last year: Canadian Imperial Bank of Commerce ( CM ) , also commonly known on the street simply as CIBC.

In my late-July coverage , I bullishly called this stock a strong buy , and it seems since then it has gone up around +4.6%:

CIBC - price since last rating (Seeking Alpha)

From key market data , we know that this sector has seen some bullishness lately, possibly pulling up this stock with it. For instance, it has grown by double-digits from 3 years ago, but also by almost 4% in 1 month:

financials sector market data (Seeking Alpha)

I would say to understand this industry it is a good idea to keep track of topics like interest rates and Fed decisions since they can impact the net interest income of banks.

Tracking equities and fixed-income markets also can tell us something about non-interest income these firms make such as fees on managing assets, and the growth in value of those portfolios can be affected by markets.

For instance, some quick facts about CIBC from their SA profile tell us they are around since the 1800s, trade on the NYSE but also on the Toronto exchange via symbol ( CM:CA ), and operate multiple business segments including personal and business banking, commercial banking, wealth management, and capital markets.

This is my second installment of covering Canada-based banks in the new year, after recent coverage of its banking-sector peer Royal Bank of Canada ( RY ), although it is more accurate to call both of them global financial firms.

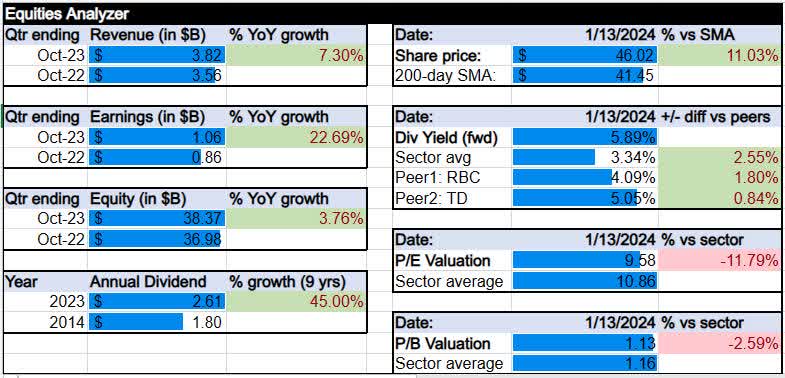

Equities Analyzer

New for 2024, we introduced our Equities Analyzer , which looks at this stock across 8 metrics such as revenue and earnings growth, equity and dividend growth, dividend yield vs peers, and valuations (P/E and P/B ratios).

Here are our results for this stock:

{kind=link}

Revenue Growth

Using data from the income statement , we see that the revenue saw single-digit percentage YoY growth:

CIBC - revenue growth (author analysis)

Breaking it down using the fiscal 2023 Q4 results that came out at the end of November (while the next ones are expected at the end of February), we can see YoY revenue growth both in net-interest income but also in non-interest income, considering that like many other global banks this one also manages assets for clients for a fee.

CIBC - NII growth (company results) CIBC - non interest income growth (company results)

Looking forward, one metric I think will provide continuing tailwind is growth in their interest-earning assets, which I think justifies my expectation of continued revenue growth going into the next few quarters.

CIBC - growth in avg earning assets (company results)

I think this category presents a buy case for this stock.

Earnings Growth

Also from the income statement , we know that earnings grew by double-digit percentages on a YoY basis.

CIBC - earnings growth (author analysis)

From the fiscal Q4 earnings release , we know that both in the Canada and US business segments non-interest expenses went up "primarily due to higher performance-based compensation."

This seemed also true in their capital markets business segment.

We know that most recent overall adjusted expense growth was just 3%:

CIBC - expense growth trend (company results)

So, my impression here is of a company with well-managed expense growth, along with continued revenue growth, a great combination and certainly a buy case from me.

Equity Growth

Using balance sheet data , we can learn that equity grew by single-digit percentages on a YoY basis.

CIBC - equity growth (author analysis)

To complement the above data, I usually want to mention something about CET1 ratio since that is a Basel III regulatory requirement for banks.

At CIBC, their data shows a CET1 ratio of 12.4% which is well above regulatory minimums.

In addition, their liquidity coverage ratio ((LCR)) was at 135% in the quarter ending October.

Although not at the equity levels of peers TD and RBC, I think that at +$38B in equity I would call this bank one with very high equity, and the proven growth in that positive equity adds to the buy case for this stock.

Dividend Growth

More positive data comes from the dividend growth charts which show us that over a 9 year period the annual dividend grew by double digit percentage points.

CIBC - dividend growth (author analysis)

As far as my outlook for future dividend hikes in 2024, I think there is a higher likelihood of that happening given that earnings have grown.

As a dividend-income investor, given that this stock has a quarterly payout of $0.68/share and a history of stable quarterly payouts for years, I think the case calls for a buy.

Share Price vs Moving Average

To discuss the share price compared to the 200-day SMA, let's look at the following YChart showing the price as of Friday's market close.

What we know is that the most recent share price is trading double-digit percentages vs its long-term moving average:

CIBC - share price vs SMA (author analysis)

Although the share price is around 11% above its 200-day SMA, it is also around $11/share above its autumn low of $35 (a +31% price growth).

At the same time, earnings, revenue, and equity have also grown too, so it is not simply a matter of the financials sector pulling up this stock due to sector bullishness, but rather the company itself also showed positive results.

The case here seems to point to a hold, rather than a buy or sell. This is on the basis of a +30% price premium vs the autumn low and 11% vs the moving average, and although earnings also grew by double digits the top-line revenue only grew by 7%.

I don't want to call it a sell, although the chart may appear to show a very nice price spread between autumn and now, setting up a nice capital gain. However, I don't want to "leave money on the table" as the saying goes and dump such a valuable bank so soon.

Dividend Yield vs Peers

From dividend yield data , the story is one of a nearly 6% forward dividend yield at CIBC, a few points higher than its sector average as well as higher than two key banking peers Royal Bank of Canada/RBC and Toronto-Dominion Bank ( TD ).

CIBC - dividend yield vs peers (author analysis)

Although both peers are above +4% on yield, which is pretty good in my opinion, by picking CIBC I am getting nearly 6%.

This clearly presents a buy case worth snatching up at this yield.

Valuation: P/E Ratio

Next, we want to have a look at the forward price-to-earnings (P/E) ratio for this stock, using valuation data .

CIBC - P/E ratio (author analysis)

What it tells us is currently the forward P/E is at 9.58, while the sector average is higher at 10.86.

In relation to the share price and earnings we already looked at, I think this is a justified valuation because although the share price jumped +11% vs its 200-day average, at the same time earnings jumped nearly +23%.

Had it been simply a case of share price growth plus declining or flat earnings, it might have looked overvalued, but the case with this valuation being at just 9.5x forward earnings is for a buy.

Also, compared to peers TD and RBC , it seems CIBC presents a better valuation case. This is because although TD is trading close to its 200-day SMA, it also saw YoY earnings declines, and RBC is trading much higher than its SMA yet only had single digit earnings growth.

For brevity, I will not compare with every single bank out there, but I think this data provides at least some adequate comparisons.

Valuation: P/B Ratio

Valuation data also tells us that the forward price-to-book value (P/B ratio) is now at 1.13, which is pretty close to the sector average of 1.16.

CIBC - P/B ratio (author analysis)

Comparing this valuation with the share price and equity data we looked at earlier, we know that the share price is 11% above its moving average while equity (book value) grew by just under 4%.

Let's face it, this is an equity-rich company, in my opinion, at $38.37B in total equity.

I think this valuation of just 1.13x book value still presents a buy case, as I am getting a company with growing equity and not just rising share price.

Key Risks

In this type of business, two key risks I want to touch upon, which I often do with bank stocks, is rising trends in the provision for credit losses , as well as level of exposure to office real estate in their commercial real estate portfolio..

We can go by the most recent data the company has for their fiscal Q4, and you can see below that PCLs either declined or were flat vs fiscal Q3, though were slightly from fiscal 2022 Q4, although we are talking about PCL ratios of less than 0.50%.

CIBC - provisions for credit losses (company results)

Given the fact that they mentioned the US commercial portfolio took an increased provision for credit losses, let's now talk about that.

Consider that a mid-December article from BNN Bloomberg highlighted growing office property default risks in large cities like Washington DC and San Francisco:

The office-vacancy rate in Washington was 21.1% in the third quarter, compared with 34% for San Francisco, according to CBRE Group Inc. Landlords including Brookfield Corp. have defaulted on office loans in the Washington area.

Even UK-based major media like The Financial Times pointed out in their Jan. 1st article the issue facing office properties in the US, and its tie to high interest rates:

Billions of dollars of debt will fall due this year on hundreds of big US office buildings that their owners are likely to struggle to refinance at current interest rates.

So, based on these and several other articles I have cited in other coverage of banks I did on this portal, we know there is at least moderate to high probability of the risk for office defaults in 2024.

However, when it comes to CIBC which has a huge loan book overall, the question is what risk impact it would be?

Here is a breakdown of their CRE exposure:

CIBC - CRE exposure (company presentation)

It appears any potential risk impact would be more likely to come from their US exposure which is 20% of their CRE book, while their Canada book is only 9% office property. In their US CRE book, though, just over half of exposure is tied to multi-family and industrial property.

Now, consider that from their fiscal Q4 presentation we see that CRE makes up just 11% of their overall $540B loan book.

CIBC - overall loan book (company presentation)

So, I think the risk impact overall of continuing office defaults, for a company of this size, is low.

However, I am more concerned about the market perception risk that could occur if there is a wave of office defaults in 2024, because as soon as there are back-to-back media headlines each day about it I think many investors may start to show some caution on bank stocks, fueling some bearishness and pulling down a perfectly good bank stock like this one with it, at least slightly.

It could also lead to some volatility, as fearful investors panic and sell but more opportunistic ones see the value in banks like this one and start to buy up.

All of this combined, I think, presents a hold case at this point.

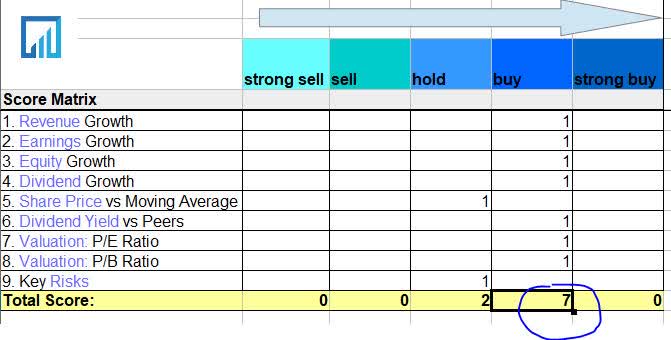

Summary and Rating

From the score matrix below, this stock earned a buy rating today, after a holistic review of 9 different points:

{kind=link}

To summarize, at first glance the share price chart may seem to be screaming sell , however after a closer investigation you can see that a buy case continues to form for this stock, although it is a slight downgrade from my July strong buy rating.

CIBC has managed to grow revenue, earnings, equity, and dividends, as well as having a leading dividend yield among several key peers.

In addition, when it comes to the risk of exposure to office loans, the risk probability in 2024 is certainly there but the risk impact I don't think is significant for a bank where commercial real estate is less than 1/4th of their overall loan book, and office property barely 1/4th of their CRE book.

My portfolio strategy here would be to continue buying up this stock and gain exposure to Canada-based banks in my portfolio, snatching up that nice +5.9% dividend yield in the process and holding for the dividend income each quarter.

I would not be in a rush to sell this bank, so the exit strategy would be to ride out the potential bank-sector market volatility in 2024 that may come from further office loan defaults, and wait out the effects of the next few Fed decisions on rates, then take a capital gain on this stock only when the share price grows at least another 10 -20%.

For further details see:

Canadian Imperial Bank of Commerce: Grab The 6% Dividend Yield And Double-Digit Earnings Growth