CAPMF - Capgemini: Long-Term Growth Story Intact But Macro Hurts The Near Term

2023-10-14 02:56:14 ET

Summary

- Capgemini is a leading provider of IT services and is well-positioned to benefit from the growing adoption of digital tools.

- The weak macro environment has impacted Capgemini's bookings growth, leading to decreased visibility on growth reacceleration.

- Despite the near-term uncertainties, Capgemini's improved resilience and focus on digitalization suggest positive growth over the medium term.

Summary

This post is to provide my thoughts on Capgemini (CAPMF) business and stock. I am recommending a hold rating as I await better visibility into the timing of growth reacceleration. While I am confident regarding the structural growth story of Capgemini, I believe the market is focused on the near-term outlook, which is heavily influenced by macro movements. Until things stabilize, I think it is better to wait for a better entry point.

Business overview

Capgemini is a leading provider of IT services, commonly known as an IT service vendor in general. They focus on helping customers transform their businesses through strategic and digital means. Capgemini serves multiple industries, ranging from defense to automotive to the TMT sector worldwide. With the growing adoption of digital tools, Capgemini is in a strong position to benefit from this secular uptrend over the long haul. Capgemini has historically been a mid-single-digit grower but has seen an acceleration in FY20 as the world was effectively forced to digitalize due to COVID. Recall that businesses need to use digital tools to ensure teams can work together; as such, demand for Capgemini services rose significantly.

Own calculation

Given the nature of the business, the largest expense is personnel costs, which represent around 60+% of the cost structure. Positively, Capgemini has been able to improve its EBIT margins over the years, from 10.9% in FY16 to 12.4% in FY22, despite personnel costs as a percentage of revenue rising by 740 basis points (60.7% in FY16 to 68.1% in FY22). The contributing factor appears to be the reduction in rent and travel expenses as a percentage of revenue, indicating that Capgemini has repositioned the business to benefit from work-from-home and remote implementation.

Investment thesis

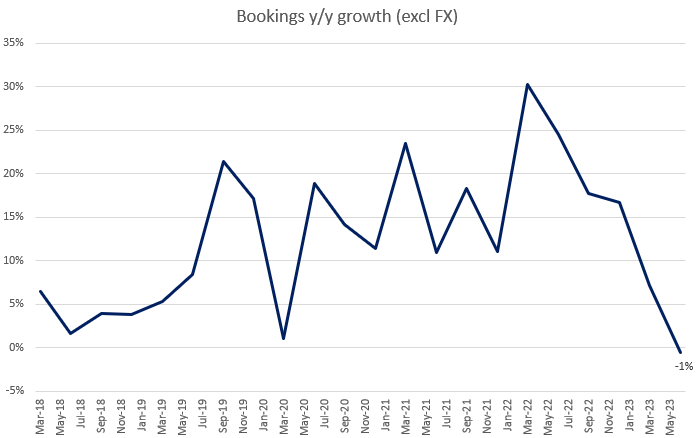

In 2Q23, Capgemini reported revenues of EUR5.7 billion , a growth of 3.2% vs. 2Q22. However, bookings growth continued to decelerate to -1%, which was a major indicator that the business is being significantly impacted by the macroenvironment, with management flagging a prolongation of the trends observed since the beginning of the year. When compared to the past 18 quarters, this is the first time it has dipped to negative territory.

{kind=link}

The weak macro environment has certainly hurt Capgemini, as can be seen from the booking growth rates. From bearish investors' perspective, this is a major red flag as it decreases visibility on when the business will see growth reacceleration and also how much more it could decelerate as the trend is broken (dipping into negative territory). At this point, it is safe to say the bearish narrative has taken over as bullish and long-term investors stay on the sidelines to monitor the macro situation.

That said, I hold an optimistic view about Capgemini over the medium-to-long term. While I see risks from the current macroeconomic environment, I believe Capgemini has become significantly more resilient than in prior periods of slowdowns, driven by increased digitalization, especially with respect to cloud computing and the rising trend of generative AI. Moreover, Capgemini is not the same business that has a large focus on Europe anymore. 10 years ago, North America, APAC, and LATAM were only ~20% of total revenue, but they are almost 40% of revenue today. If we look at the business organic growth profile historically, negative growth from each trough improved over time from -5.5% in 2009 to -3.2% in 2020. While bookings saw negative growth this quarter, it does not mean that revenue will dip to negative as bookings are impacted by many factors, for instance, deals being delayed (agreed but not signed). The fact here is that Capgemini saw positive growth over the past few quarters (4.7% in 2Q23), demonstrating the improved resiliency of the business today.

Consequently, I anticipate Capgemini's top line to grow positively over the medium term, as management guidance (an organic revenue growth range of 5% to 7%) suggests. While bookings have impaired visibility to a certain extent, management's qualitative commentary that they saw double-digit growth in their pipeline is encouraging. In particular, the company closed several sizable transformation deals, which I interpret to be major projects that may take some time to flow into the booking and revenue metrics (thus affecting booking growth). Positives include management observations of clients delaying deals rather than abandoning them, with the latter trend being more prevalent in the United States. While a resurgence in growth for next quarter might not be imminent, I expect a substantial resurgence in demand once the economy starts to recover.

So as there is some delay in these transformational deals, putting a little bit pressure on growth in this area, because some of these transformational deals, the decisions are a bit delayed, they tend to be larger deals. 2Q23 earnings results call

Capgemini's future growth is helped by the rising popularity of generative artificial intelligence. Management revealed at the recent conference that the company has been working on generative AI for over three years and that it employs more than 30,000 people in its data and AI team, compared to the 40,000 estimated by Accenture. The company plans to invest $2 billion (or double its current workforce) in data and AI over the next three years. Investment in generative AI, in my opinion, will yield benefits both internally and externally (by stimulating sales). The use of generative AI internally should increase productivity across the board, particularly for software developers (which require less time to write repetitive code). In my opinion, digitalization provides a substantial runway for growth in sales, and the advent of generative AI will aid in speeding up the delivery of value to customers. Since many customers are still refining their AI strategies and figuring out their data processes before deploying and feeding generative AI models, Capgemini is well positioned to address these concerns given its expertise.

Valuation

Own calculation

I believe the fair value for Capgemini based on my model is EUR204. My model assumptions are that the business will grow at mid-single digits for the next few years, in line with management organic growth guidance. While I acknowledge the near-term macro risk, I believe it is a blip that is inevitable through economic cycles. The important thing here is that the business has become a lot more resilient and is not enjoying a strong secular trend (digitalization) that was not a strong growth driver in the past. Hence, there should be no issues for Capgemini to sustain this growth rate (note that the business grew mid-single digits in 2Q23).

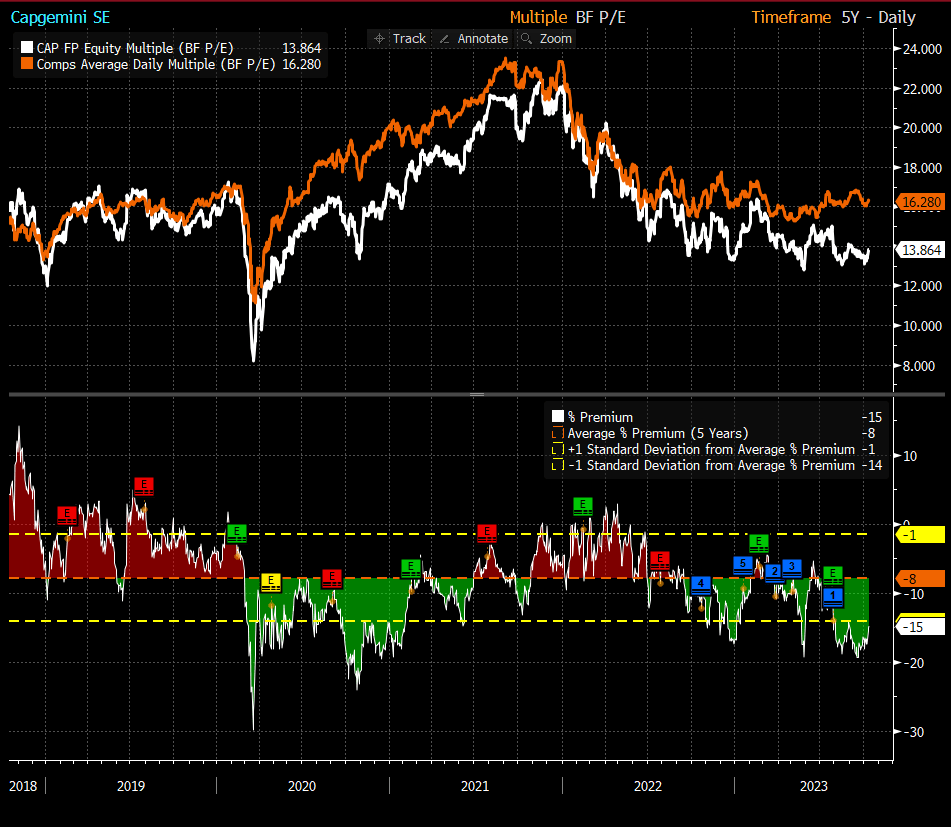

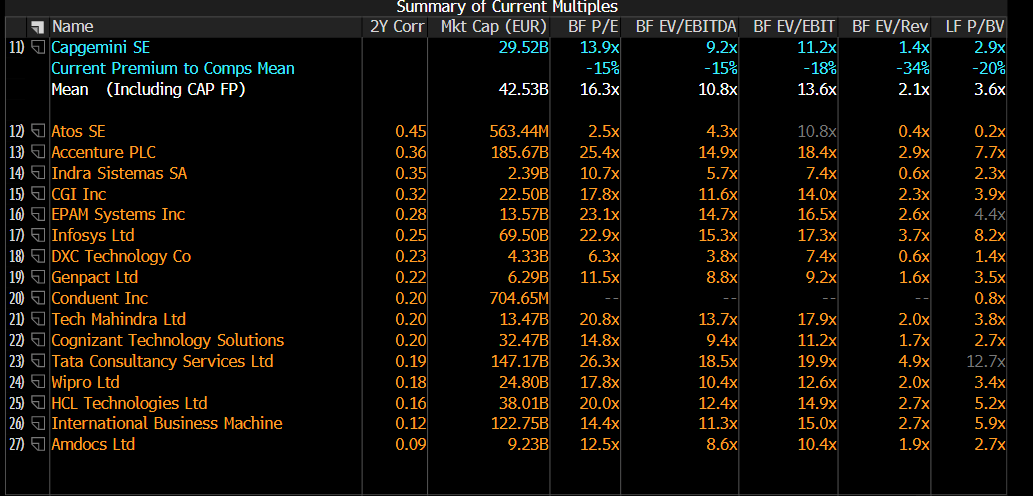

Historically, Capgemini used to trade in line with peers with a modest 8% discount but has recently decoupled to a 15% discount. I believe this discount is due to the weakness investors saw in the bookings growth. While there are merits to this argument, I believe it is a short-term issue that, once Capgemini growth reaccelerates in due time, the valuation gap will close back to the historical average. Assuming an 8% discount to peers' multiple of 16x, the stock should trade at 15x, translating to a 13% upside.

That said, I am not recommending a buy at the moment because the market seems to be focusing on the near-term outlook, which is tough to predict as the macro sentiment could get worse. I would wait for a better price point before recommending a buy.

{kind=link}

{kind=link}

Risk

While the structural growth story remains intact, I believe increased macro risks have resulted in limited visibility into an organic revenue growth reacceleration in the near term. Further deceleration could further impact the stock as consensus revised their estimates downward and bullish investors remained on the sidelines, with no capital flow to support the stock.

Conclusion

My recommendation for CAPMF is a hold rating, reflecting the need for greater clarity on the timing of growth reacceleration. While I am confident in Capgemini's long-term growth potential, the current market sentiment is heavily influenced by macroeconomic factors. As a result, it's advisable to wait for a more opportune entry point.

For further details see:

Capgemini: Long-Term Growth Story Intact But Macro Hurts The Near Term