CAPMF - Capgemini: Remains Undervalued With A Significant Upside Potential

2023-05-31 02:27:38 ET

Summary

- Capgemini remains a solid investment with a forecasted total RoR of 40-50% for 2025E and above, due to its consistent profitability, strong demand for its services, and expanding operating margin.

- Despite recent decline, the company is undervalued and has a convincing upside, with a price target of €210 per share.

- Capgemini's expertise and wide-ranging industry connections allow it to capture strong trends in client demand for digital acceleration, making it an attractive investment opportunity.

Dear readers/followers,

It's time to review Capgemini ( CGEMY ) once again. The company is down double digits since I went long last time, though it hasn't troughed on a 180-day period just yet in terms of share price. This company is, I maintain a significantly positive investment with good upside, not only in the EU but on an international basis.

Given that my last article was in February of last year, I'm now delivering my update for this company, and I'm looking to explain to you why this company still represents a solid investment.

For 2025E and above, I'm forecasting a total RoR of no less than 40-50%, or double digits per year. I'm basing this on the following.

Capgemini - Plenty to like in French Quality

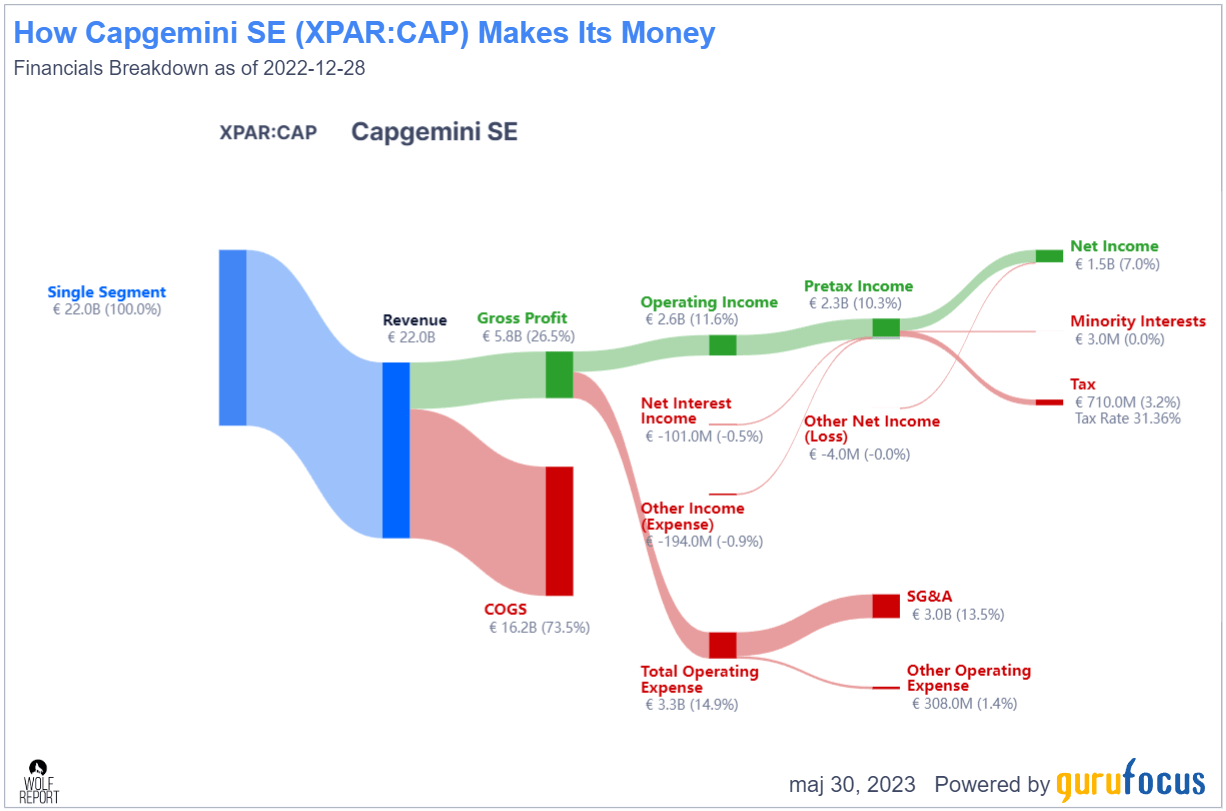

Capgemini remains a BBB+ rated €25B+ market cap It consulting segment leader - at least, it's a significantly profitable operation with clearly above-average profit numbers. This includes an 80+ percentile RoE, and above-average margin both on operating and net margin levels. Capgemini has maintained consistent profitability for the past 10 years and more. It's a single-segment operation, which somewhat colors/influences how easy this company is to decipher. What I mean is that it operates in one segment, like this.

{kind=link}

Despite the turmoil in the IT consulting market, and despite the volatility across the world as a whole, Capgemini has managed to maintain solid profitability even net of its cost of capital. For 2022, that number is 2% on an ROIC net of WACC - doesn't sound much, but it's very impressive in context. The company keeps growing its revenues as well as its overall cash flows. This is the sort of company that I am looking for - a segment outperformer. The company is expanding its operating margin, and couples this with some of the lowest overall valuation numbers in 2-4 years. More on that later in the valuation segment - but just know, this company is currently undervalued.

The latest Capgemini results are 1Q23. The company has significantly outperformed expectations, with 1Q23 revenues up 10.7%, bookings up 6.5%, and ending the 1Q23 period with a 1.02x book to bill, where anything above 1x is quite excellent for a business. Demand remains robust, and plenty of organisations and businesses are looking for Capgemini services.

{kind=link}

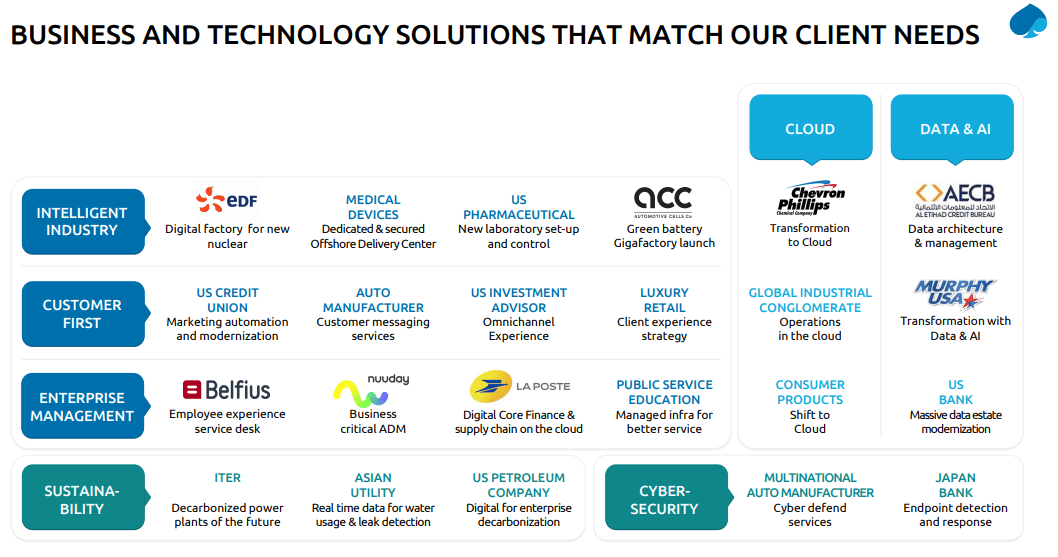

So what exactly does Capgemini do, and what are some of its customers at this point? The company really does a bit of everything - but specializes in large-customer transformations, with some of the customers including the following.

{kind=link}

The company has reiterated 2023E targets, which means that barring something disastrous, this company is coming in at high-single-digit revenue growth numbers, a 13-13.2% operating margin level, and closing in on €2B worth of organic free cash flow for the year. Impressive numbers, and they show that while we may see some decline this year following a 25.35% EPS growth in 2022, that decline isn't going to be massive - maybe 1-2% at the end. This, in turn, is likely to be followed by a high single-digit or low double-digit EPS growth in 2024-2025E - that is for each year, not just the one - once some of these new contracts hit the market and once the company sees adjustments in the market and continues to see traction from new business.

The breadth of Capgemini's portfolio and its customer appeal and expertise is what makes the company an interesting investment at the right price. 2022 was already an absolutely great year - €20B+ total for the year, 13%+ OM, and FCF on an organic basis of well over €1.5B.

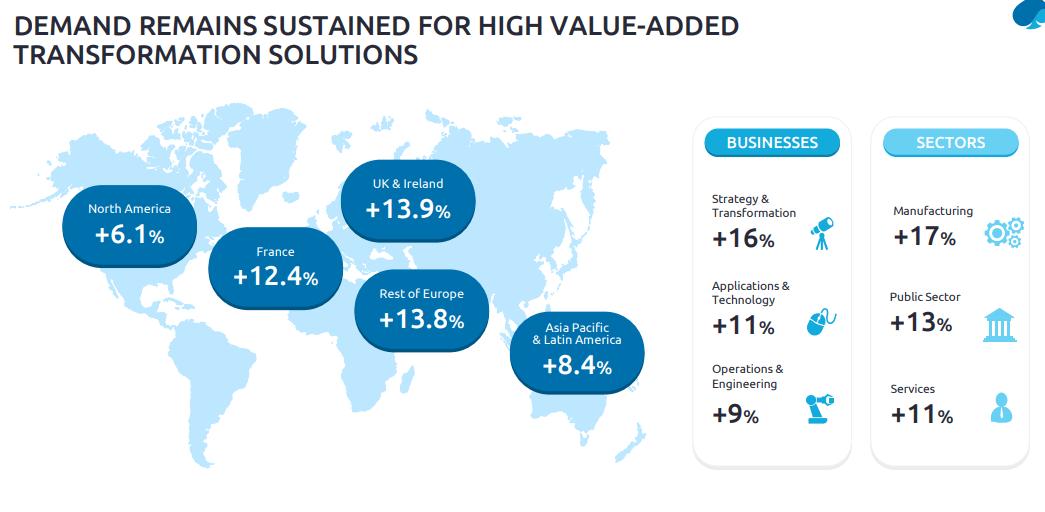

On a regional/geographical basis, which is really one of the only segmentation aside from general service areas we have, the company remains appealing, though somewhat France-centric.

Capgemini IR (Capgemini IR)

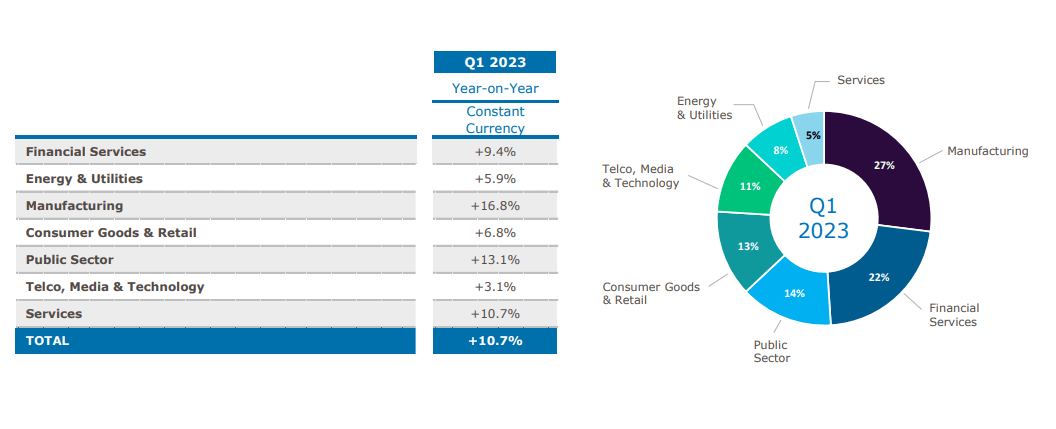

And those service areas, for 1Q23 , also are fairly appealing, with what you might expect in terms of manufacturing focus.

{kind=link}

But we don't have segment-specific or industry-specific profitability. That is just mixed into everything, which means we really don't see where the company is encountering profitability issues, or if one area is significantly better than another. All we can do is guesstimate based on other companies in similar fields which do share this.

Anything we need to be watching closely? The company is, I remind you, a business that tendentially outperforms its estimates. Over 43% of the time, if looking at S&P Global estimates, Capgemini outperforms forecast by more than a 10-20% margin of error - and the latest both in 2021 and 2022. So you'll understand why I consider it not that unlikely that the company will manage the same in 2023. If we'd seen a 1Q23 that saw a decline, I might be somewhat more careful here - but things are continuing in accordance with expectations, and I see only limited impact for the company here in terms of profitability.

We have the 1Q results, but we also have a very recent sales/trading statement call, as of the 4th of May 2023. Thanks to Capgemini's connections and wide-ranging industry expertise, the business is able to capture strong trends in acceleration in client demand for digital acceleration. What Capgemini does here is laying the foundation for the transformation for many of these businesses.

Some examples from the first quarter include ACC, where the company has worked to help the company efficiently provide green batteries for the entire European automotive industry - a JV between SAP, TotalEnergies, Stellantis, and Mercedes-Benz that's working to really bring this transition to bear across EU.

But there are other examples of Capgemini business success as well.

A top bank in the U.S. with petabytes of data spread across several platforms asked Capgemini to modernize and transition their data and analytics to the cloud to improve customer experience and ensuring analytics. The cloud data platform is the essential starting point to address a wide range of challenges such as building better credit, enhancing risk data models, launching AI-enabled customer service advisers and more. So we are definitely driven by creating substantial value for our clients.

(Source: Capgemini Earnings Call, 1Q23)

So, the company is generating solid leads, good contract growth, and good bookings overall - and I don't see any reason for this to decline going forward.

What to keep our eyes on?

Headcount evolution. Personnel costs are the big thing for Capgemini, and where we've previously seen a very front-loaded headcount growth/evolution, for the time being, we're not seeing that because the company has been optimizing and streamlining. Instead, the company is now expecting headcount growth to pick up in terms of pace by the later part of this year.

We can mention utilization declines, but these are comparatively marginal, and we're already seeing indications of improvements here. The main thing is that the current trends in the market are calling for utilization improvements during the year, which coupled with the company's bookings growth, conservative hiring and headcount evolution, should result in double-digit growth going forward.

And that's where we look at the valuation for the company - after a strong start to the year in 1Q.

Capgemini Valuation - Good upside here, attractive "BUY"

So, despite current underperformance, I'm keeping my stance of "BUY" here. I'm also not shifting my price target. Capgemini has a convincing upside to me, and the recent decline is not something that I'm worried about - I don't see it based in actual trends, but perception of a slowdown or challenges that I view as unlikely to materialize.

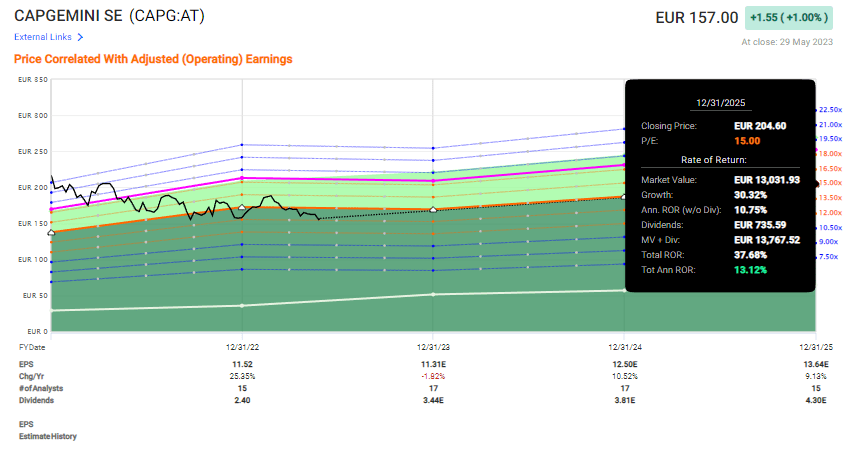

Capgemini, despite strong trends, is now trading at below 14x P/E. At any time in the past barring COVID-19, the company is likely to see good outperformance here based on what has happened to the company if bought at such valuation.

Here is a baseline upside to a 15x P/E for the company.

F.A.S.T graphs Capgemini Upside (F.A.S.T Graphs)

{kind=link}

And that's 15x P/E - the company typically works at 16-17x P/E, which enables the 50% RoR that I spoke of in the initial phases of the article.

Street targets are also fairly appealing. Capgemini is followed by 18 analysts,17 of which are either at "BUY" or "outperform". I believe this correctly describes the company's undervaluation and how likely it is to outperform. The range here starts at €185 on the low side but goes all the way to €255/share. I don't view €255 as valid, but I'm definitely sticking to my €210/share target.

Capgemini also lends itself very well to DCF forecasting, due to the stable nature of its earnings growth. The company, if forecasted at 10% growth for the next few years, which is below where it's forecasted if excluding 2023, and only going 3-4% after the growth stage, the implied FV comes to nearly €220/share. We could further impair this and bring it down to only 7-8% growth, and this would still keep it above €200/share, and that is applying a double-digit discount rate to the company.

Capgemini plays in a competitive segment, with many larger companies out here, but very few companies have the same geographical exposure or appeal that Capgemini has. Accenture ( ACN ) is the primary example here, but other than that, in terms of market size, we have IBM ( IBM ), and Infosys ( INFY ). Capgemini is among the leaders here and has been for years.

For that reason, I don't see any reason to change my expectations or my targets. Any risks to the company are small or insignificant next to what is available here in terms of quality, yield, and potential.

For that reason, I remain positive on Capgemini and unfazed by a double-digit upside. Here is my updated thesis as of May 2023 for the company.

Thesis

My thesis for Capgemini is the following:

- Capgemini is one of the world-leading IT Consulting and Business management companies. It's inherently EU-focused, but with growing exposure to other areas in the world. The future for this company seems secure, with the ever-important role of IT in today's world.

- The company is a definite "BUY" at a good valuation - delivering double-digit upside while providing conservative safety owing to very solid processes, background, and customers with very long contracts.

- I give the company a PT of €210 for the native, making the company a "BUY" here with an upside. I'm not changing my thesis on the company, or my rating, despite a double-digit decline for the company since my last article in February.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I go back and forth between cheap or no, but ultimately I don't want to call Capgemini cheap, only undervalued.

For further details see:

Capgemini: Remains Undervalued With A Significant Upside Potential