CAPMF - Capgemini: Riding The Digital Wave

2023-05-10 15:00:28 ET

Summary

- Capgemini SE is a company that provides consulting services globally.

- Revenue has grown at a CAGR of 8% and we believe high single-digit organic growth should continue.

- Margins are sticky, allowing the business to generate improving returns over time.

- Cloud and AI represent opportunities.

- Capgemini's current valuation suggests upside potential.

Investment thesis

Our current investment thesis is:

- The quality of the company's service is reflected in its consistent growth.

- Tailwinds from digital integration should continue in the coming years.

- Improved profitability and continued growth should improve distributions to shareholders.

Company description

Capgemini SE ( CAPMF ) is a company that provides consulting, digital transformation, technology, and engineering services across various industries globally.

Their services include strategy and transformation, applications and technology, business process outsourcing, transactional services, and installation and maintenance services for IT infrastructures.

Share price

Capgemini's share price has performed well over the last decade, returning over 200% to shareholders. This is a reflection of improving financial performance and industry tailwinds.

Financial analysis

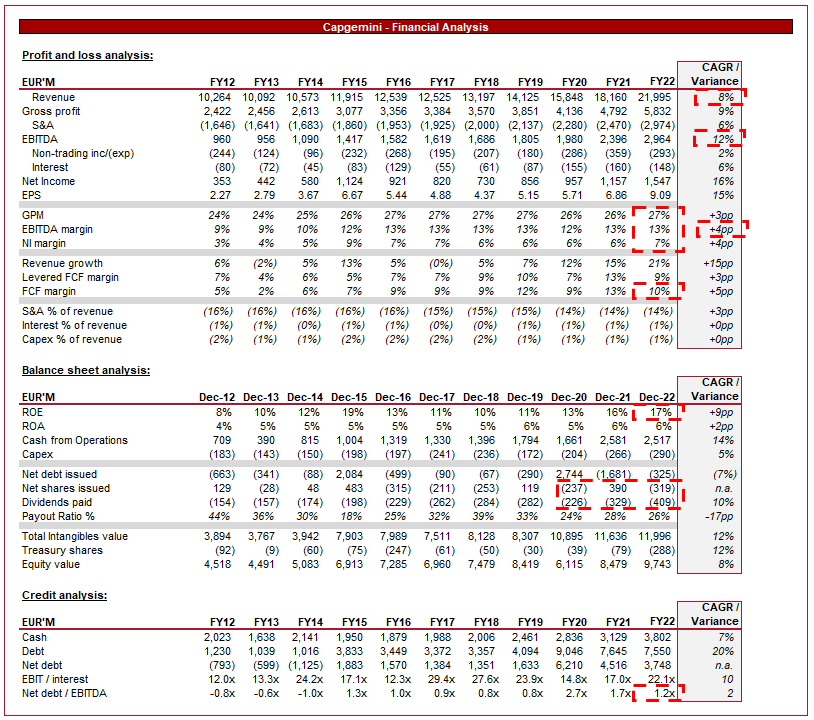

Capgemini financial performance (Tikr Terminal)

{kind=link}

Presented above is Capgemini's financial performance for the last decade.

Revenue

Capgemini has grown its revenue at an impressive 8% CAGR, with only 2 periods with less than 5% growth.

Capgemini's revenue is highly diversified, with the largest region representing 29% of its revenue. This gives the business the benefits of diversification, although comes with FX risk.

Revenue by geography (Capgemini)

More importantly in our view, the company's clients are across a wide range of industries. This is a reflection of the variety in what Capgemini provides, as it can add value regardless of industry. Further, if an industry does experience a period of weakness, the company is not overly exposed to a slowdown.

Revenue by Sector (Capgemini)

The least diversity in Capgemini's revenue is its services provided, which are primarily in relation to IT/Technology. This is the company's key area of expertise, with other services cross-sold as part of a transformation project.

Revenue by service (Capgemini)

It is worth noting that Capgemini is an acquisitive business, operating similarly to Accenture ( ACN ) (although to a far smaller degree), which supplements the company's organic growth.

Much of Capgemini's revenue growth has come in recent years, driven by a change in global operational dynamics for businesses.

The increasing digitization of society is driving demand for digital transformation services, strategy development, and implementation. Businesses are striving for efficiency gains through digital optimization on their backend while improving their front-end experience for consumers. Capgemini (and other IT consulting firms) who are specialized in the area have won a considerable amount of additional work as a result of this. Capgemini's competitive advantage here is its deep expertise in the area which allows the business to be more competitive when tendering for work, relative to the generic consulting firms such as the Big 4. Manufacturing is an industry worth highlighting, generating superior returns relative to others.

Data analytics is becoming increasingly important for companies as they look to gain insights into their operations and make data-driven decisions. We are in an information generation, as businesses place significant value on the information they can acquire from consumers. This is the primary reason social media companies are valued as they are, data is king. Capgemini assists its clients with the optimization and decision-making that comes with a data-driven operation.

Alongside this push for digitization and the acquisition of valuable consumer data, there is a growing need for cybersecurity services to protect against cyber threats. The average cyber-attack costs a business c.$1.4m, representing substantial monetary and non-monetary value (brand image, etc.) to ensure protection. Although businesses are increasing their cybersecurity software spending, larger businesses also require support with infrastructure and operational aspects.

It is clear that the driver of growth is a once-in-a-generation economy-wide transition to new technologies. Now it's worth noting the internet and digital capabilities are decades old, but we are reaching a time where even the most digitally-isolated businesses would benefit. Our view is that this should continue to be a tailwind for the business in the coming years.

In addition to the above, we see avenues for growth that should outperform those we have listed above due to the benefit they provide to consumers.

With the proliferation of IoT devices, companies are looking for IT consulting firms to help them manage and leverage the data generated by these devices as a means of increasing their top line.

An increasing number of companies migrating to cloud-based solutions, as the service becomes an operational necessity for businesses, Our view is that Capgemini is poised to benefit from the growing demand for cloud consulting and implementation services. There is scope for relative outperformance here, as the business is partnered with AWS ( AMZN ), Google Cloud ( GOOG ) (GOOGL), IBM ( IBM ), Microsoft Azure ( MSFT ), and SAP ( SAP ).

The adoption of AI technology is expected to increase in the coming years, especially given the rapid rise of consumer-ready services in the last 12 months. This will increase demand from businesses, who will look to realize the commercial benefits of this development.

Economic considerations

Current economic conditions represent short-term headwinds for the business. With heightened inflation and elevated rates, businesses are seeing demand slow and margins contract. In response to this, we could see costs being cut, or new initiatives postponed, as they protect the bottom line. This could reduce new business growth in the next 12-24 months until conditions improve.

Margin

Capgemini's margins have improved marginally over the last decade, although have been flat for the last few years. The stickiness of margins is highly attractive.

Our expectation would be for a gradual improvement, as with human services such as this, an extra project won does not require the recruitment of a whole new team. The expectation is that employees work harder/longer, so the opportunity for scale economies is high. This is why investment banks, for example, are more profitable when business picks up.

Q1 results

{kind=link}

Capgemini achieved over 10% growth in the most recent quarter, despite the economic backdrop, suggesting economic conditions are not having a material effect. This being said, we note bookings are not in line with revenue growth, which suggests prior project wins vs. new work is weighted toward existing projects.

Overall, this is an impressive result and suggests the business could achieve growth in FY23.

Balance sheet

Capgemini's balance sheet is relatively uneventful.

The company has seen its ROE improve, as growth has driven value for the business.

The company is conservatively financed, with a ND/EBITDA ratio of 1.2x. This will allow the business to conduct further M&A without any solvency risk in our view, giving sufficient runway long term.

Management's distribution policy is both dividends and buybacks, although is careful to maintain a healthy cash balance. Despite the buybacks, we have seen some dilution. Further, the current yield is relatively mild for what is a highly profitable business. We would expect the business to increase this, as cash has reached an all-time high.

Outlook

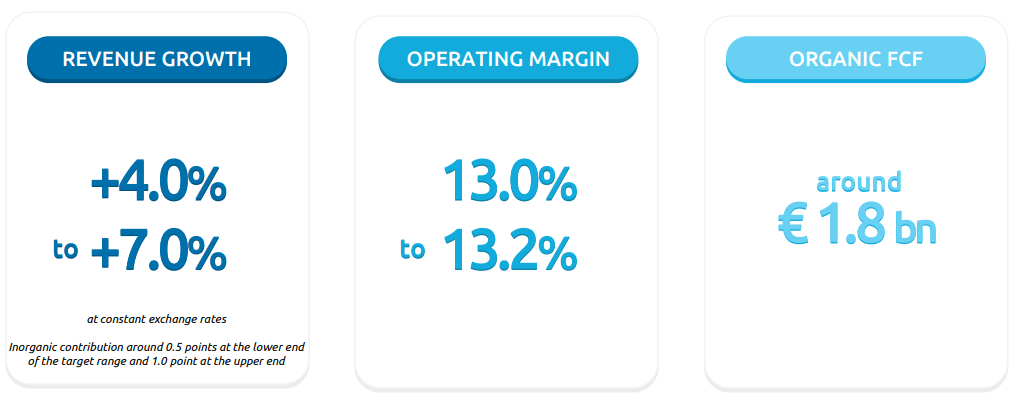

Management forecast (Capgemini)

{kind=link}

Management is guiding 4-7% growth in FY23, which given the macro backdrop, we believe to be a strong result. The majority of this will come from organic growth, which reiterates the resilience of the business. Operating margins are also expected to improve, potentially driven by bigger ticket projects.

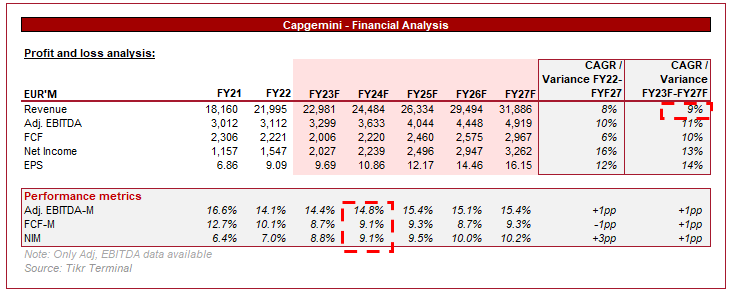

{kind=link}

Presented above is Wall St. consensus forecast for the coming 5 years.

Analysts are equally bullish on the business, with a 5Y revenue CAGR of 9%. Based on our analysis, this looks reasonable if not conservative.

Margin improvement looks unlikely, which based on historical performance, looks reasonable.

Valuation

Valuation (Tikr Terminal)

Capgemini is trading at 11x its LTM EBITDA and 19x earnings. This is in line with its 10-year average mean trading.

The key valuation question is whether the current iteration of Capgemini warrants a premium to its 10-year average.

The bull case based on our analysis is:

- Continued digital integration looks reasonable, so improved growth in recent years can continue.

- New growth opportunities have presented themselves, providing the opportunity for outperformance relative to what was historically achieved.

- Margins have improved.

- Capgemini is a larger business, which should allow for more work to be won.

- Economically resilient business.

- M&A represents an opportunity to supplement growth.

The bear case is:

- Heightened digital spending can only go on for so long.

- It seems comfortable with subpar distributions relative to cash/profitability.

Overall, we believe the argument is weighted toward the bull case. A slowdown in digital spending remains a major risk to the business but we currently see no evidence of the risk being immediate. Should new avenues continue to present themselves, such as Cloud and AI, we may never reach this point.

Final thoughts

Capgemini is a quality consulting business. Revenue has grown consistently, reflecting proof that Capgemini is adding value and increasing its client base. Further, the company is experiencing an extended tailwind, as businesses ramp up their operational capabilities.

Our view is that the business has a long runway to continue growth in a similar vein and with the business valued in line with its historical average, we see upside.

For further details see:

Capgemini: Riding The Digital Wave