CAPMF - Capgemini: Underappreciated In Turbulent Market

2023-10-28 06:28:45 ET

Summary

- Capgemini has consistently reported better-than-average organic sales growth over the past several quarters.

- It has also been able to expand its margins through headcount optimization and driving better utilization.

- Technology spends remains muted as highlighted by larger rival Accenture in its recent release.

- Despite the relative outperformance amidst tough demand backdrop, the company trades at a significant discount compared to its peers and we initiate with a Buy rating.

Investment Thesis

We rate Capgemini ( CGEMY ) a Buy as we believe the street is underappreciating the company's relatively strong organic growth through the past quarters and the relative undervaluation compared to peers. The company has strong order pipeline and has consistently maintained a healthy book to bill ratio converting billings to revenue as well as adding new clientele. In addition, its headcount optimization strategy along with other measures has also enabled them to expand margins during the past 2 years outperforming its peers significantly. Initiate with a Buy with a target price of $40 (at 20x Fwd P/E)

Company Overview

Capgemini ( CGEMY ) is a leading IT Service provider and amongst the Europe's largest provider offering a wide range of software and services solutions. It has a diversified revenue with Europe contributing about 60% of total revenues with North America contributing about 31% and remaining contribution from Asia Pacific region. By industry, Manufacturing (26%) and BFSI (22%) contributes the bulk of the revenue along with Public Sector (14%), Consumer and Retail (13%), Telecom (12%) and others. The company has built strong offshore footprint (58%) providing cost competitive services across multiple clients and sectors.

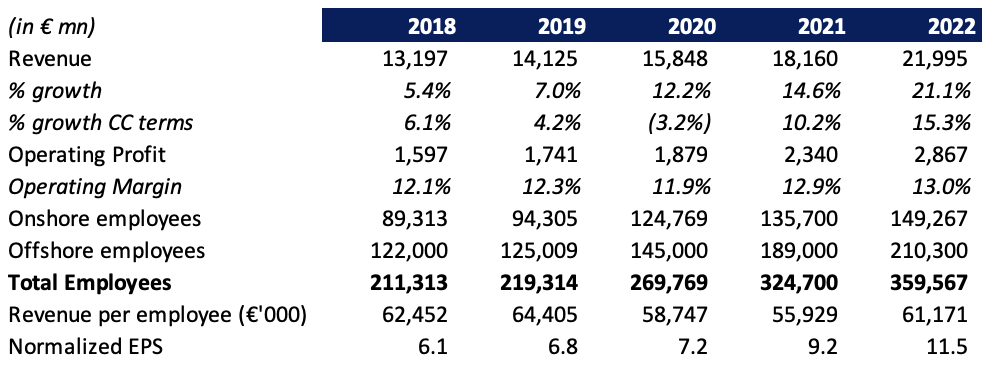

Historical Track Record

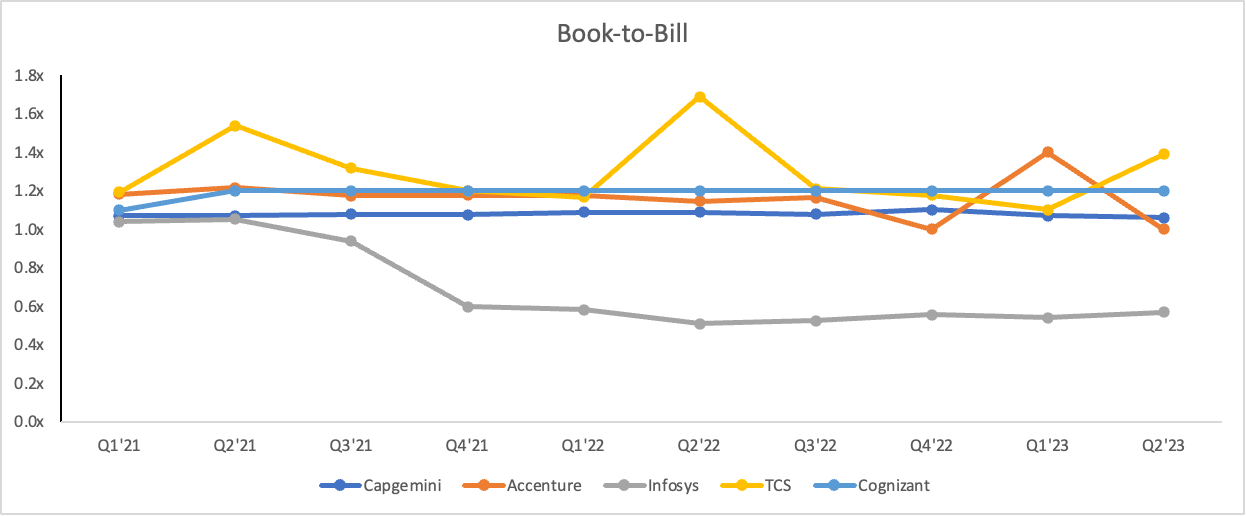

The company has reported strong growth historically driven by digital transformation amidst the pandemic with revenues growing in double digits in constant currency terms during 2021 and 2022. Personnel costs forms bulk of the costs (60%+) given its service nature of the business. Revenue per employee declined since 2018 as a result of a larger induction of freshers who have a longer training cycle, growth in onshore count, however, the decline in travel costs lead to an improvement in operating margins post-pandemic in 2021 and 2022. Order book remained strong and has grown consistently with Book to Bill ratio improving from 1.0x to 1.1x demonstrating the robust growth and customer stickiness across verticals.

{kind=link}

Note: All figures in mn except per share data.

Industry Overview and Key Trends

Capgemini operates in a dynamic global services industry which is about $1.3 trn as well as within engineering, research and development (ER&D), through its recent acquisition of Altran for ~€3.6 bn , with an estimated $250 bn market size. North America forms the biggest market with an estimated over 50% market share with Europe and APAC contributing about 25% each.

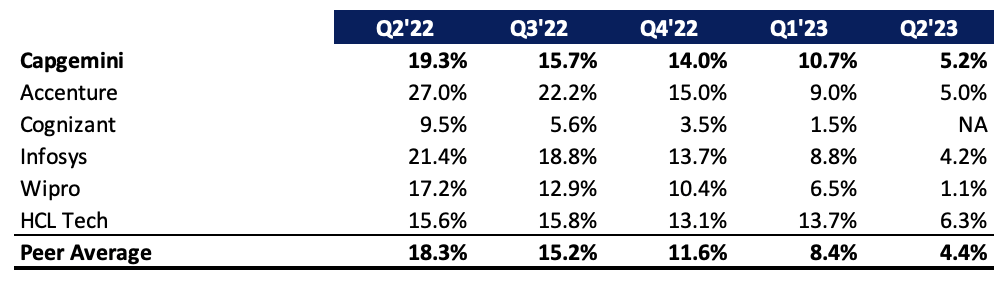

Constant Currency Sales Growth

{kind=link}

Note: Accenture quarter ending May shown in Q2.

Comparing with peers, Capgemini has reported constant currency sales growth which is among the top quartile consistently and higher than the peer average over the last several quarters.

Technology spendings remains tight as highlighted by several of the larger IT players amidst tough macro conditions. Accenture in its latest earning release reported weaker set of earnings with a 4% constant currency sales growth and guided for FY24 sales growth of 2 - 5% which came in below consensus expectations pegged at 5%.

Our clients have had to navigate a macro environment that is tougher than we anticipated at the beginning of FY23. While it's played out differently across markets and industries, we have seen greater caution globally, with lower discretionary spend, slower decision-making, and a significant impact from the challenges the comm, media, and tech industries have faced.

- Julie Sweet, Chairman and CEO, Accenture

Infosys ( INFY ) also recently slashed its full year guidance to 1 - 2.5% currency growth, its second downward revision in past two quarters (INFY provided a guidance of 4 - 7% at the beginning of the fiscal year), amidst weakening demand environment.

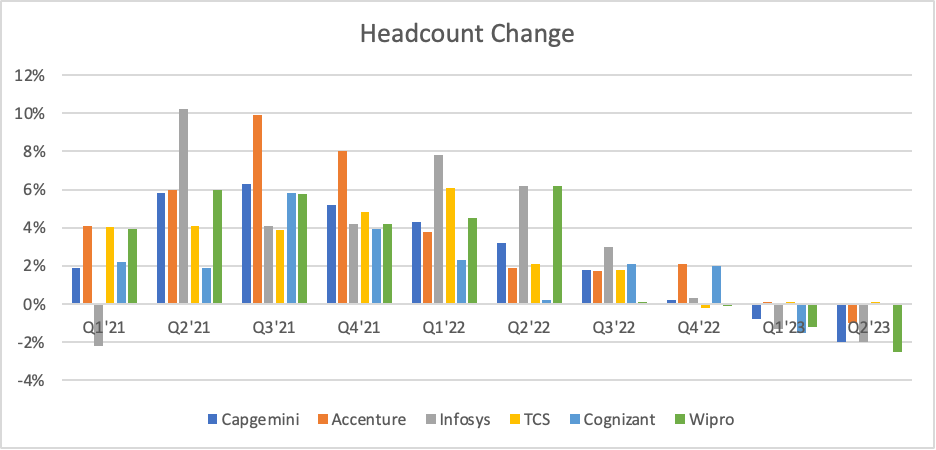

Headcount change has consistently declined over the quarters amidst a continued demand environment and optimization of the headcount as the companies looks to improve utilization and reduce its buffer capacity.

{kind=link}

The company has been able to optimize its headcount better than the competitors being slightly cautious and around the midpoint change compared to its peers demonstrating better utilization and improving operating margins.

| Company |

| EBIT Margin Change (2021 vs 2023) |

| Capgemini ( CGEMY ) |

| 40 bps |

| Accenture ( ACN ) |

| 10 bps |

| Infosys ( INFY ) |

| (180) bps |

| TCS |

| (220 bps) |

| Cognizant ( CTSH ) |

| (130 bps) |

| Wipro ( WIT ) |

| (280 bps) |

Source: SEC filings, Author.

We believe the deal wins are largely seasonal in nature and may not be an accurate representation of the pipeline. For example, Infosys in its CQ2 FY23 results reported a deal win growth of 35% YoY, however, the company had reported a 34% decline a year earlier. We compare the peers based on Book to Bill ratio which is a better metric to evaluate the order pipeline and eliminates the noise of any few large deals won during a particular quarter. The company has managed stable book to bill ratio over the period generating average growth higher than the peers which demonstrates the company's ability into converting order book into earnings as well as continuing a healthy pipeline. Other peers such as Infosys has witnessed a decline in its Book to bill ratio which has led to a softer performance. We exclude Wipro from the analysis as the company has failed to convert deal wins in revenue reporting muted growth despite a book to bill ratio of about 1.4-1.5x historically.

{kind=link}

Earnings Preview

Capgemini reported strong 5.2% growth YoY in cc terms in its Q2 amidst a soft macroeconomic environment driven by momentum in its high value added services along with continued growth in cloud, data and AI driving digital transformation for its clients. The company reported operating margin of 12.4% for H1 2023, up 20 bps YoY, as a result of improved project mix which was partially offset by higher operating cost base. The company guided that the constant currency growth would be at the midpoint of its earlier guidance of 4 - 7% slightly declining from its previous expectation of growth at the upper end of the midpoint. This sent shares tanking about 7% on the print and has been around similar levels since then which we view it as albeit high pessimism compared to the current demand environment.

We believe the company is likely to report a 2.5% growth in constant currency terms for Q3 when it reports its results on November 7. Management is likely to report a deceleration in the organic growth for Q4 (estimated at around 1.5%) and we believe the company is likely to be able to be at or slightly below the midpoint of its guidance, in line with their previous commentary. Order book and deal pipeline is poised to remain strong on the back of digital transformational deals along with vendor consolidation drive. The company has consistently delivered on Operating margin for the full year is expected to be around 13.1% at midpoint, which implies a continued acceleration on YoY basis as well as sequentially which has seasonally been stronger half along with a result of improving productivity and utilisation.

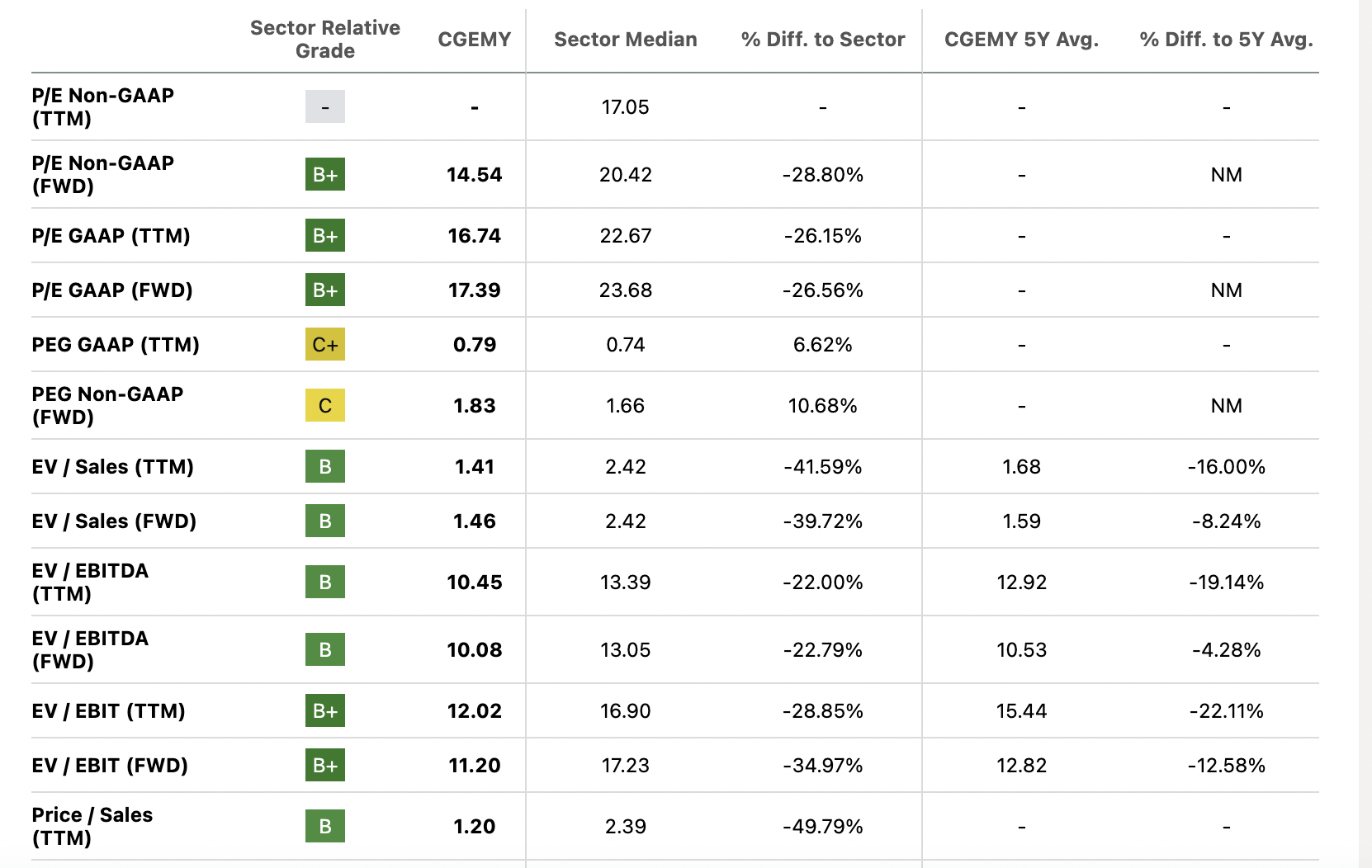

Valuation

Despite the relative outperformance over the past few quarters, Capgemini trades at a significant discount compared to its peers. We believe CGEMY has done relatively well over the past several quarters and has been quite underappreciated by the street. While we believe given the current market dynamic, revenue growth is likely to fall around 2.3% - 2.4%, the company looks poised to deliver its stated guidance. The full year guidance would still entail higher revenue growth than the peer average as witnessed historically and believe the multiples are likely to rerate to the industry averages. We initiate with a Buy rating at a target price of $40 (at 20x P/ Fwd Earnings) in line with the peer average.

{kind=link}

Risks to Rating

Risks to rating include

1) Macro pressures resulting in declining IT spends which can dampen organic growth

2) Margin guidance can come in short of expectations amidst decelerating sales and persistent cost pressures

3) Competitive pressure may intensify as companies look to woo new customers amidst a softer demand environment

4) Higher levels of attrition and failure to retain talent can significantly impact business operations

Final Thoughts

We believe the street is likely underappreciating Capgemini despite reporting higher than the peer average growth and strong deal pipeline. We believe the relative discount to the peers is unwarranted and believe the multiples should rerate towards the peer average. Despite a softer macro environment, we believe the company is likely to achieve its midpoint of the guidance for the year and assume that the company is likely to reiterate during the results scheduled in a week.

For further details see:

Capgemini: Underappreciated In Turbulent Market