BMY - Capitalizing On Inflammation's Role In Neurological Disease Part 1: Coya Therapeutics

2023-08-14 05:45:30 ET

Summary

- Coya Therapeutics is developing Treg-enhancing therapeutics to target diseases driven by inflammation, including in the central nervous system, including ALS.

- Coya Therapeutics' ALS drug could be approved based on pivotal phase 2 results and could potentially be the best drug on the market, halting ALS disease progression.

- Coya's shares appear undervalued based on simplified valuation methods (risk-adjusted, discounted peak sales multiple).

In this two-part article series, I'll review two biotech investments, both targeting inflammation in the context of neurology. Inflammation is increasingly understood as a major driver of a wide range of chronic and progressive diseases and even some acute conditions, and as such, the resolution of inflammation is a " new therapeutic frontier " according to a recent Nature review. INmune Bio ( INMB ) and Coya Therapeutics ( COYA ) are developing two different therapeutic approaches (mechanisms of action) to the same general outcome: reduced inflammation in the central nervous system, but focusing on different indications as core programs. They accomplish reduced neuroinflammation through two different paths: in Coya's case, enhancing the suppressive activity of T regulatory (Treg) cells, and in INmune's case, eliminating the destructive aspect of the well-known key inflammatory cytokine, TNF. I believe both stocks are significantly undervalued, albeit for different reasons, and both are heavily insider-owned and fairly well-funded. In this article, I'll focus on Coya and its core program. I believe Coya is undervalued due to its very promising ALS treatment and platform technology aspect.

Neuroinflammation in Chronic Disease

Inflammation is a key driver of chronic disease . The questions are in regard to the best way to alter inflammation since it can have restorative and destructive properties. In acute injury or during infection, increased inflammation or proinflammatory responses are necessary to clean up debris and destroy foreign material. Subsequently and ideally, a restorative phase then begins where tissue is regrown or healed. Dysregulation in the immune system can result, in an excessive proinflammatory response, and tissue damage can occur. This in some diseases is accompanied by persistent attempts to heal, which can result in adverse outcomes like significant scar tissue build-up over time.

The catch is that the immune system is very complex and in some respects redundant, and simply "turning down" general inflammation with traditional and not adequately specific methods is not always helpful or beneficial. For instance, this is why NSAID use (e.g., ibuprofen) won't treat ALS or Alzheimer's effectively. Clinical trials with NSAIDs for Alzheimer's fail to show benefits . Thus biotech and pharma companies are aiming to find better ways to influence inflammation.

With specific regard to neuroinflammation, next-generation drugs offer the potential to treat a variety of diseases - let's use ALS and Alzheimer's as examples. In Alzheimer's, acetylcholinesterase inhibitors have been used to limit acetylcholine levels, and in ALS and Alzheimer's, glutamate regulators limit excess glutamate activity. While these drugs may protect cells from excessive neural transmission, they do not help repair the brain's architecture and they do not significantly alter the progression of disease. Newer approved drugs like Amylyx's ( AMLX ) Relyvrio (for ALS) go one step further and are thought to improve mitochondrial function and protein production. Biogen ( BIIB ) got its new amyloid-beta targeting antibody approved for Alzheimer's (Aduhelm), and Eli Lilly ( LLY ) is expected to get its very similar drug approved by the end of this year. These drugs slow the progression of Alzheimer's by removing toxic protein (amyloid) buildup by activating the immune system against these harmful components. Despite initial high expectations for billions in sales, these drugs have modest efficacy and there is a lot of room for improvement by controlling chronic inflammation.

So let's just dive into these neuroinflammation companies that have the potential to drastically change the neurodegenerative disease treatment landscape and see what's under the hood.

Coya Therapeutics

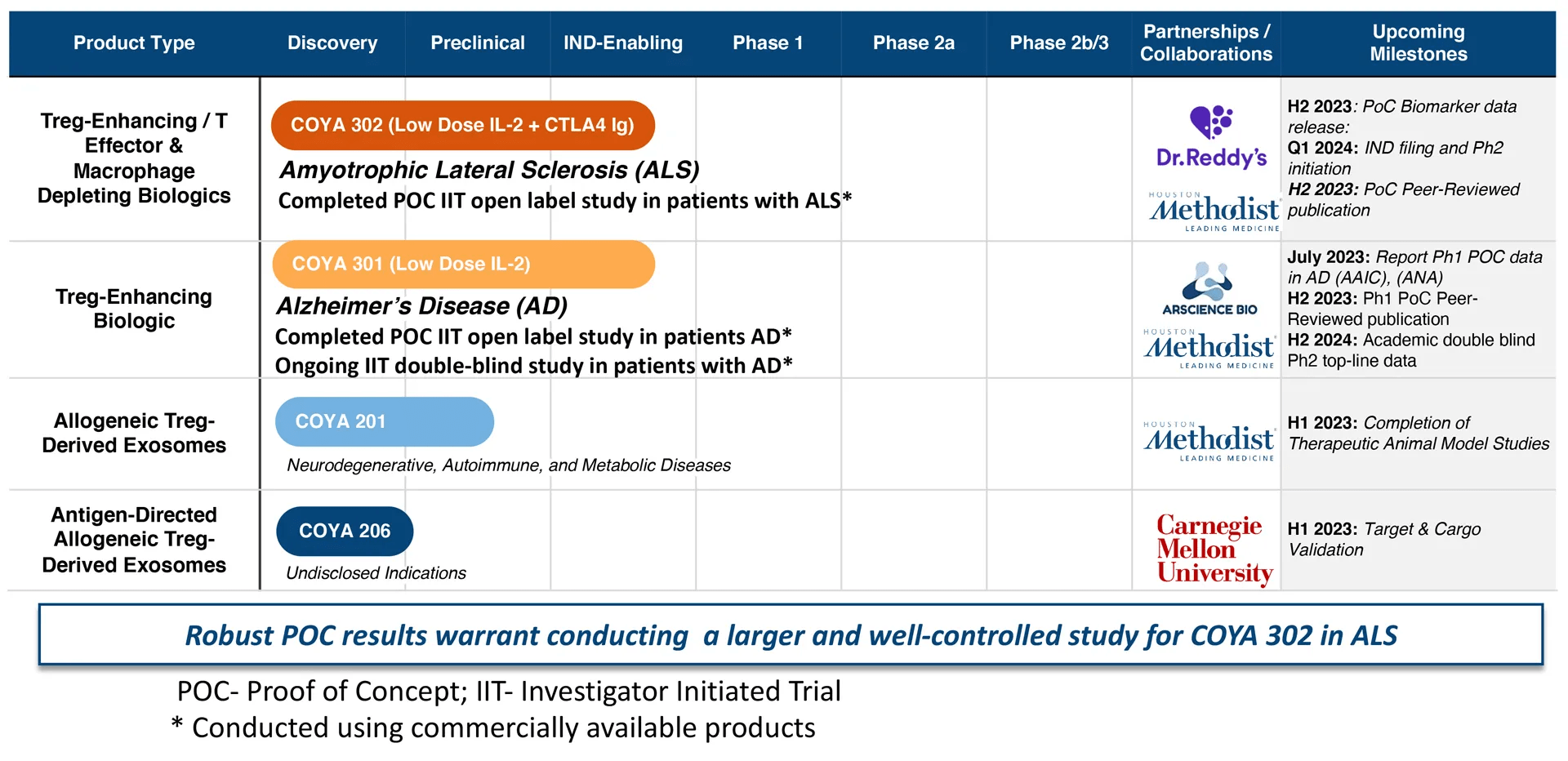

Coya Therapeutics is a biotech company focusing on treating diseases, specifically ALS to begin with, by controlling inflammation. They do this by expanding and improving T regulatory (Treg) cell function. Tregs are a type of helper T cell (CD4+), an immune cell that is basically required to orchestrate the adaptive (antigen-specific) immune response, but can also robustly influence innate ("nonspecific") immune interactions . To simplify, Tregs limit inflammation and are generally considered neuroprotective, especially in chronic and progressive diseases. The company's pipeline is shown below. In this article, we'll focus on the company's ALS indication using COYA 302, which consists of LDIL-2 (low dose IL-2) and CTLA4 Ig (CTLA4 immunoglobulin), which is a dual approach to augment Treg populations and activity endogenously . Other pipeline candidates for COYA will utilize LDIL-2 (aka COYA 301) as a backbone for different "combination therapies."

Coya Therapeutics Pipeline (Coya Therapeutics website)

{kind=link}

Coya is a mid-stage biotech company (entering phase 2 in ALS in Q1 2024) but could be much closer to FDA approval than first meets the eye. ALS therapies have recently been advanced to approval before their phase 3 trials were completed; Amylyx's Relyvrio and Biogen's Qalsody were both granted accelerated approval based on small phase 2 datasets. Both drugs' results were less impressive than the data Coya has generated to date, which will be examined below.

COYA 302 is a unique proprietary formulation of recombinant human LDIL-2 subcutaneously administered (the only available IL-2 on the market is a high-dose version that is intravenously administered) to selectively expand Tregs over Teff while using the CTLA4 Ig to reduce the inflammatory co-stimulation of T cells and induce an anti-inflammatory macrophage and microglial (brain-specific macrophage) phenotype. This promotes cell repair and axonal outgrowth. IL-2 acts as an amplifier and proliferator for CD4+ helper T cells, but Tregs have about a 100x lower threshold to respond to IL-2. So a low dose of IL-2 will help selectively expand Tregs and not Teff. The CTLA4 Ig works synergistically with the IL-2 to further help push the anti-inflammatory, "immunosuppressive" phenotype. This unique combination works inside the patient's own body. This can be important as expanded Treg cells ex-vivo are not necessarily exposed to the proper antigenic stimuli (which can be important to ensure their specific suppressive response through TCR stimulation) and therefore may not be as effective when readministered. In other words, expanding endogenous Tregs in this manner (IL-2 + TCR stimulation) could/should result in a more potent and sustained response . Also, these biologics will likely be easier to manufacture, store, and administer than cell therapies. So potentially, the biology and logistics work out better when influencing patients' own T cells compared with administering the actual cells.

The benefit of influencing an entire cell type is that the immune system is extremely complex with many interacting and redundant pathways. Targeting one pathway may not adequately change the course of the disease or the total state of inflammation. For instance, blocking RIPK1 via a small molecule, may not be enough to influence inflammation and may cause significant adverse effects , as evidenced by the discontinuation of Denali's ( DNLI ) DNL747.

Beyond ALS and COYA 302, the company has the potential to use its expertise and Treg-focused solutions to address other inflammatory and progressive diseases with high unmet needs.

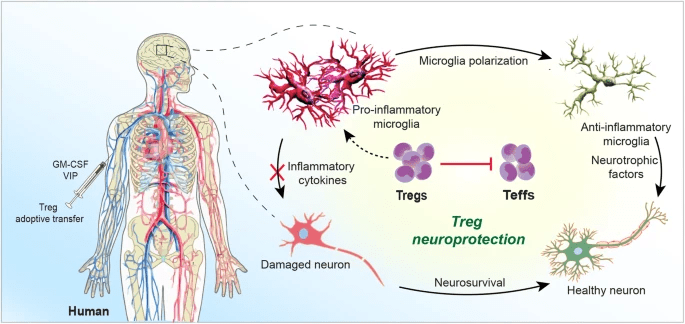

Tregs' Role in Neuroinflammation (The Pivotal Role of Regulatory T Cells in the Regulation of Innate Immune Cells)

{kind=link}

According to a recent Frontiers article :

it is now accepted that adaptive immunity can affect brain development and homeostasis. For example, deficiencies in CD4+ T cell number and function lead to impaired neurogenesis and cognition. Also, restoring a balance between divergent T cell subsets can sustain neuronal homeostasis and preclude disease-inciting pro-inflammatory events. Progressive neurodegenerative, neuroinflammatory, and neuroinfectious disease rests, in measure, around adaptive immunity. All are sped by elevated effector and downregulated regulatory T cells (Teffs and Tregs). However, past attempts to correct such aberrant host immunity using immunosuppressive agents have failed to affect disease outcomes. This led to initial discouragements in immune-based approaches for CNS disease by some neuroimmunologists. Indeed, by some due diligence, a new therapeutic frontier has emerged designed to transform neurotoxic Teffs into neuroprotective Tregs. [...] What is now broadly accepted is that activation of peripheral immunity, regardless of cause, triggers neural tissue repair and controls the tempo of CNS injury. Both innate and adaptive immunity can incite neuroinflammation and accelerate aggregated misfolded protein accumulation that lead to neuronal demise. Such pathogenic events are operative, at varying degrees, in Alzheimer's and Parkinson's diseases (AD and PD), amyotrophic lateral sclerosis (ALS), multiple sclerosis ((MS)), and stroke. In contrast, peripheral immunity also facilitates brain repair, in part, by suppression of neurotoxic Teff responses.

Coya is focusing on balancing the helper T cell populations by augmenting the Treg response, which helps limit neurotoxic Teff responses and, through a cascade of effects, the inflammatory responses of other immune cells. Some may think that the central nervous system is completely removed from the peripheral immune system, but there are actually brain-resident (CNS-usually mature) Tregs , not just peripheral Tregs, that play an important role in brain health. That, and peripheral immunity can greatly influence the CNS.

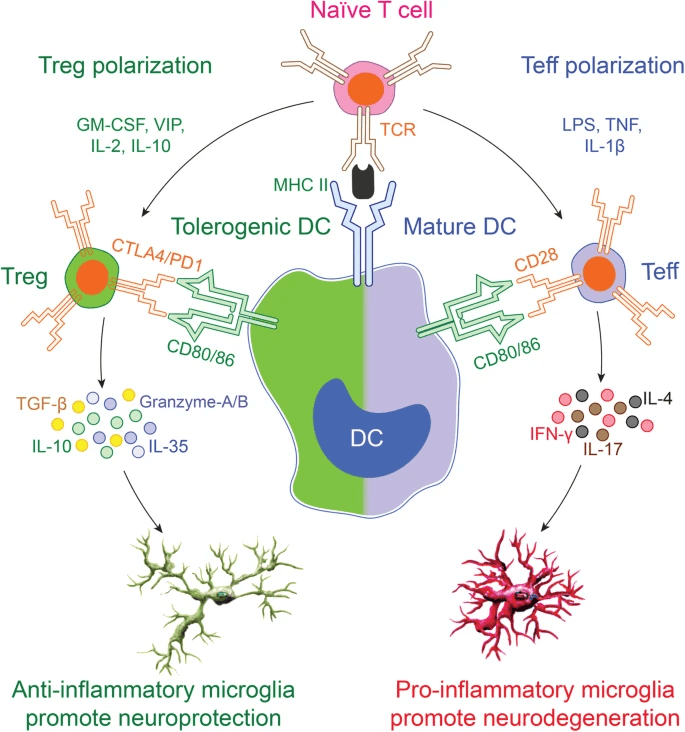

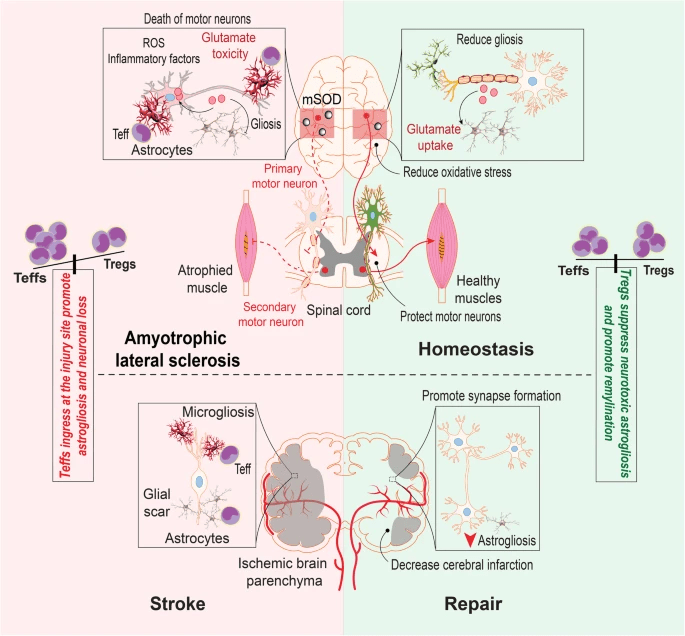

Treg Polarization in CNS (The Pivotal Role of Regulatory T Cells in the Regulation of Innate Immune Cells) Tregs in ALS (The Pivotal Role of Regulatory T Cells in the Regulation of Innate Immune Cells)

{kind=link}

{kind=link}

In the graphic above one can see how CD4+ T cell polarization influences inflammation, influencing the highly-important microglia which, along with astrocytes and oligodendrocytes, can prune or repair neurons and their axons. In many cases, this is thought to be the difference between stable/improved disease, and progressive disease. So how does all this work in the context of ALS?

What is ALS (Amyotrophic Lateral Sclerosis)?

ALS is a neurodegenerative disease characterized by the progressive loss of motor neurons, leading to deadly paralysis. The exact pathophysiological mechanisms of ALS are not considered known, but there are a few theories as to what causes the disease, including immune disorder, redox imbalance, autophagy dysfunction, disordered iron homeostasis, and glutamate excitotoxicity. Some theories focus on dysfunctional signaling within the CNS while others propose that at the CNS periphery, the immune system attacks the motor neurons. With respect to glutamate excitotoxicity, there is the drug, riluzole, which is made by Sanofi ( SNY ). It's the only approved drug to extend lifespan, but it doesn't affect the disease course. Edaravone, developed by Mitsubishi Tanabe Pharma ( MTZPY ), is an antioxidant (redox imbalance) that only reduces ALS symptoms. As of 2021, these were the only two FDA-approved drugs, and they came with significant side effects.

ALS is a rapidly progressing condition that usually leads to death in 2-3 years after onset of symptoms, in ¾ of patients. The other patients typically live for 5-10 years. Approximately 20% may survive for a time range between 5 and 10 years after initial symptom onset. The immune dysfunction and pathophysiology in ALS have become better understood in recent years and, in my opinion, more compelling than other ALS theories, though aspects of theories might overlap. Increasing evidence supports autoimmune mechanisms driving pathogenesis in ALS, including but not limited to T-lymphocytic infiltration in the anterior horn of the spinal cord (where the motor neurons that die are located), circulating immune complexes, association with other autoimmune conditions, and high-frequency of specific MHC types. Additionally, immunoglobulins from ALS patients have been shown to cause apoptosis of motor neurons in vitro as well as cause degeneration of motor neurons in vivo . In ALS, Treg effectiveness is impaired , with greater Treg dysfunction correlating with greater disease burden and faster progression. These studies at the very least show the contribution of inflammation in ALS. Therefore, it's no surprise that COYA 302 could compare favorably to existing marketed drugs.

Comparing to Recent FDA-Approved Drugs

COYA 302 has the chance of being granted accelerated approval based on the precedent set by Amylyx's Relyvrio and Biogen's Qalsody.

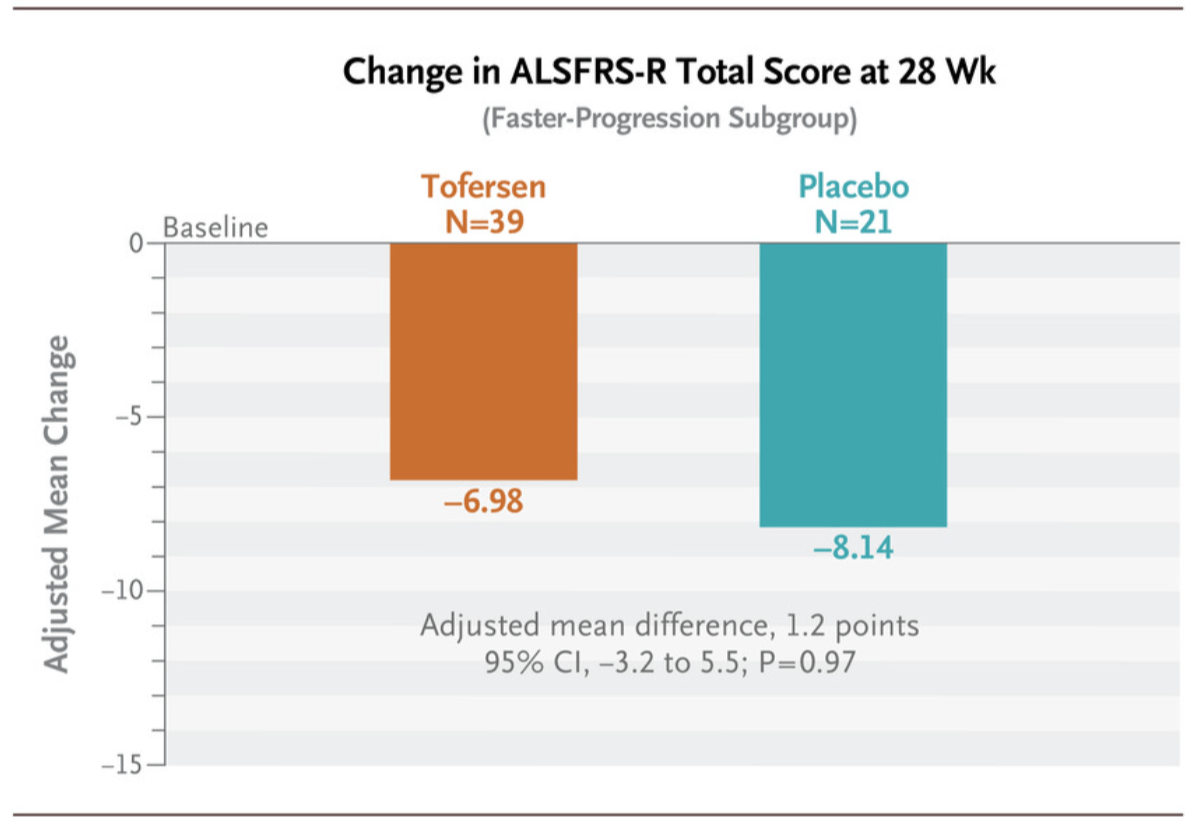

Tofersen (Qalsody) ALSFRS-R Results (Trial of Antisense Oligonucleotide Tofersen for SOD1 ALS | NEJM)

{kind=link}

Qalsody (tofersen), which targets SOD1 mutation, a mutation of interest in ALS, was approved based on NfL reductions, a biomarker for axonal injury and neuronal degeneration. The patients in the primary analysis group declined slower than placebo but this difference was very modest and not statistically significant. The rationale is probably that: since high NfL is considered a leading indicator for symptoms as it typically predates disease progression, perhaps there is a delay in the separation of the placebo and active arms in ALSFRS-R score. Reduced NfL is therefore considered a biomarker that neuronal and axonal destruction is slowing. Despite these modest, statistically insignificant results, Qalsody was approved in April 2023 for patients with SOD1 mutations only. The drug is expected to sell for just under $200,000 annually and garner peak sales of about $300 million .

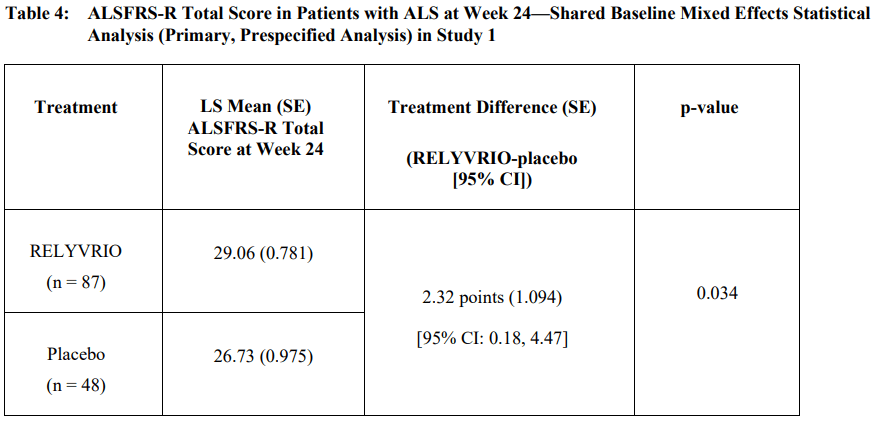

Relyvio performed a bit more impressively over 24 weeks.

Relyvrio ALSFRS-R Clinical Trial Results (RELYVRIO US Prescribing Information)

{kind=link}

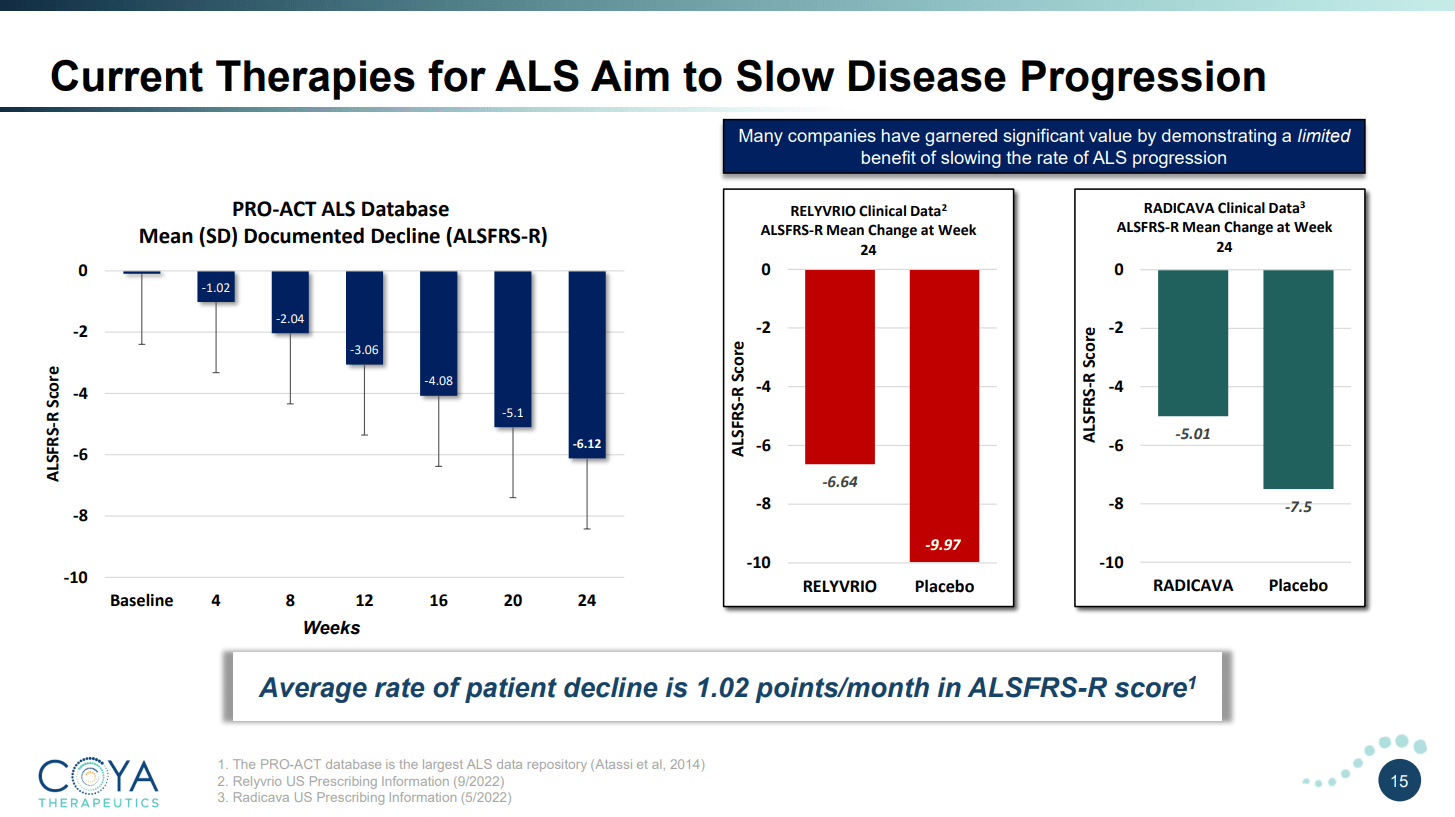

Compared with a 1.16 difference in score over 28 weeks with Biogen's Qalsody, Relyvrio was able to show a 2.32 ALSFRS-R score difference at week 24. The pricing is similar, with Relyvrio costing over $150,000 per year . Both Relyvrio and Qalsody slow the disease progression slightly. Coya has a slide of the differences when compared to placebo (not just a delta change, which doesn't tell the full story). As one can see, patients on either drug will still progress fairly quickly with progression only being slowed by roughly 33% for both drugs.

COYA 302's Competition ALSFRS-R Performance (Coya Therapeutics June 2023 Investor Presentation)

{kind=link}

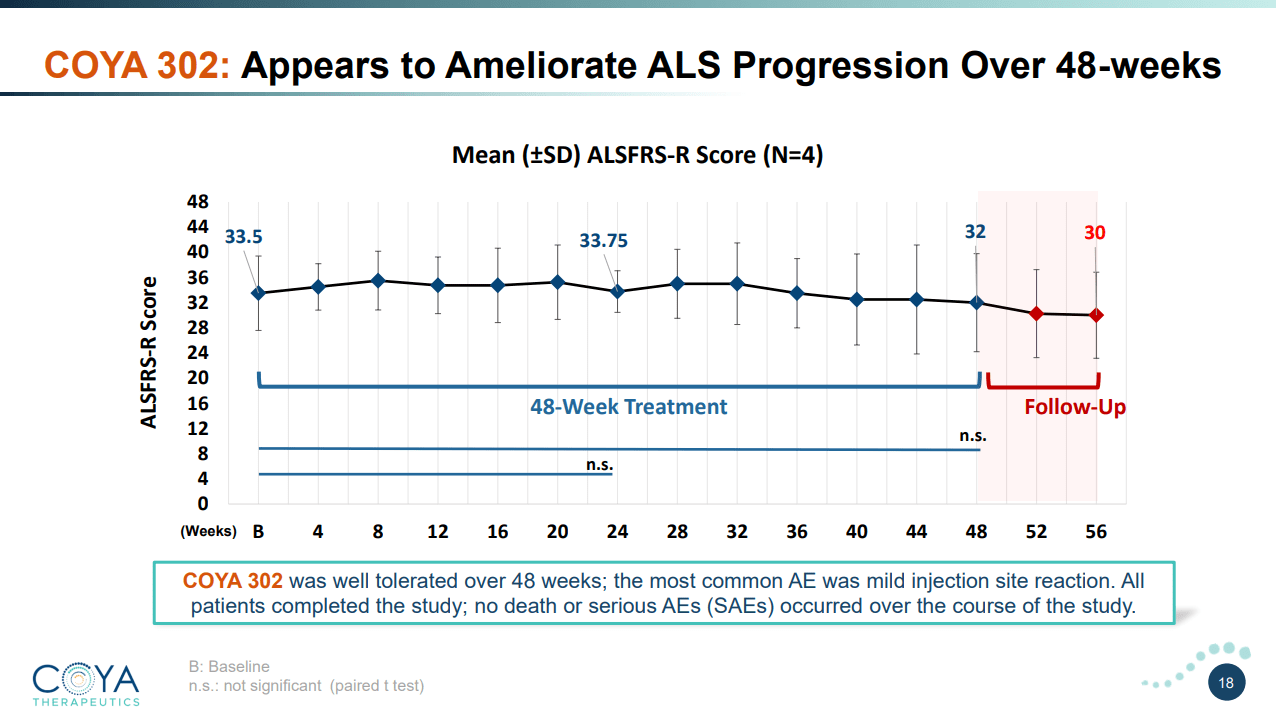

This is where COYA 302 starts to shine. Considering the company has data on only 4 patients using COYA 302, the observed efficacy signal from this study is very encouraging. The average patient decline fell by only 1.5 points over 48 weeks . Considering the average ALS patient declines at 1.02 points per month , this represents a reduction in disease progression of 88%, or essentially, a halting of disease progression, at least under the measured 48 weeks. Notably, patients taken off therapy declined at the normal rate immediately after COYA 302 therapy was terminated. Of note, these patients were declining at an average rate of 1.1 points per month before initiating treatment with COYA 302. Importantly, these improvements correlated well with measured Treg numbers, suppressive function, and other biomarkers.

COYA 302 Clinical Results (Coya Therapeutics June 2023 Investor Presentation)

{kind=link}

So while the number of patients is small, the efficacy signal was very strong and patients tolerated the treatment without any significant adverse effects. Dr. Stanley Appel conducted an ex-vivo expanded Treg cellular therapy trial which had similar results for responders with certain biomarkers. As I reviewed, I believe the endogenously expanded Tregs will perform better so it's no surprise that the phase 1 trial with COYA 302 (biologics, not ex-vivo expanded Tregs) performed better and more consistently than the cell therapy trial. While the biomarker analysis on Neurofilament Light Chain (NfL) in this study is still under review, the company has identified an even more sensitive potential biomarker in ALS with significant predictive value (results to be presented in 2H 2023). If these encouraging results are replicated in a larger phase 2 trial, along with the potential biomarker for ALS noted above, it will be difficult to deny that COYA 302 is simply in a different league than any of the available ALS therapies currently on the market and together the FDA may view COYA 302 very favorably.

The company also recently released open-label Alzheimer's disease results this year. The results look promising with no cognitive decline measured by ADAS-Cog or CDR-SB, and reductions of key proinflammatory cytokine and chemokine biomarkers. But one has to caution against any detailed interpretation of the data given Alzheimer's study cohorts are likely more susceptible to placebo responses than in ALS. As an investor or as a company executive, my opinion is that one does not want to run into the controversy that Cassava Sciences ( SAVA ) endured by leaning too heavily on a non-placebo-controlled study. Therefore, the company is awaiting the completion of a double-blind placebo-controlled study with low dose IL-2 that is funded by the Gates Foundation in 46 patients with mild to moderate Alzheimer's disease and expects to have a readout in Q2 2024 .

Approximate Valuation

What is COYA 302 worth? One has to take into account that the drug may receive accelerated approval after completing a well-sized phase 2 trial (N=120). This may only require $12-15 million in investment, so the returns could be quick (not waiting for phase 3, running a 24-week phase 2 study) and robust (only requiring $12-15 million for potential approval). A bit of simplified math would peg COYA 302's value in the hundreds of millions. Assuming the drug is at least as good as Biogen's, it should be able to bring in at least $300 million in peak sales about 8 years from now. Using a 15% discount ratio, a 4x peak sales multiple, a 40% probability of success (approval after phase 2), and subtracting $40 million for a post-approval phase 3 trial, we can arrive at an approximate current valuation of $117 million for COYA 302.

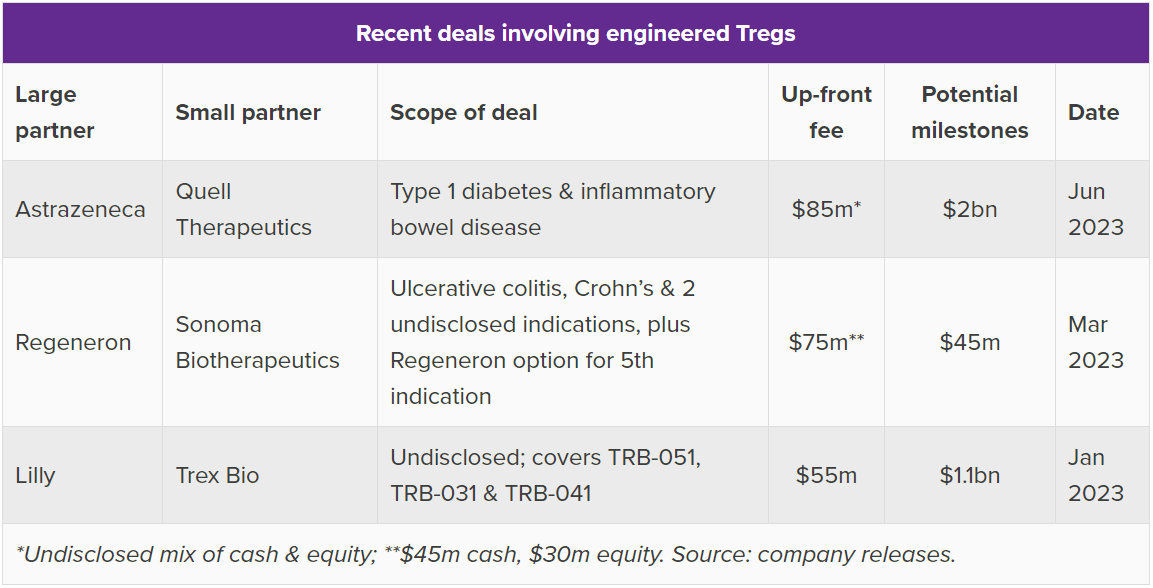

What is the rest of the company worth? Probably the best way to determine this is to understand COYA 301 (LDIL-2) as a technology platform for improving endogenous Tregs and a potential "backbone" therapy for other combinations. Big Pharma has put money down on Treg deals recently. Evaluate Pharma published a nice chart summarizing the recent deal space. Since Tregs have broad therapeutic potential, it's worth looking at Treg deals for disease indications unrelated to ALS.

Treg Pharma Deals (Evaluate Pharma)

{kind=link}

Quell Therapeutics is in Phase 1 with several collaborations and is reportedly worth $780 million . The company inked a collaboration with AstraZeneca ( AZN ) with upfront fees of $85 million, tiered royalties, and $2 billion in milestones. Sonoma was reportedly valued over $1.1 billion during the market bubble in 2021, where it raised $265 million in an oversubscribed deal. Both of these companies are in early clinical stages with engineered Tregs, and Sonoma is aiming for one-time dosing. Trex Bio is reportedly worth just under $300 million and inked a similar-sized deal with Lilly compared with Quell's deal with AstraZeneca.

These deals and valuations showcase Coya's potential undervaluation. It seems Coya should be at least trading for $200 million given COYA 302's promise, its potential for accelerated approval, and other Treg companies' valuations reaching into the billions while these companies are still moving through phase 1 trials while Coya is entering what could be a pivotal phase 2. A $200 million based on 9.95 million shares outstanding translates to $20.10/share. Fully diluted, the number comes out to $15.20/share based on 13.12 million shares.

Perhaps the most interesting thought about COYA's market potential is the size of the ALS market (5,000 Americans diagnosed every year) despite the very short 2-3 year lifespan most of them have. In 2022, the ALS market size was an estimated $673 million . If patients can have their disease progression halted as Coya showed in their proof of concept, these patients may not die and the market size could explode. The market size for COYA 302 could potentially be significantly greater than the current ALS market today, though this is optimistic speculation.

Financials

The company recently released its quarterly report showing it had $13.1 million in cash and cash equivalents as of June 30th. The company had a cost of operations of $12.9 million in the last year. They also owe Dr. Reddy's, the company that they in-licensed abatacept (a-CTLA-4 part of COYA 302) from, $2.9 million in pre-approval milestones. According to the agreement press release :

COYA 302 is comprised of two components - COYA 301 and CTLA4-Ig. Coya will develop COYA 301. Under the terms of the Agreement, Coya has been granted an exclusive, royalty-bearing license to Dr. Reddy's proposed biosimilar Abatacept for the development and commercialization of Coya 302 for the treatment of certain neurological diseases for sale in multiple territories including North and South America, the EU, United Kingdom, and Japan. As consideration for the license, Coya will pay a one-time non-refundable upfront fee to Dr. Reddy's. In addition, Coya will owe tiered payments to Dr. Reddy's based upon Coya's achievement of certain developmental milestones. Coya will also owe royalties to Dr. Reddy's on Net Sales of Coya 302 within its licensed territory on a tiered basis. The Agreement does not preclude Dr. Reddy's from launching its proposed biosimilar Abatacept globally for approved indications post regulatory approval. [...] The Agreement also provides for the license of Coya 301, Coya's low dose IL-2 to Dr. Reddy's to permit the commercialization by Dr. Reddy's of Coya 302 in territories not otherwise granted to Coya. Coya will receive royalties on Net Sales by Dr. Reddy's in their territories based on the same tiered structure as Coya owes Dr. Reddy's. The Agreement also allows Dr. Reddy's and Coya to enter into a mutually satisfactory commercial supply agreement at an appropriate time.

So the agreement goes both ways; there are parallel royalty-bearing licenses. The company also owes $13.25 million in milestones to ARScience Biotherapeutics for the low-dose IL-2 formulations as well as royalties (10-20% on sublicensed products), all for COYA 302. How much is due soon is unknown.

Therefore, it is reasonable to think that a license with upfront payments is executed in the near term and/or the company raises additional funds, most likely through an equity offering. The company's business development executive has a good track record but there are never any guarantees.

Management And Investors

First things first, David Einhorn, the famous billionaire who runs Greenlight Capital, has invested a significant sum into Coya (and also Gain Therapeutics ( GANX ), another company I've written about). Einhorn's typical investments are not high-risk biotech companies, so this is a nice vote of confidence. As for the rest of management, it's worth highlighting Dr. Stanley Appel's involvement on the company's scientific advisory board. Appel is a world-renowned, distinguished ALS researcher and clinician who has led Treg research into neurological disease. Management has invested personally along with board members, with the CEO, Howard Berman, owning almost 1 million shares.

The company recently brought on Arun Swaminathan, a seasoned business development executive who has a great track record of making deals with major pharma as evidenced by Alteogen's stock price performance under his tenure. Swaminathan also has had an impressive career at Covance (now LabCorp ( LH )) and Bristol-Myers ( BMY ). His LinkedIn page highlights his biz dev accomplishments well:

Within 1 year of joining Actinium, he successfully moved forward negotiations to closure and executed a $452M deal with $35M upfront. Prior to Actinium, he was the CBO at Alteogen (196170.KQ) where he spearheaded over $6B in deals, including deals with two of the top 10 global pharma companies and a $1B+ deal within the first year of assuming the role of CBO.

The company has been publicly open about partnering COYA 301 with other therapeutics for different indications, as well as licensing its exosomes platform for further research. With Swaminathan joining the team, great early ALS data, and a platform product all under the new Chief Business Development Officer's watch, it's not unreasonable to think the company could be seeing some exciting deals inked within the next year or two.

Risks

Coya is a mid-stage, pre-revenue biotech. With that comes risks including but not limited to dilution, funding concerns, clinical and preclinical study failures, regulatory risks, and high market volatility. With regards to funding, there are also unknowns in the company's current licensing agreements with ARS and DRL regarding abatacept and the IL-2 formulations.

There is also the risk of other market entrants that also may perform similarly to COYA 302. It's also important to note that the phase 1 trial Coya ran is a very small sample size and it's entirely possible that these results looked so positive due to chance. However, one does have to note the patient ALSFRS-R score declined resuming immediately after therapy was terminated.

Currently, the company also has quite a low trading volume and so entering and exiting an investment position could be challenging, though trading volume may change. Certainly, portfolio weighting should be taken into account given the low trading volume, numerous relatively high risks, and low market capitalization.

Conclusion

Coya offers investors a unique approach to investing in diseases driven by immune dysfunction, starting with ALS. The company has generated extremely encouraging early-stage data, with ALS progression essentially eliminated during therapy. COYA 302 could turn out to be the best ALS therapy on the market if subsequent clinical trials mirror early-stage results. With the company's phase 2 trial potentially being pivotal, they could have a shorter path to approval and commercialization than other biotech companies in their stage of development.

COYA 301 could be used as a backbone for additional combination therapies for other diseases driven by immune dysfunction. There may be an additional upside to the stock if the company can ink development deals with other companies using COYA 301 in combination with other therapeutic agents. However, the base case for an investment in Coya is the ALS indication, where the stock appears significantly undervalued based on COYA 302 in a risk-adjusted peak sales multiple estimation.

An investment in the company comes with significant risks which are common to early to mid-stage biotech companies operating with limited budgets and in need of additional future capital. Investors interested in Coya should size positions appropriately to their portfolio size and risk tolerance.

For further details see:

Capitalizing On Inflammation's Role In Neurological Disease Part 1: Coya Therapeutics