CRLFF - Cardinal Energy: An Unhedged Liquids-Rich Oil Producer Rating Upgrade

2023-08-17 10:43:34 ET

Summary

- Cardinal Energy is an oil producer with a production split between light oil and medium/heavy oil.

- Due to the recent underperformance, the lack of hedges could present an opportunity for bullish oil investors.

- Q2-23 results showed a slight decrease in production compared to Q1, but adjusted funds flow increased by 7%.

Investment Thesis

Cardinal Energy (CRLFF) is an oil producer, which I covered earlier this year , and I added it to the portfolio during the weakness we saw recently before energy prices recovered some. This article discusses the Q2-23 result, which was released a few weeks ago, and my general views on the company.

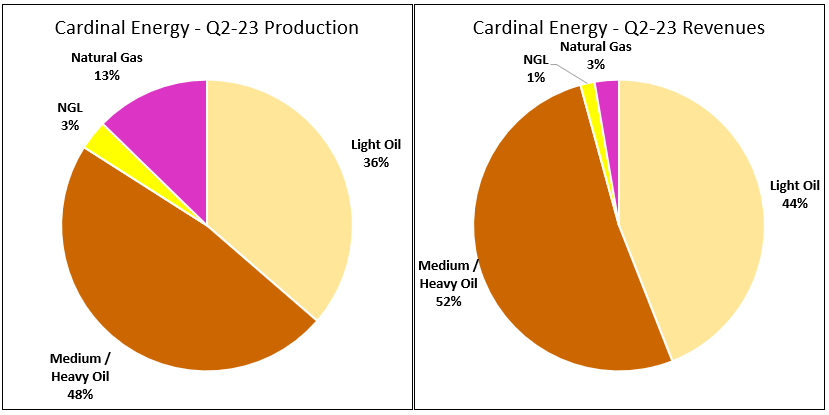

Figure 1 - Source: Data from Q2-23 MDA

{kind=link}

The company derives most of its production and revenues from crude oil, which is in turn split between light oil and medium/heavy oil. So, Cardinal Energy has been less impacted by the lower natural gas prices lately, compared to some of its peers.

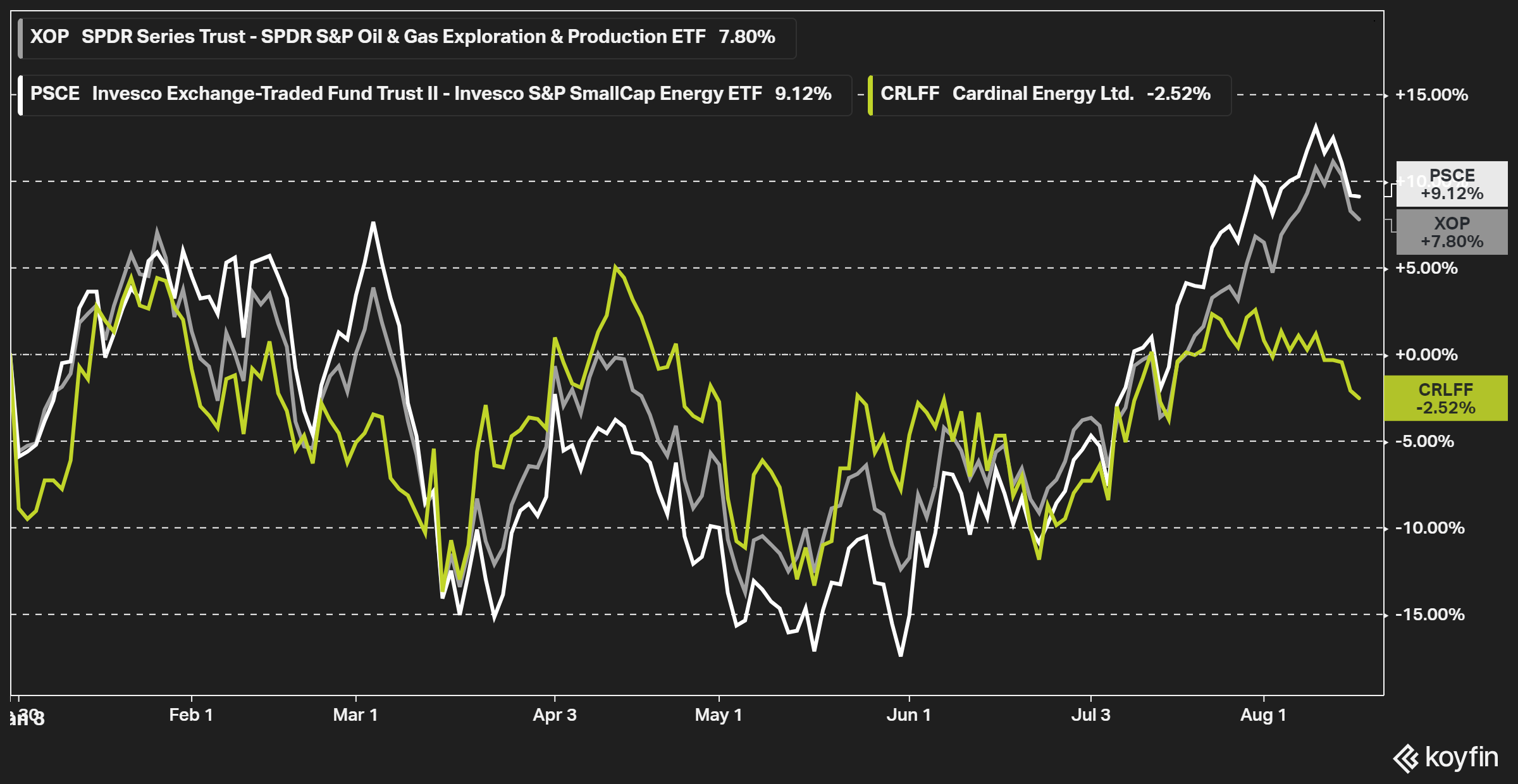

However, the stock has despite the liquids-rich production profile underperformed some of the regular industry ETFs in 2023. Given that Cardinal Energy has few hedges in place, the recent underperformance could be an opportunity to add or increase a position in Cardinal Energy for anyone with a bullish view on the price of oil.

{kind=link}

Q2-23 Result

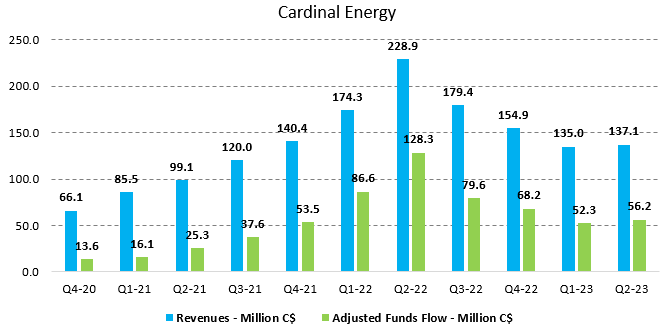

Cardinal Energy was like many other Canadian oil & natural gas producers impacted by the forest fires during Q2-23, where 700 boe/d was temporarily shut down. The company has since managed to restart all curtailed operations. The average production in the quarter was 21,047 boe/d, which is a slight decrease compared to Q1 at 21,726 boe/d. Current production is around 22,000 boe/d, on par with the annual guidance. The expectation is for H2-23 production to go above the annual guidance volume.

Figure 3 - Source: Cardinal Energy Quarterly Reports

{kind=link}

Adjusted funds flow in the quarter was C$56.2M, up 7% compared to Q1, which is primarily due to a higher realized price for its medium/heavy oil. Light oil and natural gas prices did otherwise decline in Q2 compared to Q1.

Figure 4 - Source: Cardinal Energy Quarterly Reports

{kind=link}

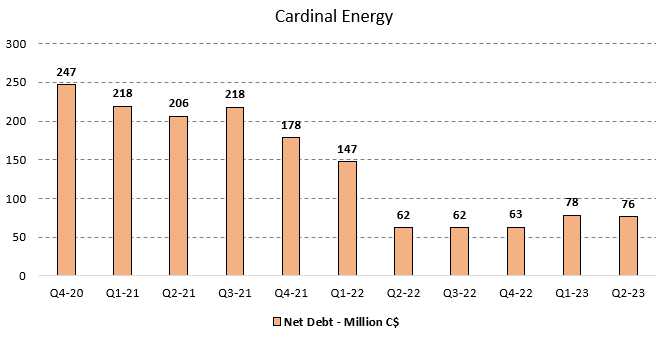

The stronger cash flow in the quarter led to a very slight decrease in the net debt from C$78M last quarter to C$76M in Q2. So, the company continues to have very little financial leverage.

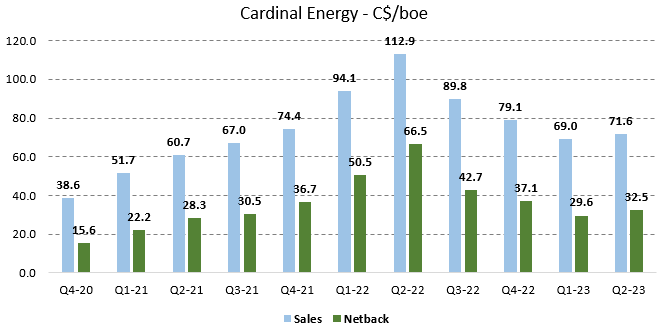

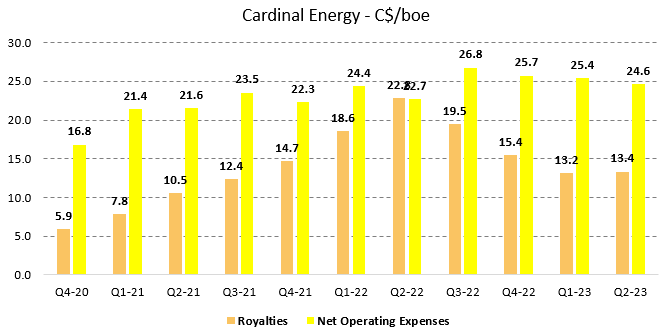

Costs

In the charts below, we can see the sales price, netback, and a cost over time. Where the realized sales price is down substantially from the highs seen last year, but the company did still generate a solid netback of C$32.5/boe in the most recent quarter.

Figure 5 - Source: Cardinal Energy Quarterly Reports

{kind=link}

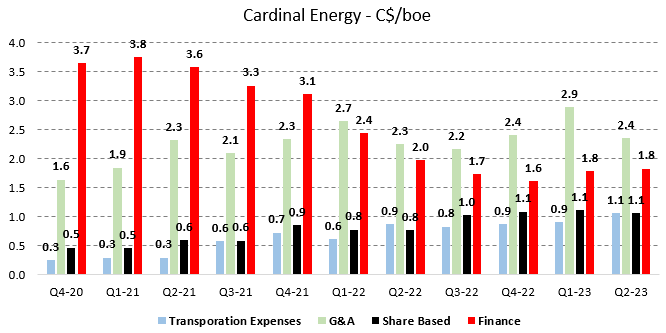

Among the larger costs, royalties have, as expected, decreased in-line with a lower sales price. Net operating expenses have otherwise been relatively flat over the last few quarters, even if we have seen some increases in costs over the last few years, which is partly to be expected due to higher inflation and higher energy prices. We can also see how the decreased financial leverage has cut the financing cost in half over the last few years, despite the increase in interest rates.

Figure 6 - Source: Cardinal Energy Quarterly Reports Figure 7 - Source: Cardinal Energy Quarterly Reports

{kind=link}

{kind=link}

Conclusion

Cardinal Energy is a liquids-rich producer, with low financial leverage, and is unhedged, except for a few WCS basis contracts that can be seen below. This is the type of exposure which I think has a good chance of outperforming over the next couple of years.

Figure 8 - Source: Cardinal Energy Q2-23 MDA

The company pays a very attractive dividend yield of 10.3%, using the latest share price, with monthly distributions. That dividend is covered at the current oil price and a marginally lower WTI price, a little bit dependent on how Western Canadian Select holds up as well, which has done well so far this year.

Having said that, one of the main risks for the company would be a dividend cut, which could happen if saw an extended period of lower energy prices. A dividend of this magnitude often attracts investors primarily focused on that payment, where a cut would naturally lead to quite a bit of selling. However, I think the upside risk is higher than the downside risk for the oil price, which is why that is an acceptable risk for me.

It is also worth pointing out that H2-23 is likely to be better than H1-23 for Cardinal Energy due to a higher production volume together with, what at least so far looks like a higher oil price.

For further details see:

Cardinal Energy: An Unhedged Liquids-Rich Oil Producer, Rating Upgrade