CWQXF - Castellum: An Analysis And Why I'm At A 'Hold'

2023-04-11 14:57:27 ET

Summary

- My long-term holding in Castellum was, for the most part, sold off during extreme highs during last year. When the company hit 225 SEK+, I sold over 80%.

- This proved to be the right choice, as Castellum since has gone into a mix of infighting between large shareholders, and some interest rate issues.

- Despite solid fundamentals, the company saw it necessary to cut its dividend.

- Here is how I currently invest in the company and what my outlook is.

Dear readers,

My last public articles on Castellum ( CWQXF ) were at "BUY", and "HOLD", but they were published over 2.5 years ago on Seeking Alpha. There is a reason for this. Since those articles, Castellum, due to fighting between large shareholders in Sweden, has become a somewhat problematic stock, at least in the short term. The long-term appeal of its assets is very much intact, but the battle over who controls Castellum has been going on since pretty much mid-2021.

Revisiting Castellum

In February of this year, this led to the previous CEO and large stakeholder, Rutger Arnult, choosing to leave the board immediately and declare his stake in the company to "no longer be of strategic long-term value", but more as a financial investment.

As the company argues, the cutting/elimination of its dividend was necessary due to market interest rate changes. This argument came from the new entrant into the company, Roger Akelius, who'd expanded his stake. It was his demand of cutting the dividend that I view as leading to the decision to do so. ( Source ) I view this as incorrect, and part of the battle of the leadership for the company, given that large stakeholders bought massive amounts of shares at what was viewed as a cheap valuation, only to then be proven wrong as the stock crashed further, briefly dropping below 110 SEK. It would be speculation to say that the dividend was cut to cut shareholders' ability to pay down the debt and then used to increase their stake in the company - but at the same time, it's a very logical move to make, given Akelius goals in going into the company. Akelius now owns 12.8% of the voting power, and Arnhult is down to a mere 4.8%. His dumping of shares is part of what has resulted in the last 6 months of share price movements.

{kind=link}

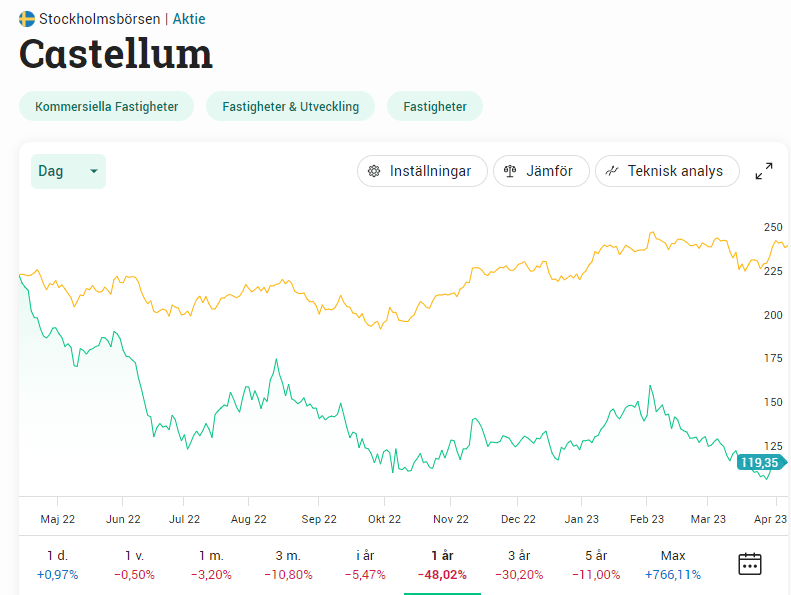

I'm happy that I recognized the overvaluation inherent in the company and sold at a significant profit. When I sold, Castellum was more than 9% of my total portfolio. That is also the reason I sold - it had grown far too large, and it doesn't pay off, in many cases, to sit on 3-digit RoR, especially not overvalued RE in a potentially rising interest rate environment.

Of course, I'm also a value investor. And Castellum is now trading at a price to NAV of less than 0.48x, which is one of the steepest discounts Castellum has ever seen for the past decade.

So why am I not buying? Are results not good, or indicating further trouble?

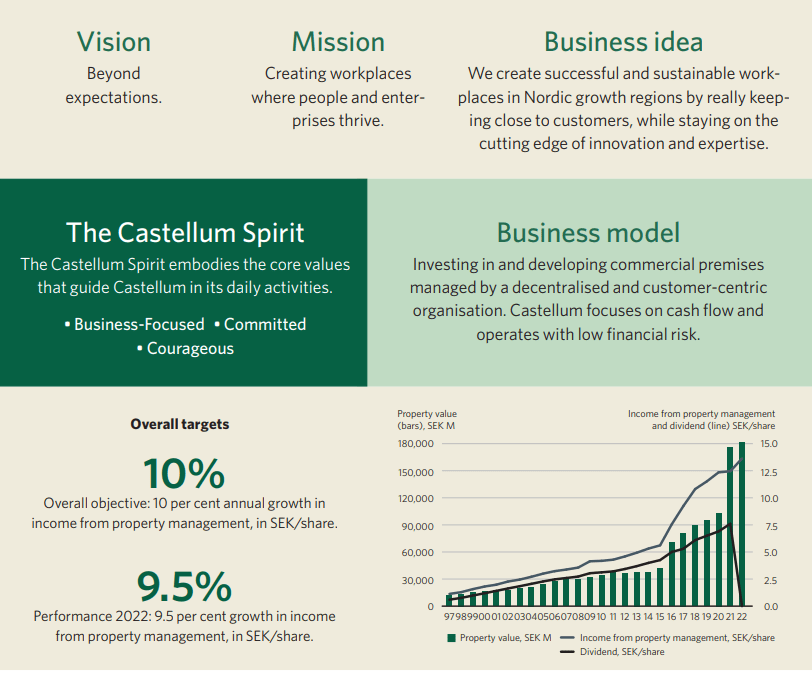

The 2022 results were good - at least in some ways. The company generated nearly SEK 9B of income but dropped almost 80% in net - while prop value when up by over 5B, and property management increased by almost a full billion. However, next to income we have soft indicators like "sustainability-certified properties" and "equality". While these are not unimportant, they pale, in my opinion, to actual relevant financial indicators. Whenever a company begins by presenting such things, you know something else might not be entirely right. In this case, it's obvious.

The merger with Kungsleden and the other things happening in the company in terms of leadership have left Castellum without a dividend (it's calling it "paused", but no - it's a cut in my view).

I'm not saying, by the way, that the issues are all at the company's management level. The economic slowdown we're seeing is of course, real. And while Castellum has a very diverse and good mix of tenants, including over 10-15% public tenants who do not become delinquent, in the end, Castellum is mostly an Office property RE business - and this comes with both risk and correlation when we look the growth prospects.

In short, Castellum is most definitely slowing down.

Castellum is presenting results much in this light. A troubled world, but with Castellum performing very well and beyond expectations. The company targets double-digit annual growth in income from property management, something it has managed fairly well for the past 20 years. The one key thing that happened though, was this.

{kind=link}

The focus on the "soft" indicators continues, at the top of the company's annual report, for much of the first segment - again, as I believe it is indicative for what we should expect out of the company. I do not think it's fair to say that Castellum quickly will communicate a restored dividend. if they do restore it, it will likely be at a lower level than before. At the time of my selling Castellum, I was at a YoC of nearly 6.5%.

We can also see the changes in "why" Castellum thinks that investing in the company is a good idea.

{kind=link}

Gone are the profit-focused metrics, gone are dividends, and instead, we look at "innovation", "local business", "sustainable", and a well-diversified portfolio, which I view as a must, not as an optional thing.

As you can probably tell by my rhetoric, I am not a big fan of what has been going on over the last 6-7 months. It doesn't have anything to do with the people involved, more that their power play went out over shareholders. The notion that Castellum's dividend was unsafe is one I view as false. Would it have stretched finances? Somewhat, perhaps. But it would in no way have been untenable.

Whenever management drama and power play goes out over shareholders, that is a company I avoid, 100%, until I see it as likely that it's settled down.

A good example of this, also in Sweden, was Hemfosa AB. This was another large Swedish RE company, owned and managed by one of the most capable teams in the country (now in charge of Nyfosa). However, they sold their property portfolio to another business, SBB AB (No symbol), managed by Ilija Batljan, who has made a history of overleveraged and risky bets and headlines in the real estate sector. As soon as I got my shares in trade, I logged on and sold every single share of the company I'd gotten. Hemfosa was, for me, a 5.5% position at the time. This is a lot of capital to have to reinvest, at what wasn't really an attractive overall market.

But was it the right choice? Well, I could have held on until the bubble and sold at 40-50 SEK, but that would have been speculative. Instead, I sold at 25 SEK - the share price today is 13.

I view this as the right choice. I don't really trust management teams that make headlines like that, or act in a volatile manner as I view it, unbefitting to their position or their relationship with their shareholders.

So I avoid such companies. Just as I, unfortunately, had to do with Castellum.

At least for the most part.

You might expect that Castellum's financials are in disarray due to the canceled dividend. That is not the case. LTV is at 42%, which is above the 40% policy (65% commitment), but interest coverage is at almost 4x (3x policy), with average debt maturity of 3.1 years. A quick glance at debt maturities also gives us the picture that isn't currently exposed to any material interest rate risk, at an average of 2.7%. However, the latest refi's are at a rate of 7.2%, to be compared to the 0.3% that Castellum borrowed not 3-4 years ago. So there will come a crunch, but it won't be breaking with regard to the company's credit commitments.

The dividend cancellation by Castellum (I will continue to say cancellation, despite management's use of the word "pause", because they do not give an estimated time to "unpause") makes the company a harder investment, especially together with management (though I now view the battle for Castellum as over - Arnhult lost, Akelius won), but it does not make Castellum uninvestable.

In fact, I have been investing in Castellum during all this time.

How?

Valuation and investing in Castellum

While it's too early to say just when the dividend will return and when things will settle down, I know one thing. Castellum is worth a lot more than 110 SEK, and the P/NAV of 0.45x.

For that reason, I've been writing cash-secured Put options. These have netted annualized RoR of between 11-36%, depending on where I've "caught" the company, and not a single one has, thus far, expired ITM. I currently have two running with expirations in 2 weeks at strikes of below 110. If I am assigned at that price, I will happily hold (or maybe sell at a profit, I'm not sure), because the company is worth more than that.

You could buy the common shares. In fact, even with management issues and with the dividend cut and the interest rate uncertainty, I believe that Castellum, including Kungsleden, is worth well above 150 SEK/share in any way, shape, or form.

S&P Global analysts following the company give it a range of 90 SEK on the low to 190 SEK on the high, with analysts uncertain of where to go. The average is at 145 SEK, 2 at "BUY", 2 at "HOLD", and 2 at "Underperform" or "SELL". This move caught everyone by surprise, including experienced analysts like myself who've followed Castellum for pretty much my entire investment career.

Had you asked me a few years back, I would have told you there is no way Castellum is doing this or going anywhere - but this goes to show you, no company is really truly safe. All you can do is make the best-informed investment choices, both "BUY" and "SELL" that you can, and don't think that any one holding is safe ad infinitum.

Castellum has one of the best portfolios in real estate in Sweden, bar none, when it comes to office and production space. While the company has taken a tumble due to changes in management and some worries in terms of the economy and interest rates, the market is, as I see it, overlooking some fundamental strengths that should not be ignored. The company is worth a lot more than it's currently being traded at.

However, with declining margins, debt growth, interest cost growth, altman-z score declines, low interest coverage, and lowering profitability, I do not judge investors for taking a cautious step back to see where things actually go. Given that I myself use options to invest (or not invest) in Castellum here, I too am taking the cautious road, since I'm making sure my strikes are below 110 SEK/share - at least for the time being.

I will be watching Castellum with curiosity to see when it would be tenable to once again invest in the common shares. For now, that's not something I'd be interested in doing.

This is my thesis on Castellum as it currently stands.

Thesis

- I sold Castellum at a significant profit, and I am very happy that I did so. It was perhaps the best example of me following my "SELL"/Trim rules when a stock becomes overvalued. The capital I reinvested from Castellum has stayed relatively stable and has not declined over 45% since. The company remains a business with a solid asset portfolio but has taken damage in the management/trust perspective, and I am unwilling to move any closer here with my capital until I see some signs of things calming down.

- My current approach involves writing medium-dated CSPs with strikes at least 15-20% below the current share price, and I have done so successfully for 3-4 months at this point without a single assignment. Even if one had been assigned, I would have been able to sell it at a profit at the current price.

- For the time being, due to the trouble in the company, I'm bullish on the company, but I believe put options are the way to go here. The common shares do come at a PT of 140-150 SEK/share long-term, but there's plenty that could happen until then. I do not see the upside to buying the common shares yet.

- Because of that, I am on a "HOLD".

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company doesn't fulfill my safe/conservative indicators, nor my dividend requirement. For that, and everything said above, I'm at a "HOLD".

For further details see:

Castellum: An Analysis, And Why I'm At A 'Hold'