CWQXF - Castellum: The Upside Is Crystallizing (Rating Upgrade)

2023-06-29 11:42:21 ET

Summary

- I have previously written about Castellum and sold a significant 8% portfolio stake, but continue to monitor the company for potential investment opportunities.

- Despite a recent decline in the company's value, I believe it is unlikely to decrease much further without significant economic changes, even including interest rates.

- I review the latest results from Castellum to determine if it is becoming a more attractive investment opportunity - and I'm switching to a "BUY".

Dear readers/followers,

I've been a fairly frequent writer on Castellum (CWQXF) both before and after selling my relatively massive 8%+ portfolio stake, leaving me with a small watchlist position to determine my next point of entry. My last article on the company was published in April of 2023, and this was at a "HOLD". The company has declined since then, and the S&P500 is up. That makes that very short-term thesis a correct one as things stand.

While it's premature to say that we're in a position to go completely positive on Castellum as an investment here, I think it's fair to say that the company isn't going much lower without some significant headwinds from here on out. Those headwinds may materialize - Sweden is particularly somewhat "late" to raise interest rates.

But, I don't see given the company's portfolio, that we're seeing much lower levels here for the longer term.

Let's see the latest results and what causes my update here.

Castellum - The company is starting to look interesting here

So, Castellum remains a high-quality play on the Swedish property sector. The removal, even if temporary, of the company's storied dividend was a bit of a problem, but not a problem for me as an investor. The reason is that I sold most of my Castellum at insane highs of over 200 SEK/share - a price the company is not justified in trading at.

This leaves me with a rather unexciting watchlist position, observing the company as it struggles, naturally without its appealing dividend, to climb back above the 120-130 SEK level.

As I mentioned before, the reason for the dividend cut and the struggle in Castellum was a fierce battle between a former CEO and a large stakeholder which ultimately "lost" the battle when he resigned and sold much of his previously massive Castellum investment, and left a more conservative owner to take the reins. I won't call Akelius dividend-hostile - but he doesn't have the same view as the previous large stakeholder has, and his first act was cutting that dividend to zero temporarily - and that's where we currently are.

It would be speculation to say that the dividend was cut to cut shareholders' ability to pay down the debt and then used to increase their stake in the company - but at the same time, it's a very logical move to make, given Akelius (the new large shareholders) goals in going into the company, which was to lower the leverage and "prepare" the company for the interest rate changes we're currently in.

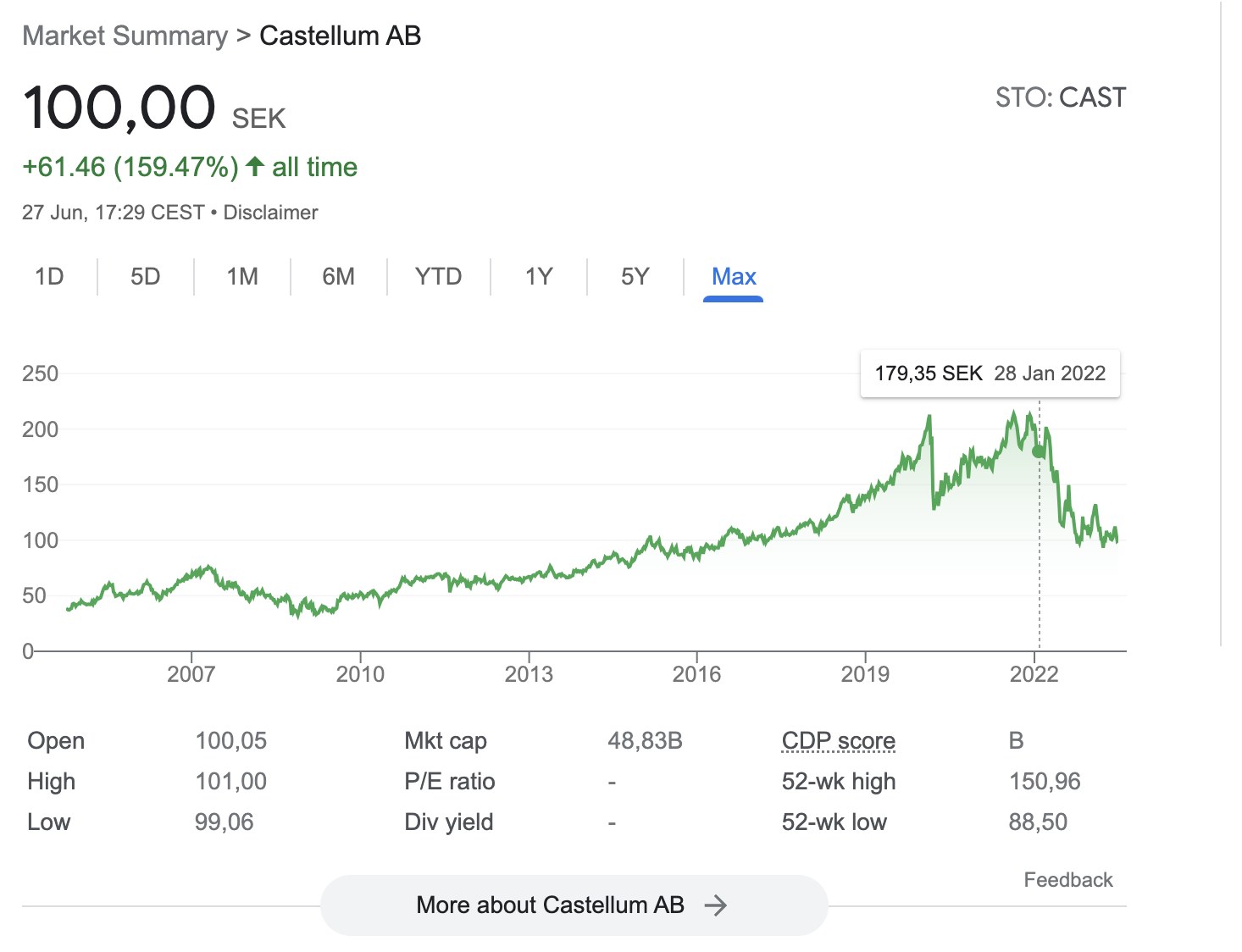

Akelius now owns 12.8% of the voting power, and Arnhult is down to a mere 4.8%. His dumping of shares is part of what has resulted in the last 8-10 months of share price movements that have left Castellum trading at less than 105 SEK as of this time, with a current share price of exactly 100 SEK less than 20 minutes before market opening today, on the 28th of June.

Castellum share price (Google Finance)

{kind=link}

This was one of the biggest bullets I ever "dodged", because Castellum was almost 10% of my total portfolio - a position in the hundreds of thousands of dollars, and I managed to lock in a 140% profit as opposed to a small loss as the position stands today. It highlights the importance of profit rotation , a concept many conservative dividend investors are less familiar with or not exercising as they should - in my humble opinion.

The market is a very big place - an international place. Any investment can always be replaced by something of quality and at a lower valuation. You should not make excuses for companies trading above, or below where they "should" trade - instead, every investment should have a target both on the upside and the downside that causes you to act. To not do so, in my opinion, means that the investor doesn't fully understand the limitations of the company.

That doesn't mean a thesis can't change. I frequently update/raise my price targets - but this needs to be done conscientiously and clearly.

Castellum, for instance, was no longer the company I had once invested in. The company merged with Swedish Kungsleden, which changed the sort of business it was in terms of its dividend payout ability - even if its fundamentals are very much intact.

I want to reiterate as of this article, and the main reason for my thesis change, that I do not see an elevated level of risk here. Not at this price. At close to a double-digit share price, you're buying the company at a very cheap valuation - more on that in a bit - but the issues or risks , as I see them, are actually at the management level , not in terms of the properties operating income or same-store cash flow trends.

{kind=link}

While there is some current uncertainty and issues in the Swedish property market, including the fact that Swedish tenants overall are fairly high-leveraged, the overall picture of the Swedish market is a continued positive one in terms of demand. I'm talking occupancy trends, I'm talking leasing spreads. The company's income is actually positive and up, with a total 12.6% increase. This was mostly due to indexed leases, renegotiations, and new letting. So the trends in the share price, are in no way reflective of a declined demand or interest in the company's properties, but rather in the macro and overarching trends on the market.

So while risks do exist - and it's entirely possible that parts of these forecasts that I am making turn out to be incorrect if the interest rate increases go higher and longer than I assume (3-4 years at this point before going down, given the Swedish FED rate cycle), it's equally important to remember that Castellum has already done the biggest thing to solve payment risks - namely cutting their dividend. Because of this, forecasts for GAAP/EPS and OCF/FFO are in the positive going forward, and there isn't an estimate that is forecasting negative adjusted EPS for the company - the lowest current being 8.7 SEK/share in 2023 (Source: FactSet).

{kind=link}

Net operating costs, for instance - up almost 25% in the first quarter, due mostly to hedging for energy costs. These are non-recurring though, and they will settle back to normalized levels over time.

The Swedish property market remains problematic though. An already high level of leverage in market participants coupled with the resulting demand for high yield results in a very anemic/sluggish transactional market, with many of the objects available actually at poorer quality. New construction has declined- it's not at a standstill, but it's not n a good place. Castellum delivered two new buildings which reflect the company's focus - a public building for the court, and a new head office for E.ON (EONGY) - but these were exceptions in an otherwise tepid market.

The outlook going forward is mixed. Castellum's assets are top-tier and will continue to make money. However, due to increased interest costs and Sweden having to raise rates for longer and higher than other countries due to that increased leverage and not having raised at the same pace as other nations (which has impacted our currency, that is currently at the lowest level in history in some FX perspectives), the outlook for the company on a high level is definitely not without its issues.

Castellum will have to rely on its public tenants, its long-lasting banking relationships and its management skill in order to navigate an environment that goes from borrowing costs of less than 1% to above 3-5% over time. This will of course impact the dividend the company may pay, as well as what the company may earn overall.

However, Castellum is one of the most conservative RE companies in the nation, and not even close to the same quality as a declining business like SBB which is close to going bankrupt due to an elevated, 70%+ leverage. Castellum is at less than 45% LTV, with an average effective debt interest rate of 2.8%, still investment-grade, and 51% unsecured assets.

Most of the company's ongoing projects are already pre-letted, and many of them are to the public sector, which does not "reneg" on deals or buildings such as this. Property values, which have been propped up and rising for years, will now normalize somewhat - and we'll have to be prepared for this - but the current valuation already assumes a massive devaluation of the values.

Let me show you what the valuation trends actually say about the company here.

Valuation for Castellum - I'm updating my rating

So, to put it very simply and succinctly. The company is being significantly undervalued to what it is able to do, and even in a company with no dividend, there is a limit to the degree of market irrationality that I will accept. That degree has now been reached.

At close to a double-digit share price, the company represents a 0.38x to its NAV, and given the company's degree of publicly-let buildings, and its conservative overall profile, this is undervalued to the degree we see in companies like Vonovia (VONOY) and others. What do I mean by this? In this case, I mean that Vonovia is being valued at 0.45x to NAV from a share price basis, while Castellum is below 0.4x at the current share price. Given the relative size differences of the company as well as the overall quality, I believe both of them are undervalued - but Castellum even moreso. Castellum is not a REIT, so we can better use metrics like P/E - where the company typically trades at 15-16x P/E premiums, and currently trades close to 10x. That 140-150x target marks a range of that 15-16x P/E, based on conservative forecasts assuming very little (or no) growth in earnings over the next 2 years.

Currently, 9 analysts follow Castellum, and out of those 9, 6 are either at "BUY" or "Outperform". The company's average PT is 121 SEK, which is interesting when you consider that less than a year ago, that same average PT was over 100 SEK higher and no analyst considered Castellum worth less than 190 SEK.

Today, the lowest share price from an analyst is 85 SEK.

This is why I listen very little to such short-term analysts but instead build far longer-lasting models and account for changes in the market and other assumptions.

I say to you that the potential upside for Castellum based on a 140-150 SEK PT is significant - almost 50% here. This PT is derived from a conservatively adjusted 0.5-0.6x P/NAV, including the inclusion of Kungsleden in the company as of the merger more than 10 months back.

Such an upside will take significant time to materialize, that is true - but I have no doubt it eventually will come.

Normalization to 15-16x in terms of earnings comes with a potential upside of 50% total RoR - and that is without a dividend and with a negative 7-8% earnings growth rate for the next 2-3 years. This showcases the degree of undervaluation the company is currently under.

As I said - at close to, or at double-digit share price levels, this company goes from being just a CSP target for me to me actually buying shares on the market. The upside is too good, and the fundamentals for what the company does - management coupled with portfolio and earnings - are too solid. I see no downside where this investment, in the long term, could realistically lead to a loss of capital, and that is why I "BUY" here and change my rating.

My updated thesis is as follows.

Thesis

- I sold Castellum at a significant profit, and I am very happy that I did so. It was perhaps the best example of me following my "SELL"/Trim rules when a stock becomes overvalued. The capital I reinvested from Castellum has stayed relatively stable and has not declined over 45% since. The company remains a business with a solid asset portfolio but has taken damage in the management/trust perspective, and I am unwilling to move any closer here with my capital until I see some signs of things calming down.

- My current approach involves writing medium-dated CSPs with strikes at least 15-20% below the current share price, and I have done so successfully for 3-4 months at this point without a single assignment. Even if one had been assigned, I would have been able to sell it at a profit at the current price.

- For the time being, due to the trouble in the company, I'm bullish on the company, but I believe put options are the way to go here if the price is above 120 SEK. The common shares do come at a PT of 140-150 SEK/share long-term, but there's plenty that could happen until then. I do not see the upside to buying the common shares yet.

- At a near-double-digit share price though, in addition to my conservative CSPs, I'm starting to "BUY" common shares. Why? Because at 100 SEK/share, the company is being valued at less than 0.4x to its NAV, which is insane.

- I'm switching to "BUY" here in my thesis and I'm buying shares.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I now view the company as a "BUY" due to massive undervaluation, despite what's going on in the property market.

For further details see:

Castellum: The Upside Is Crystallizing (Rating Upgrade)