CWQXF - Castellum: The Upside Is Significant In Case Of A Fair-Value Reversal

2023-09-12 23:15:11 ET

Summary

- Castellum's share price has seen some ups and downs but is still not at fair value.

- The company has changed due to management changes and is no longer a high-yielding dividend stock.

- Castellum remains a high-quality player in the Swedish property sector, but macro and interest-rate risks persist.

Dear readers/followers,

In my last article on Castellum ( CWQXF ) back in June, I changed my rating to a "BUY" as the company traded at what I consider to be close to trough valuations. The company has, since that point, really seen some advancement in terms of share price - some ups and also some downs. But it's nowhere near to where I would consider it being traded at fair value.

That being said, even if we have a very attractive Swedish RE market in terms of availability and market dynamics - which we can see in the quarterly results - problems do persist, and Castellum is not the ultra-value dividend-paying compounded that I once invested in. The politicking in the company has changed that. I don't believe it will ever go back to being a 4-5 %-yielding company in RE.

That combined with what I believe management to be aiming for means that I'm currently mostly out of the company, only slowly adding to a position that was once over 5% of my conservative dividend portfolio but has become less than 0.5% for the time being.

Let's see what sort of trends we have here compared to my last article, and where the upside for this company lies.

Castellum - Things to like, but macro risks and company risks are present

With the exception of companies that have been around as long as Castellum itself, this business is probably one of the highest-quality plays on the Swedish property sector that exists. I didn't necessarily see the dividend cut as a problem - because I was at the time already out of the investment, having sold my position at an insane overvaluation of 200 SEK per share. This investment, which at one time was over 7% of my portfolio due to share price appreciation, has become my "landmark" case for rotating and trimming overvalued investments. My 100%+ RoR would have been a 25% one if I had waited a year longer.

My watchlist position which remains to this day has been trading in the 100-130 SEK range for some time.

The reason for the dividend cut wasn't, as I argue, a lack of safety in the business. Castellum could very likely have continued to pay out the dividend without issue. The LTV was and is solid. Yes, exposures to floating rates were and are higher than I'd have liked, but the company really hasn't seen the sort of deterioration we would associate with the need for a dividend cut.

The reason for the dividend cut and the struggle in Castellum was a fierce battle between a former CEO and a large stakeholder which ultimately "lost" the battle when he resigned and sold much of his previously massive Castellum investment, and left a more conservative owner to take the reins.

The new captain at the helm, while not dividend-hostile, has no interest, as I see it, in turning the company back to a 4-5% yielding business. Akelius now owns 12.8% of the voting power, and Arnhult is down to a mere 4.8%. His dumping of shares is part of what has resulted in the last 8-10 months of share price movements. Castellum, as of this specific date, trades at 115 SEK and has stayed in the aforementioned range for months.

The 2Q23 again confirms that the need for a dividend cut was hardly clear. With a 12.6% YoY increase in rental income, a 10.5% increase in NOI, a lease value of nearly 10B SEK, and an economic occupancy over 92.5%, the only negatives for this company are the income from property management and changes in NAV - which are completely expected in this sort of environment.

{kind=link}

Castellum is, without any doubt in my mind, one of the highest-quality plays you can make on the entire sector here. With the cut of the dividend, Castellum now has the admirable ability to focus the entire might of its income on the repayment of bonds, completion of bonds, and improvements of its fundamentals. The company has one of the highest-quality selections of tenants that exist in Sweden, many of which are public.

{kind=link}

And despite a volatile environment, the company has continued to manage positive quarterly net leasing trends and increases in rental incomes. Property values are down - but they were up at unsustainable levels anyway - so that shouldn't be a surprise to anyone.

How exactly has the removal of the dividend impacted the company's fundamentals?

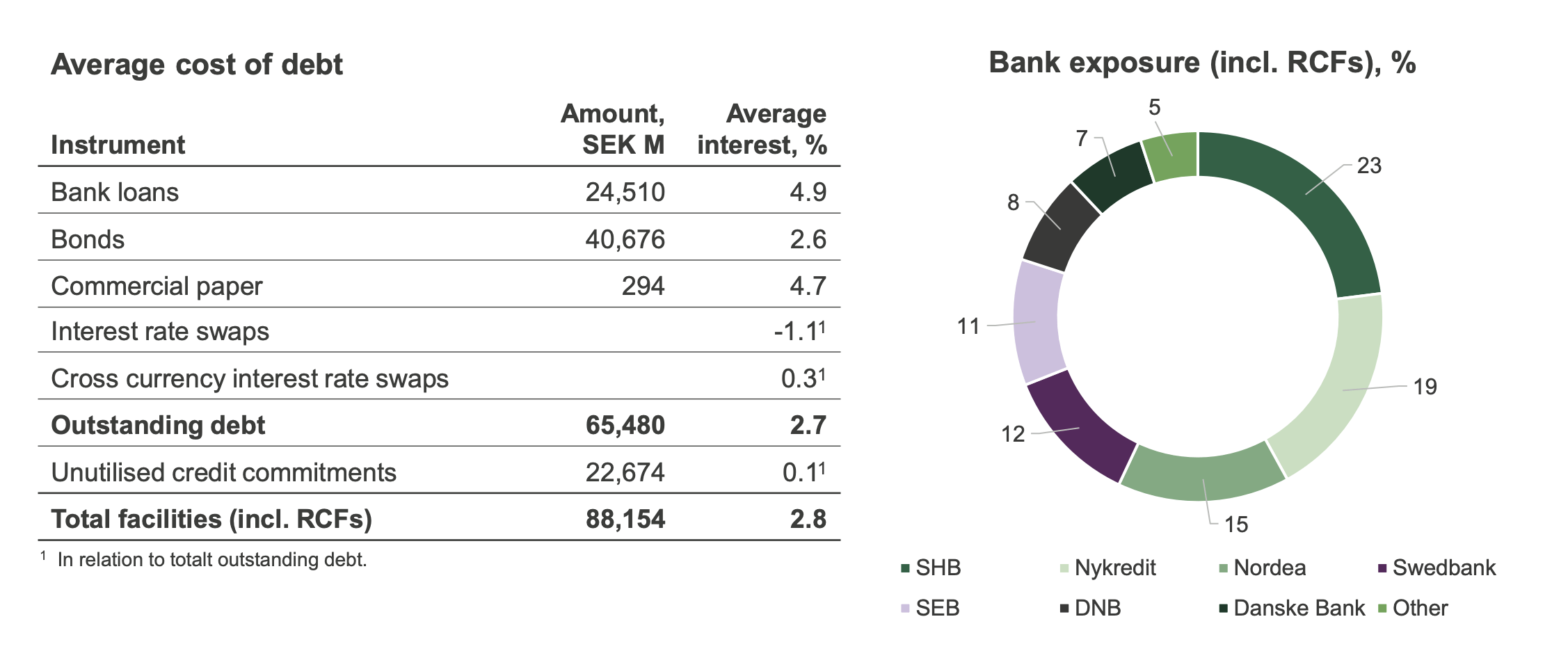

By a significant amount. The company now works with an LTV of 36.9%, which given that I see this company as a REIT is superb. The effective interest rate is 2.7% - compared that to any international RE player. Credit outlook is stable with Baa3, 71% of debt is now hedged, and the company's average maturity is 3.2 years, which given the current interest rate environment, is exactly what you want to see. The company has one of the lowest costs of debt compared to any real estate company in Europe and the world.

{kind=link}

'It's not as great as it once was. Remember, the company was at one point below 1.6%. But it's still extremely solid for the current environment.

The company works with multiple ESG levers to achieve higher sustainability. As you know from my previous work, this is only of very limited interest to me. Castellum installs solar, improves energy efficiency, and has a continued 2030 target of zero-fossil fuel energy.

Risks for the company? They're primarily macro and interest-rate driven. Sweden is paying the piper for a decade of extremely low interest rates, which has skewed the entire real estate sector towards ridiculous valuations and fundamentals - both on the corporate and on the private side. This will take years to correct - and plenty of pain on the interest rate side. The common belief is a reversal in the rate policy next year. I disagree with that. KPI in Sweden is still over 6%, compared to a target of 2%. Rates not only need to stay high for a long time - 2025-2026 as I see it - they need to go higher. That's why the key rate is expected to rise to 4% in a matter of a few weeks.

An already high level of leverage in market participants coupled with the resulting demand for high yield results in a very anemic/sluggish transactional market, with many of the objects available actually at poorer quality. New construction has declined- it's not at a standstill, but it's not in a good place, and most market participants with capital are being extremely conservative as to how they are moving. Banks are increasingly tight with capital. Things are, as I see it, going to get worse before they get better.

For the market itself, the outlook I would argue is grim to at least slightly negative. For Castellum , the outlook is more positive. Thanks to arguably unnecessary but in the end attractive moves in terms of dividends, the company is now one of the most conservatively-leveraged companies in this sector in all of Sweden. This puts the company in a very good position in terms of upside when the reversal actually comes.

And, I'm fairly sure that the reversal is actually on its way if we look at a 2-3-year basis.

Let's make clear what this means on a 2-5-year basis in the form of potential RoR.

Plenty to like about Castellum in terms of valuation.

So, I sold Castellum at a significant profit a few years back. I've been "playing" with Castellum by selling conservative puts, preferably with strikes below 100 SEK, to make 8-17% annualized RoR. My current running CSP expires in 3 days on Friday, and it has a strike of 100. At the current valuation that means I'm over 14% inclusive of the premium of being assigned, and I'm happily making 13% on my buying power here on an annualized basis.

If you know at what price you're willing to buy a company and what the uspide is likely to be, there are very few limits to what you can achieve and what tools you can utilize to make good alpha on a company. My investment mistakes have always come from either not knowing what I would be willing to pay, or miscalculation of what I'd be willing to pay for a company. That's why this is my first focus, bar nothing.

Castellum is expected to see significant earnings and FFO decline this year. 20-30% at least - however, it's estimated to go up after this, as the impacts of the property sector start to wane.

At a conservative 15-16x P/FFO, which is below the 18x that the company typically trades at, the company has an upside of 13.6% per year - but this is without dividends. If we include even a 1-2% yield, this has the potential of being 15% per year even just on a PT of 140-150 SEK/share, which the company most assuredly is worth.

S&P Global, compared to valuing this company at over 220-265 SEK less than a year ago (Source: S&P Global), which I believe shows their ability to accurately value a business such as this, is now at a range of 89-160 SEK with an average of 120 SEK. I maintain my previously-communicated PT of 140-150 SEK, which is also coincidentally where I would estimate the company at for the long term. 7 out of 10 analysts are at a "BUY" here, and I'm one of them - but my target is above that of the average for those reasons.

For the time being, however, I'm comfortable playing the volatility with options as opposed to putting massive amounts of capital to work directly.

Thesis

- I sold Castellum at a significant profit, and I am very happy that I did so. It was perhaps the best example of me following my "SELL"/Trim rules when a stock becomes overvalued. The capital I reinvested from Castellum has stayed relatively stable and has not declined over 45% since. The company remains a business with a solid asset portfolio but has taken damage from the management/trust perspective, and I am unwilling to move any closer here with my capital until I see some signs of things calming down.

- My current approach involves writing medium-dated CSPs with strikes at least 15-20% below the current share price, and I have done so successfully for 3-4 months at this point without a single assignment. Even if one had been assigned, I would have been able to sell it at a profit at the current price.

- For the time being, due to the trouble in the company, I'm bullish on the company, but I believe put options are the way to go here if the price is above 120 SEK. The common shares do come at a PT of 140-150 SEK/share long-term, but there's plenty that could happen until then. I do not see the upside to buying the common shares yet.

- At a near-double-digit share price though, in addition to my conservative CSPs, I'm starting to "BUY" common shares. Why? Because at 100 SEK/share, the company is being valued at less than 0.4x to its earlier NAV, which is insane.

- I'm maintaining "BUY" here in my thesis.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I now view the company as a "BUY" due to massive undervaluation, despite what's going on in the property market.

For further details see:

Castellum: The Upside Is Significant In Case Of A Fair-Value Reversal