EIC - CCIF: Creating A Successful New CEF From A Troubled Old One

2023-12-11 22:24:36 ET

Summary

- Carlyle Credit Income Fund is a new closed-end fund that offers high-yield income from collateralized loan obligations.

- CCIF was created by Carlyle Group by acquiring an existing CEF managed by a small fund manager.

- The fund holds mostly CLO equity and offers a consistent 15% distribution to shareholders, with the potential for continued high-yield returns.

If you follow trends and opportunities for income-oriented investments, you have likely come across some CEFs. There are several advantages to closed-end funds that are enticing for those who enjoy the high yield income that many CEFs can offer in part due to their common use of leverage, along with discounts or premiums to NAV to help with trading decisions. The discounts available on some CEFs can help to mitigate the risk and improve long-term returns.

I have written previously about several CEFs that offer high yield income with potential for strong total returns, including the most recent batch of a dozen CEFs that were launched in 2021. The timing of those funds going public was not ideal as I explain here .

And the market for new publicly listed CEFs has dried up in 2023. No new CEFs have gone public since October 2022. Instead, actively managed ETFs are all the rage with fund managers lately as I learned when I attended a recent virtual conference on CEFs and ETFs, My Takeaways From The 22nd Annual Capital Link CEF/ETF Forum.

So, what if you did want to create a new CEF that offers high yield income from a relatively low risk-adjusted asset class such as CLOs ? You can do what Carlyle did recently and buy an existing CEF managed by a small fund manager who was looking to liquidate its poor performing fund. That is exactly what they did to create the Carlyle Credit Income Fund (CCIF). From the fund's latest annual report , dated September 30, 2023, here is a brief description of the transaction:

On July 17, 2023 Vertical Capital Income Fund ("VCIF") announced that it changed its name from VCIF to Carlyle Credit Income Fund ("CCIF") in connection with the transaction pursuant to which Carlyle Global Credit Investment Management L.L.C. became the investment adviser to the Fund. In connection with the transaction, the Fund's investment mandate changed to focus on investing in equity and debt tranches of collateralized loan obligations ("CLOs") to drive potential shareholder value.

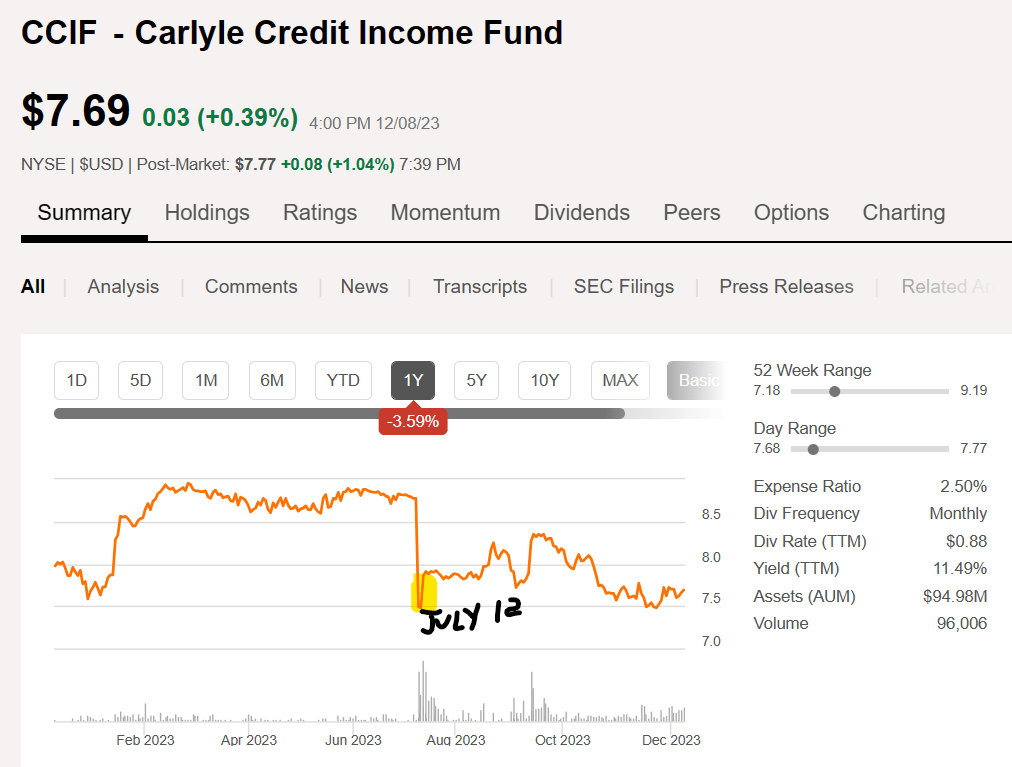

The former fund that had ticker VCIF, the Vertical Capital Income fund, was struggling to cover its distribution and maintain its NAV from holding mortgage loans. Shareholders of the former VCIF were caught by surprise when Carlyle announced the changes in July. Looking at the chart of CCIF it is quite apparent when the news hit and the effect that it had on the fund's share price.

{kind=link}

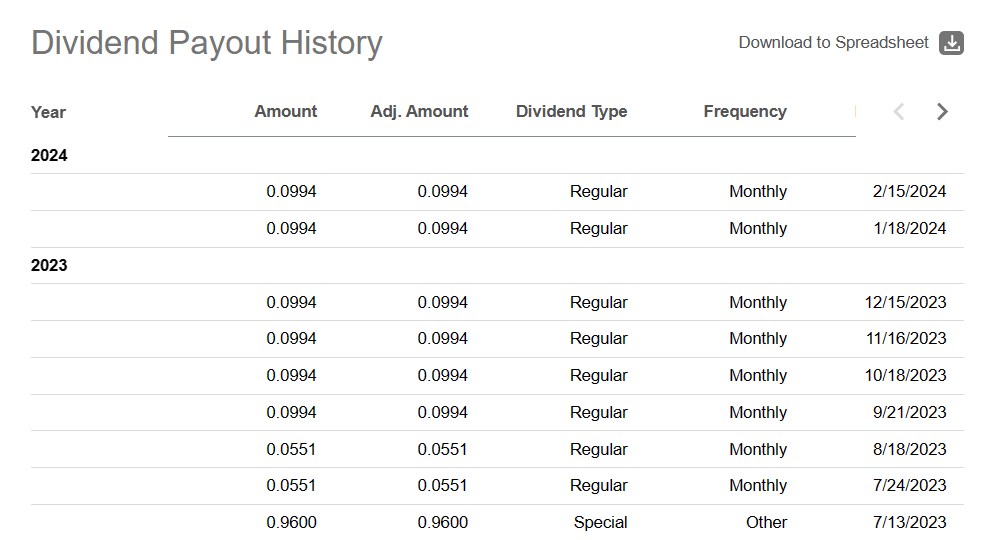

From my perspective, I consider the start of the CCIF fund as the beginning of a whole new CEF and therefore the history prior to July 12 is irrelevant to me. I started buying shares of CCIF for my Income Compounder portfolio in September, shortly after they announced the substantially increased monthly distribution of $0.0994 per share. That yield amounts to 14% annually based on the NAV of $8.27 as of August 31. However, being a CEF the fund trades at a discount to NAV. The market price as of the close on 12/8/23 was $7.69 so the current monthly distribution amounts to a yield of 15.5% at market price.

In addition, the NAV improved to $8.42 as of September 30, and then back down to $8.20 as of 10/31. The fund is currently trading at about a -5% discount to NAV as I write this.

Current Fund Holdings

The annual report includes some very useful information that is relevant to the current CLO-based fund and describes how the transition from VCIF to CCIF was completed as of September 12.

The transition plan included the following steps:

- Carlyle completed the $10 million one-time payment to the fund's shareholders of record on July 14, 2023

- Carlyle completed the tender offer to purchase $25 million of CCIF shares on August 28, 2023

- Carlyle made an additional $15 million investment in CCIF in newly issued shares and a private share purchase

- Carlyle successfully deployed the available initial cash proceeds for investments received from the portfolio sale announced on July 11, 2023 into a diverse pool of CLOs

- Carlyle declared a monthly dividend of $0.0994 for September, October, and November 2023, equating to 14.0% annualized dividend based on net asset value ("NAV") as of August 31, 2023, higher than the 12.0% target dividend yield previously disclosed to investors

Also, according to the annual report as of 9/30/23:

The current portfolio consists of 24 unique CLO investments managed by 19 different collateral managers with exposure to 2,053 separate loans. The weighted average effective yield of the portfolio is 18.16%.

In order to achieve the fund's leverage goals, an initial offering of preferred shares was issued on October 18, 2023. The fund issued 1.2 million 8.75% Series A Preferred Shares due 2028 (CCIA) at a public offering of $25 per share, raising $28.8 million in net proceeds. With two additional subsequent share issuances, the preferred shares now provide about $52 million in total leveraged assets to support further NAV expansion. The CCIA shares are rated BBB+ by Egan Jones rating company and offer risk-sensitive investors a compelling 8.7% yield at much lower risk than the common shares of CCIF.

CLO Market Review

The current market environment favors CLO investments due to the consistent high yield risk-adjusted returns provided by the underlying loans. In fact, several new CLO ETFs have been introduced recently as fund managers recognize the growing interest in CLOs from retail investors who are seeking consistent high yield income with relatively low risk. There are also a few relatively new CEFs that specialize in CLOs including Eagle Point Income (EIC), launched in 2019 that holds mostly CLO debt, and OFS Credit Company ( OCCI ) went public in 2018 and recently updated its distribution policy, but no new CLO CEFs have been launched since 2019 - until now.

In this recent CLO market update from VanEck , CLOs have been strong performers over the past six months and are likely to continue to deliver strong returns heading into 2024.

CLOs generated positive total returns across the capital stack in September, the sixth straight month of positive returns, with returns primarily driven by positive carry. The technical backdrop remained supportive as the strong levels of new issuance and a return of refinance and reset transactions.

Carlyle is the world's largest manager of CLOs with about $50B in CLO assets globally (just ahead of Blackstone), so they have their finger on the pulse of the CLO market. The loan market continues to be resilient, and defaults remain at historic low levels. The timing of starting a new CLO fund in the summer of 2023 appears to be working well:

During the quarter, the LSTA U.S. Leveraged Loan Index (the "Index") rose above $95 for the first time since August 2022, rising 1.27 points to end the quarter at $95.56. Leveraged Loans have returned 10.16% year-to-date through 9/30, the highest since the financial crisis.

In the third quarter of 2023, new loan issuance totaled $76.3 billion, the highest level since the Federal Reserve began tightening monetary policy in the first quarter of 2022. The LTM default rate of the Index has decreased to 1.27% from 1.71% for the second quarter of 2023. This compares to the historical average of 2.17% since 2003. Finally, the underlying companies in U.S. Carlyle managed CLOs, which totals approximately 600 companies, have experienced high single digit EBITDA growth in the third quarter of 2023.

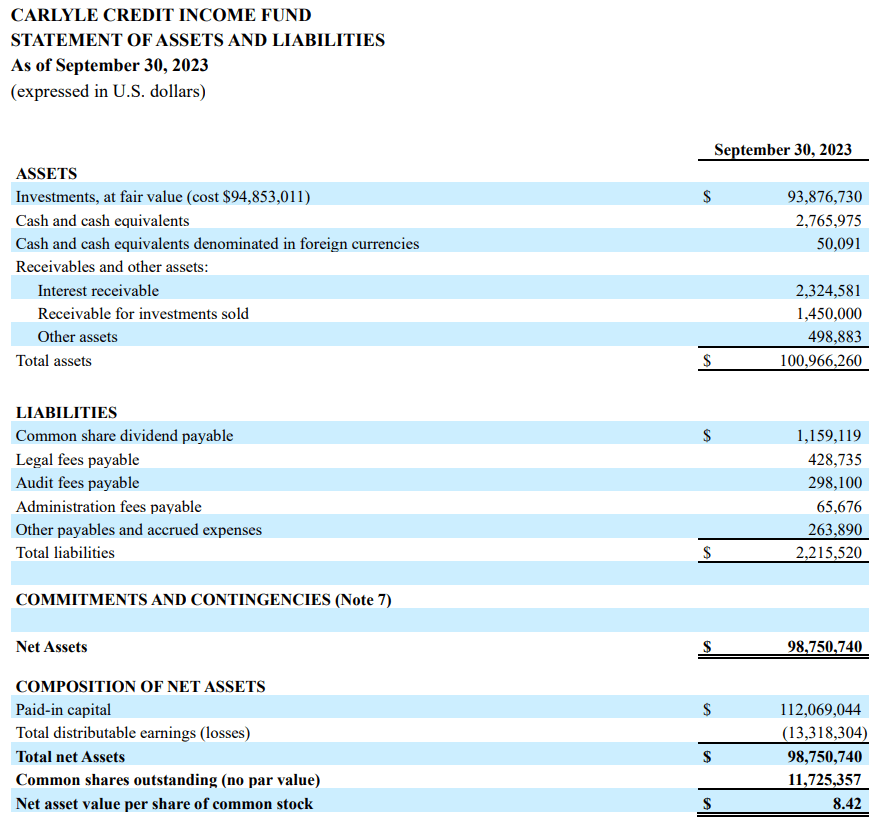

As of September 30, the fund had about $94 million in net investments at fair value and $101 million in total investments with total liabilities of just $2.2M leaving about $98M in net assets.

{kind=link}

Compared to Eagle Point Credit Company ( ECC ) with about $550M in AUM and Oxford Lane Capital ( OXLC ) with nearly $1B in AUM, CCIF is still a relatively small CLO fund. However, the fund is off to a good start and will likely find ways to grow the net assets by leveraging its global CLO exposure.

According to Fitch Ratings as of November 21, 2023, new US broadly syndicated CLO activity improved in Q323. Fifty-one new US CLOs priced at $22B in notes and equity were issued, up from 40 CLOs priced at $17B in Q2 and compared to 68 new CLO issues priced at $30B in Q322.

CCIF holds mostly CLO equity (about 96% as of 9/30/23) and a small amount of CLO debt. The equity tranches of CLOs offer the highest yields and in 2023 those yields are better than they have been in years. This aspect of the fund's CLO holdings is described in detail in the summary section of the annual report where they explain how the equity tranches currently return 17% on an annual basis at par; however, the CCIF equity tranches were mostly purchased on the secondary market at reduced prices, so the effective yield is even higher.

Quarterly payments to the equity tranche averaged 4.20% in the third quarter of 2023, in line with 4.18% for the second quarter of 2023. We believe fourth quarter 2023 payments may be similar. The second and third quarter 2023 equity distributions are the highest we have seen since 2016. The 4.20% average equity payment in the second quarter of 2023 represents payment on par and equates to approximately 17% on an annualized basis. We expect CCIF's quarterly cash-on-cash to be closer to mid-twenties given that we purchased CLO equity investments in the secondary market at discounted prices.

These high yielding equity payments enable the fund to offer a consistent 15% distribution to shareholders without returning investor capital or negatively impacting the fund's NAV.

Dividend Reinvestment Plan

For those investors who are willing and able to reinvest the monthly distributions back into more shares of CCIF, there is an additional advantage that is spelled out in the Annual Report under the description of the DRP.

When the Fund declares a dividend, capital gain or other distribution (each, a "Distribution" and collectively, "Distributions") Equiniti, on the Shareholder's behalf, will receive additional authorized shares from the Fund either newly issued or repurchased from Shareholders by the Fund and held as treasury stock. Distributions that are reinvested through the issuance of new shares increase our Shareholders' equity on which a management fee is payable to the Adviser. The number of shares to be received when Distributions are reinvested will be determined by dividing the amount of the Distribution by 95% of the market price per share of the Fund's common stock at the close of regular trading on the NYSE. The newly issued shares would be issued whether our shares are trading at a premium or discount to NAV.

This is an advantage that is also offered by some other CLO CEFs including OXLC and ECC, which typically trade at a premium to NAV. While CCIF currently trades at a discount to NAV, the policy still offers investors the ability to grow their share count at a discounted price offering an even better total return.

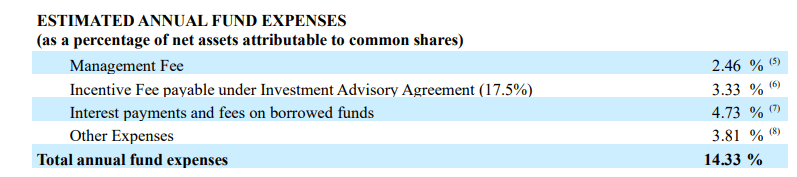

Fund expenses are consistent with or slightly higher than peer CLO equity funds such as OXLC and ECC. For comparison, OXLC has a 3.15% management fee, 3.91% interest expense, and 6% other fees for a total of 13.14%. ECC shows total estimated annual expenses of about 10%. Keep in mind that these expenses are just the cost of doing business and do not affect the distribution yield.

{kind=link}

Risks and Summary

As with any investment in CLOs, the biggest risk to investors is that the default rate on the underlying loans could rise resulting in a loss of NII. The fund NAV will also likely experience volatility due to market pricing of CLOs as secondary market pricing rises or falls. Therefore, unlike equity-based or more traditional fixed-income CEFs where the NAV is more predictable, the NAV of CCIF may not be a good indicator of how healthy the fund is at the time. A more useful indicator may be to consider what the CLO spreads are doing. This discussion from the annual report explains why Q3 2023 was a good time for the fund to load up on new CLO issues, or CLOs purchased at a discount in the secondary market.

The third quarter of 2023 generally experienced a risk-on tone in the U.S. CLO market, although it experienced some softening towards the end of September. Spreads tightened in July as payroll data fell below expectations and the consumer price index figures pointed to further deceleration in prices. CLO spreads tightened with the rally persisting into August, albeit at a more moderate pace. The first half of September remained relatively calm; however, heightened concerns over potential rate increases, a persistently strong labor market, and a lower likelihood of a Federal Reserve rate pivot in the near term resulted in an increase in volatility and a softening of spreads in the month's second half.

I believe that CCIF is now well-positioned to leverage the growing CLO equity position that it established over the summer of 2023 to deliver consistent, high yield returns to investors over the coming years.

{kind=link}

It is important when evaluating CCIF to consider only the distributions that have been announced or paid since September because any prior history was a different fund (VCIF) that did not have the benefit of CLO equity investments. It is still early in the fund's history but with now six months of dividends declared at $0.0994 through February 2024, I believe that CCIF is well positioned to deliver consistent high yield income from its CLO equity investments for many years to come and stacks up nicely against peers such as ECC and OXLC.

For further details see:

CCIF: Creating A Successful New CEF From A Troubled Old One