SLRC - Cedar Creek Partners - Propel Media: Amazing Opportunity In The Expert Market

2023-07-28 05:20:00 ET

Summary

- Cedar Creek Capital Management took advantage of an opportunity in the expert market by purchasing shares of Propel Media at a low price.

- Propel Media may potentially be acquired by IQVIA Holdings for a reported price of $700 to $800 million, which could result in a significant gain for Cedar Creek.

- The court ruling on the acquisition and the outcome of the FTC's lawsuit will determine the final result for Cedar Creek's investment in Propel Media.

The following segment was excerpted from this fund letter.

Expert Market Exposure

Our exposure to stocks trading in the expert market increased significantly in the quarter, due to purchases noted above in PD-Rx and First IC, and due to the purchase of Propel Media (PROM) profiled below. Expert market stocks are companies impacted by SEC Rule 15c2-11. For those unfamiliar, the rule prevents brokers from not only displaying quotes for non-reporting companies but also restricts transactions to selling only. Institutional accounts, depending on the broker, are not subject to the buying restriction. We started the quarter with 27% exposure and ended at 37% of the fund.

Three positions make up about 65% of the expert market exposure - PD-Rx Pharmaceuticals (PDRX), which is about 12% of the fund, Pacific Coast Oil Trust (ROYTL), which is roughly 6.5% of the fund, and Propel Media (PROM) is about 5.5%. We discussed PD-Rx Pharmaceuticals briefly in our Q1 2021 letter and Pacific Coast Oil Trust in our Q2 2022 letter. We also provided more detail on both in our 2022 year end letter .

Amazing Opportunity in the Expert Market We Have Waited For

While we thought it was a stupid decision by the SEC and harmful to retail investors, our hope was that the expert market would create occasional opportunities to put capital to work at incredibly attractive prices. For the first year we were able to build positions in PD-Rx and Pacific Coast Oil Trust ( ROYTL ) which could be worth five times its current price if, as we believe, the improper assessment of asset retirement obligations to the trust is reversed by the courts. While both of those opportunities are very attractive, we had yet to come across the opportunity we were hoping for. That changed in the quarter.

Propel Media ( PROM ) - trades on the expert market. We briefly covered it in our 2020 first quarter letter . At the time it had 246 million shares outstanding. It traded around $0.13 per share and earnings in 2018 were $23 million, or $0.09 per share. Earnings were being used to pay down debt.

We sold the entire position at up to $0.29 in the second quarter of 2021 and explained our reasoning - we had achieved a decent gain and the business was declining - earnings had fallen to $0.04 per share in 2019 and the outlook was not positive.

We felt fine about our decision as the stock rarely traded after the implementation of Rule 15c2- 11 forced it onto the expert market. In fact, between January 1, 2022 through April 30, 2023, it appears only about 20,000 shares traded. Most at $0.10 per share, which the fund actually bought, and about 1,000 shares at $0.01 and an even smaller amount at $0.0001. The only information we had received was in April 2022 when Propel communicated their decision to sell what had been their primary business for a $24 million note receivable, plus potential earnouts, in order to focus on their healthcare advertising business, DeepIntent.

Apparently, we never updated our Google alerts because, on May 13 of this year, we received an alert about IQVIA Holdings ( IQV ) acquisition of Propel Media potentially being blocked by the FTC . This was the first report that there even was a potential acquisition of Propel. What got our attention (massive understatement) was the reported price in the article of $700 to $800 million. Assuming no change in the outstanding shares that would be equal to $2.77 to $3.17 per share. Wow! A $0.10 stock possibly being worth $3 per share. We confirmed the share count at otcmarkets.com was essentially unchanged at just over 252 million. We, unfortunately, had no way to confirm the potential purchase price - we had to trust that the journalist actually had multiple sources and got it right.

Would the stock price of an expert market illiquid security react to a Politico article noting a possible merger? If so, how long would it take? The price of a listed stock typically reacts within minutes or even seconds. An unlisted stock can take hours or occasionally a few days, but volume is usually only enough for a small investor to make a decent gain. Interestingly, the article did not contain ticker links so it did not show up on financial news platforms for IQVIA or Propel. As we write this neither company has mentioned the possible acquisition.

More importantly, could we get shares in an illiquid, expert market security with public news of it possibly being acquired? It was a long shot but worth trying. We already had in place a 100,000 share "stink bid" at $0.01 per share for a while with no hits. Our broker said there were 5,000 shares available at $0.10 per share. While hardly meaningful we took them. Another 5,000 shares came on the market and we bought those too. Combined that was $1,000 plus commissions. Certainly not meaningful. We ended the day buying 20,000 shares at $0.10 per share. We raised our bid to $0.15 per share, which was the high bid, and waited. And waited. And waited. There were no sellers at all. Nearly a month goes by with nothing happening. On June 14 a small seller of 23,000 shares shows up at $0.30. We didn't want to cause a big price jump, but we decided to take them and keep our bid at $0.15. While we were making some progress, it was still not meaningful in relation to the fund's size. Then my broker called to say another seller showed up with 2,500 shares at $0.35 and he thinks there may be some size behind it, meaning the seller likely wants to sell more shares than what was being displayed.

The broker engaged in negotiations with the selling broker and near the end of the trading day the fund purchased just over 300,000 shares at $0.25 per share. At cost, the $75,000 was still not significant, but if Propel were to be bought for $3 per share it would be nearly a $1 million gain. That is meaningful for Cedar Creek. The next day, June 15, we put out a bid for 200,000 shares at $0.25 to see if the seller was still there, with instructions to buy up to one million shares. Crickets. Bummer. A few hours later my broker emails me that he had negotiated a purchase of one million shares at $0.24. Now we are talking. We added another 750,000 later in the day. At day end, we owned over 2.1 million shares at a cost basis of roughly $0.25 per share. We added another 98,000 shares on June 16. We continued our due diligence (see below) and purchased another million shares the following week. That made it our 6th largest position at around 5% of the fund. We must have exhausted the seller because the ask jumped to near $1 and less than 1,000 shares have traded in nearly a month.

If the acquisition is consummated at the current terms, of roughly $3 per share, we would have a return of 12 times our cost basis, which works out to roughly a 50% gain for the fund as a whole, net of fees. We had no idea what will happen. We expected both the seller and buyer to work diligently at alleviating any concerns the FTC had. On July 17, the FTC announced that they were suing to block the transaction . While approval would have been ideal, the FTC filing suit does not kill the deal. The FTC had done the same thing, with similar reasoning in the Microsoft ( MSFT )/Activision Blizzard ( ATVI ) transaction and the courts sided against the FTC. A court date for the IQVIA/Propel Media matter was set for December 2023.

Possible outcomes are:

- The court rules in favor of IQVIA and Propel and the deal goes through!!!

- The court rules in favor of the FTC and blocks the deal. That means Propel has to be valued on its own merits and maximum value is the price of the next best acquirer, which would most likely be below $700 to $800 million. For us to lose money, the value as a going concern or what the next strategic buyer would be willing to pay would have to be less than 1/10 of what IQVIA is willing to pay. That seems highly unlikely. We also think it is reasonable to conclude that it is more likely than not that Propel is profitable, or about to turn the corner on profitability. Why else would IQVIA pay $700 to $800 million?

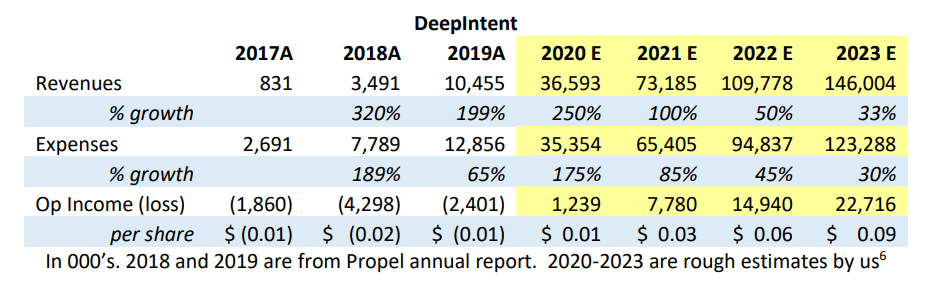

We had Propel's 2018 and 2019 annual reports which thankfully broke out the revenue of the healthcare advertising business, DeepIntent, at $3.5 million and $10.5 million, respectively. It also noted an operating loss for DeepIntent of $4.3 million for 2018 and $2.4 million for 2019. Revenue grew significantly faster than costs in both 2018 and 2019.

We combed through DeepIntent press releases and other news articles on the company, and found the following interesting data points:

- DeepIntent press release announced that revenue had increased by 300% or more for four consecutive years between 2017 and 2020 . Apparently, someone at DeepIntent is not very good at math - 2019 revenue was $10.5 million versus $3.5 million in 2018, a 200% increase, not 300%. Revenues tripling is 200% growth, not 300%. The article noted that 2020 also had 300% growth, so we know it was greater than 200%, which would put 2020 revenue between $31 to $42 million (we split the difference in our estimate below).

- We found a release that noted that DeepIntent had more than doubled in revenue annually from 2016 to 2021. For 2021, we are comfortable projecting a doubling of 2020 revenue to a range of $61 to $84 million.

- We could not find specific revenue growth for 2022. DeepIntent said in a release that they grew revenues in both 2021 and 2022 and that 2022 had robust year-over-year growth. We would not define growth of under 25% as robust, so we assumed 50% growth in 2022.

- A number of reports on employee growth line up with our revenue projections. For example, we read that employee growth doubled in 2020 and was planned to double again in 2021.

- We also found that SLR Investment Corp ( SLRC ) granted an ABL facility to DeepIntent, which had $16.9 million drawn at yearend out of $20 million of borrowing capacity (p. 7 and 30 of SLR's 3/31/23 10-Q). Most lenders limit borrowing capacity to 85% to 90% of receivables. That level of accounts receivable would exceed our revenue estimates assuming 60-day average receivables (60 days of receivables would equal roughly 1/6 of annual revenue, thus 20 million divided by 90% capacity times 6 = 133 million of annual revenue).

{kind=link}

Our conclusion was that even if the deal does not close, we are gaining ownership in a fast-growing company at a very attractive price. At $0.24 per share, the market cap is $60 million, which is not only less than 10% of what IQVIA is willing to pay, it is less than half our estimate of current revenue, and possibly two to three times earnings.

Update

On July 19, 2023, the Wall Street Journal had an interesting article (paywall) on the changes in how the FTC was viewing acquisitions. It focused on the FTC's adoption of new guidelines and how it viewed vertical mergers, in particular. The FTC was saying they were just codifying current law in their guidelines, while others argued the FTC was putting forth guidelines that have not been successful in courts lately.

Time will tell if we truly found that amazing opportunity in the expert market or not, but so far, the signs are very positive.

| DISCLAIMERS Fund Performance The financial performance figures for 2022 and 2023 presented in this report are un-audited estimates based on the best information available at the time of the letter and are subject to subsequent revision by the Fund's auditors. Past performance may not be indicative of future results and no representation is made that an investor will or is likely to achieve results similar to those shown. All investments involve risk including the loss of principal. Net Return reflects the experience of an investor who came into the Fund on inception and did not add to or withdraw from the Fund through the end of the most recently reported period. The reported net return figures will therefore include the impact of high water marks in the cumulative return. Individual investor returns will vary depending upon the timing of their investment, the effects of additions and withdrawals from their capital account, and each individual's high water mark figure, if any. Index Returns The S&P500 Index returns are reported using the S&P500 Depository Receipt Trust (SPDR) which trades under the ticker symbol SPY. Reinvested dividends are included in these figures. A spreadsheet showing the SPY performance versus the fund since inception is available upon request. Nasdaq performance excludes dividends, which historically have been immaterial to the total return of that index. In recent years more technology stocks have begun paying dividends thus the inclusion of dividends would increase the reported figures. Russell 2000 performance is from data reported on Russell's website, and includes reinvested dividends. DJIA returns are reported using the SPDR Dow Jones Industrial Average which trades under the ticker symbol DIA. Reinvested dividends are included in these figures. A spreadsheet showing the DIA performance versus the fund since inception is available upon request. While reported returns for SPY and DIA will likely be a few tenths of a percentage lower than the representative index annually, we believe they are a better reflection of what a non-institutional investor would earn following a passive investment approach. Index returns are provided as a convenience to the reader only. The Fund's returns are likely to differ substantially from that of any index, and there can be no assurance that the Fund will achieve results that are superior to such indices. Share Prices Share price figures for listed stocks are from Yahoo! Finance and unless specified otherwise are the closing price as of the previous month end. Share price figures for unlisted stocks are closing bid prices as reported on otcmarkets.com, except for unlisted stocks classified as expert market, which do not have public availability of quotes, and are marked to last sale. Forward Looking Statements This letter and the accompanying discussion include forward-looking statements. All statements that are not historical facts are forward-looking statements, including any statements that relate to future market conditions, results, operations, strategies or other future conditions or developments and any statements regarding objectives, opportunities, positioning or prospects. Forward-looking statements are necessarily based upon speculation, expectations, estimates and assumptions that are inherently unreliable and subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements are not a promise or guaranty about future events. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Cedar Creek Partners - Propel Media: Amazing Opportunity In The Expert Market