PAXS - CEF Report August 2023: Taxables Get Bought And Are Not Very Compelling Munis Look Best

2023-09-01 15:47:25 ET

Summary

- Taxable closed-end fund discounts have narrowed, reducing their attractiveness, while credit spreads have tightened, producing returns in some areas of the CEF market.

- Municipal CEFs remain exceptionally cheap, with discounts wider than 99% of historical observations.

- The risk-reward in the taxable bond CEF space is on the downside, while the upside potential in municipal CEFs is significant, but dependent on a shift in Fed policy and inflation.

- Lots of swap opportunities exist. You have to assess the kind of investor you want to be.

Discounts have narrowed markedly over the course of the summer in taxable closed-end funds, or CEFs, and are now not all that attractive. With a narrative shift towards a no-landing scenario, credit spreads have tightened and discounts have closed producing nice returns in some areas of the CEF market. However, much of the upside has not been reaped and the risk-reward is firmly on the downside.

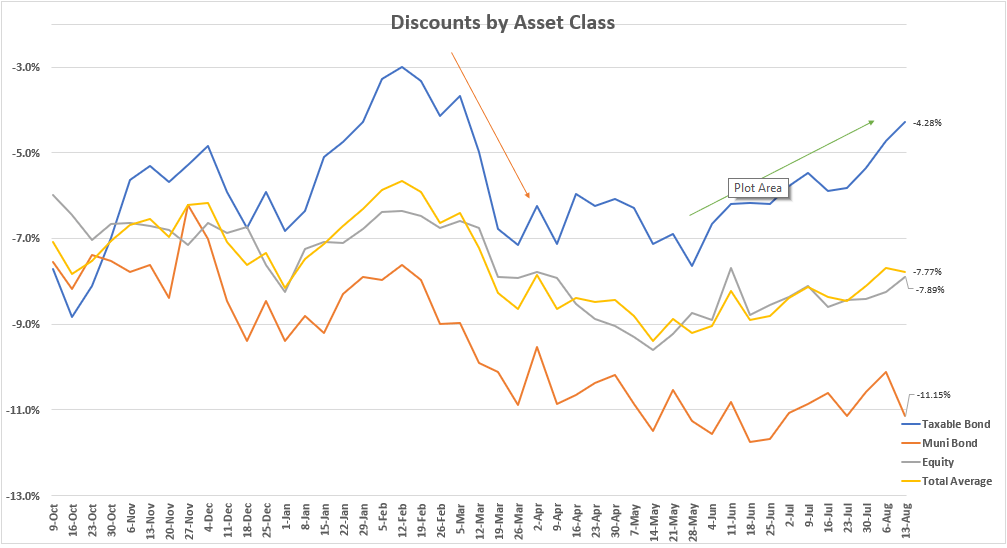

The chart below shows the discounts of the three main asset classes: taxable bonds, municipal bonds, and equity CEFs.

{kind=link}

From late 2022 through 2023, taxable bond CEFs have had two distinct cycles of rallies and declines. Taxable bond CEFs rallied in the fourth quarter of last year and for the first two months of 2023. They began to roll over in late February when it appeared the economic slowdown predicted was not going to materialize any time soon.

Discounts widened out by about 4 percentage points, aided by the fall of Silicon Valley Bank. They bottomed at the end of May.

Since Memorial Day, taxable bond CEFs have been in rally mode closing in an almost linear fashion. They rallied from -7.6% to the current -4.3%. The average discount is still about 1.3 percentage points away from where they were in early February.

Discounts are now in the 68th percentile (meaning discounts have been tighter 68% of the time going back to 1996). That is close to fair value for the space.

Muni CEFs remain exceptionally cheap. We discussed muni CEFs in our monthly letter for August outlining the opportunity they contain today. That opportunity is difficult to express in a time frame but not in a performance return as discounts, higher NAVs, and distribution raises lay ahead. The big question is when?

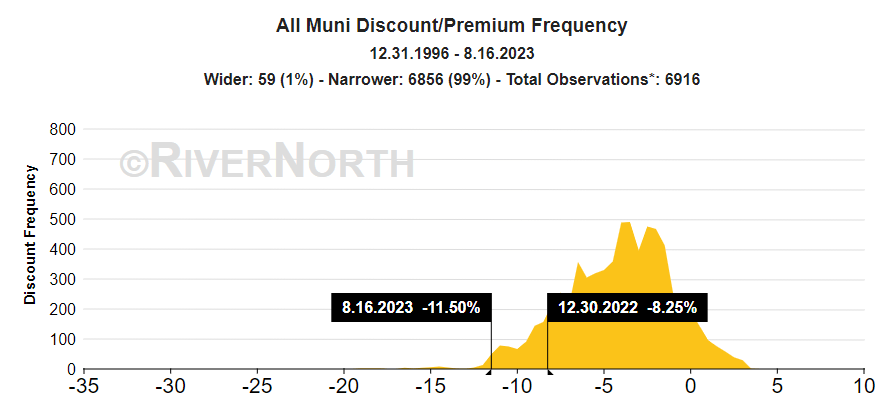

Just how cheap are muni CEFs? In the 6,916 daily discount observations recorded since 1996, the average muni CEF discount has only been wider on 59 occasions. That is less than 1% of the time.

{kind=link}

The split makes sense. Taxable bond CEFs are largely credit vehicles and will trade based on fears of default/economic slowdown/exogenous shocks. These are the events that lead to credit spreads widening out.

Muni CEFs have very little risk of default. They are long-duration assets of high quality (investment grade). The risks here are interest rate sensitivity or the fear of interest rates rising.

In the last several months, it has been the latter that retail investors have been scared of, not of the economy falling into an economic recession.

Buy-and-Hold vs. Tactical Counter-Cyclical Investing

This topic has come up several times over the last few years in our service and in others on Seeking Alpha. It does bring up some good points which I want to highlight, but primarily, my goal is to suggest that you can be both.

A lot of investors are buy-and-hold, which I think is a good strategy. So many retail investors feel the need "to do something" at times of increased volatility in the markets. That "need" is typically more psychological than anything else as they believe that the doing something is positive or additive to their portfolio.

At times, that doing something means adding when there is "blood on the streets," which can be a good thing. The old adage of "buy low, sell high" is that for a reason. Most investors tend to do the opposite out of fear and regret.

That is where buy-and-hold comes in. This strategy means you do not do anything during those periods of volatility. This helps prevent you from making mistakes and takes the emotional component out of the equation.

Is one the right way?

No. It really comes down to the individual and the investment strategy. So many of you are retirees living off of the income that your portfolio throw off. Everything you do is thought of in terms of yield, not total return or other factors. In fact, 100 years ago, wealth was primarily calculated based on your yield or total income from the portfolio, not the portfolio's market value itself. The thought being that a $5mm producing $100,000 per year in income and a $6mm portfolio producing $100,000 per year in income were worth the same.

I consider myself a hybrid of the two: what we've dubbed a "buy-and-rent" strategy. This is where you buy CEFs and reap the income benefits as well as rotate to take advantage of new discount opportunities.

CEFs pay out regular monthly (sometimes quarterly) cash distributions. There really is no other investment security that provides the steadiness of cash flows that a regular paycheck once provided.

Because of this many investors prefer to just hold and focus on the income. Of course, in CEFs, I tell investors to make sure the NAV is at least steady. Income comes from the NAV so if the NAV is in a permanent downtrend you know the distribution will eventually be cut.

In my CEF portfolios, I have positions that are effectively buy-and-hold (I consider any CEF that I've held more than a year a buy-and-hold investment) and some that are tactical 'trades.'

I hate using the term "trades" because it evokes the thought that I'm day trading or swapping every day. Doing some work on my trades and noting them (like a journal) I found that my average 'non-buy-and-hold' CEF position was held for approximately 6.5 months.

In the last 7.5 months (YTD), my average purchase was done at an average discount of 12.8% and my average sale was done at an average discount of -8.2%. In other words, in general, I recycled an -8.2% discount for a -12.8%. My guess is that if I continue to go back and look at prior years' trades, the same sort of thing would be found.

That is the essence of a counter-cyclical investment strategy in closed-end funds. You are recycling or swapping discounts that have closed and tightened below their long-term average for funds that have widened out and are beyond their long-term average.

Where Are Those Opportunities Today?

In preferreds:

I swapped long-time holdings Cohen & Steers Tax-adv Prd Sec and Inc ( PTA ) for Flaherty & Crumrine Total Return Fund ( FLC ).

- Sell PTA, -6.9% discount, 9.01% yield.

- Buy FLC, -12.55% discount, 7.55% yield.

I sold out of PIMCO High Income ( PHK ) (*a few weeks ago), for PIMCO Access Income ( PAXS ).

- Sell PHK, 12.05% premium, 11.68% yield.

- Buy PAXS, -2.7% discount, 12.53% yield.

For a family member, I sold BlackRock Floating Rate ( FRA ) and swapped into Nuveen Floating Rate Inc ( JFR ).

- Sell FRA, -6.32% discount, 11.41% yield.

- Buy JFR, -12.6% discount, 12.81% yield.

I sold Putnam Master Intermediate Income Trust ( PIM ) and moved into Eaton Vance Short Duration Diversified Income Fund ( EVG ) (*several weeks ago but still good).

- Sell PIM, -6.8% discount, 8.25% yield.

- Buy EVG, -7.2% discount, 9.11% yield.

For a member, I recommended they sell DoubleLine Income Solutions ( DSL ) and rotate into RiverNorth Opportunity ( OPP ).

- Sell DSL, 1.1% premium, 11.1% yield.

- Buy OPP, -11.25% discount, 14.80% yield.

For another member, I suggested they sell Western Asset Premier ( WEA ) and swap the capital into BlackRock Credit Allocation ( BTZ ).

- Sell WEA, -4.9% discount, 7.54% yield.

- Buy BTZ, -10.2% discount, 10.25% yield.

In munis, there are a few opportunities, but I always caution investors in munis to consider the tax consequence of the swap. If you have an unrealized gain (unlikely today) you are producing taxable income or long-term cap gains, and it may not be worth it.

- Sell MFS High Yield Muni ( CMU ), discount -9.1%, yield 4.01%.

- Sell Nuveen Muni Credit Opps ( NMCO ) , discount -1.6%, yield 5.32%.

- Sell Nuveen Dynamic Muni Opps ( NDMO ), -1.0% discount, yield 7.05%.

- Sell Nuveen Muni Income ( NMI ) , -3.1% discount, 4.03% yield.

- Sell Nuveen Select Tax-Free ( NXP ), 0.6% premium, 4.08% yield.

- Buy Nuveen Muni Credit Inc ( NZF ) , -14.9% discount, 4.59% yield.

- Buy PIMCO NY Muni Inc ( PNF ) , -6.9% discount, 5.01% yield.

- Buy Eaton Vance Muni Inc ( EVN ) , -11.9% discount, 4.64% yield.

- Buy Eaton Vance 2028 Term ( ETX ) , -8.4% discount, 4.07% yield.

- Buy DWS Strategic Muni Inc ( KSM ) , -14.3% discount, 4.32% yield.

Concluding Thoughts

CEFs today on the taxable side are pretty fairly valued but carry a skew to the downside in terms of overall risk. That is a combination of discount risk and spread risk (the risk that credit spreads widen out). Today, credit spreads are tight signaling an all-clear to investors that no recession (or perhaps even a soft landing) is imminent.

While we hope that is the case, we do not know for sure. That is the risk facing investors today in the taxable bond CEF space.

Muni CEFs remain exceptionally cheap. They are in the top 0.5% of the widest discounts of the last 27 years. The only times they were wider were on a few occasions in 2008, 2013, and 2018. It's a little odd that this is happening every five years.

But this time it lasts far longer. During those prior times, it was a few days of extreme volatility that created those data points. Today, the average discount is hanging around the widest levels ever and has been doing so for several months.

The muni CEF space will require not just lower volatility - like we have now - but also a macro environment change. That change will be a Fed pivot and the current quantitative tightening environment shifting to a neutral rate or even an easing environment.

However, the upside in muni CEFs today are massive. The question is not if, but when. When will the Fed shift their policy and rates subside. It will be dependent on inflation falling back to the Fed's long-term target.

-----------------

For further details see:

CEF Report August 2023: Taxables Get Bought And Are Not Very Compelling, Munis Look Best