PAXS - CEF Weekly Commentary | December 10 2023 | High Quality Opportunities

2023-12-15 13:00:00 ET

Summary

- Stocks were up slightly as the jobs report shifted the narrative towards 'higher for longer.'

- The payroll report came in stronger than expected, but the narrative was that it was a hawkish report, meaning higher rates for longer.

- Discounts for CEFs continue to tread water, with real estate and interest rate-sensitive bond sectors performing well, while emerging market equity and convertibles performed poorly.

- Some good opportunities in ETX and NMCO in munis, and Flah & Crum preferreds. Sell JLS, HIX, IGI, HYI, and DSU.

Macro Picture

Stocks were up slightly on the week, with small caps outperforming large caps as the jobs report shifted the narrative back slightly towards 'higher for longer.'

The payroll report came in a bit stronger than expected at 199K - though this was augmented by the UAW strike. Without them, it was just 118K. Health care made up 83% of the rest of the growth in jobs.

Still, the narrative was that it was a hawkish report, meaning higher rates for longer. Prior to the release, the Fed Funds futures showed the first cut in March but after its release, it moved to May 2024.

Permanent jobs losers is still growing sharply. That is normal ahead of a recession.

Longview

Overall, the narrative did shift a bit towards higher for longer, though I don't think the jobs report was all that bullish.

lplblog

CEF Market Commentary

{kind=link}

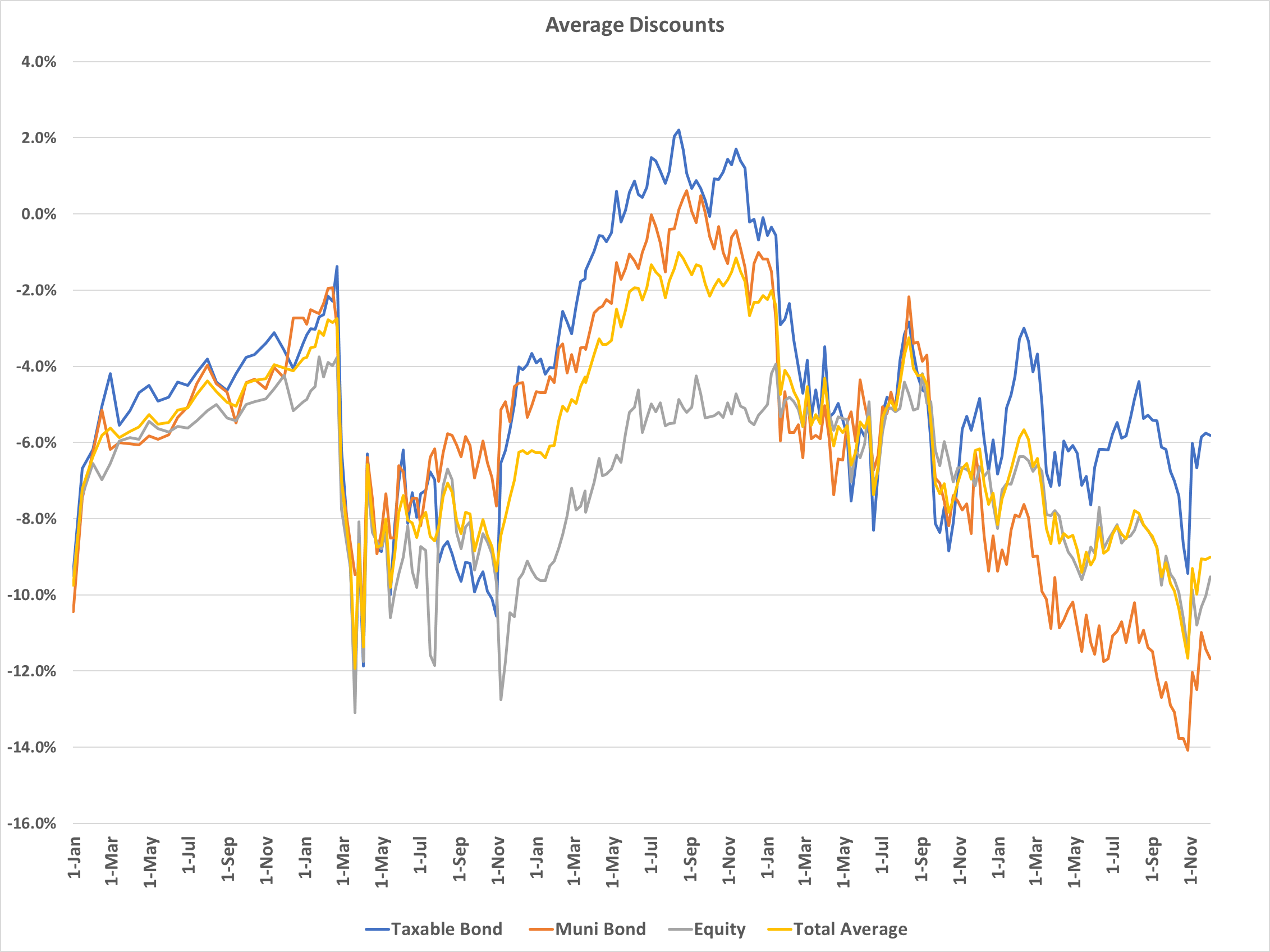

Discounts continue to tread water for the third straight week, with taxables hanging around the -5.8% level and munis still not all that far off their wides at -11.7% (widest levels were -12.5%).

Real estate and interest rate sensitive bond sectors were the best performers on the week, while emerging market equity and convertibles were the worst.

{kind=link}

Miuni CEF NAVs were up another 1.3% on the week, bringing their trailing month to +6.8%. Over the last 7 weeks now, muni CEF NAVs have recovered by more than 10%.

Real estate is the only sector that has done better. In the last month, Real Estate NAVs are up 10.3% and nearly 15% in the last 7 weeks since the narrative shift.

Preferreds got moderately cheaper on the week, leading all sectors on the week lower. Mortgages, Asian equities, and MLPs did the best as judged by the most amount of discount tightening.

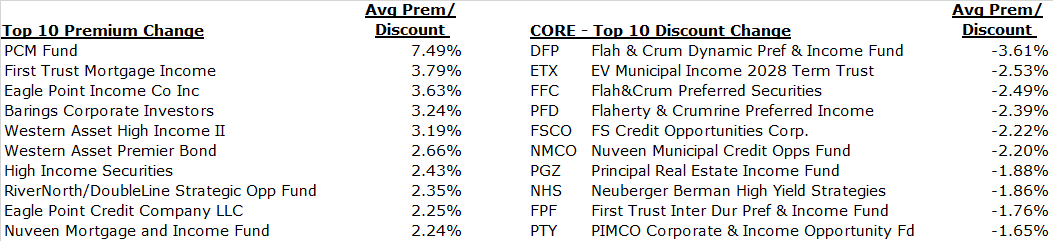

That is evidenced by the fact that the top 10 list of discount wideners has five preferred CEFs.

{kind=link}

There's a few great opportunities here for those who were waiting for better entry points. For one, starting with munis, there's

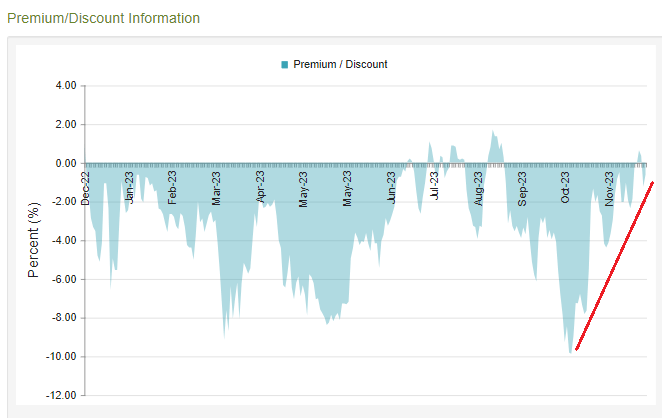

Eaton Vance Muni Inc Term 2028 ( ETX ) which saw its discount widen back out after rallying hard the last couple of weeks. The chart below shows the discount rally (in addition to the NAV/price rally) since the end of October. With the shares back to -8%, we are firmly in buy territory. The -8% discount will close over the next 5 years as the fund approaches its liquidation date in Dec 2028 (term fund structure). That means in addition to the 4% tax-free yield, there's an 8% discount captured for a 5.6% annualized IRR.

cefoconnect

Nuveen Municipal Credit Opps ( NMCO ) is another option in the muni space, as the discount has widened back out to -10.5%. The yield is now 5.4% tax-free, though the covered yield is about 4%. This fund was great a couple of years ago with the second-best 3-year return, but more recently has struggled in its NAV performance, finishing dead last in the last year in the category. I still like this fund, and it's one of my larger positions today.

CEFConnect

Moving to preferreds, I like the Flah & Crum preferreds and think banks are still extremely cheap. While a banking crisis is always a risk in the background, I think that risk has come down as the yield curve has mostly uninverted. The scare of Silicon Valley Bank helped banks shore up their risks to navigate this environment, if they hadn't done so already.

You can really buy any Flah & Crum fund here, but I primarily own FLC and PFO, the two most discounted funds. That was not the motivation, however, as the discounts are largely driven by the market equalizing the yields.

On Friday, I discussed Templeton Global Inc ( GIM ) in more detail. It remains the 'cheapest' fund on my screen as the post-tender sell off continues. The discount is now -11.1% and the yield 8.8% but by buying this fund, you are playing the special situation of the Saba takeover of the fund (and change of the ticker to SABA).

BlackRock Taxable Muni ( BBN ) is now at a -9% discount and 7% yield. Again, great option for the IRA and high-quality taxable muni income. This is a duration play.

On the other side, a few of the funds we've been pushing lately have risen in valuation, including First Trust Mortgage Inc ( FMY ) and High Income Securities ( PCF ) . I know a bunch of members own RiverNorth/DoubleLine Strategic Opp ( OPP ) , which has also run strongly.

I wouldn't buy any of these here, and I wouldn't necessarily sell here either. For FMY, the shares have rallied hard, but so has the NAV. The discount of -4.1% is slightly overvalued relative to fair value. I just don't think it's overly expensive enough to cut off our income stream and look for something else.

CEFConnect

Funds I would be selling (if I owned them) would be Nuveen Mortgage and Inc ( JLS ), Blackrock Debt Strategies ( DSU ) , Western Asset High Income II ( HIX ), Western Inv Grade DefTerm Opp Inc ( IGI ), and Western High Yield ( HYI ) - all based on valuations being excessive here.

Commentary

For the commentary this week, I wanted to go through the rationale for the swap of PIMCO Access Income ( PAXS ) for PIMCO Income Strategy Inc II ( PFN ) . This raised a few questions as to why, and I did not provide a good explanation in the monthly letter.

The primary factor here is the leverage levels and cMBS exposure. The swap has nothing to do with the distribution safety. This has more to do with NAV performance and future expected performance.

PAXS leverage is now at 44%, which is excessive and likely means that they will have to cut it back if the NAV comes down a bit. PFN leverage is far more reasonable at 23.8%.

The yields are fairly close, with both having a 12-handle.

But check out the NAV performance between the two. PFN trounces PAXS. The largest explanation for the difference in the NAV performance is almost assuredly the allocation to cMBS for PAXS and high yield for PFN.

YCharts

PAXS has a large allocation to commercial mortgages, primarily office and retail. PIMCO believes that they bought these at a deep enough valuation that they will be profitable even with lots of defaults. That remains to be seen, though I do think PIMCO may be a bit early on this trade.

PFN has a lot of high yield that has helped the NAV rally in the last couple of months as the environment went strongly "risk on."

Lastly, there is the relative valuation between the two funds. We run a PIMCO swap model to help identify opportunities among PIMCO funds. PAXS is now at par, which is well above fair value of approximately -4.7%.

{kind=link}

PFN is also near par, slightly above at +1.6% premium. However, that is below of approximately 5.2%.

It isn't all that often you see PIMCO CEFs trade in different directions-meaning one fund rises in valuations (premium rises) and one fund falls in valuation (premium falls). Once that variance between the two 'fair values' breaches a certain level, an alert is triggered.

CEF News and Corporate Actions

Distribution Increase

Blackrock Debt Strategies ( DSU ): +8.4% to $0.09873

DWS Muni Inc ( KTF ): +6.0% to $0.0265

BlackRock Floating Rate Inc ( BGT ): +5.9% to $0.12028

BlackRock Floating Rate Inc Strat ( FRA ): +5.8% to $0.12384

Templeton EM Inc ( TEI ): +5.0% to $0.0462

Templeton Global Inc ( GIM ): +2.9% to $0.0288

Special div: $0.0699

Distribution Decrease

MS Emerging Market Debt ( MSD ): -5.9% to $0.20

BlackRock Enhanced Equity Div ( BDJ ): -2.1% to $0.055

Tender Offer

MS China A Share ( CAF ): The fund announced a new tender offer for up to 20% of shares at a -1.5%.

-

The Tender Offer will commence on January 22, 2024 and will terminate on February 20, 2024, unless extended. If the Fund's shares are trading at a premium to NAV on January 22, 2024, no Tender Offer will be conducted. Additional terms and conditions of the Tender Offer will be set forth in its offering materials, which will be distributed to the Fund's stockholders. If more than 20 percent of the Fund's outstanding shares are tendered, the Fund will purchase its shares from tendering stockholders on a pro rata basis (odd-lot tenders for stockholders who own fewer than 100 shares are still subject to pro ration), based on the number of tendered shares, at a price equal to 98.5 percent of the fund's NAV (net of expenses related to the Tender Offer).

For further details see:

CEF Weekly Commentary | December 10, 2023 | High Quality Opportunities