FPF - CEF Weekly Commentary | Discounts Hit Lows Of The Cycle

Summary

- Major indices were mostly lower (Dow finished up) on the week as the earnings season unofficially has begun. We also saw a hotter-than-expected CPI.

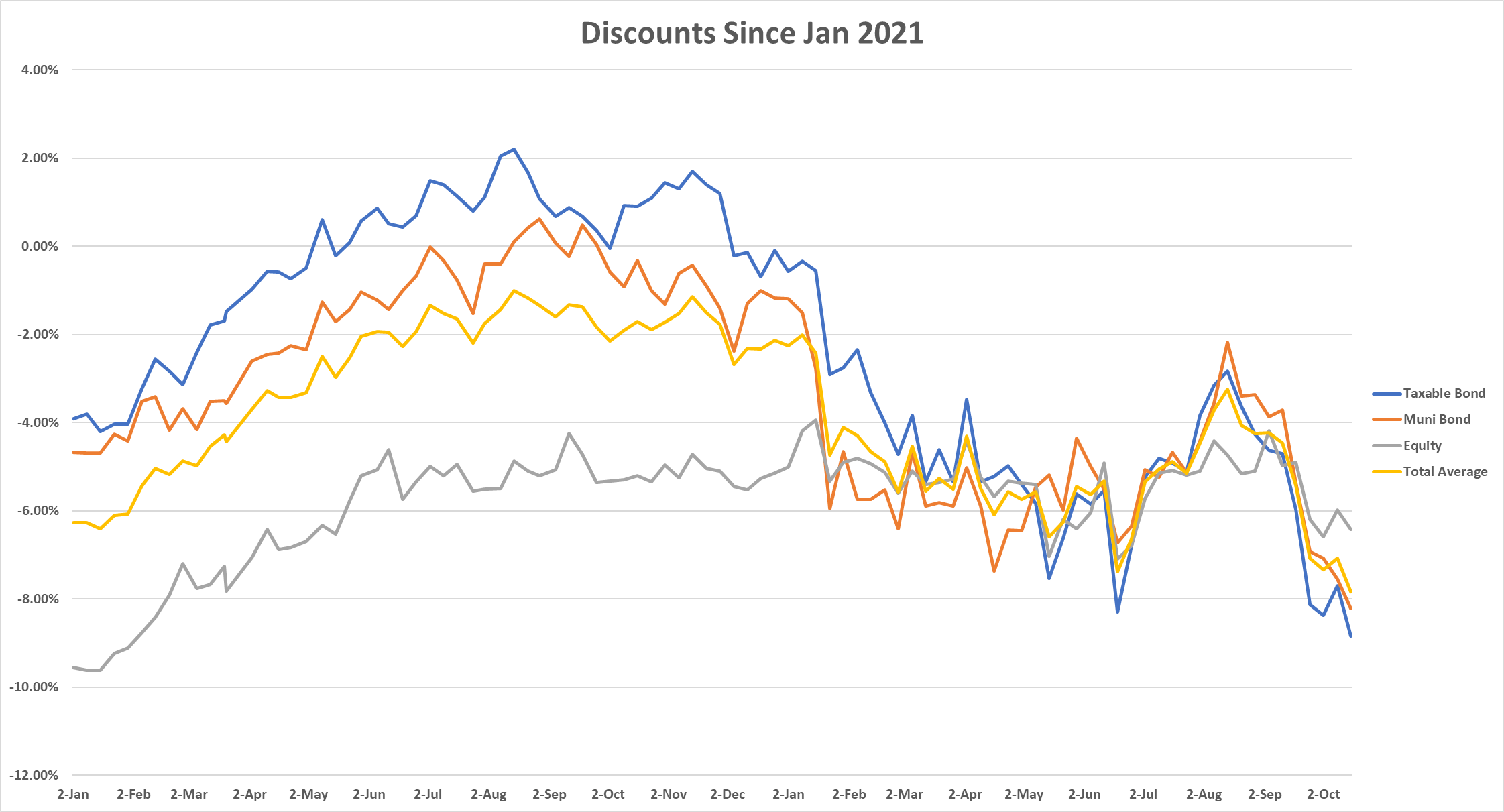

- Discounts are widening out once more and approaching levels not seen since the depths of the March 2020 Covid Crash. Discounts on taxable funds widened to new "wides".

- Those discounts are now entering the left tail which is traditionally that buy-zone area. We are still very concerned about the relatively tight credit spreads.

- We like a blended approach here to minimize regret by nibbling on some muni CEFs here but being patient. We also think you can buy some individual bond issues.

(Attention: This note was written on October 15, 2022. All data herein is from that date).

Macro Picture

Major indices were mostly lower (Dow finished up) on the week as the earnings season unofficially has begun. We also saw a hotter-than-expected CPI ("inflation") report. 14 out of the last 15 have been "hotter" than expected meaning that the market continues to underprice inflation risk.

Headline inflation came in at +8.2%, down 0.1% from the month prior on yoy terms. Stripping out food & energy, the "core" reading rose to +6.6% from +6.3%. Rising prices for services, particularly those of shelter and health care (which tend to be sticky), helped fuel the advance. With inflation continuing to run hot, investors fully priced in a 0.75% increase in the fed funds rate at the November meeting of the Federal Open Market Committee of the US Federal Reserve. They also priced in a 60% chance of another 0.75% hike at the December meeting.

Based on the report, the two-year treasury rate, a benchmark gauge for Fed Funds down the road, rose to 4.5%. So you can now get a 4.5% yield on a two-year risk free note for the first time since 2007.

Fixed income remains a big thorn on investors' side. Check out major asset classes via ETFs (S&P 500, Nasdaq 100, Investment grade bonds, and high yield bonds).

ycharts

The largest takeaway is that high yield bonds - the riskiest layer of the bond market, is the best performing of the bunch. That is an odd outcome this year as, in some cases, investment grade bonds are down more than stocks.

YTD the S&P 500 is down 24% while the investment grade index is down 22.9%. That, obviously, has never happened before. The market right now is pricing in a higher for longer interest rate environment. The question is, "when does the pivot from the Fed take place that shifts us back to a declining and lower interest rate environment.

That will obviously be when inflation comes down to its targeted level. The problem is that it is not really declining. In fact, just looking at Core, it is rising. However, we can look under the hood and see that shelter costs and other factors are a big driver of that and they are rolling over fast.

Shelter will eventually be a drag on inflation as housing prices drop. Shelter costs are ~40% of the entire CPI calculation. The report last week pushed the terminal rate near 5%.

The question will be when does that break something? When will we have a key card in the house of cards fall which makes other things tumble?

lpl blog

CEF Market Review

{kind=link}

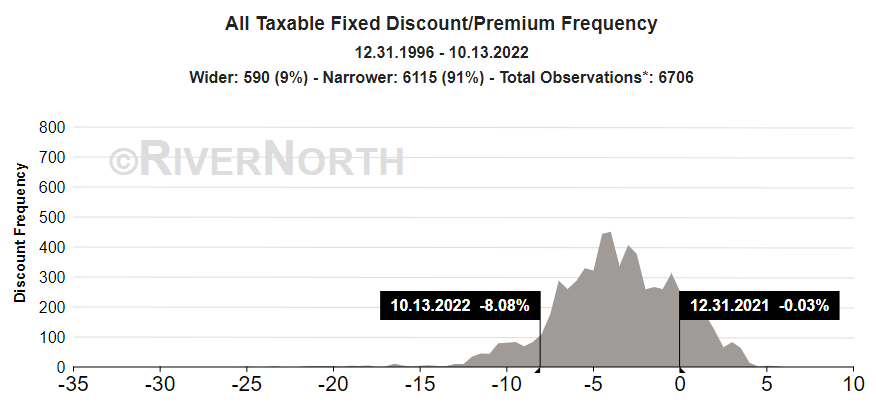

Discounts are widening out once more and approaching levels not seen since the depths of the March 2020 Covid Crash. Discounts on taxable funds widened to new "wides" on the year hitting -8.84%. In just a month, the average discount on a taxable fund doubled. After a slight rebound last week, we widened out more hitting the 91st percentile.

Those discounts are now entering the left tail which is traditionally that buy-zone area. We are still very concerned about the relatively tight credit spreads pushing lower NAVs. Additionally, leverage costs are eating into net investment which causes a two-fold effect:

- NAVs will move lower as the rest of the distribution has to come from holdings

- Tends to reduce distributions for those matching NII = distribution

{kind=link}

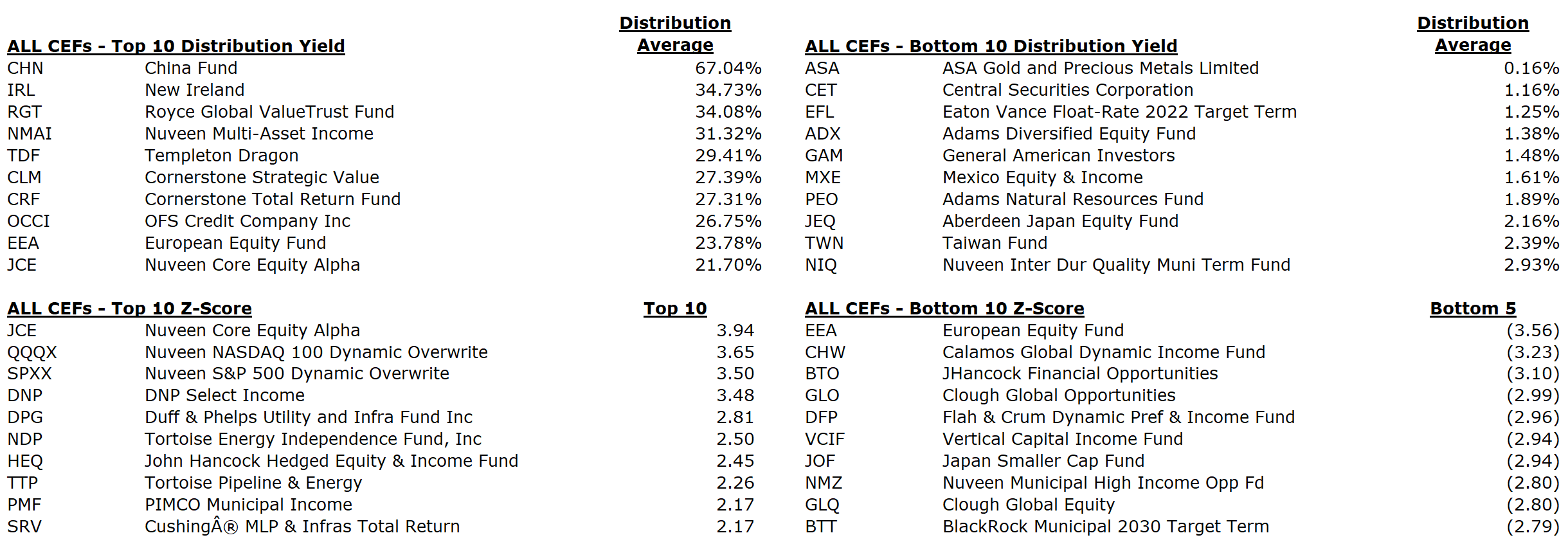

Muni CEFs also saw a lot of widening and are now at -8.2% average discounts. Coincidentally enough, that's the same percentile level going back to 1996 as taxables, 91%.

Again, we are entering the left tail. I'm more sanguine on munis today than taxables simply due to the quality. They are down and out because of interest rate movement and not due to credit concerns (like in 2010). There are little-to-no credit concerns today thanks to state and local budgets being flushed with cash from a strong economy and Federal stimulus.

(more below in Commentary)

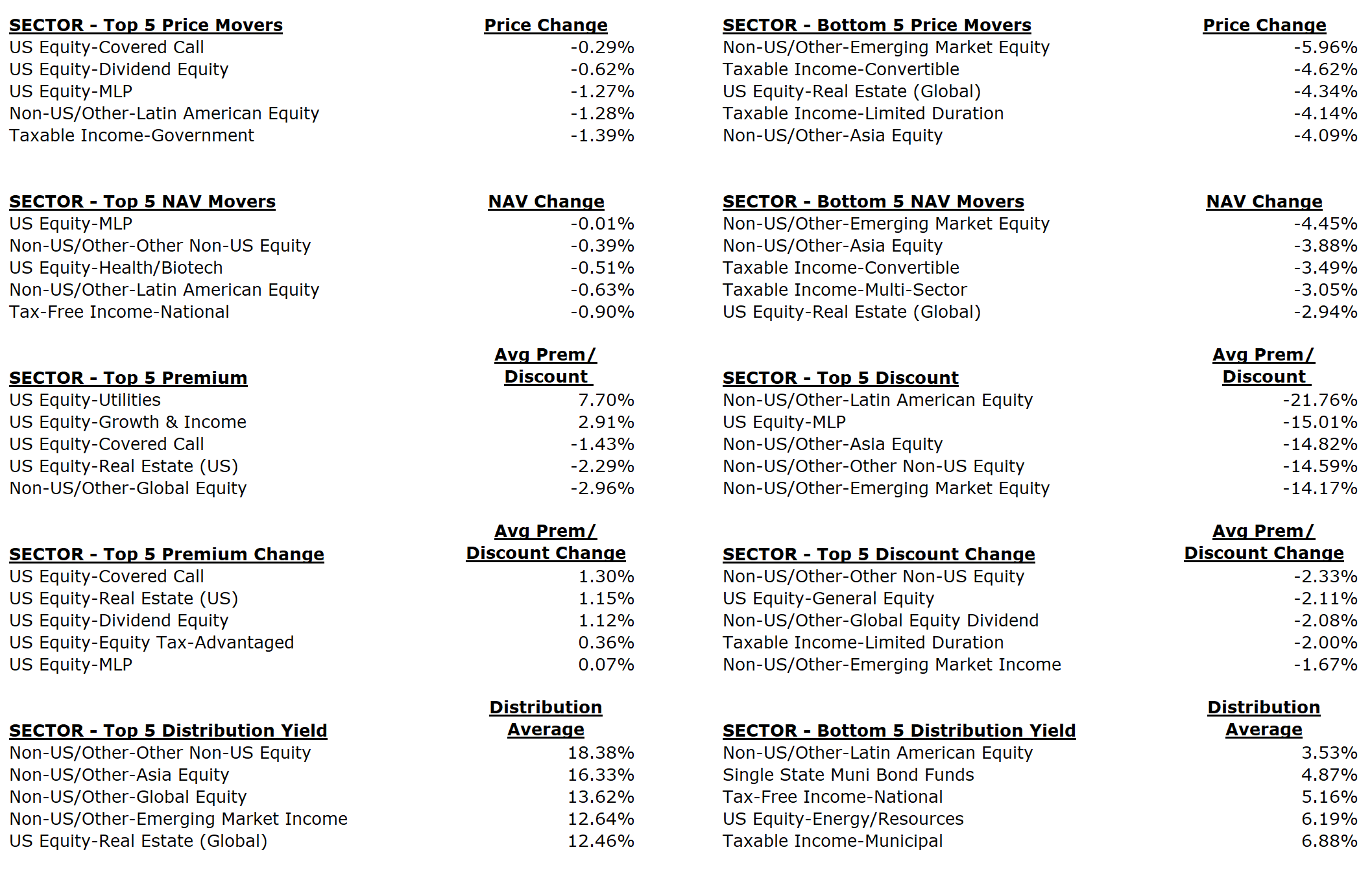

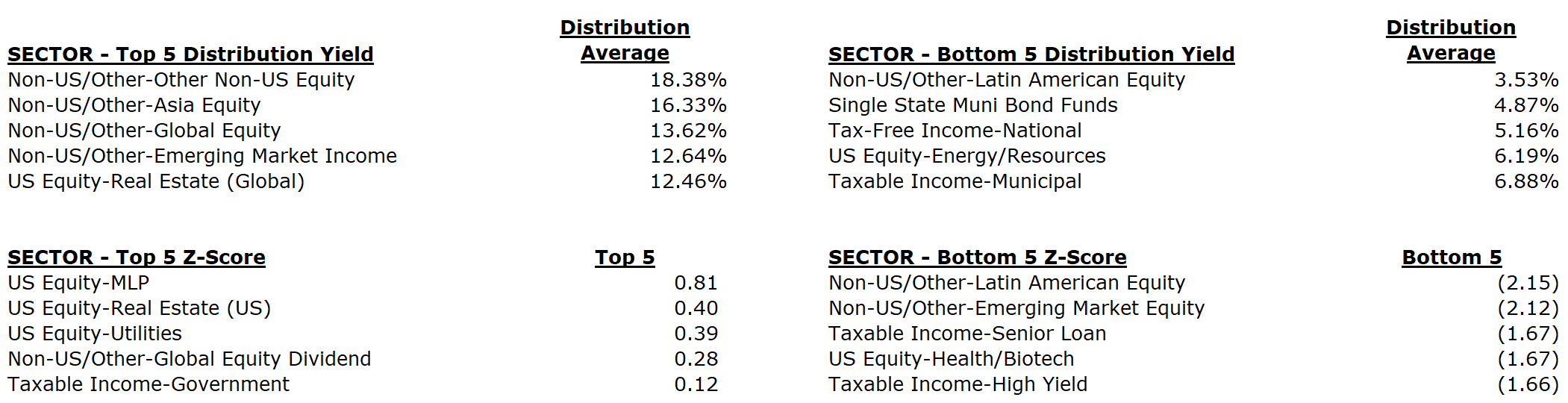

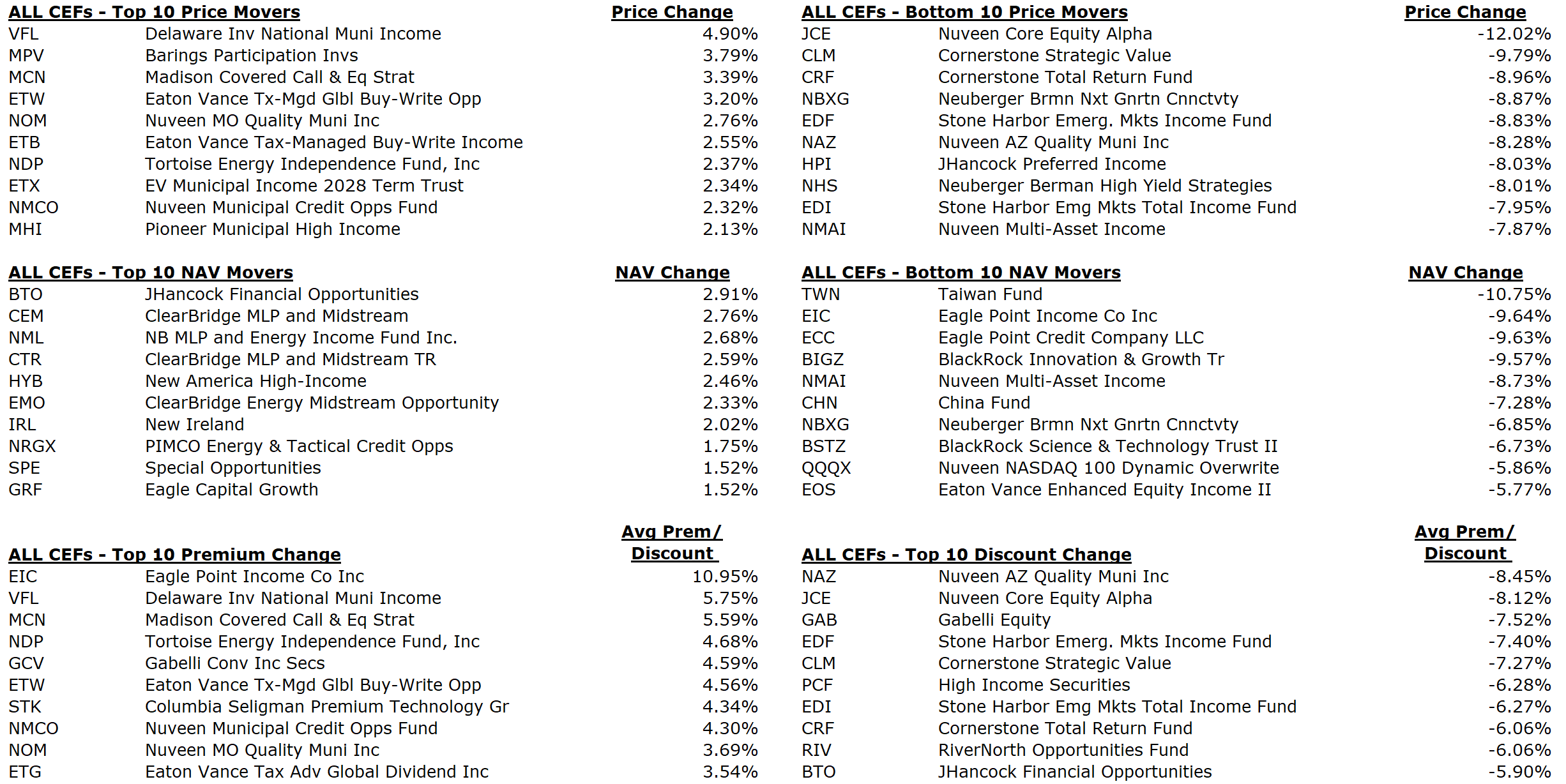

Among sectors, the best areas were energy and international stocks. But most NAVs were lower on the week. The worst were convertibles, real estate, and EM.

Covered calls and real estate also saw the most discount tightening among sectors while equities and dividend equities widened the most.

{kind=link}

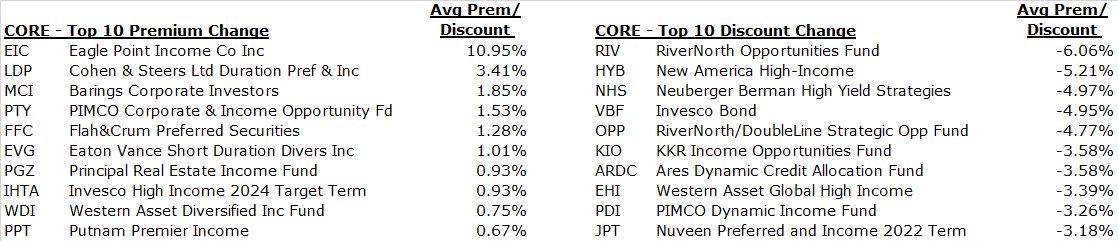

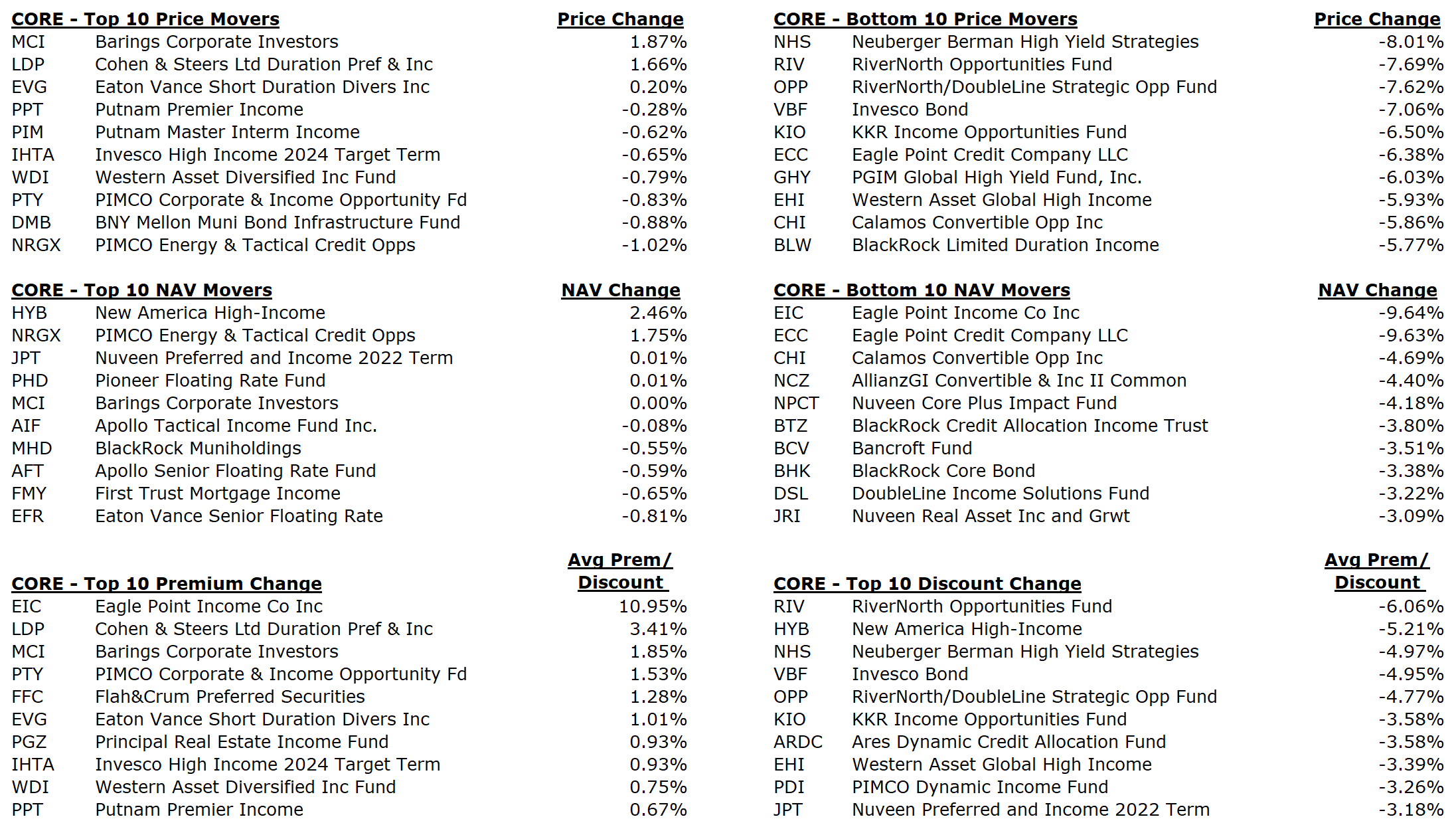

In core funds, only three were positive on the week (MCI, LDP, EVG) on a price basis. Most funds were down more than 2%. Some funds were down more than 5% with a few high yield options down 7-8%.

RiverNorth Opp ( RIV ) had the most discount widening on the week seeing a -6% valuation change. This was due to the rights offering announced last week. We discussed how the discount would widen out on the news. We also saw several funds on the high yield side see significant selling pressure.

{kind=link}

NHS, HYB, and KIO saw discounts really widen out from 3.5%-5.0% - on the week. High yield is finally seeing some selling pressure. There are those that believe that CEF prices (or discount widening/tightening) is a function of the market forecasting where the NAV will be.

charts

It is our belief that the US will enter a recession over the next few quarters and that we need to continue to play defense. While discounts look attractive here, we think there is a substantial risk to the downside in NAVs, especially on the taxable bond CEFs.

We would rather play on the muni side for now. There you don't have as much worry on NAVs falling due to credit concerns. The risk there is that interest rates continue to shoot up. With a 5.0% terminal rate implied already, we think there isn't a whole lot more that it would move up before something really goes wrong.

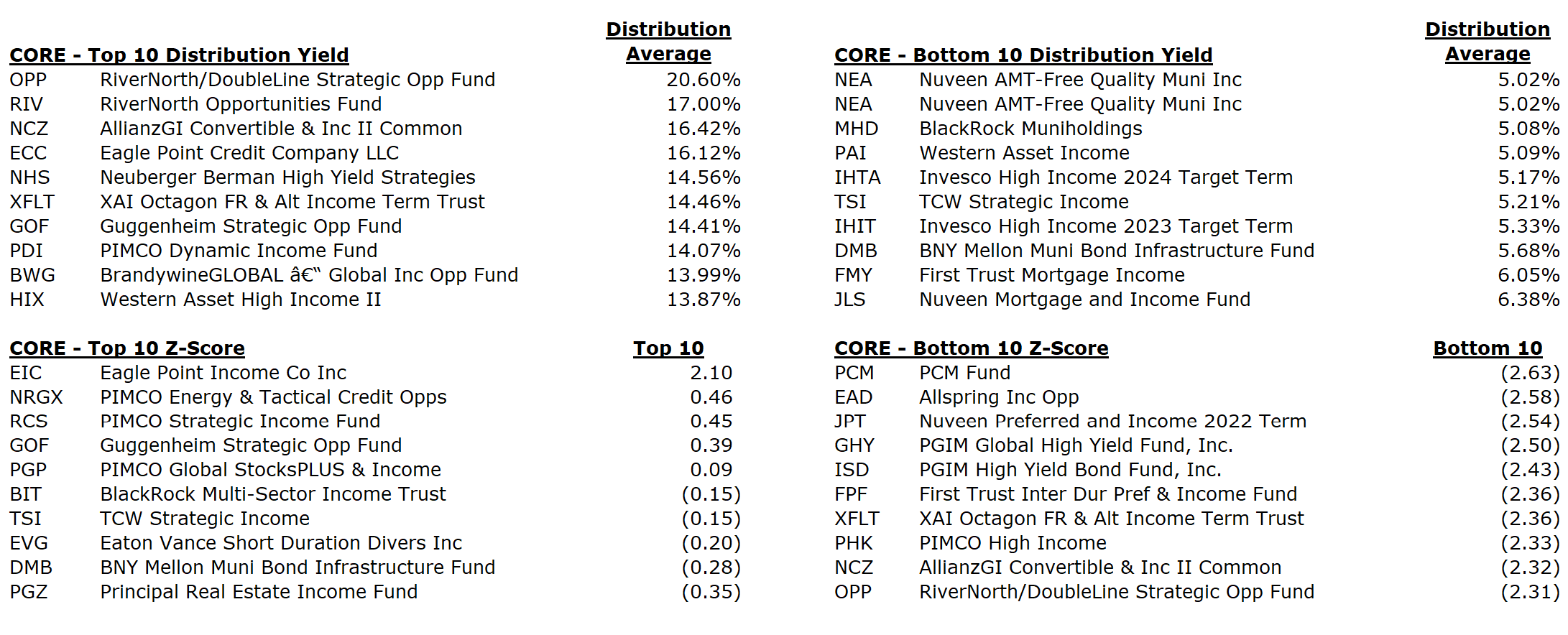

Here are the cheapest funds out there today among the Core set of funds we follow.

{kind=link}

The best option on the list is First Trust Intermediate Duration Preferred & Income ( FPF ). The fund cut the distribution 12% and the bottom has since fallen out. The discount is now nearly -14% and the new yield is 8.6%. That is higher than the old yield before the cut thanks to a much wider discount. We think the shares offer a rare opportunity today.

The reason being is that it's a higher quality portfolio with a relatively lower duration. So the two main risks for bond portfolios being credit and interest rate, primarily doesn't effect this fund. The duration is four years which isn't nothing but it isn't a significant risk when rates rise. Most of the positions are investment grade which doesn't mean no default risk, just much lower.

The primary risk to this fund is leverage costs, via short-term rates. As short rates rise, the leverage costs rise, cutting into net investment income and reducing the distribution. That is what happened this year.

However, when short-rates reverse, they should be able to re-raise the distribution back up. That will likely close the discount significantly.

CEFConnect

We think investors could load up on this one here or set an array of limit buy orders to average in over time.

Virtus Convertible & Income II ( NCZ ) released a statement on the 12th that it had postponed the distribution for October to be paid on November 1.

As previously announced, the declaration of the Fund's monthly distribution of $0.0375 per common share that was scheduled to be declared on October 3, 2022 and paid on November 1, 2022 was delayed after recent market dislocations caused the values of the Fund's portfolio securities to decline and, as a result, the Fund's asset coverage ratio for total leverage as of September 30, as calculated in accordance with the Investment Company Act of 1940, was below the 200% minimum asset coverage guideline. Compliance with the asset coverage ratio is required by the Fund's governing documents for declaration or payment of the monthly distribution. As a result, the Fund is not authorized to declare or pay its monthly distribution until the coverage ratio is in compliance.

The Fund still intends to resume declaration and payment of its monthly common share distributions once its coverage ratio is in compliance. If the Fund is unable to declare a distribution sufficiently in advance of November 1 to set the record date and arrange payment, the payment date will be postponed as well. The Fund will provide information regarding record and payable dates for delayed distributions when available.

Lastly, we have activism by Saba in ClearBridge MLP & Midstream ( CEM ). The hedge fund now owns 682K shares, which just eclipses the 5% threshold of all shares outstanding. The discount on the fund is -15.8%. This is early innings but I can see them eventually triggering a tender or something given that discount. You have to want MLP exposure though.

Commentary

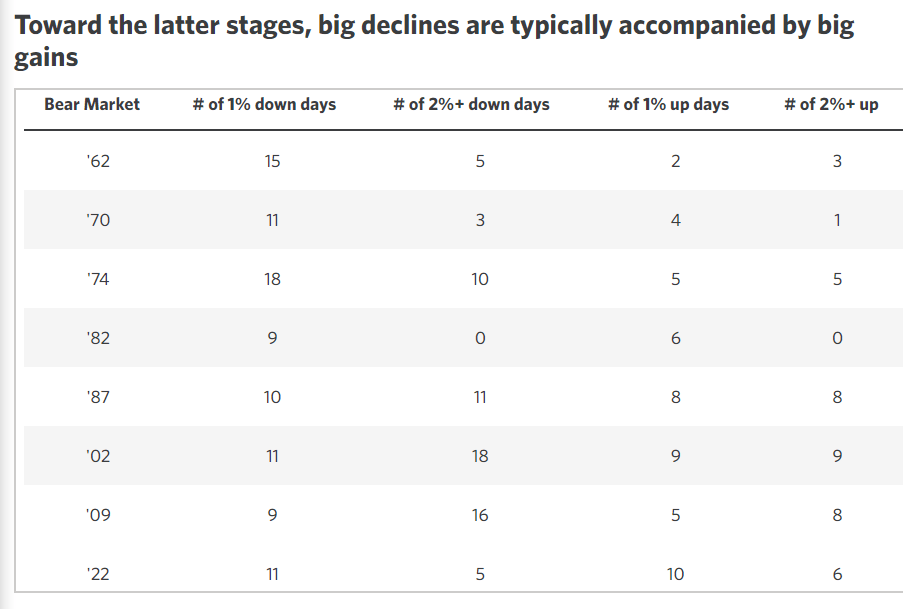

The bear market rages on. We thought this was a helpful article from Edward Jones:

{kind=link}

The last seven bear markets have seen an average decline of 40% 1 . While this year's decline is still well short of that, we don't think we have to approach that level this time. The decline in the mid-'70s was driven by an oil embargo and a painful recession. The early-2000s saw the tech bubble pop get exacerbated by 9/11. Meanwhile, the housing bubble and global financial crisis were behind the '07-'09 decline. This is not to suggest the current bear market is devoid of its own risks, but we view this as more of a cyclical downturn than one that will see extra fuel from shocks and imbalances associated with above-average declines. Excluding the instances mentioned above, the average decline for the remaining bear markets was closer to 30%, which is not too far from the decline we're already experienced 1 .

While the losses are painful to endure, pullbacks are a normal part of investing. Importantly, reaching your destination requires you to stay on the road. Doing so enables you to participate in the rebounds, which are often quite strong right after the market has put in its bottom, with the stock market historically averaging nearly a 50% gain in the first year alone. We think it may still be premature to declare the coast is clear, given ongoing uncertainties around upcoming Fed rate hikes and their impact on the economy. But we believe this market will exhibit a sharply positive reaction when the evidence becomes more clear that the Fed will begin to let its foot off the brake (smaller rate hikes and an eventual pause) 1 .

This bear market can have some legs and could be a longer duration event than many think. The indicator to watch is, of course, inflation. The longer inflation prevails at a rate above 4%, the longer the Fed will keep the screws on the economy.

Above we noted that municipal bonds were a decent opportunity here. It may be a bit early as rates are still rising but sooner, rather than later, rates will turn lower and these muni CEFs will bounce hard.

Discounts are now at the 91st percentile which means that they have only been wider 9% of the time going back to 1996.

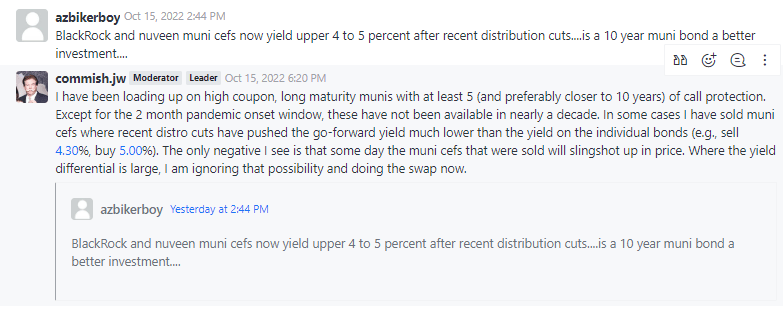

This is an exchange on the chat on Seeking Alpha between a member and one of our moderator/leaders:

{kind=link}

Commish.jw is a muni expert. He noted that he wants to lock in these yields on individual bonds. Yes, as he notes, he is potentially going to miss the snapback in discounts and, to some extent, NAVs.

We are launching two reports this week on locking in yields here for the future. Like I said, it could be a bit early, but it makes sense to start thinking about it and start nibbling.

We have discussed this a lot on the taxable side posting many individual issues of investment grade quality yielding more than 5.50%. That's a great yield to lock in for the next couple of years.

But you can lock in for much longer on the muni side, if you are careful about call protection. With munis, you can lock in a 5% tax- free yield for the next 5-10 years before calls kick in.

Muni CEFs will continue to endure some cuts here but they offer yields of 5.50% or more at discounts of -8% to -12% or more. So the potential for significant upside from here is large if those discounts close back to the long-term average of -2.5%. That's 8-10% upside in cap gains (taxable). Additive to that is if rates come back down, you could see distributions rise by 10%-20% or more depending on how fast they come down and by what magnitude.

We like a blended approach here to minimize regret by nibbling on some muni CEFs here but being patient. We also think you can buy some individual issues or alternatives. The report later this week will have some alternative options for those that do not like buying individual bonds.

- MainStay DefTerm Muni Opps ( MMD ), yield 6.54%

- Nuveen Municipal Credit Inc ( NZF ), yield 5.39%

- Eaton Vance Muni Inc ( EVN ), yield 5.10%

- BlackRock L-T Muni Adv ( BTA ), yield 5.70%

Some final words from Lord Abbett:

It has been a challenging environment for municipal bonds due to persistent inflation and swift and substantial Fed rate hikes. Municipal bond funds have experienced record outflows in 2022 due to investors concerned over rising rates and the impact on the U.S. economy. These factors have caused muni bond yields to significantly increase across maturity and quality segments, while municipal credit has remained strong, particularly in certain sectors. We are focused on areas of potential risks, such as the healthcare sector, but those risks do not suggest increases in default, or that the historically very low default rate within municipal bonds will rise. As the Fed continues its battle against inflation, most municipal bond sectors are well positioned for an economic slowdown. Higher muni bond yields have also been noticed by crossover investors that have begun to step into the market. We think inflows from retail investors will increase as interest-rate volatility gradually subsides. Combined with the resilience of the asset class and the potential for tax-free income, we think these higher yields enhance the appeal of muni bonds for long-term investors seeking attractive tax-free income.

CEF News and Corporate Actions

Distribution Increase

N/A

Distribution Decrease

Destra Multi-Alt ( DMA ): Distribution decreased by 3.9% to $0.0541

Merger

Nuveen OH Quality Muni Inc ( NUO ), Nuveen GA Quality Muni Inc ( NKG ), Nuveen Muni Credit Inc ( NZF ): Nuveen is proposing to merge the former two funds into NZF.

-

- The reorganizations are intended to create a larger fund with lower operating expenses, enhanced earnings potential, and increased trading volume on the exchange for common shares. The proposed reorganizations for the funds are subject to certain conditions, including necessary approval by the funds’ shareholders.

-

- NUO and NZF will hold a Special Meeting of Shareholders to consider approval of the reorganization proposal on February 8, 2023. NKG will hold its 2023 Annual Meeting of Shareholders to consider approval of the reorganization proposal and to elect Board Members on February 8, 2023. Detailed information on the proposed reorganizations and the candidates for election to NKG’s Board will be contained in proxy materials expected to be filed in the coming weeks.

Activism

Statistics

Sector:

{kind=link}

{kind=link}

Core:

{kind=link}

{kind=link}

All CEFs:

{kind=link}

{kind=link}

-----------------

For further details see:

CEF Weekly Commentary | Discounts Hit Lows Of The Cycle