ECCV - CEF Weekly Commentary | Swap Some MAIN Bonds?

2024-01-19 08:00:00 ET

Summary

- Macro markets saw positive movement, with the S&P 500 up 1.81% and bonds performing well.

- The PPI report offset slightly hot CPI, leaving uncertainty about how the Fed will respond to rising inflation figures.

- PIMCO Corp & Inc Strat (PCN), a fund I've been high on for some time, has gone parabolic. There was a recommendation from a Seeking Alpha author that likely drove.

- MAIN 2029 bonds look like a screaming deal here so I made a relatively small partial swap from my large 2026 bonds to the 2029s. I still hold a lot of the 2026s though.

Macro Picture

Markets reverted back to a winning week with the S&P 500 up 1.81%, Nasdaq up 3.09%, and Dow up 0.34%. Small caps lost fractionally. Bonds did well with the Agg up +0.71%, munis up fractionally, and credit up 1.04%.

The driver of the markets was the benign PPI report (wholesale inflation) that offset the slightly hot CPI (consumer inflation report). Headline CPI came in at +3.4% y/y, up 30 bps from +3.1% in November. That was above the Street's forecast of +3.2%.

Core inflation climbed +3.9%, a 10 bp downtick vs. the +4% in November but above the Street's +3.8% forecast. The thing is that both CPI and PPI ROSE in December. I'm not sure how the Fed pivots with these figures.

With a January cut off the table (probability is just 3.8%), that leaves 7 Fed meetings for 2024. That would mean that the market expects a cut in almost every other meeting this year. (the market has six cuts priced in and part of a seventh).

jim bianco

We also saw congress reach a topline budget deal. The Senate leader and Speaker of the House came to agreement on topline spending figures ahead of the January 19th expiration of a temporary funding bill.

Interest rates are on the move - mostly with the 2-year treasury yield coming down. 10s - 2s (10 yr rate minus 2 year rate) is quickly disinverting.

AGC

CEF Market Review

{kind=link}

{kind=link}

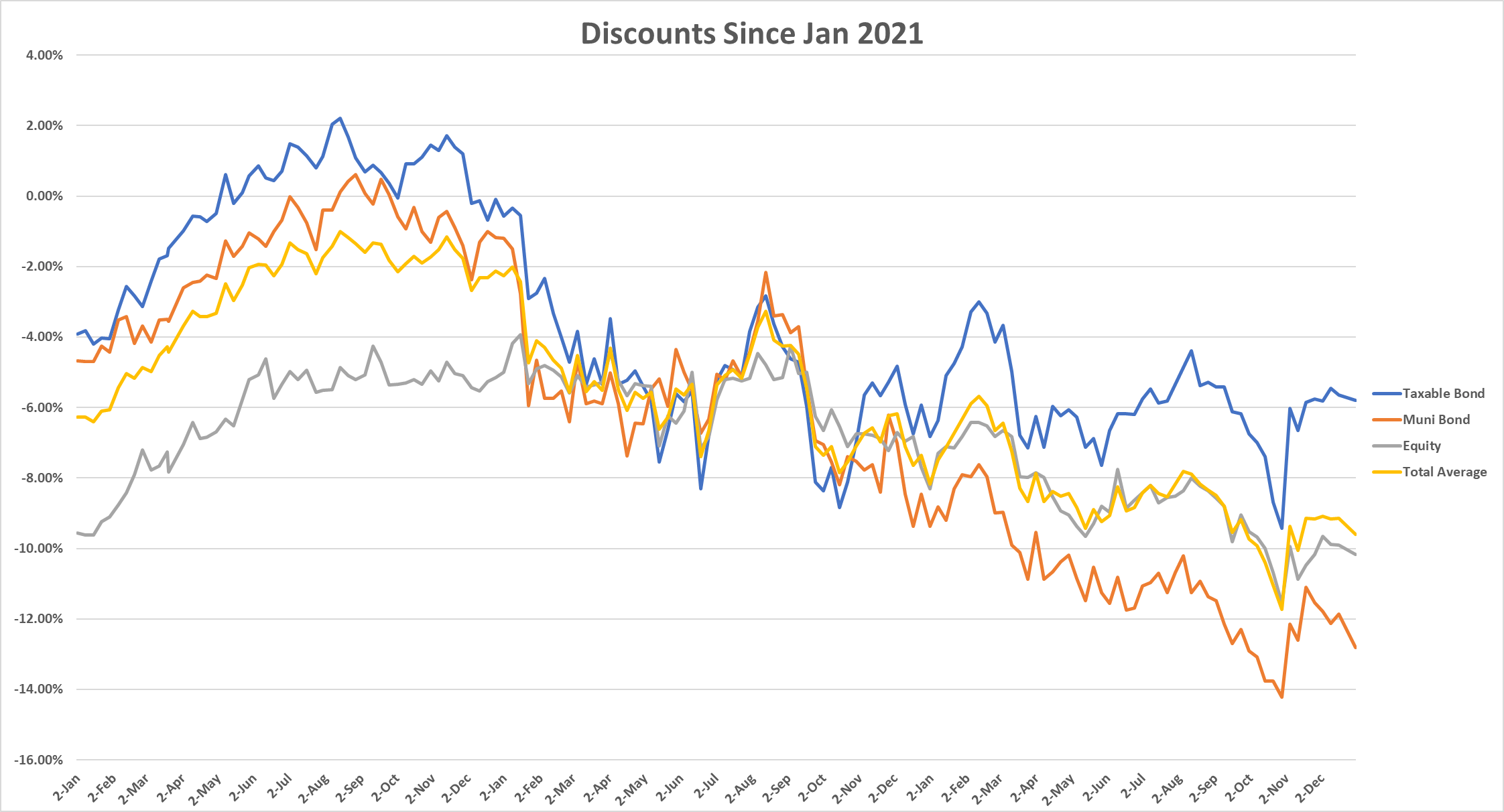

In the last two weeks, we've seen taxables catch a bid and discounts tighten by about 1%. Munis have seen the same discount tightening but they are starting from a much wider level. In fact, munis are no longer at the 98th percentile.

{kind=link}

The equity side of the CEF market saw the best movement on the week while utilities and natural resources/energy were the worst as the energy sector fell 1.5%.

But the price of energy/MLP/natural resources held up causing discounts to tighten overall by as much as 150-170 bps. That made these sectors some of the most expensive in the CEF world (dividend equity beats them out as most expensive).

The cheapest sectors are now covered calls, munis, and preferreds (of which I did a mini report on this past week).

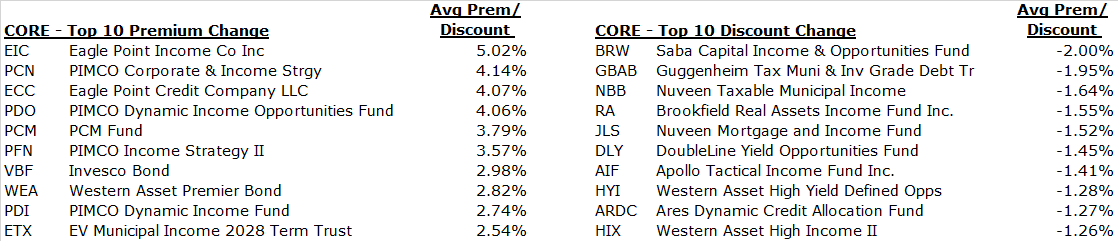

Looking at the biggest movers (to be clear, the largest discount return movers), we had the taxable munis see some of the most discount widening on the week. But the discount of Nuveen Taxable Muni ( NBB ) is back to -6.8%, which is still tighter than the -7% one year average. For reference, the long-term average is -3.0%.

{kind=link}

Of the group on the right, Brookfield Real Assets ( RA ) is interesting at a -12.7% (though I like to buy wider than -13.5%). Despite the massive distribution cut last year, the yield is still near 11.0%. Leverage is light at 17% and 27% of the portfolio is floating rate which reduces the duration down to 3 years making it a good fit for those that want to keep their maturities short.

Most of the funds on the right side (funds that became cheaper) are funds that we've stressed were good trims/sells rather than good buys here. ( AIF), (ARDC), (JLS), (HYI), and ( HIX) all look like excessively valued CEFs coming down in value but not falling to the levels that would make them a buy.

On the left side of the above graphic are the funds that saw the most 'discount return' or valuation change to the upside.

The PIMCOs populate a lot of this list. PIMCO Corp & Inc Strat ( PCN ) , a fund I've been high on for some time, has gone parabolic. There was a recommendation from a Seeking Alpha author that likely drove the jump on Friday.

PCN chart:

CEFConnect

At +13.1%, the fund is now back above fair value (+9-10% premium). If we see additional buying, I will likely be trimming my position as it is now one of my largest.

PIMCO Dynamic Inc Opp ( PDO ) and PIMCO Income Strat II ( PFN ) are both on the list as well. And both are now firmly above fair value. PFN is now at +7%, a level it has not been at since the start of 2023. PDO , at +4.1% premium, is near the highest premium levels it has ever traded.

I would be looking to trim both of these if we have an up move on Tuesday or next week as a whole.

{kind=link}

Looking at another measure of valuation, z-score, shows a few other expensive names. Blackstone Strategic Credit 2027 Term ( BGB ) is one that caught my eye. The discount has broken out to single digits after being in the teens and low double digits for about 2.5 years.

The discount is back to its long-term fair value. However, the question is whether or not the fund is starting to trade on its term feature. I've noted in the past that the term feature starts to play a role around 3 or 4 years left in the term. BGB liquidates Sept 15, 2027.

Sister fund Blackstone Senior Floating Rate 2027 Term Fund ( BSL) liquidates May 31, 2027. That fund also is seeing its discount tighten up nicely and has broken below -9%.

The tailwind yield over both funds are rising through the 2s (meaning that you get a 2%+ bump each year as the fund approaches its liquidation date and the discount closes). This figure can be found on the 'Term Funds' tab on the Google Sheet (column L).

I just can't be certain that the funds will actually liquidate. Blackstone has no history to create a track record as these are their only funds. They have the three floating rate funds ( BGB, BSL , and BGX ). The first two are term funds and the latter is a perpetual.

As I've stated in the past, I still think they merge BSL and BGB into BGX to conserve the AUM. That may just be the cynic in me but I've been in this industry long enough to develop that cynicism.

So What To Do?

I would say if we see more tightening, I will likely let go of my position. BSL/BGB along with FS Credit Opportunities Corp. ( FSCO) , are my floating rate loan funds. I still like FSCO , a lot, and even re-added to it recently.

Another fund I would sell here is Western Asset Premier Bond ( WEA ) which is now down to a -1.5% discount. This is a plain vanilla corporate bond fund with some leverage. No reason it should trade this close to NAV with an expense ratio above 1.0%. You could buy LQD for a few bps and get the same exposure. The capitalization of the expense ratio alone should account for -5% discount alone.

YCharts

Funds to consider trimming/selling:

AGC

Over to the muni side, I continue to nibble and add to my overall allocation as I've ceased buying individual munis simply because of the 1) supply has dried up and 2) the upside in muni CEFs is far superior.

BlackRock Long-Term Muni Adv ( BTA ) remains a big SELL here, trading at NAV. We are not sure why this fund continues to trade this rich (maybe a recommendation from somewhere). We would definitely sell, even if you are a staunch buy-and-holder. The fair value of the discount is much wider and amounts to several years of distributions.

Nuveen Muni High Inc ( NMZ ) continues to get cheaper and is now at -11.6%. I bought some more shares last week as the discount is getting close to the level of late October when it reached its widest levels ever. The yield is now over 5.2%.

Eagle Credit Company ( ECC ) recently issued a new term preferred stock, with an 8.0% coupon and a maturity date of 1.31.2029. However, I think the chance of it reaching that date is low given the high coupon, so the call date is probably more important at 1.31.2026. It pays monthly on the last day of the month. This preferred stock is very rare in that it has a maturity (most are perpetual) and pay monthly instead of quarterly.

Innovative Investors

(H/T Innovative Income Invstr)

Commentary

I've received a number of questions on the individual bond sleeve of the service and whether or not I'm still allocating to it. The answer is yes, but my 'bucket' is basically full. Individual corporate bonds (not including munis) are nearly half of my portfolio (% of TLA). That is not just fixed income but all assets.

That's about as large as I want it given that I have about 20% in equities if I include some passive account structures. The rest are munis and CEFs.

The Daily Shot

I don't trade my individual bonds. As was said by Commish one time, 'I buy them and stick them in the drawer and don't look at them, focusing on the income collection instead.'

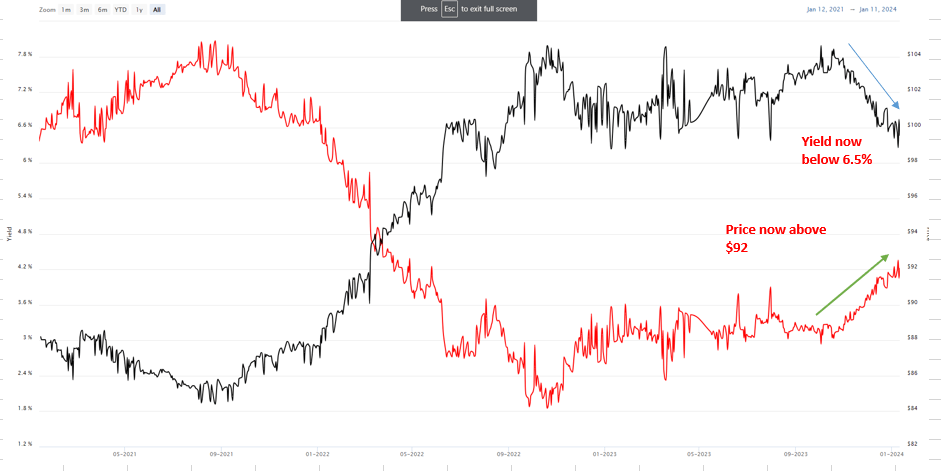

While I 100% agree with that, I did get bought on a relatively small amount of my MAIN 2026 bonds (56035LAE4). The reason I sold this was simple: the price has come up to the point where the yield-to-maturity was low enough and 2) new MAIN bonds were priced with a 2029 maturity date, three years later than these.

Here is a chart on the MAIN 2026 bonds:

{kind=link}

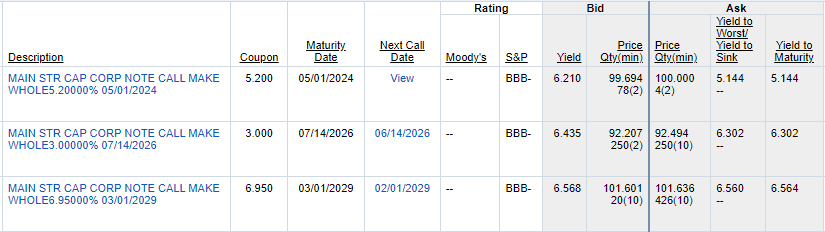

The new 2029 bonds are replacing the May 2024 bonds that are maturing soon. Here is the info on the 2029s: CUSIP: 56035LAH7 , YTW: 6.56%

The variance in the yield is not all the compelling at 6.56% for 2029 vs. 6.30% for 2026. However, this is a high-quality holding and 2026 is not far off. Remember the January letter was titled "Lock It In" and if I can lock it in for an extra 3 years, to me that is worth it. That's why I made a very partial swap and may do more.

{kind=link}

For those that don't want to swap, simply buy the 2029 bonds. I can foresee these bonds eventually being the largest in my portfolio.

CEF News and Corp Actions

Distribution Increase

abrdn Global Infra Inc ( ASGI ): Distribution increased by 33.3% to $0.16

Liberty All-Star Equity ( USA ): Distribution increased by 13.3% to $0.17

Liberty All-Star Growth ( ASG ): Distribution increased by 10.0% to $0.11

Distribution Decrease

Clough Global Div & Inc ( GLV ): Distribution cut by 11.9% to $0.0526

Activism

MainStay CBRE Global Infra ( MEGI ): Saba bought 15.4K shares or $207K, bringing their total to 10.53% of all shares.

BNY Mellon Muni Inc ( DMF ): Saba bought 6,100 shares and now owns 10.7% of all shares.

Added to: ECAT, NXJ, NQP, MAV, NDP, KSM, ENX, VPV, VTN

Selling: VTN, HIE

For further details see:

CEF Weekly Commentary | Swap Some MAIN Bonds?