PAXS - CEF Weekly Review: Term CEFs Continue To Perform Well During Liquidation

Summary

- We review CEF market valuation and performance through the fourth week of August and highlight recent market action.

- CEFs had a second down week, after a solid rally over the previous month.

- We look at a liquidating term fund EFL to see how its NAV has performed over a difficult period - a worry for many investors vis-a-vis term CEFs.

- We also highlight the distribution cut in FPF and Tortoise tender offers.

- We made a couple of relative value CEF switches this week.

This article was first released to Systematic Income subscribers and free trials on Aug. 24.

Welcome to another installment of our CEF Market Weekly Review where we discuss CEF market activity from both the bottom-up - highlighting individual fund news and events - as well as top-down - providing an overview of the broader market. We also try to provide some historical context as well as the relevant themes that look to be driving markets or that investors ought to be mindful of.

This update covers the period through the fourth week of August. Be sure to check out our other weekly updates covering the BDC as well as the preferreds/baby bond markets for perspectives across the broader income space.

Market Action

After a strong July and first half of August, the CEF market stalled, delivering a second negative weekly return in a row. The refusal of the Fed to go along with the market consensus and make a dovish pivot is largely to blame. Only the MLP sector delivered a positive return this week.

Systematic Income

The CEF market has retraced about a quarter of its previous rally and has moved to the levels of early June.

Systematic Income

Fixed-income CEF discounts widened back out about 1% while equity CEF discounts remain tight and expensive, in aggregate.

Systematic Income

Market Themes

The Eaton Vance Floating-Rate 2022 Target Term Trust ( EFL ) plans to liquidate on October 31, 2022. So far only Nuveen has been a consistent terminator of their term CEFs so it is nice to see another manager doing it.

It also shows how investors can monetize the discount as a way to generate additional alpha in their portfolios. The chart below shows that the discount of EFL blew out to a similar level as the average Loan CEF sector discount in 2020 but then tightened much more sharply given its term profile (which, if liquidated, ensures that the discount moves to zero on termination).

Systematic Income

Our view has been that term CEFs can be very attractive portfolio holdings particularly if they trade at discounts close to the sector average as that offers a positively asymmetric risk/reward. This is because a term CEF discount will move to zero on termination. However, if it instead turns into a perpetual fund (on a shareholder vote like the one we saw for DMO) then its discount can be reasonably expected to trade not far from the sector average, especially if the fund's historic performance is decent.

Some investors raise two worries with respect to term CEFs. One worry is the potential for some sort of liquidity / unwind crisis where the fund has to pay through the nose to get someone to take its assets off its hands on liquidation. The environment in the first half of this year has been one of the worst on record for credit assets so it serves as a good test case. Loans are not highly liquid instruments with a very complex settlement process so if the liquidity worry is correct we should see a significant underperformance in EFL versus the sector as it struggled to get rid of its assets.

The chart below shows that we don't actually see that. If anything what we see is the opposite - EFL has outperformed the broader loan CEF sector as the sector sold off. The sector only caught up to it when the fund already went to cash (shown by the flat line).

Systematic Income

Another worry for investors is that they can get stuck selling assets below par (because the liquidating fund is selling assets on their behalf) when they don't want to and that's bad because it leaves money on the table. The idea here is that eventually asset prices will move up and the investors may miss out on the rally. This can happen if the fund moves to cash but then takes several months to liquidate and return the capital to investors.

EFL likely sold its loans around $95 so investors who didn't want to get out of their loan position at $95 may be miffed. This may be true but nothing says the investor has to stay in the fund until the final liquidation. It becomes clear that a fund will liquidate before it starts moving to cash at which point most of the discount amortization juice is squeezed. EFL has been trading at a discount of 0-2% over the last few months, meaning there was very little upside for investors. This means that as soon as the fund says it is moving into cash its discount move is more or less done and the investors can happily transition to another loan fund without forfeiting the allocation or the potential upside.

All in all, EFL, once again, demonstrates that the fear of some sort of sharp loss due to asset liquidation in term CEFs is the dog that fails to bark. Term CEFs remain attractive in the current environment both due to potential discount amortization as well as greater price stability.

Market Commentary

First Trust Intermediate Duration Preferred & Income Fund ( FPF ) cut its distribution by 12%. Investors who followed what happened in the sector in 2020 won't find this surprising. In fact, after the Nuveen preferred fund ( JPS ) cut its distribution we were wondering if FPF was going to do the same.

What's important to know here is that Nuveen and First Trust preferred funds tend to deleverage during drawdowns due to their strict leverage caps. A deleveraging will also obviously hit income though not every fund will cut after a deleveraging.

FPF, along with the Nuveen preferreds funds, did make a distribution cut after a deleveraging in 2020 so, given the difficult price action this year, it's not a surprise they deleveraged again. What's interesting is that the fund started to deleverage slightly even before the start of the year.

Systematic Income CEF Tool

In retrospect that was actually a good move even if it pushed net income lower. Generally speaking, it's a lot better to deleverage, wait out a drop in prices and then add when prices are depressed. That can allow the fund to avoid a forced deleveraging (i.e. it's better to sell when prices are high than when prices are low and you have to sell to avoid breaching a leverage mandate). And it can also improve longer-term returns (by selling high and buying back low).

During 2020 the fund cut its borrowings every month until July when, for the first time, it added borrowings. Borrowings remain about 13% below their September 2020 level. Because FPF cut its borrowings almost each month from October to June it's not yet clear if it will lock in economic losses.

Funds that tend to lock in economic losses are those that wait for the last minute to cut their borrowings, often doing so when prices are already well below their previous peaks. Then they add assets only when prices jump much higher (and typically above the prices at which they sold). Deleveraging gradually through the sell-off can allow the fund, in theory, to then gradually add borrowings during the bounce, keeping economic losses minimal. Historically, FPF has done better than the Nuveen funds though not as well as the Flaherty and the Cohen funds which tend to leave their borrowings alone.

Elsewhere, Tortoise will be running a tender offer for their 5 energy funds (TYG, NTG, TTP, NDP, TPZ) for 5% of outstanding shares at a price of 98% of NAV. Investors unfamiliar with CEF tender offers can have a look here . These funds are trading at double-digit discounts so it can be interesting, however, the tender offers are not due for some time, MLP funds have enormous volatility (i.e. you can make money on the tender offer but lose more on the NAV drop) and there is only an offer for 5% of stock (in practice this can be higher for individual investors as some people will not tender any shares). Net net these tender offers can make sense for people who are already quite happy holding MLPs and want to make a bit of alpha on the side. It makes less sense for MLP tourists who want to make some alpha on the tender offer.

Stance and Takeaways

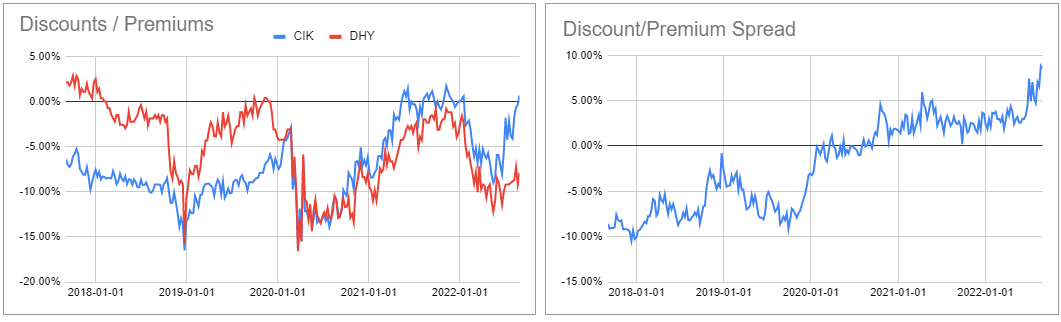

This week we made a couple of CEF switches on valuation grounds in Core and High Income Portfolios. The Credit Suisse Asset Management Income Fund ( CIK ) is switched to sister fund ( DHY ). The discount differential between the two is close to 10% which is (at least) a 5-year record.

{kind=link}

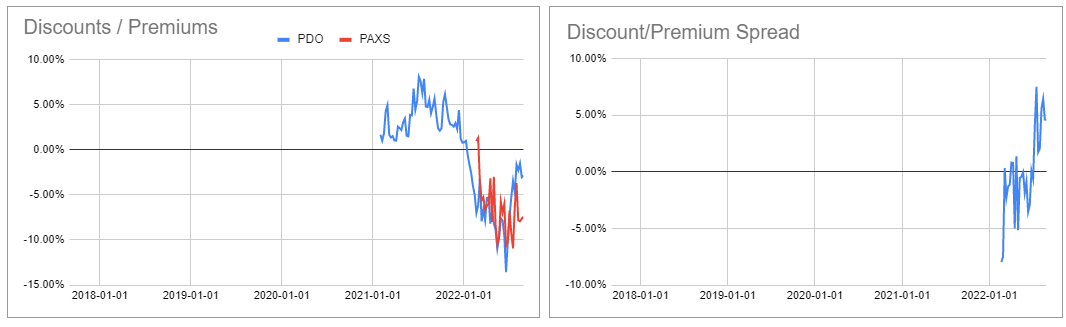

We also made another small rotation between two PIMCO CEFs, specifically, from the PIMCO Dynamic Income Opportunities Fund ( PDO ) to their Access Income Fund ( PAXS ).

The discount differential between the two funds widened out since PDO hiked its dividend. In reality, the two funds have a very similar level of income generation and we would expect PAXS to hike its dividend as well in the medium term. When we made the rotation PAXS offered a close-to 6% wider discount versus PDO - the discount differential has closed somewhat to about 4.5%.

{kind=link}

For further details see:

CEF Weekly Review: Term CEFs Continue To Perform Well During Liquidation