CGAU - Centerra Gold Stock Is A Fair Hold

2024-01-10 11:43:10 ET

Summary

- Centerra Gold has had a rocky few years with the loss of one mine and temporary shutdown of another, resulting in low share prices.

- Recent improvements in financial results make shares of CGAU a decent hold, with a 3.6% dividend yield.

- The company's actively producing mines, Mount Milligan and Öksüt, have provided $49m in free cash flow in 2023.

Centerra Gold ( CGAU ) is a Canadian miner that primarily produces gold but also copper and is expanding into molybdenum, with various mineral assets in Canada, the U.S., Turkey, and Finland. It's had a rocky last few years with its overseas assets, involving the permanent loss of one mine and temporary shutdown of another in 2022. Shares have been low as a result since. Yet, with recent improvements in financial results, weighted against some of the other risks, I'll make the case that shares of CGAU, with their 3.6% dividend yield, are a decent HOLD for the time being.

Brief History

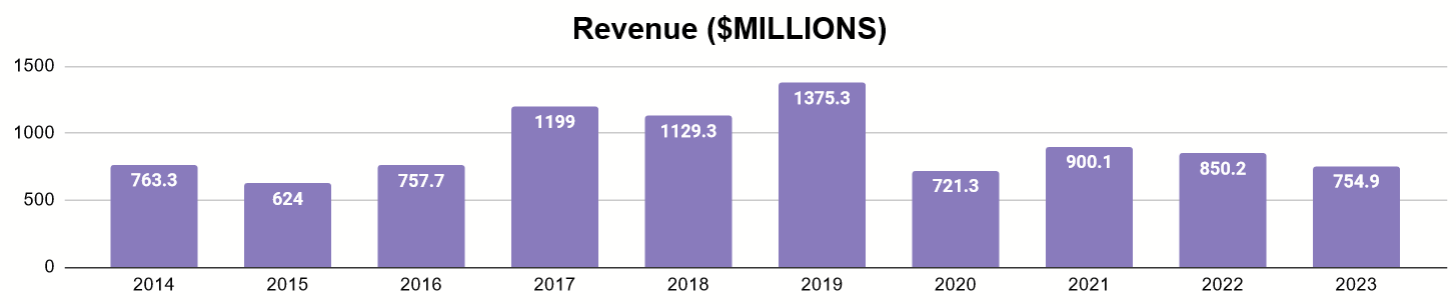

Let's take a look at the financial data on this company from the past decade, including annual results and reported YTD data for 2023. We'll start with a view of the revenues.

{kind=link}

The revenues paint an unusual picture, having had a rise and a fall.

{kind=link}

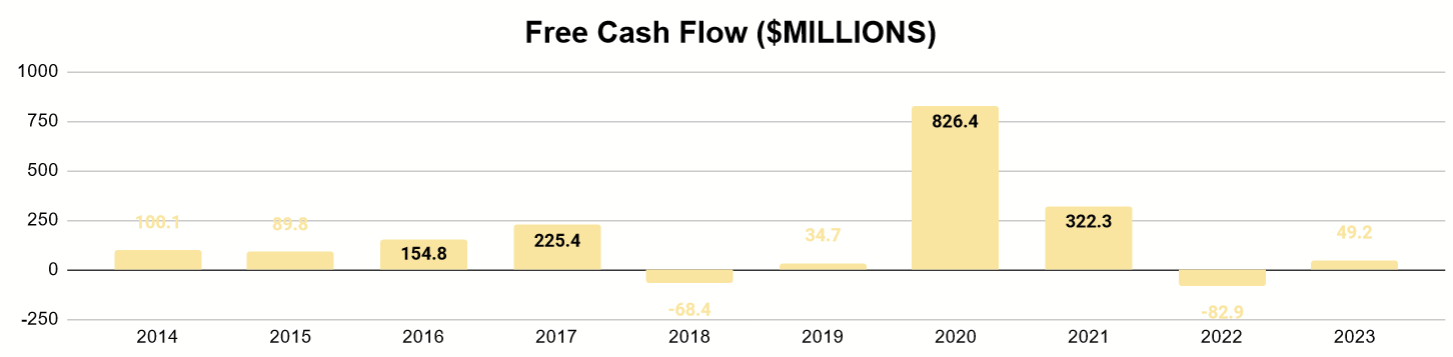

Similarly, free cash flow, while usually positive, has had some negative spots. The dip seen in 2018 was largely due to a rapid rise in operating costs and capex during the period, while revenues did not keep up. Some of this rise followed the company's 2016 acquisition of Thompson Creek, which established its molybdenum operation. By 2020, higher gold prices and increased copper production produced a windfall of positive cash flow for the company.

2020 saw the beginning of operations at its Öksüt mine in Turkey. That year also saw political turbulence in Kyrgyzstan and, consequently, the dispossession of the Kumtor mine in 2021, which was a valuable asset for the company and immediately led to a reversal of these improved financial results. An agreement was reached for Centerra to give up its claims on the mine, in exchange for the repurchase and cancellation of about 77.4m shares that were owned by Kyrgyzaltyn, a Kyrgyz company that held almost a fourth of the Centerra's equity at the time. Concurrent with this, the Öksüt mine in Turkey was temporarily shut down in 2022 to work on safety issues and did not resume production until this year.

Since then, the company has worked to bounce back with improvements on its other assets.

Current Operations

{kind=link}

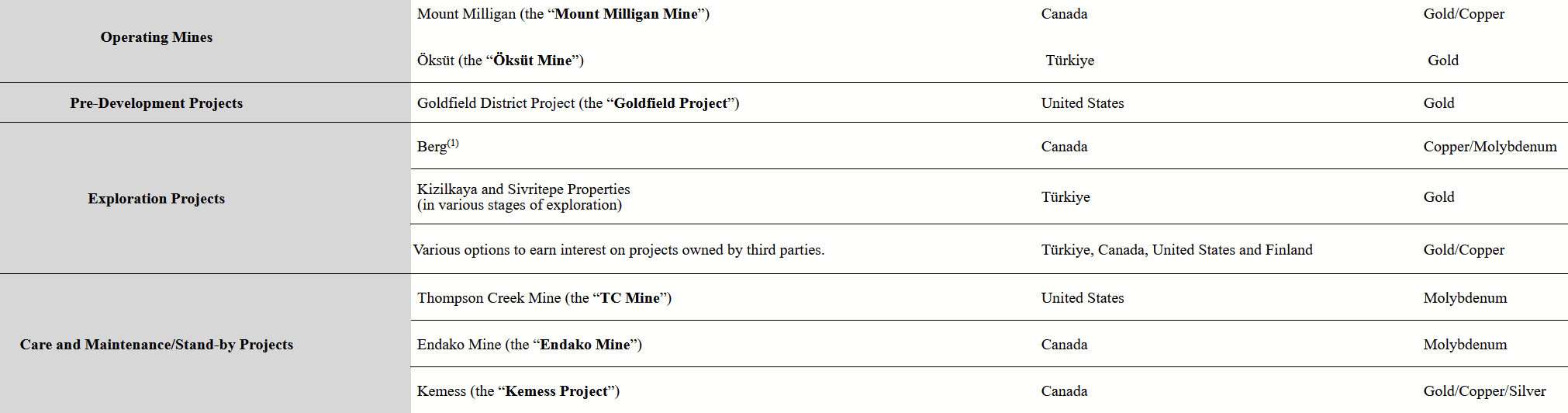

The company has several assets to its name. At the moment, only two are actively producing ores: Mount Milligan and Öksüt. YTD for 2023, these mines, even after expenses related to other assets in the company, have provided $49m in free cash flow.

Mount Milligan

This mine is located in British Columbia, producing both gold and copper ores.

{kind=link}

The mine currently produces at least 160K oz of gold per year and around 70m lbs of copper. Centerra reports a 10-year life of mine as of last November.

Öksüt

This mine is located near Kayseri, Turkey and produces gold.

{kind=link}

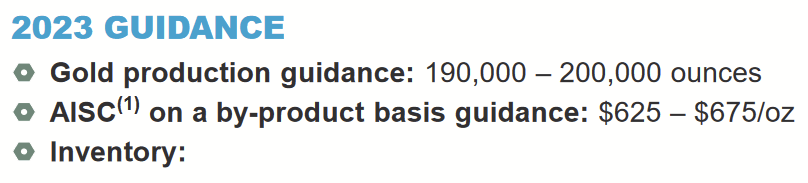

It's currently producing about 190K oz of gold per year. Last November, the company reported a 7-year life of mine.

A Look to the Future

With its history of lumpy cash flows, shareholders will want to see that Centerra can continue toward maintaining positive levels.

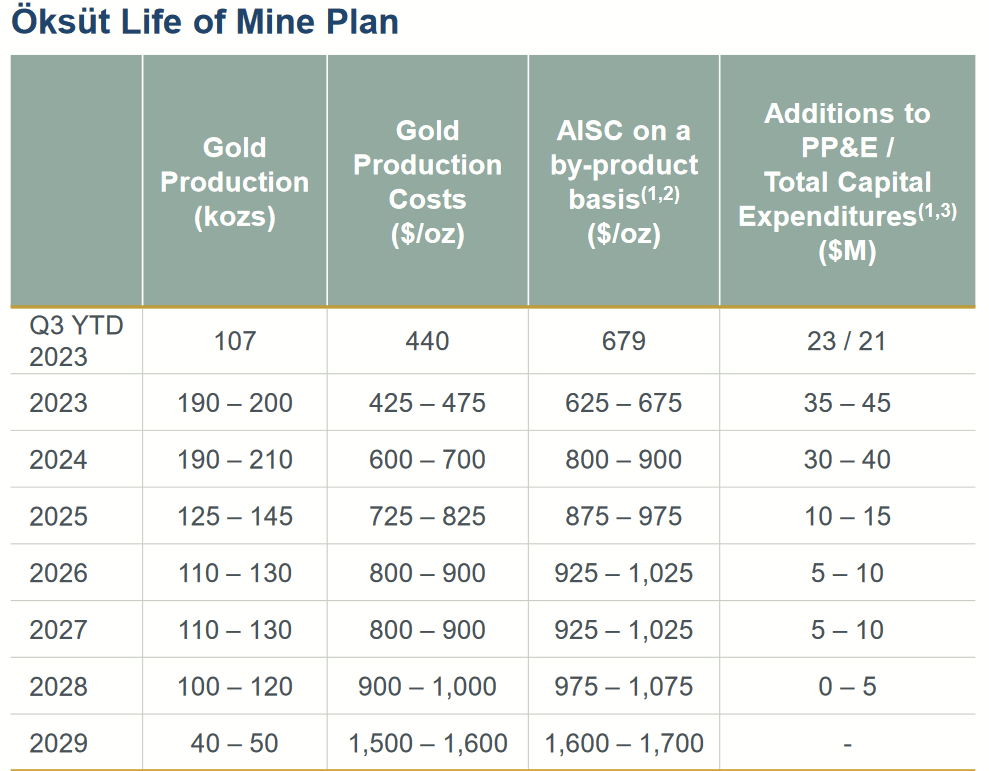

Life of Mine for Öksüt

{kind=link}

The company's life of mine plan for Öksüt does not show currently levels of production lasting for too long. In a few years, they will begin to decline, while AISC/oz is estimated to increase. This will majorly impact revenue for the company unless something can replace it in due time.

Milligan

With a longer life of mine plan, the outlook here is more assuring. Additionally, the company is projecting high production in 2024 as the mine reaches higher grades of ore. I believe Milligan will be a more stable pillar of the company going forward.

Thompson Creek Mine

{kind=link}

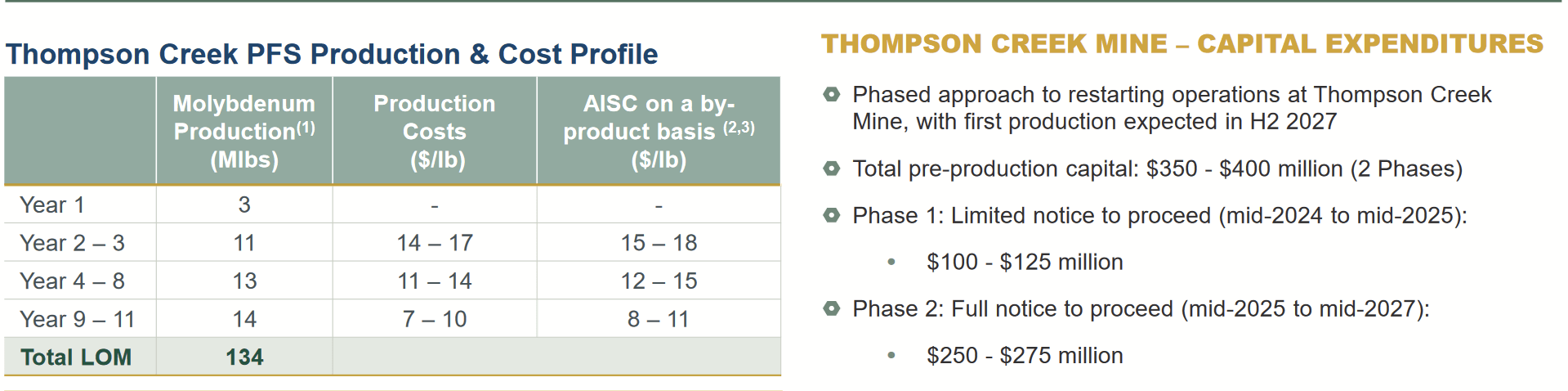

Thompson Creek, which they've had since 2016, is becoming more interesting. I'll quote the Q3 2023 MD&A:

On September 18, 2023, Centerra announced the results of a prefeasibility study ("PFS") on the restart of mining at Thompson Creek, including an optimized mine plan with 11-year mine life with a total molybdenum production of 134 million pounds. The restart of Thompson Creek, vertically integrated with operations at Langeloth, would result in a combined $373 million after-tax net present value (5%) and 16% after-tax internal rate of return, based on a flat molybdenum price of $20 per pound.

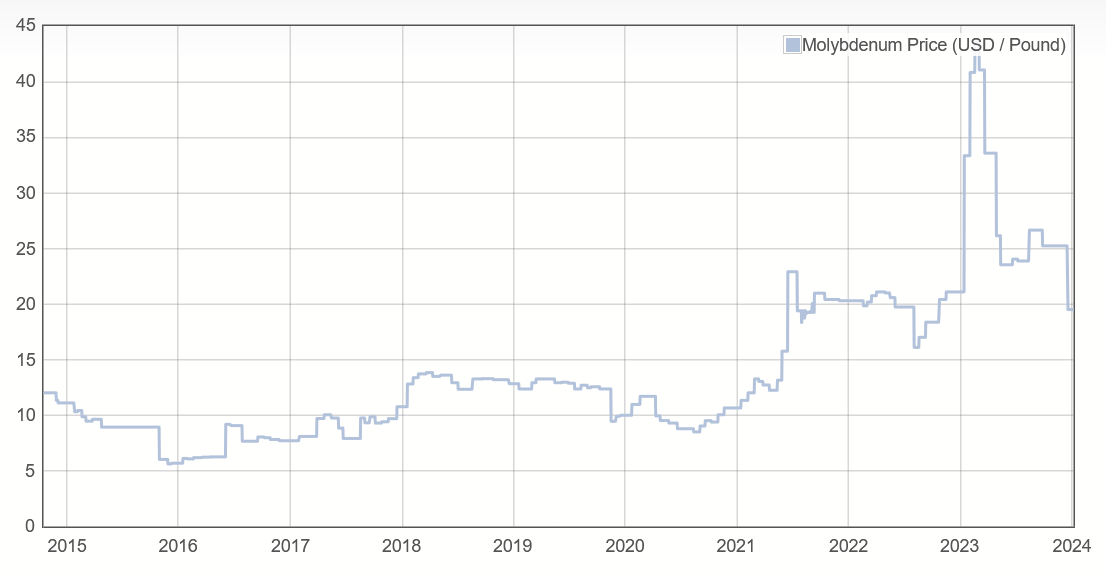

As mentioned here and in the slide above, they don't expect production to restart until 2027, and the initial returns won't be great but are expected to improve with time. They are working with an assumption of $20/lb of molybdenum. Is that a good assumption?

{kind=link}

That's not the lowest the price has been, but given its use in making steel alloys and how China aims to boost fiscal spending to spur its economic growth, I believe demand for steel will remain strong and thus that of related commodities. $20/lb seems like a reasonable assumption to me, and this means Thompson Creek should be able to replace the cash flows that will dissipate as the Öksüt mine matures.

Other Projects

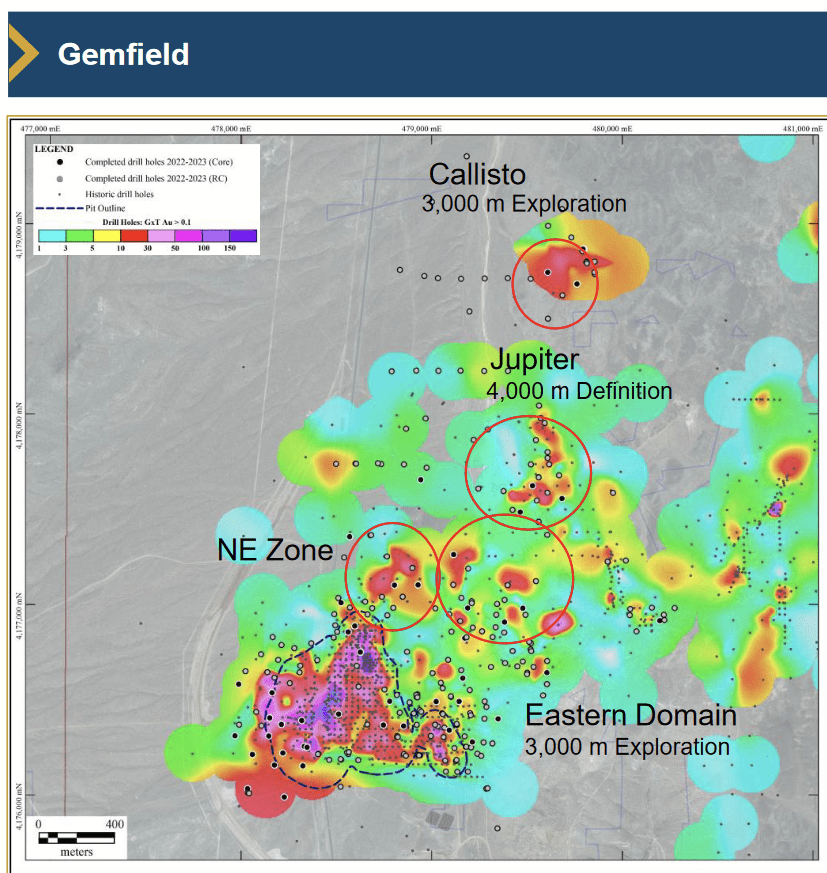

The company acquired the Goldfield assets in Nevada in 2022. The main area of focus there will be Gemfield.

{kind=link}

The company believes that it could serve for open-pit operations that extract oxide and transition materials. This will be one of their main assets to watch going forward.

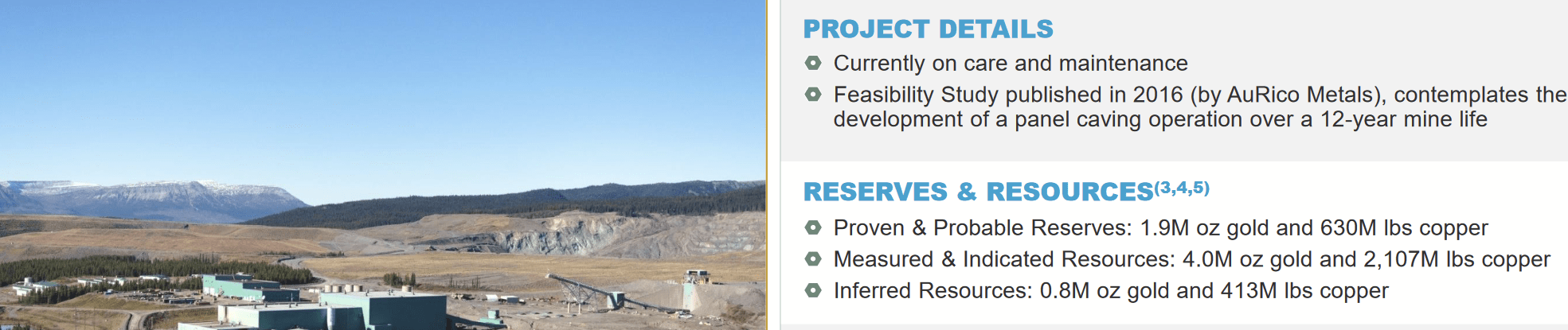

Another asset in British Columbia worth watching will be the Kemess mine, initially acquired in 2018 and currently under care and maintenance.

{kind=link}

It notes in this slide that the previous owner's feasibility study suggested a 12-year life of mine for gold and copper production. A more updated study might be in order now, but this is another thing that could produce additional upside in the long-term. We do not currently know when the company will make use of Kemess, so it's difficult to say more until the company makes further plans.

Balance Sheet

{kind=link}

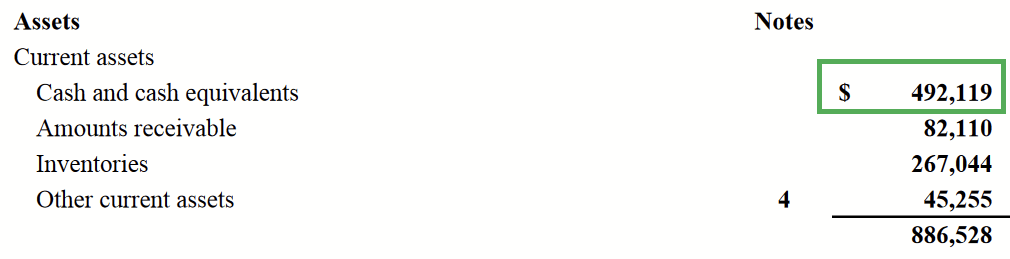

As of Q3 2023, the company reported over $492m in cash on its balance sheet. With zero debt, this brings net cash per share to about $2.28. I believe this cash cushion will be very helpful to the company going forward. Even during the unpleasantness of 2022, the negative free cash flow was only $83m, suggesting the company has sufficient liquidity to navigate this uncertain future and even maintain its current dividend.

Valuation

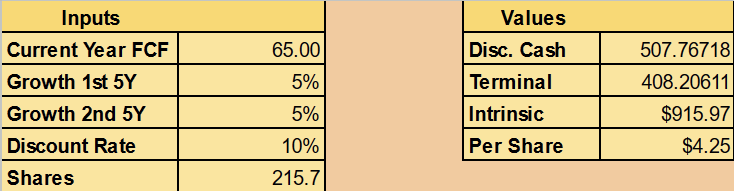

With all these factors to consider, I am going to calculate a conservative Discounted Cash Flow with these assumptions:

- Baseline annual FCF of $65m

- Average annual growth of 5% in FCF the next decade

- A terminal multiple of 10

I believe $65m is reasonable given that it's not historically excessive and that reported YTD 2023 FCF is $49m. I believe 5% is reasonable given the company's plans to make incremental improvements at Milligan going forward and that eventual unveiling of Thompson Creek, which should substitute Öksüt's fading cash flows and eventually see rising production levels thereafter. A terminal value of 10 will reflect the additional value of its exploratory assets farther into the future.

{kind=link}

That gets us to an intrinsic value per share of $4.25. An additional cushion of value also comes from the net cash per share of $2.28.

Most of the uncertainty is in the latter half of the decade, and miners being miners, it concerns both upside downside. There could be execution failures with Thompson Creek, while Öksüt will probably wrap up all the same. Similarly, production levels could be higher than guided, or the company could benefit from higher mineral prices for the same projected costs, and the exploratory assets could prove actionable much sooner as well.

Yet, with its healthy balance sheet and a decent dividend yield around 3.6%, CGAU is not a particularly risky stock to hold while we wait and see.

Conclusion

Centerra Gold is a company that has been kicked around over the last few years. Yet, 2023 showed a return to positive free cash flow and thus returns for patient shareholders. The current price slightly exceeds conservative estimates of cash-generative ability, but the company's large cash reserve and adequate dividend yield make holding it a reasonable option as well. Milligan will keep the course steady, and Thompson Creek is where a lot of the hopes of the near-future are.

Shareholders should watch these developments closely and should have entry/exit plans based on possible price fluctuations in the near-future. For all these reasons, CGAU is a fine HOLD for the long-term investor in my view.

For further details see:

Centerra Gold Stock Is A Fair Hold