CRNT - Ceragon Networks: This $1 Tech Stock Is My Top 'Buy And Hold' Pick

2023-04-18 11:34:11 ET

Summary

- Ceragon Networks is deeply undervalued based on numerous factors and financial metrics.

- This company is a best in breed industry leader with a savvy management team that is also aligned financially with shareholders.

- After years of investing in 5G technology, this company can now reap the benefits of secular growth coupled with expanding profits.

- Analyst price targets of $5.25 per share implies significant upside, but I think $10 per share is possible in the next couple of years.

A couple of years ago, I wrote a bullish article on a beaten-down tech stock that was trading for about $1. That article did not get much attention in terms of page views or comments (only 11 comments), but it turned out to be an amazing investment for anyone who bought and held the stock, because that same stock now trades for around $37 per share. It's these kinds of gains that keep me interested in micro and small cap stocks that are not on the radar for most investors. Before Aehr Test Systems ( AEHR ) turned into a gold mine, it languished for years and had a number of spikes in the share price, but then it suddenly took off and became a huge winner, making life-changing gains for many shareholders who were willing to buy and hold. I see another small tech stock that has similar characteristics which could also be poised for big gains in the next couple of years, so let's take a closer look:

Ceragon Networks ( CRNT ) makes equipment for the telecom sector. It now trades in the $1 to $2 range, just as Aehr Systems did. It also has a very low price to sales ratio, a very strong balance sheet, an experienced management team that perseveres, and its products have a significant total addressable market, which were other similar traits that I saw in Aehr Test Systems. The chip industry has strong growth potential and that has helped to turn Aehr Test Systems into a secular growth stock story. I see similar growth potential with Ceragon Networks for a couple of reasons which include robust demand for telecom, especially with 5G and future connectivity buildout needs. But there is also another huge positive for Ceragon Networks and that is the desire for Western countries and companies to increasingly seek goods that are not supplied from a Chinese company. The geopolitical risks of sourcing and buying Chinese tech products has increased significantly and some countries have even placed bans on certain Chinese companies and products.

The Chart:

StockCharts.com

As shown in the chart above, this stock surged to around the $7 level in early 2021. In May and June of 2022, the stock traded around the $1.60 level and bottomed out there, and then surged again to nearly $3 per share. The stock is now currently trading around the same $1.60 to $1.70 per share range that it bottomed out at in May and June of 2022. This could be a sign that a very bullish double bottom is forming on the chart now. This stock is now at a level that has almost always rewarded shareholders who bought at the current price. The 50-day moving average is $1.80 per share, and the 200 day moving average is about $2.05 per share. Based on this, the stock could be poised to rebound back towards the $2 level in the near-term and hit the key 200-day moving average support level.

The Buyout Offer In 2022 For $3.08 Per Share And Analyst Price Targets Of $5.25 Suggests This Stock Is Deeply Undervalued:

Aviat Networks ( AVNW ) offered $3.08 per share to buy Ceragon Networks in late 2022, but the offer was rejected. Management viewed the offer as too low, given the longer term potential of this company. With shares now trading for just around $1.70, this stock appears to be a bargain, trading for nearly 50% off of what another company was willing to pay for it not long ago. It also appears deeply undervalued based on the recent price target of $5.25 per share , which was set by analysts at Needham in February 2023.

There are other metrics that suggest this stock is deeply undervalued. According to data from Seeking Alpha, earnings estimates are at 23 cents per share for 2023, with revenue estimates coming in at around $334 million. For 2024, estimates are at 34 cents per share on revenues of around $364 million. Based on 34 cents per share in earnings, this stock is trading for just about five times earnings. In addition, Ceragon Networks has a strong balance sheet with just about $54 million in debt and nearly $23 million in cash.

With a market capitalization of just about $140 million, and annual revenues that are well over $300 million, this company also looks deeply undervalued in terms of the price to sales ratio. Many tech companies trade for multiples of their annual revenues, so this leaves a lot of room to the upside for Ceragon Networks. On March 28, 2023, Ceragon Networks announced it received a $29 million order from India . This is very impressive (and suggests shares are undervalued) coming from a company that has a current market capitalization of about $140 million. This major order is expected to be shipped and deployed in 2023, so it can add to revenues this year.

The Shareholder Base Is "Smart Money" And This Suggests Potential For A Much Higher Share Price:

Zohar Zisapel is the founder and Chairman of Ceragon Networks. He owns about 6.8 million shares. He has been called the "Bill Gates of Israel" and the father of Israel's high tech industry". I see Mr. Zisapel as part of an impressive management team that appears to be financially aligned with shareholders. The current share price might make some investors regret that management refused a $3.08 per share buyout. But longer term investors might still do very well, because management must see a much higher exit strategy for shareholders as well as for the millions of shares they own.

As mentioned previously, "The Bill Gates of Israel", Zohar Zisapel, owns about 6.8 million shares, and he is not the only "smart money" investor who has taken a significant stake in Ceragon Networks .

Aviat Networks, which made an offer to buy Ceragon Networks for $3.08 per share, owns around 3.3 million shares. Aviat Networks is still holding these shares, even after their offer was turned down. This suggests that Aviat Networks could be thinking this stock is a great investment to hold, or perhaps they have a continued interest in making another buyout offer. I view Joseph Daniel Samberg, CEO and Chairman, of JDS Capital Management, which owns or controls about 8.3 million shares of Ceragon Networks, as yet another "smart money" investor. Mr. Samberg wrote a letter that supported the decision to reject the buyout offer from Aviat Networks, giving a number of reasons why Ceragon Network shares could become increasingly valuable in the coming years, it stated :

"Over the past few months, the Company has reached out to my team and me to explain its revised strategy and prospects, and mostly these conversations have been with the CEO, Doron Arazi. These conversations were constructive and, we believe, honest and forthright. In the past year since Doron was appointed CEO, we believe he has positioned the Company well for future growth as evidenced by, among other things, the healthy order pipeline. We believe that, over the coming years, several factors should significantly improve the Company’s prospects: supply chain issues should subside, new technology offerings will increase margins, network investment in 5G will accelerate, and economies will continue to open post-COVID. We believe that, once some or all the factors come to pass, the Company’s current projects and offerings will turn into profitable revenue growth and significantly increase value for shareholders. We have confidence in Doron and his team and believe their skills and experience will be critical in creating significant value in the Company."

Why Ceragon Shares Could (Once Again) Trade At The $7 Level And Beyond:

Based on this statement from Mr. Samberg, and his willingness to forgo a buyout offer of $3.08 per share, it would appear to suggest that transformative growth potential is expected in the coming years. Along with that revenue growth, there should be a corresponding impact on the share price. It's my belief that a savvy investor with millions of dollars in this stock would not turn down over $3 per share in a buyout, unless they had a strong belief that these shares would hit at least double or triple that amount in the coming years.

Ceragon Networks shares did spike to about $7 per share in early 2021, so there is fairly recent historical precedent for a much higher share price. If this company meets 2024 earnings estimates of 34 cents per share, a price to earnings ratio of just around 20, would put the share price back around the $7 level. If the company can grow earnings to 50 cents per share (as revenues rise) in 2025, a similar valuation could push the shares up to around $10. If/when hedge funds and institutional buyers take note of this stock as they did with AEHR, the valuation could be much higher than it is now.

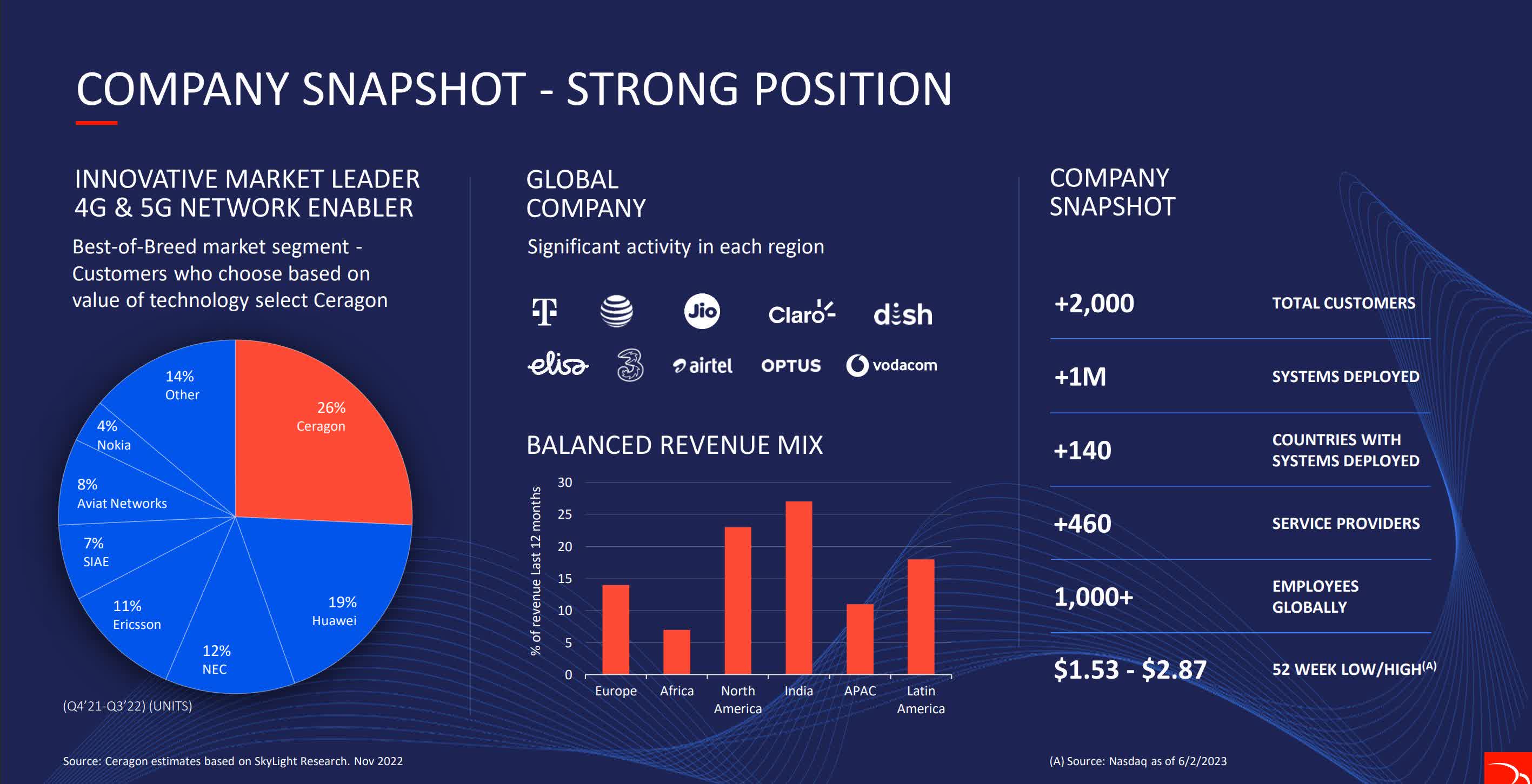

Ceragon Networks Is The "Best In Breed" Industry Leader:

As shown below, Ceragon Networks is a market leader and best of breed when considering various metrics. It also shows this company has a geographically diversified customer base and it is doing business with the biggest companies in this industry.

Ceragon Networks Investor Presentation

{kind=link}

Source: Ceragon Networks Investor Presentation

As shown below, there is an estimated $77 billion+ in funding for broadband that supports connectivity and 5G. This is just for the United States alone and it shows the ongoing secular growth potential for companies like Ceragon Networks.

Ceragon Networks Investor Presentation

{kind=link}

Source: Ceragon Networks Investor Presentation

China Security Concerns And Bans Will Benefit Ceragon Networks:

As you can see in the graphics above, Huawei has a significant share of the market and that could erode as Western companies increasingly seek to avoid Chinese tech products due to security and chain supply concerns. Many countries have already banned certain Huawei products, and it was recently reported that Germany is considering a ban of certain components from Huawei in its 5G networks. These concerns and additional bans are likely, especially as tensions rise over spying concerns and threats against Taiwan. This could tremendously benefit Ceragon Networks in the coming years. Not only would bans and concerns about doing business with China help boost revenues, it could also significantly expand profit margins.

A.I. Is About To Boom, Taking 5G And Potentially Ceragon Networks With It:

Many tech industry leaders are now saying that A.I. is now having an "iPhone moment" in order to suggest how transformative and ubiquitous it will now become. It is expected to transform every industry over the next few years. This is likely to drive increased demand for connectivity and 5G networks. A recent article by Entrepreneur discusses the combined force of 5G and A.I. and how these disruptive technologies are synergistic. It makes the point that A.I. is going to accelerate the demand for 5G and it states :

"Artificial intelligence and 5G are the two most critical elements that would empower futuristic innovations. These cutting-edge technologies are inherently synergistic. The rapid advancements of AI significantly improve the entire 5G ecosystem, its performance, and efficiency. Besides, 5G-connected devices' proliferation helps drive unparalleled intelligence and new improvements in AI-based learning and inference. Moreover, the transformation of the connected, intelligent edge has commenced as on-device intelligence has garnered phenomenal traction. This transformation is critical to leveraging the full potential of 5G's future."

Ceragon Networks recently announced that it is offering a new A.I.-based Intelligence and Management Software Suite called Ceragon Insights which will offer capabilities such as analysis, automating and management of wireless networks. These tools will help their customers to improve network performance, efficiency and troubleshooting. This new software offering could lead to increased recurring revenues for Ceragon Networks.

Upside Catalysts For 2023 And Beyond:

When Ceragon Networks rejected the buyout offer, management offered a number of reasons as to why the offer of just over $3 was not fair value, and why the stock could be valued at much higher levels in the not too distant future. In a statement to shareholders, the company outlined projections for improved margins as well as revenues to reach a range of $325-$345 million in 2023 and then rise to around $500 million annually in the next few years. Improved margins, a reduction in supply chain issues and rising revenues could be strong upside catalysts for this stock. The company stated :

"With the strength of our core business, combined with our new growth initiatives and supply chain normalization, we expect to drive revenue of $325–345 million in the full year 2023, and are targeting revenue of approximately $500 million and gross margins of at least 34–36% within the next five years."

In the Q4 2022 earnings call transcript, the company discussed the plans to launch a new chipset which is expected to drive revenues higher in 2024 and beyond. It stated :

"Throughout 2022, we made significant headway in the productization of our new system on a chip technology, and we are on track and expect to finish productization in 2023 and launch our new product line in 2024. We strongly believe this system on a chip will drive strong demand and have a transformative impact on the industry and on our market share and performance, mainly due to two to three years' time to market advantage we expect to have over our competitors.

When we look into the future, we expect a strong 2023. Given the positive business traction and our operational momentum, we expect to continue our growth in the leading regions we operate in. We anticipate substantial growth coming from our E-band sales, especially with the new coming cost-effective product that enables covering a broader market base. We also expect that our sell-side routing and managed services businesses to increase in 2023 and beyond."

Potential Downside Risks:

When evaluating an investment in any company these days, I want to consider what the impact of a potential recession would be on revenues, and also review the strength of the balance sheet. Because this industry and 5G takes a multi-year investment approach and because communications and connectivity demand remains strong even if the economy weakens, Ceragon Networks appears to be recession-resistant. It has a strong balance sheet with plenty of cash and minimal net debt.

The price you pay for a stock is a key factor in evaluating potential downside risk, and with this stock beaten down to just around $1.70, I believe the downside risk from this level is limited. In fact, buying around this level has historically rewarded investors. Based on this, the biggest potential risk might just be management execution and opportunity cost. For example, if management does not meet earnings estimated for 2023 and 2024, the shares might be stuck in a trading range and below the 52-week high of nearly $3 per share, and the funds invested in this stock might have generated more gains in another tech stock.

In Summary:

Similar to the investments AEHR Test Systems made for years before revenues and its share price surged, Ceragon Networks has been investing for the 5G opportunity and the rewards are now likely to enrich shareholders. This belief seems to be supported by the decision by management to reject a buyout and to remain an independent company. As previously discussed, this view also seems to be supported by Mr. Samberg along with his multi-million dollar investment in this company. I believe this stock has the potential to trade around the $7 level it held in 2021, and possibly go even beyond that level if management delivers. That would provide strong gains for those who take advantage of the opportunity to buy shares which are (in my opinion) trading at a ridiculously low valuation of just around 50% of what a competitor was willing to pay to takeover this company.

The balance sheet is strong, and this company has multiple growth tailwinds including 5G and national security concerns resulting in a ban on Chinese competitors. The price to sales ratio, the price to earnings ratio, 5G/connectivity growth potential and the $3.08 per share buyout offer all suggest that this stock is a bargain at current levels, with major upside potential.

No guarantees or representations are made. Hawkinvest is not a registered investment advisor and does not provide specific investment advice. The information is for informational purposes only. You should always consult a financial advisor.

For further details see:

Ceragon Networks: This $1 Tech Stock Is My Top 'Buy And Hold' Pick