CERE - Cerevel Therapeutics: High Standards And Development Burden Poses Reflexivity Risks

2023-11-02 10:48:54 ET

Summary

- Cerevel Therapeutics is a pre-revenue company focused on developing therapies for several neurological diseases.

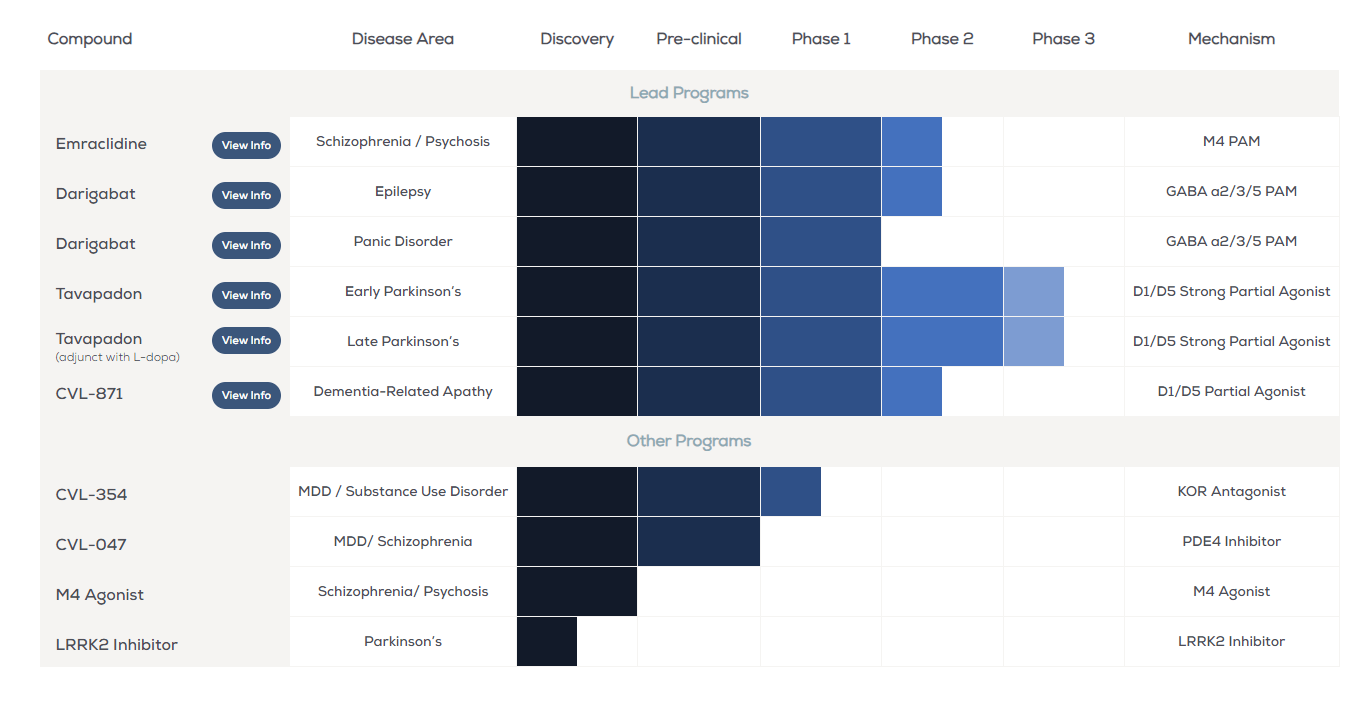

- The company's main products in development include Emraclidine for schizophrenia and psychosis in Alzheimer's disease, Darigabat for epilepsy, Tavapadon for Parkinson's disease, and CVL-871 for dementia-related apathy.

- The company faces a common financial issue, including potential dilution from equity compensation plans and the need for additional funding, making it a highly speculative investment.

- There are many contingencies, and besides being very apparent in the current equity market environment, the risks are difficult to quantify.

- With the market value already in the billions despite outstanding development burdens for treatments that are up against quite high standards of current treatments, there isn't obvious upside.

Cerevel Therapeutics (CERE) is another company that has come into existence from the 2020 and 2021 SPAC merger boom. That means that at a minimum, there is the potential for substantial dilution from equity compensation plans, but in the case of the reflexivity-rife funding environment, of dilution on weak terms also from equity raises. The therapeutic areas that the company delves into are interesting, and we have spoken to people in the field to better understand what is going on, but it is virtually a certainty, admitted even by the company, that CERE will have to go to the markets for more funding. Dilutions affect the margin of safety, and reflexivity makes it unpredictable how badly affected upsides will be. The markets are large, as the burdens of the diseases addressed are large, but therapies already exist and while more coarse than what CERE proposes, they are potent. The situation is difficult to quantify, and the vicious cycles of reflexivity for this company with a large outstanding development burden mean that a slip up by the company would be very costly for today's investors. Very speculative, and there might be easier-to-quantify rare disease options within the space that could take CERE's place in a mad money allocation.

Products and Innovation

Cerevel Therapeutics has a broad spectrum of therapeutic candidates for curing neurological diseases, the most progressed of which are in Phase 2 or 3 of clinical trials, and some of the candidates that are in early stages (discovery phase or phase 1). Our focus today will be main elements, (Emraclidine, Darigabat, Tavapadon and CVL-871), since they can potentially be approved for broad use in the nearer future, although there is still some time to go.

Drugs in Development (Website)

{kind=link}

Emraclidine

Emraclidine is a positive allosteric modulator ((PAM)) for muscarinic receptors type 4 (M4 receptors), which means that Emraclidine affects M4 receptors by changing how they respond to stimuli (since it's a positive modulator it's clear that drugs can increase receptors affinity and efficacy). The drug is potential candidate for treating Schizophrenia as well as psychosis in Alzheimer disease.

But why this therapeutic option potentially better than current options? The main thing is the story about side effects of the currently used drugs. Considering that Schizophrenia is a disease of excessive dopamine in the brain, current therapeutic options are targeting dopamine receptors by directly blocking them. This is linked with many potential side effects that may occur. On the other hand, by targeting M4 receptors (which emraclidine does) they can modulate dopamine levels indirectly, potentially "bypassing" negative effects which are caused by targeting dopamine receptors itself. Although it seems like a good solution, current drugs are apparently quite potent, so the standard is high in this market. This therapy is in phase 2.

Darigabat ,

Before discussing Darigabat , a preamble: in order for our brain to function properly, it's really important that neurons aren't overstimulated. Gamma-aminobutyric acid ((GABA)) has a key role. GABA is the main inhibitory receptor in our central nervous system ((CNS)). Epilepsy and panic disorder are probably first diseases that comes to mind when we are talking about GABA transmission working improperly. We have two main groups of GABA receptors called GABAa and GABAb. GABAa receptors have 5 subunits (subunit 1, 2, 3, 4, 5), and are the one that are mostly targeted by conventional drugs (such as benzodiazepines, barbiturates etc). These drugs are not very selective in their pharmacological effect, which means that they affect all subunits of the GABAa receptor. Some studies are reporting a link with some unfavourable motoric side effects. Benzodiazepines are known for their addictive potential.

Darigabat (company's second product that we are reviewing) is a PAM of GABAa receptors, but targeting only subunits 2, 3 and 5. It's supposed to be more selective and therefore avoid some side effects. Although the company selected this drug for treatment of epilepsy, it is clear that we need some more feedback from clinical trials which are still in phase 2 which we could expect in the first half of next year.

Tavapadon

Next is Parkinson's disease, which is very debilitating. It's a progressive neurodegenerative disorder mainly affecting motor function. Key of the problem is lack of dopamine in motor regions of the brain. Current therapies (L-dopa is the main one) are dealing with it by blocking all of the dopamine receptors, of which we have 5 (from D1 to D5). Again, this non-selective approach leads to developing some CNS side effects such as hallucinations or sedation through the day, since these receptors appear in many regions of the brain are not only involved in motoric function.

Tavapadon for Parkinson's selectively binds to D1 and D5 dopamine receptors thereby avoiding appearance of potential side effects. Another potential benefit is in avoiding overexcitation and a refractory period (period in which receptors are not able to be stimulated).

This is another great idea and another promising opportunity, but as we said previously, from medical perspective we need to see reports from clinical trials in the second half of 2024, although this one is more progressed and is in indications for both early and late stage Parkinson's in phase 3.

CVL-871

Last drug for this report from their pipeline is CVL-871 as a therapy for Dementia-Related Apathy. It has the same mechanism of action as Tavapadon (D1/D5 receptor activator) and the main difference is in how strong it binds to the receptor. Basically, slight pharmacological differences from Tavapadon and for a different indication.

Financial Comments

With companies like these, there are a lot of financial considerations. Firstly, there are quite a lot of shares that could be issued associated with both convertible notes and equity compensation plans, thereby putting a minimum in terms of dilution at around 20% assuming those options and conversions are exercised. Furthermore, reflexivity is a dangerous phenomenon for all companies that depend on the value of their stock to raise capital. If prices of these stocks go down, the fundamentals of the business are actually affected, and reflexivity describes this vicious cycle that can easily be triggered in a weak funding environment that we have today, punctuated by a total collapse in SPAC activity but even in more traditional activity like IPOs .

The cash burn of the company is not insubstantial. Current run-rates of cash burn give the company about 2-3 years before they have to go to markets again. Moreover, in the risk sections, the company acknowledges in no uncertain terms that it will have to go to market to secure funding.

The question is when do their phase 3 drugs possibly hit the market, and are those markets vigorous enough to limit the extent of the fundraising needed if they are able to come online in time?

Beginning with Parkinson's, the burden is in the $50 billion zone for the US in terms of direct and indirect costs. These are the phase 3 drugs. The phase 2 drugs for epilepsy and schizophrenia are $343 billion including indirect costs, which are worth including in terms of evaluating value capture possibilities, and $62 billion in direct costs . Epilepsy is over $100 billion . The markets are big at over $200 billion for these products up for value capture, but they are also addressed already by a range of existing therapies, and Cerevel is making incremental improvements. The company is worth $4 billion, so the size of the markets are not lost on investors.

In terms of timelines, there will be some important readouts next year. Given that cash burn has really ramped up this year, and that it can survive at these levels for another couple of years, it is pretty likely that some real steps are taken towards approval before the cash is clean out. We always use the $2.3 billion benchmark for how expensive it is to develop a completed drug. They are over halfway for some key drugs with big markets, as due to the intensity of later phases, phase 3 tends to be some steps past the halfway mark. However, the company has lots of drugs in earlier stages that are going to continue to require funding. It is not going to be possible even for drugs crossing the finishing line in time or at all to offset the capital needs of the business to stop the other trials from dying out. It would not be good if the younger trials were scrapped - we've seen that unfortunately happen with some SPAC merged pharma development companies. Furthermore, it is possible approvals don't come in time to get some revenues, and also there is a risk that they don't come in at all due to a failure in the trials.

In other words, as said in the risk factors in the 10-K, a capital raise will be needed at the very least for the outstanding clinical trials to be brough forward, and whether debt or equity, it will be expensive, although at least debt doesn't have the reflexivity issue to be concerned about. Moreover, while the markets are big, they are not open seas and there will be a fight ahead of them to disseminate knowledge about their therapies. Finally, there is always the dilution issues that hang as a Sword of Damocles over investor returns. With 20% dilution from compensation plans, and with potentially much greater dilution from capital raising needs depending on where the price is, which is exposed to reflexivity risks, the imputed valuation could be multiples of the current market cap - it's impossible to say how large the multiple is because we don't know what the price of the stock will be in the next equity raise, if an equity raise is needed over debt. Supposing markets of around $50 billion to be conservative for just the Parkinson's therapies, and considering the binary nature of clinical stage biopharma bets, even a quite small dilution multiple on the $4 billion market cap gets you close to the TAM for Parkinson's pretty quickly. The Parkinson's therapies may be completed on current liquidity, but it will probably cost more than $1.5 billion to bring to a conclusion each of the phase 2 trial drugs, and there are 4. Then the even earlier stage therapies will cost closer to $2 billion, and there are 4 of those. With the other drugs adding quite a bit more TAM, maybe up to $200 billion, investors might be satisfied with the current valuation, but there could be more than a $12 billion outstanding clinical investment for Cerevel, and we don't know how it will be paid for - possibly reflexively with a deteriorating stock. If the phase 3 drugs don't get approved and ramp quickly, on top of 20% equity plan dilutions, there is more than a 75% dilution from financing the rest of the trials at current stock prices, which will deteriorate as dilution risks becomes more apparent. Dilution from ESPs as well as funding requirements of what is obtainable from those ambitious TAMs brings down the upside quite quickly, and there are still risks that investors lose possibly all their money if something goes wrong in a major trial, and they are up against potent drugs as an existing standard.

There are many contingencies, and they cannot be accurately modeled. Reflexivity must be taken seriously, and CERE is highly speculative in the current market. If we were to speculate, we might prefer rare disease therapies because at least obtainable markets are easier to quantify since there won't be as many existing therapies ensconced in markets.

For further details see:

Cerevel Therapeutics: High Standards And Development Burden Poses Reflexivity Risks