FOUR - CHI: Nice Assets But High Valuation Given The Risks Of A Distribution Cut

2023-11-08 14:40:59 ET

Summary

- Calamos Convertible Opportunities and Income Fund offers a high level of current income with an 11.12% current yield.

- The CHI closed-end fund focuses on investing in convertible securities, which provide stable income and upside potential.

- The fund has delivered a 3.98% total return year-to-date, outperforming many other closed-end funds and the bond index.

- The CHI fund failed to cover its distribution during the most recent 18 months for which we have data, which is very concerning.

- The fund's valuation is incredibly high right now, which greatly reduces its appeal when combined with the challenging finances.

The Calamos Convertible Opportunities and Income Fund ( CHI ) is a closed-end fund, or CEF, that investors can use in order to achieve a very high level of current income from the assets in their portfolios. This is evident in the fact that this fund has an 11.12% current yield today. This is relatively in line with many other closed-end funds, as the current high-yield environment has resulted in the yields offered by these entities being pushed up to very high levels.

This fund is somewhat more interesting than many other closed-end funds though because it focuses its efforts on investing in convertible securities, which can be very hard to get ahold of compared to ordinary stocks and bonds. This is a shame because these securities may be some of the best things in the market for income-focused investors to own. This is because convertible securities provide the stable and secure income of bonds while still boasting the upside potential of common stocks. As many of these companies are issued by start-ups or financially distressed companies, the upside potential can be quite enormous if the company manages to succeed. This is one of the few funds that invests in these securities, so including it in your portfolio could be an attractive proposition if only to gain exposure to the total return potential of these securities.

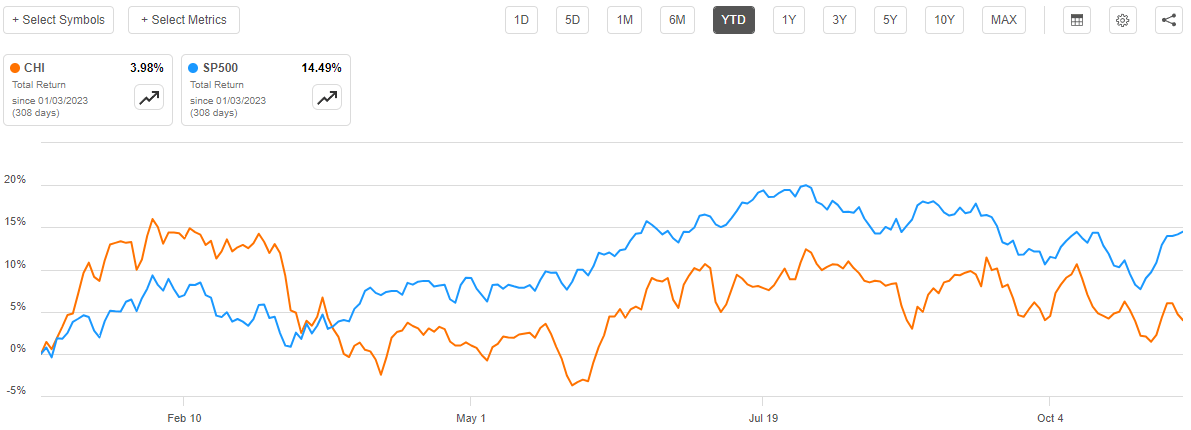

As regular readers may recall, I have discussed a few Calamos funds in the past. The funds offered by this fund house tend to be somewhat similar, as they all provide exposure to securities that are otherwise difficult to acquire. However, I have never discussed this particular fund. This is a major oversight on my part, as this fund has actually delivered a decent performance so far this year. As we can see here, the Calamos Convertible Opportunities and Income Fund has delivered a 3.98% total return year-to-date, which is disappointing compared to the S&P 500 Index ( SP500 ) but it is still better than many other closed-end funds have managed:

{kind=link}

It is important to note that the above chart shows the return that investors receive once the dividend is taken into account. The fund's shares alone are actually down 3.76% year-to-date. This just shows the importance of the fund's high yield as investors in this fund still managed to make money this year despite the shares declining in price. With that said though, the fund has still underperformed a money market fund over the same period.

Let us investigate and see if buying this fund makes any sense today.

About The Fund

According to the fund's website , the Calamos Convertible Opportunities and Income Fund has the primary objective of providing its investors with a high level of total return. Specifically, the website states:

The Fund seeks total return through capital appreciation and current income by investing in a diversified portfolio of convertible securities and high-yield corporate bonds.

Convertible securities are basically just preferred stock or bonds that can be converted into shares of common stock when certain conditions are met. Ordinarily, a fund that invests in securities like this would be expected to have an objective of the provision of income. After all, bonds have no net capital gains over their lifetimes. I have discussed this in a number of previous articles. This fund is somewhat different though, because it is investing in convertible securities. In fact, 63.23% of the fund's portfolio is invested in convertible securities:

CEF Connect

Convertible securities can provide significant upside when the issuing company enjoys some success. After all, many of these securities are issued by start-up companies or financially distressed companies that may have difficulty obtaining debt financing at a reasonable price. As such, their balance sheets are usually very weak, and their stock price is pretty beaten down as a result. For example, Tesla, Inc. ( TSLA ) issued convertible securities in its early days, and Ford Motor Company ( F ) issued them back when the 2008 Financial Crisis was threatening to bring down all of the major automakers. Once their fortunes improved, both of these companies delivered very a strong performance in the stock market. Holders of the convertible securities issued by these companies benefited from these stock market runs too because their bonds could be converted into common stock. Total return is the combination of direct payments made to investors and capital gains, so it makes sense for this fund to be targeting capital gains.

A look at the fund's portfolio does indeed reveal that it contains a significant number of securities issued by start-up companies, which is exactly what we would expect for a convertible bond fund:

{kind=link}

Ford Motor Company is certainly not a start-up, but as mentioned it issued some of these securities when the auto industry encountered severe financial stress about fifteen years ago. Ford weathered that crisis better than many of its peers. In fact, I remember seeing numerous articles in the financial media around that time that basically stated that the company's financial strength relative to its peers came from the fact that it had a lot of cash due to newly issued debt. One of the reasons for this is the convertible bonds that the company was issuing around that time, as this Wall Street Journal article points out.

The remainder of these companies are generally younger ones. We can see that here:

| Company |

| Founding Year |

| Uber Technologies, Inc. ( UBER ) |

| 2009 |

| ON Semiconductor Corporation ( ON ) |

| 1999 |

| DexCom, Inc. ( DXCM ) |

| 1999 |

| PPL Capital Funding |

| N/A - Subsidiary of PPL Corporation ( PPL ) |

| Palo Alto Networks, Inc. ( PANW ) |

| 2005 |

| Vail Resorts, Inc. ( MTN ) |

| 1997 |

| Wayfair Inc. ( W ) |

| 2002 |

| Shift4 Payments, Inc. ( FOUR ) |

| 1999 |

| Sea Limited ( SE ) |

| 2009 |

Some readers may point out that many of these companies date back to the late 1990s, which was about 25 years ago. However, that is not very long in the business world. After all, Uber Technologies was founded in 2009 but did not conduct its initial public offering until 2019. Thus, some of these companies are newer to the market than their founding year may suggest. In addition, it is important to keep in mind that some bonds have thirty-year terms, which means that a bond issued back in 1993 could still be trading today. The basic point though is that many of these securities are issued by young companies that may not have sufficient cash flows to obtain funding through normal methods, so they need to offer the conversion feature in order to convince anyone to lend money to them at an affordable price.

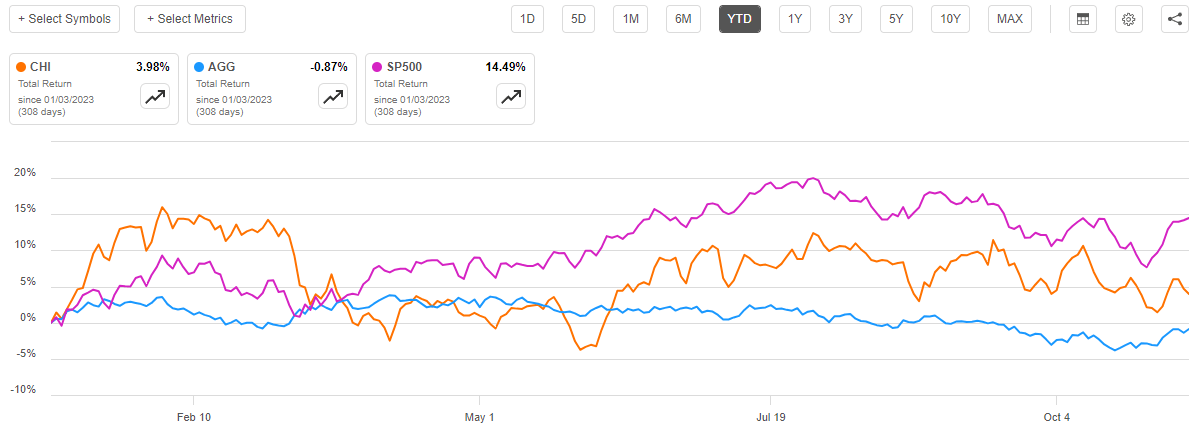

As a result of the conversion feature, many of the securities in this fund will not trade like ordinary bonds. After all, if the common stock of the issuing company goes up then the conversion feature becomes more valuable regardless of what interest rates are doing. The value of this conversion feature needs to be included in the price calculations. This is almost certainly one reason why this fund has substantially outperformed the Bloomberg U.S. Aggregate Bond Index year-to-date:

{kind=link}

We can see that the fund's performance correlates at least somewhat with the S&P 500 Index despite many of the securities technically being bonds. This is due to the conversion feature possessed by the bonds in the portfolio. However, it is unlikely that it will actually outperform common stocks during a reasonably strong bull market. After all, convertibles are still lower risk than common stocks and an integral rule of finance is that higher risk translates to higher rewards. However, the fact that these securities provide a payment to investors should result in them outperforming common equities during a bear market. That is actually not really a bad deal for a risk-averse investor who is seeking a high level of income and lower volatility than could be obtained in common stocks without having to sacrifice all the upside potential offered by equities.

A look at the largest positions in the fund's portfolio may make someone assume that this fund is heavily weighted toward the technology sector. After all, we can see that several of the companies that are on the list are technology firms, and technology is one of the most popular sectors for start-up firms. As already mentioned, start-up firms are one of the largest issuers of convertible securities. However, only 18.9% of the fund's assets are invested in technology firms right now:

Calamos Investments

This is significantly less than the 28.75% weighting of the technology sector in the S&P 500 Index. In fact, this fund is much more balanced than the index. Here are the sector weightings of the S&P 500 Index:

State Street

The fact that this fund is more balanced could also prove quite attractive to some investors. After all, the Calamos Convertible Opportunities and Income Fund will be less impacted by sector-specific problems than the broader index. For example, the consumer discretionary sector is far more impacted by recessions than utilities or consumer staples. There are some signs that the American economy could enter into a recession next year. In fact, this is one of the reasons why the market went up so much last week, as investors began to expect a near-term recession that would force the Federal Reserve to cut rates.

Unfortunately, we can see that the Calamos Convertible Opportunities and Income Fund has somewhat limited exposure to recession-resistant sectors like utilities. This is at least partly because these sectors do not issue convertible securities heavily since they have sufficiently strong cash flows to obtain funding with traditional bonds and do not need to offer the conversion feature to attract investor dollars. Fortunately, the fact that this fund is investing in debt securities should protect it somewhat from a recession. After all, the companies that issue these securities still need to make their required payments or fall into default. Most companies want to avoid defaults, so they will probably not just randomly skip paying interest on their debt. This is much better than a common stock, which will almost certainly decline if the company's financial performance deteriorates.

As already mentioned though, most of the companies that issue convertible securities have either limited cash flow or are experiencing financial distress for some reason. The fund's website also explicitly states that it invests in both convertible securities and junk bonds. As such, we can expect that many of the securities that are represented in this portfolio will have below investment-grade ratings. That is certainly the case, as we can see here:

Calamos Investments

An investment-grade security is anything rated BBB or higher. As we can see, that only describes 12.8% of the portfolio's assets. The rest of the portfolio is invested in junk-rated securities. This is something that may concern more conservative investors, such as many retirees, who generally want to preserve their principal. Fortunately, this fund appears to be reasonably diversified to avoid too much in the way of losses due to defaults. As we already saw, the largest position in the portfolio is only 1.6% of the fund's net assets. This fund also has 610 issuers represented throughout the portfolio. As such, any default should have a negligible impact on the fund's total assets. We probably will not even notice the default in the fund's share price or portfolio performance. Thus, we probably do not have to worry about default risk too much, unless there is a situation where mass defaults occur throughout the American economy. In such a situation, pretty much everything except for cash is going to hand large losses to investors and we will have bigger problems than just this fund.

Leverage

As is the case with most closed-end funds, the Calamos Convertible Opportunities and Income Fund employs leverage as a method of boosting its total returns beyond those provided by the securities in the fund. I explained how this works in numerous previous articles. To paraphrase myself:

Basically, the fund borrows money and then uses that borrowed money to purchase convertible securities and high-yield junk bonds. As long as the purchased securities deliver a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.

However, it is important to note that leverage is not as effective at boosting returns today as it was two years ago. This is because interest rates are significantly higher today and the difference between the rate at which the fund can borrow and the yield that it can receive on the purchased securities is narrower than it was two years ago.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because this would expose us to an undesirable amount of risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Calamos Convertible Opportunities and Income Fund has levered assets comprising 39.25% of the portfolio. That is quite a bit higher than the one-third level that we really want to see. With that said, the fact that this fund is investing mostly in convertibles and high-yield bonds allows it to carry a higher level of debt than a common equity fund could. This is because these securities are generally less volatile than common equity. I would certainly prefer to see the fund's leverage be lower, though. This is especially true in today's high-interest-rate world, although fortunately the securities that the fund purchases will generally have a higher yield than the interest rate that the fund has to pay on the money that it borrows to purchase them.

Distribution Analysis

As mentioned earlier in this article, the Calamos Convertible Opportunities and Income Fund has the primary objective of providing its investors with a very high level of total return. However, that objective is only because of the conversion feature on many of the securities that it provides. Aside from the potential capital gains from that feature, this is just an ordinary fixed-income fund that provides its investors with income. Many of the securities in which this fund invests are high-yield speculative-grade bonds, which have much higher yields than investment-grade securities. This fund collects the payments that it receives from these securities and then distributes the money to its shareholders, net of its own expenses. As such, we can expect that this fund would have a very high yield itself.

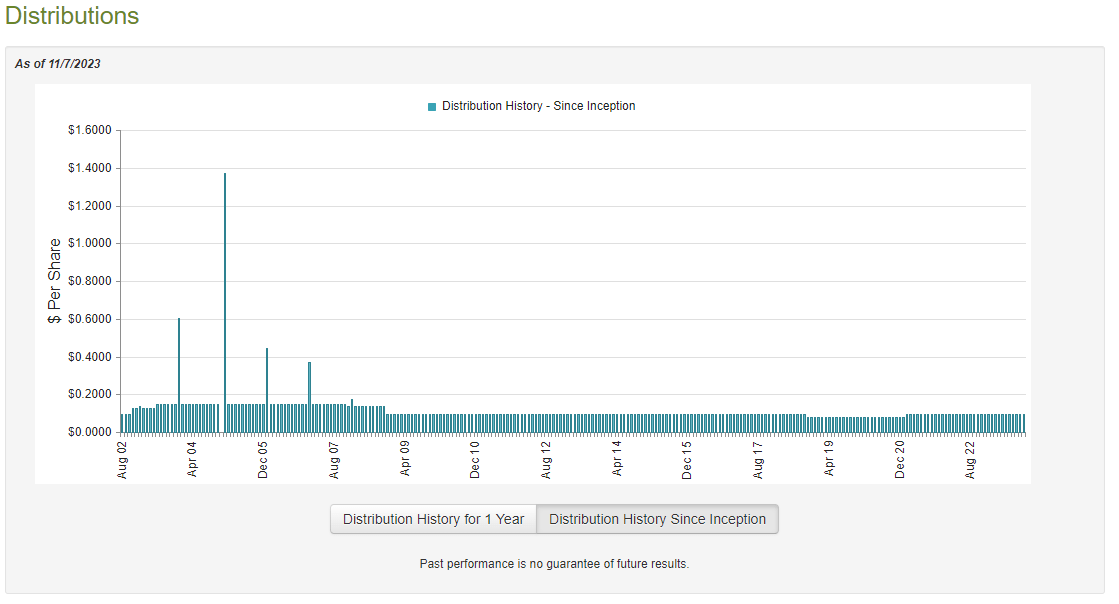

This is certainly the case. The Calamos Convertible Opportunities and Income Fund pays a monthly distribution of $0.0949 per share ($1.1388 per share annually), which gives it an 11.12% yield at the current price. That is certainly a respectable distribution that gives this fund a substantially higher yield than just about any index fund or common stock in the market. The fund has also been reasonably consistent with respect to its distribution over the years. However, it has not been perfect:

{kind=link}

For the most part, we can see that the fund was very consistent with respect to its distribution except for in 2019 and 2020. Otherwise, the fund has paid a $0.0950 per share monthly distribution consistently. While it did technically reduce its distribution in the most recent month, it was only by $0.0001 per share so it is unlikely that anyone will notice unless they own an enormous number of shares. For the most part, this distribution history will probably appeal to anyone who is seeking to generate a safe and secure level of income from the investments in their portfolios.

As is always the case, it is very important that we have a look at the fund's finances and determine how sustainable its distribution actually is. After all, very few funds that invest in interest-rate-sensitive securities have been able to deliver a performance that is as stable as this one. Thus, we want to see how it is able to accomplish a feat that its peers have not.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on April 30, 2023. This period was a very interesting one for the market. The last two months of last year were generally weak as rising rates were weighing on the markets and generally driving investors out of common stocks and many bonds and into cash. That pushed down asset prices during November and December, but things turned around in a big way after the New Year. During the first few months of this year, we saw a bubble form in artificial intelligence stocks that eventually spread to the rest of the market. This pushed down yields as well, as some market participants were optimistic that near-term rate cuts were imminent. That may have given this fund some potential to earn capital gains, and this report will show how successful it was at that task.

During the six-month period, the Calamos Convertible Opportunities and Income Fund received $15,656,339 in interest and $2,936,397 in dividends from the assets in its portfolio. However, some of the interest payments were considered a return of principal and are not considered to be interest income for tax purposes. As such, this fund only reported a total investment income of $14,027,383 during the period. This was not enough to cover the fund's expenses, and it ended up reporting a net investment loss of $1,139,421 during the period. That is concerning as the fund very obviously did not have sufficient net investment income to cover its distributions. However, it still paid $42,306,819 to its shareholders over the period.

However, the fund does have other methods through which it can obtain money to distribute to its investors. For example, exercising the conversion feature on some of the securities can give the fund substantial capital gains that can be paid out. In addition, the fund might have simply been able to generate capital gains by exploiting price changes of the securities in the portfolio. It had somewhat mixed results at this over the period. The fund reported net realized gains of $47,408,075 but these were partially offset by $27,399,389 net unrealized losses over the period. Overall, the fund's assets declined by $19,710,218 during the period after accounting for all inflows and outflows. Thus, the fund failed to cover its distribution during this six-month period.

The fund also failed to cover its distribution during the previous full-year period. During the full-year period that ended on October 31, 2022, the fund had a net investment income of $714,868 and net realized gains of $66,657,732. That was nowhere close to enough to cover the $82,919,043 that it paid out over the period. The fund had net unrealized losses during that full-year period as well, so its net assets declined over the course of that year.

Overall, it appears that this fund cannot sustain its distribution at the present time, and it may ultimately be forced to cut the payout.

Valuation

As of November 7, 2023 (the most recent date for which data is currently available), the Calamos Convertible Opportunities and Income Fund has a net asset value of $9.29 per share. The shares currently trade for $10.31 each. This gives the fund's shares a 10.98% premium on net asset value. That is an incredibly high price to pay for any fund, although it is not as bad as the 11.12% premium that the shares have averaged over the past month. Thus, investors really have to pay through the nose to get this fund, and that makes it difficult to justify a purchase right now.

Conclusion

In conclusion, convertible securities have a lot to offer investors as they provide a way to receive the high yields that accompany fixed-income securities without having to sacrifice the potential upside inherent in common stocks. The Calamos Convertible Opportunities and Income Fund is one of the few ways to gain exposure to these securities and as such it is fairly attractive. The fund's diversity is also quite attractive, as it is somewhat better balanced than the S&P 500 Index. Unfortunately, the fund appears to be unable to generate sufficient investment profits to cover its distribution as it has failed to accomplish this task for eighteen months. That could be a sign that the fund will need to cut its distribution in the near future. When we combine this with an incredibly high valuation, it may be best to look elsewhere to gain exposure to convertible securities.

For further details see:

CHI: Nice Assets, But High Valuation Given The Risks Of A Distribution Cut