CHI - CHI: Not A Bargain Yet Even After Premium Drop

2023-04-22 00:32:54 ET

Summary

- CHI's premium has come down recently, but it still isn't at a point where I'd be looking to buy.

- The fund's distribution remains elevated, and despite that, Calamos has chosen not to cut the distribution.

- A distribution cut, if it happens, could potentially provide the catalyst for an opportunity to reenter this fund.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on April 20th, 2023.

Earlier in January 2023, I sold off my position in Calamos Convertible Opportunities and Income Fund ( CHI ). The fund's premium ran up to double-digit levels, and even while I try to be a buy-and-hold type investor for most of my positions, at some point, even I sell. Being a closed-end fund investor, it's easy to let valuations guide our investing because premiums/discounts often present clear signals when something is over or undervalued.

In the case of CHI, the fund's premium has dropped back down to more attractive levels. At the same time, it still isn't quite the bargain yet, and it still trades over its historical trading valuation. However, it also isn't necessarily overvalued anymore either. I still believe that the double-digit yield, while certainly attractive, should still be watched for a potential cut. Avoiding a cut would take the overall market and fund to continue recovering from the lows we saw in 2022, as they require significant capital gains to fund their distributions.

The Basics

- 1-Year Z-score: -0.16

- Premium: 6.16%

- Distribution Yield: 10.66%

- Expense Ratio: 1.34%

- Leverage: 37.24%

- Managed Assets: $1.201 billion

- Structure: Perpetual

CHI states its objective as "seeks total return through capital appreciation and current income by investing in a diversified portfolio of convertible securities and high yield corporate bonds." This is fairly straightforward but can also be beneficial to retail investors.

The fund's total expense ratio, with the leverage costs, has risen to 2.44% in the latest annual report . That's an increase from the prior fiscal year end of 1.83%. The main culprit is the higher interest rates costs brought on by the Fed raising interest rates. Their fiscal year-end is October, so since then, we've seen costs rise even further.

The largest form of leverage they have is through a credit facility that pays at a rate of OBFR plus 0.80%. At fiscal year-end, the interest rate was 3.86%. However, OBFR is now at 4.82% at the last check ; adding the spread and we would see that interest rates on this form of leverage come to around 5.62% now.

To help soften some of this blow from higher interest costs would be their fixed-rate mandatory redeemable preferred shares they have outstanding.

{kind=link}

At the end of their fiscal year, they had $339.4 million drawn on their credit agreement. Today, they've deleveraged a bit to $314.4 million. It isn't clear if it was a forced deleveraging due to asset prices dropping or an effort to self-regulate their excess leverage, as the effective leverage ratio would have been over 40%, as we saw it was earlier in 2022 . In fact, it's worth noting that in that earlier 2022 update, they were showing $399.4 million withdrawn on this agreement.

Either way, less leverage would mean that the earnings potential of the fund is reduced. At the same time, when leverage costs are higher than your coupons collected on your underlying portfolio, it can make sense to deleverage.

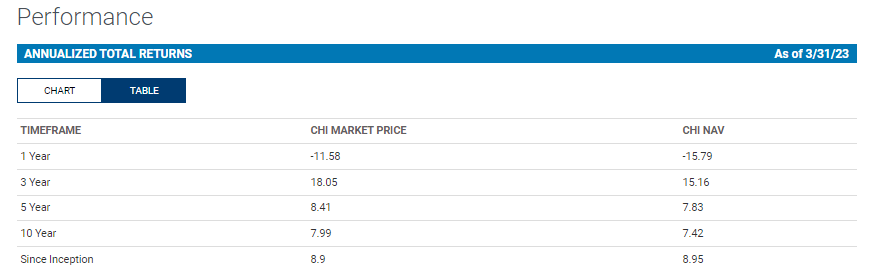

Performance - Premium Keeps Me At A "Hold"

Historically, the fund had delivered fairly attractive results. Of course, the bull market would have helped their portfolio's convertible side. It also meant their portfolio's high yield side benefited from easy money conditions throughout most of the last decade. That environment has changed, and that's kind of the whole point of why we saw the bear market we did in 2022.

{kind=link}

The actual benchmark of CHI would be a mixture between convertibles, high-yield bonds and even some narrower allocations to bank loans. However, the overwhelming majority of the fund is split between convertibles and high-yield bonds. Those two security types make up nearly 91% of the fund. Below is a comparison between CHI and the iShares Convertible Bond ETF ( ICVT ) and the iShares iBoxx High Yield Corporate Bond ETF ( HYG ) to provide some color on the comparison of how CHI performed.

As expected, it is somewhere in the middle. With the added leverage for CHI and the premium/discounts, we can see that more recently is when the total price return results for CHI started to decline relative to IVT.

Ycharts

Worth pointing out is that the chart for CHI on a total NAV return basis, what its actual underlying portfolio is doing, seems to track ICVT closer. This makes sense, as almost 66% of CHI was last reported as convertibles. At the same time, coming out of the Covid pandemic, it would appear that the high yield component was a drag on CHI's results. So the added leverage of the portfolio was taken relatively lower due to positioning here, as well as a higher expense ratio that it had to overcome.

I don't think that makes it a bad fund, but perhaps some investors would have thought that it would have been more competitive with ICVT. Of course, if you are looking for higher payouts, an investor would naturally gravitate towards CHI over ICVT due to a difference in monthly payouts.

Additionally, where I think we can exploit CEFs, is with discounts/premiums. Ultimately, that's where CHI remains a "hold" for me. The fund's premium had come down from where we were in January when I sold it, but the fund is still historically overvalued.

One could even suggest with some logic that a slightly larger discount from where this average is even could be more appropriate. Interest rates are higher, so at this point, leverage is costing the fund more than they are earning in some cases. Thus, a deeper discount could be reasonable.

Ycharts

With that, waiting for a 5 to 10% discount before picking up shares could make a lot of sense if you want to get a "good" deal, in my opinion.

What I ended up doing when I sold CHI was to make my Ellsworth Growth and Income Fund ( ECF ) position even larger. That was on January 23rd, 2023. Neither fund had provided any sort of great performance since that time. However, ECF was able to come out on top in terms of total share price return. That was even despite ECF even seeing its discount expand even further. On top of that, ECF saw its total NAV return deliver a slightly lower return too.

Ycharts

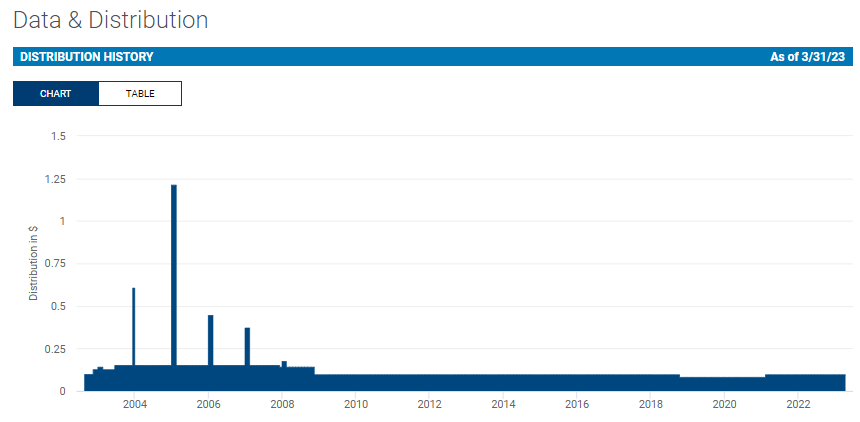

Distribution - Some Caution

Calamos has shown a hesitancy to cut their funds distributions in the past. Instead, they try their best to remain patient and hope for the best. That's certainly valiant, but it isn't always the best course of action. Although that's subjective, and some investors would say they prefer for funds to continue holding steady even when unsustainable.

{kind=link}

Unfortunately, when a distribution cut is put into place in these cases when a fund is at a higher premium, it can mean more damage than usual. While the fund's premium has come down, should they decide to cut (which is complete speculation on my part), we could see the fund's premium turn to a discount.

That's a good thing for an investor sitting on the sidelines like me, but it could be frustrating for investors already holding the fund and seeing their values drop. Of course, a truly dedicated income investor would see it as an opportunity to add to their positions and not be bothered by short-term noise.

Above, I touched on the fund deleveraged throughout the last year to keep their leverage ratio at appropriate levels. Since the fund's underlying portfolio is mostly fixed and low-yielding instruments, the higher interest rates meant higher leverage costs.

At the same time, the yield in their portfolio wasn't rising. So the leverage reduction means less potential earnings, but it also could have been the better of the two evils since higher leverage that isn't being covered by the yields on the underlying portfolio would be costing the fund anyway.

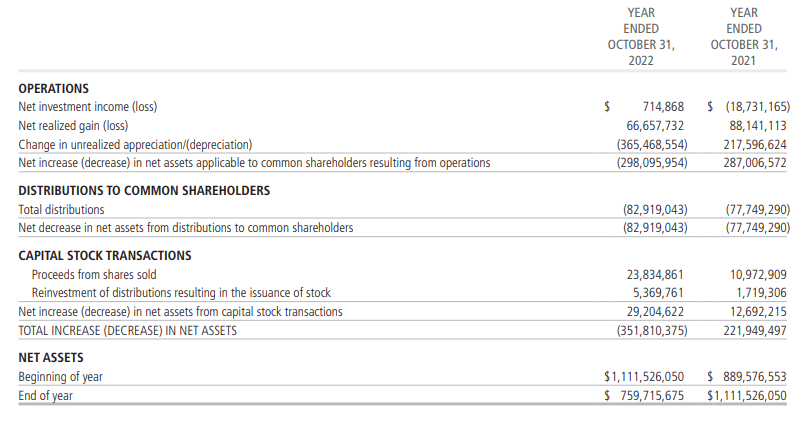

With both of those factors, we would expect to see the fund's net investment income drop year-over-year.

{kind=link}

In this case, we don't. We see it has raised substantially instead from a deep negative number to a slightly positive ~$715k. At this point, one might be wondering what the heck is going on if you aren't following this fund closely. Well, we have more noise for this fund as amortization reduces total investment income.

{kind=link}

Adding amortization back into the fund's NII gives us $11.836 million. That works out to NII coverage of 14.27%. Therefore, you see why capital gains become so necessary for this fund's distribution. Worth noting is that they had some contributions to the realized capital gains pool from writing options.

The fund's amortization last year was even higher. When factoring that in, last year's NII would have been $15.696 million. So that gives us what we would expect to see, declining NII year-over-year. That's even despite the fund being able to issue more shares due to trading at premiums, which is accretive and positive for investors.

This details why I believe that a distribution cut may be necessary.

But let's look at it more simply from another angle. The fund's NAV distribution rate is 11.32%. They need to earn at least that and the fund's expense ratio in order for the fund to have its distribution technically covered.

While I would never say that is impossible - especially after a bear market year when we are already seeing some promising signs of rebounding - it is at a level where it does appear to be an improbable level to achieve going forward. If the Fed cuts rates, that could help ease the leverage costs and produce higher NII for the fund.

For tax purposes, most of last year's distribution was classified as long-term capital gains. However, in prior years it was mostly ordinary income. So this is one fund to keep an eye on (or avoid) if you are a tax-sensitive investor wanting to put this in a taxable account.

{kind=link}

CHI's Portfolio

Turnover for the fund is fairly moderate, with the prior year showing a turnover rate of 39%. That being said, the fund's main weightings stay relatively similar from update to update.

CHI Asset Allocation (Calamos)

The ~66% convertible weighting is right around what we've seen in each of the last two previous updates. The fund's weighted average duration came to 2.6 years as of March 31st, 2023. That, too, is exactly where we saw it one year ago. Meaning that overall the portfolio isn't too sensitive to interest rate changes in terms of its underlying portfolio, at least not directly.

However, being that convertibles are often issued by more growth-oriented companies that are viewed as 'longer duration' assets, that can have an indirect impact. If tech/growth stocks are taking a hit, their convertible bond prices will also take a hit as it becomes less attractive to hold the bonds for conversion. The benefit of convertible bonds is that they eventually have the floor and, barring bankruptcy, should receive face value at maturity.

The tech composition of the fund has come down, but it remains the largest sector.

CHI Sector Allocation (Calamos)

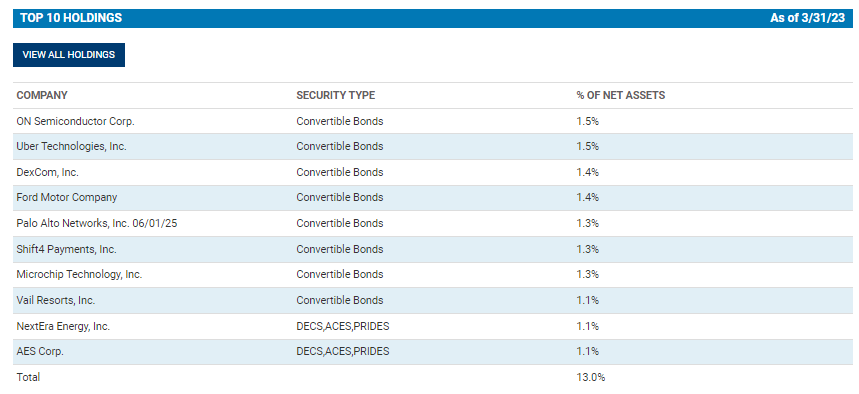

Perhaps unsurprisingly, then, when taking a look at the top ten, we see plenty of tech companies listed. Still, we can also see that the overall weighting of each position is relatively slim. That helps to add to the diversification of the fund as it isn't any one or two companies that can really have a meaningful impact. CEFConnect shows that CHI has 600 total holdings.

{kind=link}

To tie in our discussion of leverage throughout this article and highlight why leverage is costing more than the fund can earn in terms of income, let's take a look at some of the yields these are paying. Remember, their leverage costs are now pushing closer to 6%.

The largest weighting here is the ON Semiconductor Corp's ( ON ) 3.875% convertible. Uber Technologies ( UBER ) is a zero coupon bond with a principal value of $20 million, while at the end of October, it was valued at $16.537 million. The DexCom ( DXCM ) convertible here pays 0.25%, and the Ford Motor Company ( F ) convertible is also a zero coupon bond that had a face value of $16.75 million with a value of $16.93 million.

To be fair, CHI holds some Ford bond exposure that pays between 2.9% and 6.1%. Also, the fixed-rate debt is between 2.68% and 4%. Still, some of the yields the fund is receiving are still below the yields they are paying on the leverage.

CHI Ford Bond Holdings (Calamos)

The problem is, if the fund sells off these assets and we get a rebound, they wouldn't participate. In the above, we can see that on the left of the security listed is the face value and on the right. Here's an example looking at the 6.1% bond they hold, which has a face value of $1 million, but it was only valued at $917k. That means they will or should see that face value paid out at maturity. Should rates drop, we could see the value rise, so that's what they'd give up if they sold off these lower-yielding instruments, the opportunity to participate in the upside that comes from lower rates when they happen.

That's basically the overall problem of all leveraged CEFs at the moment, in general. At least those that aren't hedged through derivatives or fixed-rate financing.

However, it then goes back to the whole theme that CHI is at a premium. You may be buying a basket of discounted bonds at the moment, but you are paying a premium to do so. That cancels out some of the benefits.

Conclusion

CHI continues to trade at a premium, but it did come down from a recent spike in the fund's premium. Despite our uncertain environment, the fund continues to trade at a fairly lofty level, even compared to its history. Therefore, I will continue to wait on the sidelines and view CHI as a "hold" for now.

For further details see:

CHI: Not A Bargain Yet, Even After Premium Drop