KBND - China: September Inflation Flirting With Disinflation Again

2023-10-13 05:45:00 ET

Summary

- September's inflation data remind us that despite some firming in activity indicators recently, China's economic recovery remains challenged, and is perhaps behind recent rumours of a slightly more accommodative approach to central government deficits.

- One month does not constitute a trend, however, and the base effect story, which we believe will slowly lift Chinese inflation over the coming months, is still in play.

- Even with the sort of improvement we are anticipating, full-year inflation will likely only just push above 1% in 2024, up from our forecast of 0.5% CPI inflation for full-year 2023.

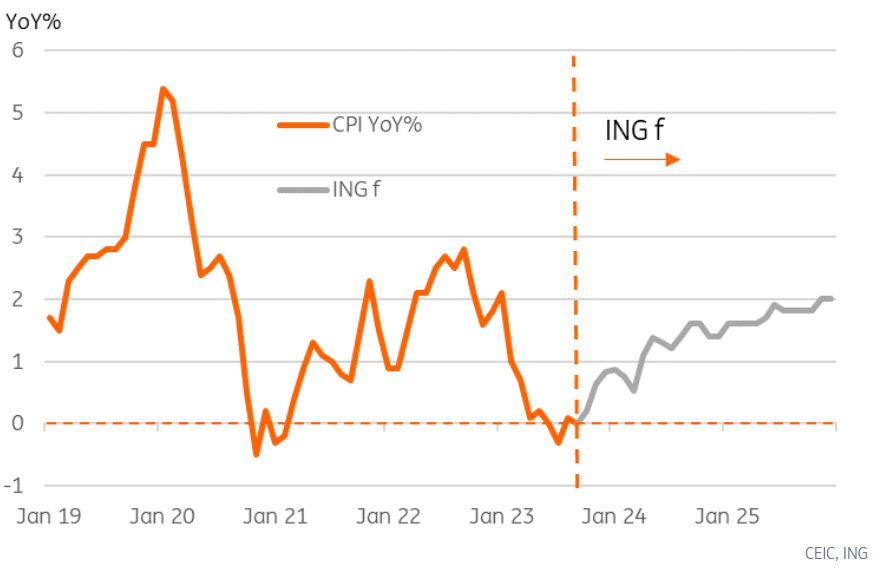

CPI flirts with disinflation again

After a brief spell in negative territory in July, China's August inflation data pulled itself back to a positive setting, though only just (0.1% YoY). We and the market were expecting this slight improvement to continue in September. Instead, the September inflation rate has fallen back to 0% YoY, and according to our calculations, this implies a small (0.1pp) decline in the underlying price level. That itself is quite disappointing because those same calculations showed that in the previous couple of months, most of the decline in inflation was due to the run-off of earlier food price shocks. The underlying run-rate of inflation back then remained encouragingly positive.

One month does not constitute a trend, however, and the base effect story, which we believe will slowly lift Chinese inflation over the coming months, is still in play. However, if the underlying run rate is softer even than the conservative figures we are pencilling in, then this may be a much more nuanced improvement.

China CPI inflation (YoY%)

{kind=link}

No room for monetary support, so maybe fiscal policy to be loosened?

Even with the sort of improvement we are anticipating, full-year inflation will likely only just push above 1% in 2024, up from our forecast of 0.5% CPI inflation for full-year 2023.

And it's not just CPI inflation where we see weakness. The PPI inflation data released today also undershot expectations, though at -2.5% YoY, they did at least improve on the -3.0% PPI inflation recorded in August. This may presage some slight improvement in industrial profit growth, which was still down 11.7% YtD YoY% in August.

Next week, we have the 1Y medium-term lending facility rate decision. But with the PBoC engaged in a daily struggle to keep the CNY from depreciating, we think it is extremely unlikely that they will be able to respond to this inflation weakness with lower policy rates.

Instead, in recent days, we have been reading reports that the authorities may be mulling a slightly wider central government deficit to help offset or minimise the pain from the local government financing gap weighing on activity in overleveraged provinces.

There are a couple of points to make about this. Firstly, we don't discount these reports. The economy does need more support than the numerous supply-side measures we have already seen so far. But equally, the policy intent to deleverage and draw a line under the borrowing excesses of local governments seems firm and appropriate.

Whatever does emerge from Beijing over the coming months, it likely won't be quick enough to make any meaningful difference to 2023, and at best, it should be viewed as a pain management tool for the transition to a less leveraged economy. And that is a multi-year project.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more .

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

China: September Inflation Flirting With Disinflation Again