CD - Chindata Group: Customer Concentration Is A Double-Edged Sword

Summary

- Chindata's performance for Q2 2022 was reasonably good based on an evaluation of the company's key metrics for the recent quarter.

- CD's key anchor customer, ByteDance, helped to drive the company's good results in Q2, but this is also an area of concern considering its high degree of dependence on ByteDance.

- I have a Hold rating for Chindata; CD's medium-term outlook is excellent, but a slowdown in Q3 and Q4 2022 seems likely and I am concerned about customer concentration risks.

Elevator Pitch

I assign a Hold investment rating to Chindata Group Holdings Limited's ( CD ) stock. CD's reliance on its key anchor customer ByteDance ( BDNCE ) is a double-edged sword. On the positive side of things, BDNCE is at a stage of high growth, and this translates into strong top line and bottom line expansion for Chindata. On the negative side of things, if ByteDance pulls back on its growth plans or considers doing more business with other providers, CD will be adversely affected. As such, I deem a Hold rating to be appropriate for Chindata.

Good Q2 2022 Financial Performance

On its corporate website , Chindata refers to itself as "a leading carrier-neutral hyperscale data center solution provider" and "a first mover in building next-generation hyperscale data centers" in Asia. CD disclosed the company's financial results for the second quarter of this year on August 25, 2022 before the market opened, and I think that Chindata's most recent quarterly financial and operating metrics were good.

With regards to headline financial numbers, Chindata's top line rose by +13% QoQ and +51% YoY to RMB1,038 million in Q2 2022. The company's non-GAAP EBITDA margin expanded by +310 basis points YoY from 49.3% in Q2 2021 to 52.4% for Q2 2022. The robust revenue growth and the significant operating profitability improvement helped to drive a +114% YoY and +36% QoQ increase in Chindata's adjusted net profit to RMB242 million for the recent quarter.

CD also impressed investors with its key operating metrics.

The company's utilization rate improved by approximately +900 basis points QoQ and +800 basis points YoY to 78% for Q2 2022. Separately, Chindata is managing its costs well as seen with certain operating efficiency metrics. In its Q2 2022 earnings presentation slides , CD revealed that the company's construction cost on a per MW basis and its Power Usage Effectiveness or PUE (the lower the better) were $3.3 million (in USD terms) and 1.19, respectively for the second quarter of this year. In comparison, Chindata highlighted that the industry average construction cost per MW and PUE were much higher at $7-8 million and 1.59, respectively.

Capacity Expansion Pipeline Is Supportive Of Intermediate-Term Growth Expectations

CD's in-service capacity grew by +42% YoY from 361 MW in the second quarter of the previous year to 511 MW in the most recent quarter.

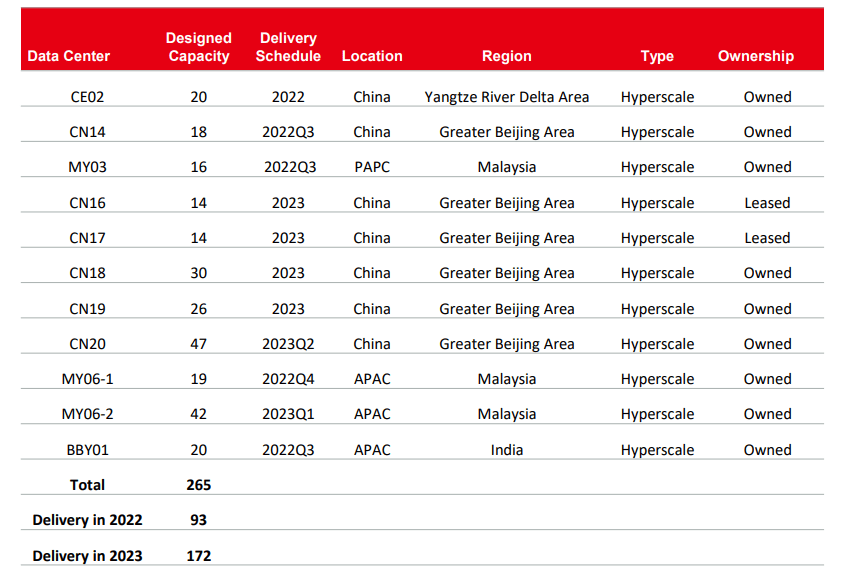

The Expected Timeline For Chindata's Under Construction Capacity To Come Onstream

{kind=link}

As indicated in the chart above, Chindata currently has 265 MW of capacity that is under construction which should come onstream by 2023. The timeline provided by CD suggests that CD's in-service capacity is expected to increase by +37% from 404 MW at the end of 2021 to 604 MW as of December 31, 2022, before rising by another +29% to 776 MW by the end of next year.

The expected expansion of Chindata's in-service capacity for this year and the following year are aligned with the market's consensus financial estimates for the company. Based on the sell-side's consensus projections taken from S&P Capital IQ , CD's revenue is forecasted to grow by +47.0% and +34.7% for fiscal 2022 and fiscal 2023, respectively. Similarly, the analysts think that EBITDA for Chindata can expand by +51.9% and +36.9% in the current year and the next year, respectively.

Watch Customer Concentration Risks And Slower Near-Term Growth

Although Chindata should deliver strong top line and operating profit growth for full-year FY 2022 and FY 2023 as described in the preceding section, the company's shares might not necessarily perform well in the very near term.

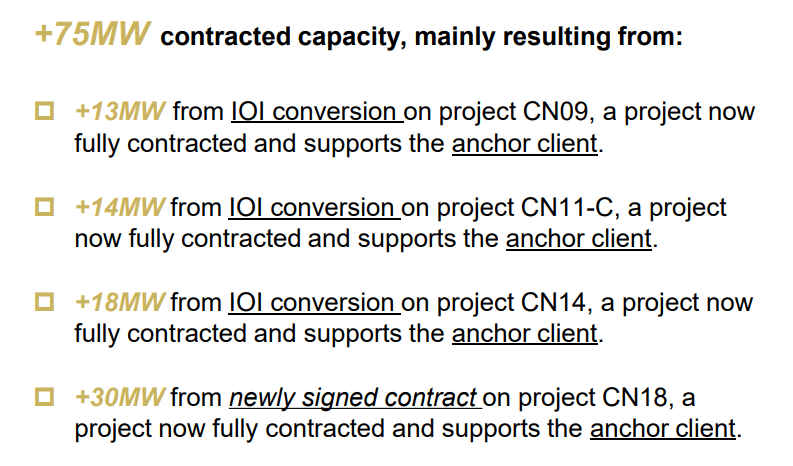

One concern is customer concentration risks, or more specifically Chindata's reliance on its key anchor client, ByteDance, best known as the parent of TikTok. BDNCE contributed 83% of CD's revenue in fiscal year 2021. ByteDance was also the driving force for Chindata's strong growth in Q2 2022, as per the chart below indicating the increase in capacity contributed by its anchor client, BDNCE in the recent quarter.

The Incremental Contracted Capacity Growth Contributed By CD's Anchor Customer In Q2 2022

{kind=link}

Looking ahead, ByteDance continues to be the key driver of Chindata's future growth. Referring to the earlier chart detailing the timeline for CD's under construction capacity to come onstream presented in the preceding section, BDNCE is the customer for Chindata's key data center projects in the pipeline such as CN-14, CN-18, and MY06-1, MY06-2.

There is no denying TikTok's popularity, but trees don't grow to the sky and an eventual slowdown in ByteDance's growth going forward might hurt CD in the future. The customer concentration risk is clearly on analysts' and investors' minds. At the company's Q2 2022 earnings call on August 25, 2022, an analyst from Goldman Sachs ( GS ) questioned whether there are "any other potential customers (apart from ByteDance) with pretty significant demand that we are in the progress of like trying to win orders." In response, CD noted that "we are in the process of landing more capacity with international customers." Nevertheless, client diversification should still be a work-in-progress for Chindata at this point in time, as BDNCE is a very substantial customer for CD.

Another concern is that there might be a moderation in CD's operating earnings growth for the second half of this year.

The current consensus sell-side analysts' estimates taken from S&P Capital IQ imply that Chindata's YoY EBITDA growth will go from +60.7% for Q1 2022 and +60.8% for Q2 2022 to +43.0% and +49.9% for Q3 2022 and Q4 2022, respectively. The key factors that will impact CD's near-term profitability are an expected increase in utility expenses in China and a rise in marketing costs (temporarily reduced in Q2 2022 due to lockdowns in Mainland China) for the second half of the year.

Concluding Thoughts

I rate Chindata as a Hold. CD is currently riding on the growth of its key client, ByteDance, and this is seen with its good results for Q2 2022. But this is also a key risk factor for Chindata, with BDNCE representing 83% of its top line last year. I find it hard to consider Chindata as a Buy, until the company makes considerable progress with its customer diversification efforts.

For further details see:

Chindata Group: Customer Concentration Is A Double-Edged Sword