CMG - Chipotle: Following Bill Ackman's Rationale To Owning The Stock

2023-09-28 21:33:55 ET

Summary

- Bill Ackman's Pershing Square fund owns 3.4% of Chipotle's outstanding share capital, making it the largest holding in the fund.

- Ackman admires Chipotle's straightforward and cash-generative business model, as well as the company's ownership of all its restaurants.

- Chipotle's clean balance sheet and ability to capitalize on favorable interest rates further contribute to its strong cash flow generation and profitability.

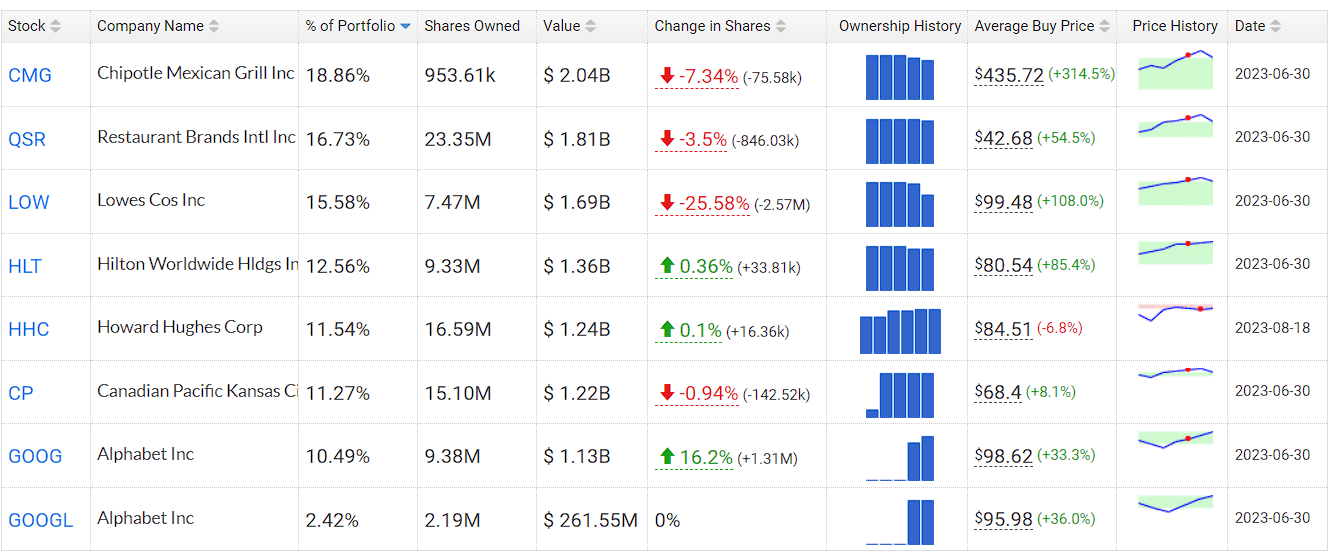

Bill Ackman loves his position in Chipotle's ( CMG ) stock. The Mexican food-oriented QSR company is the largest holding within the legendary investor's London-listed fund, Pershing Square ( PSHZF ). As of its latest filings, the fund owned 953,608 shares of Chipotle, representing about 3.4% of the company's outstanding share capital.

Pershing Square's Holdings (HedgeFollow)

{kind=link}

It's worth noting that Chipotle has been among Pershing Square's holdings since Q3 of 2016. Owning the stock for seven years, the fund's investment team has developed extended knowledge of the business. Combined with the fact that the stock remains Pershing Square's largest holding after such a long time, it should speak volumes of their confidence in the stock.

In a brief excerpt from an interview conducted two years ago, Bill Ackman briefly expresses the foundations of his affinity for Chipotle stock. In essence, he admires Chipotle's straightforward yet highly cash-generative business model. Furthermore, he highlights two additional factors contributing to his enthusiasm: Chipotle's ownership of all its restaurants and the company's commendably pristine balance sheet.

Let's take a deeper look at these factors and discuss why they should keep being a very positive catalyst for the company's investment case.

Chipotle Owns All Of Its Restaurants

To understand why it is highly beneficial for Chipotle to own all of its restaurants, we first have to understand the journey the majority of Quick Service restaurant chains take in order to succeed.

Picture the journey of a QSR chain as an adventure with two key phases. In the first leg, it's all about securing your spot in the bustling QSR scene. Now, this part can be a bit pricey – setting up a bunch of company-owned spots to show off your genius idea to future franchisees. Franchisees play a crucial role in a chain's expansion by providing vital upfront capital and mitigating the otherwise high costs and risks associated with corporate growth.

This is why the first phase is so hard. It's just too capital-intensive. Shake Shack ( SHAK ) makes for a good example here, as the company still has a hard time generating meaningful profits. In fact, the company is sort of in between the two stages. They're picking up the pace in selling licenses to franchisees, but at the same time, they're still opening their own spots in new markets to establish a "proof of concept".

The second leg is the "maturity phase". This is when a company starts shifting the mix to include more franchisee-owned. Think McDonald’s ( MCD ) and Domino’s Pizza ( DPZ )- they've mastered this, with a whopping 95% and 99% of their spots being franchised , respectively.

Here's where the magic happens. Real profits start rolling in with high-margin royalties on those franchise sales, rental cash from franchised joints, and even the added sales from distributing ingredients to the franchisees. All without the headaches of running the restaurants themselves.

But here's where Chipotle is doing something extraordinary. They've aced the first phase without selling a single license to any franchisee. Wrap your head around this: over 3,200 locations and the company hasn't franchised one restaurant. No other player in the QSR world can boast such a feat.

Of course, pursuing franchising is also a great strategy, as other giants in the space have demonstrated. And sure, Chipotle’s avenue of operating each and every location on a corporate level is more tedious. However, this strategy comes with many perks, with the most significant being complete control over the quality of the food and scaling economics, allowing for a gradual expansion in margins.

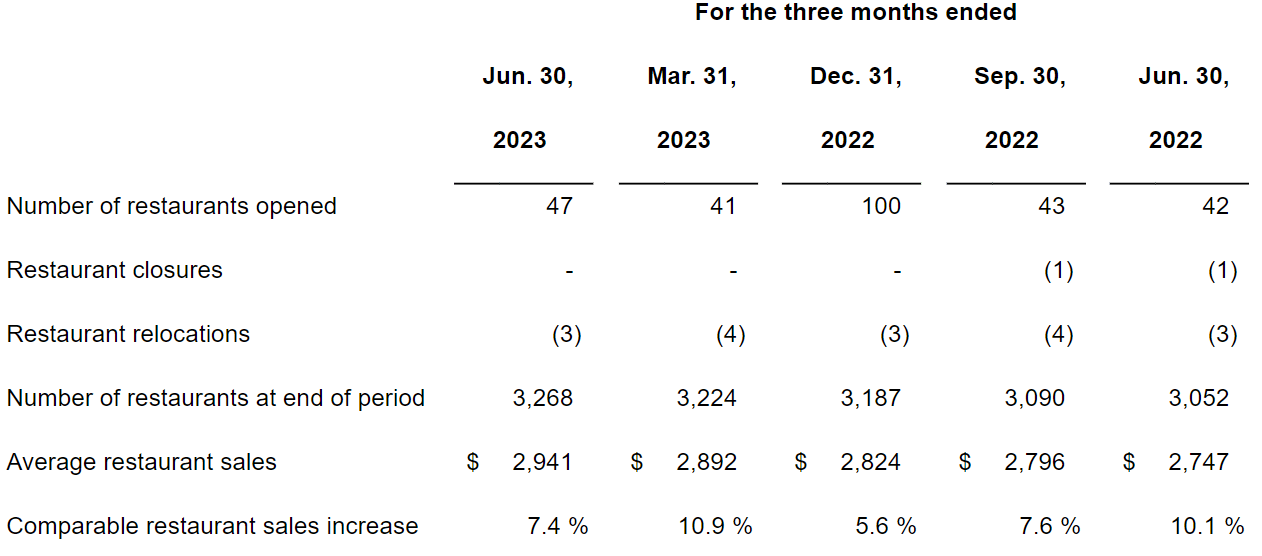

To illustrate, in Q2, Chipotle's average restaurant sales rose to $2.94 million from $2.75 million in the previous year. With higher same-store sales, you get improved unit economics efficiencies. Consequently, Chipotle's restaurant-level operating margin by 230 basis points to 27.5%, propelling the overall operating margin to 17.2% from 15.3% in Q2 2022.

Restaurant Metrics (Chipotle Q2 Results)

{kind=link}

These margins are incredibly juicy for a company that, again, doesn't collect high-margin royalties, licensing fees, and rental revenues. With economies of scale set to continue benefiting margins as Chipotle opens more locations over time, its strategy has set the company on a trajectory for a superior expansion in profits.

A Clean Balance Sheet During Rising Rates

The second attractive characteristic that Chipotle has is the fact that the company's balance sheet is clean, allowing for improved cash flow generation. Excluding its operating lease liabilities, which were valued at $3.63 billion in Q2 and essentially represent the present value of lease payments not yet paid, Chipotle has virtually no debt.

This presents a significant strategic edge for several compelling reasons. Firstly, Chipotle possesses the flexibility to readily incur debt when necessary—say, to fuel rapid expansion—without the encumbrance of heightened existing leverage concerns.

Secondly, the company is exempt from the burden of interest expenses, a particularly noteworthy advantage given the prevailing macroeconomic landscape. Notably, Chipotle even managed to generate a positive net interest income of $16.4 million from its own cash being invested in treasuries in Q2.

Chipotle's Income Statement (Chipotle's Q2 Earnings Release)

Therefore, you can see how the gain in operating margins I discussed earlier translates seamlessly to a significant net income increase. The combination of higher revenues, higher margins, and additional income from interest resulted in Chipotle's Q2 EPS surging by 33.2% year-over-year to $12.32

Chipotle's Valuation Is Risky But Reflects Its Qualities

In my view, Chipotle's investment case is less risky compared to that of its competitors due to the company having complete control over the day-to-day operations of its restaurants.

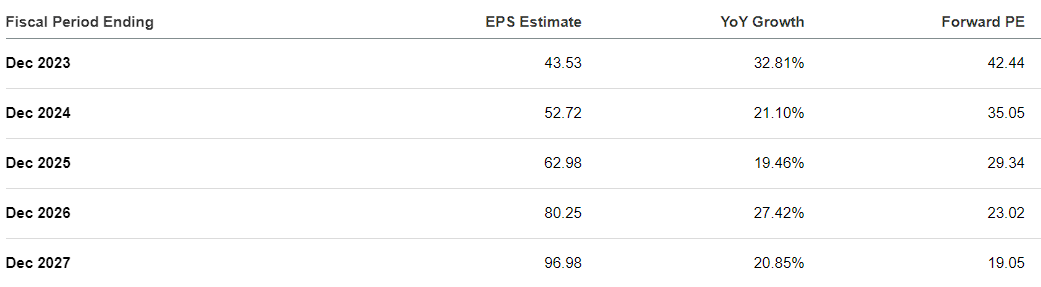

However, if there is a notable risk that is worth mentioning, it is the stock's hefty valuation. Precisely due to its strong organic growth, high prospects for rich margins, and lack of indebtedness, investors have been willing to pay a premium for the stock on a consistent basis. At their current levels, shares are trading at a P/E of around 42 based on this year's expected EPS of ~$43.53.

Chipotle's Valuation (Seeking Alpha)

{kind=link}

Admittedly, this valuation appears quite ambitious in the present macroeconomic landscape. Nevertheless, it finds justification in the high expectations investors harbor for the company's growth, evident in the forecasted 20%+ increase in EPS over the medium term, as depicted in the accompanying image.

However, it's crucial to acknowledge that Chipotle's valuation introduces an element of risk. A substantial P/E compression could ensue if the company falls short of these growth estimates. In such a scenario, potential declines in the stock could overshadow its otherwise commendable qualities.

Takeaway

Chipotle's unique position as a QSR chain that owns all of its restaurants is a testament to its disruptive approach in the industry.

By bypassing the typical franchising route, Chipotle maintains full control over food quality and enjoys scaling economies, contributing to steadily rising margins and impressive profitability.

Moreover, the company's clean balance sheet, with minimal debt and the ability to capitalize on favorable interest rates, positions it favorably in the face of macro uncertainty. After all, this edge has translated into robust cash flow generation, evident in the substantial bottom-line growth reported in Q2.

When we look at Chipotle's investment story through Bill Ackman's points, it's clear why both the company and its stock are doing so well. Chipotle is sticking to its proven plan, and it seems like they've set things up for more growth and strong profits. This setup gives ample reasons to feel optimistic about Chipotle's future prospects.

However, it is crucial for investors to exercise caution regarding the stock's valuation. The rich multiple at which shares are currently trading allows minimal room for error, thereby diminishing the margin of safety for current investors.

For further details see:

Chipotle: Following Bill Ackman's Rationale To Owning The Stock