CRTSF - Chr. Hansen: Buying More Shares After The 12% Decline

2023-08-23 21:09:06 ET

Summary

- Christian Hansen is a Danish company with premiumization and low yield, but offers above-average growth potential.

- Enzymes business, including Christian Hansen, has seen a decline in the past month, presenting a buying opportunity for long-term investors.

- The company has a strong position in the European food production value chain, developing natural solutions for the food industry.

Dear readers/subscribers,

Enzymes are a very profitable business to be in, no matter the 12%+ decline we've seen in the matter of a single month when it comes to Chr. Hansen ( OTCPK:CRTSF ). My stake in the company remains comparatively small, but any decline here is exciting because buying this business at a low valuation comes with a very pleasant overall upside - at least for the long term.

Now, there is a degree of premiumization to this company. There is in fact premiumization to most Danish companies on the market. They have a tendency to combine the unappealing qualities of both low yield and high premiumization, and some of them don't even offer above-average growth with this. That's one of the reasons I don't tend to overexpose myself to Denmark as a geography, despite it being part of Scandinavia, where I invest plenty of capital.

Christian Hansen trades under the native symbol CHR on the Copenhagen exchange. That is also how I believe you should go about investing in the business. The ADRs are thinly traded, and overall diversification is positive here because the Danish crown, DKK, doesn't share the same weaknesses as the SEK is currently exhibiting.

Christian Hansen - Plenty to like about the valuation & upside.

The main argument for investing in Christian Hansen, aside from the quality of the company, is the upside we find ourselves in Post-drop. This requires you to legitimize a high premiumization for the business, but given the company's long-term growth rate and overall safety, I find this to be possible.

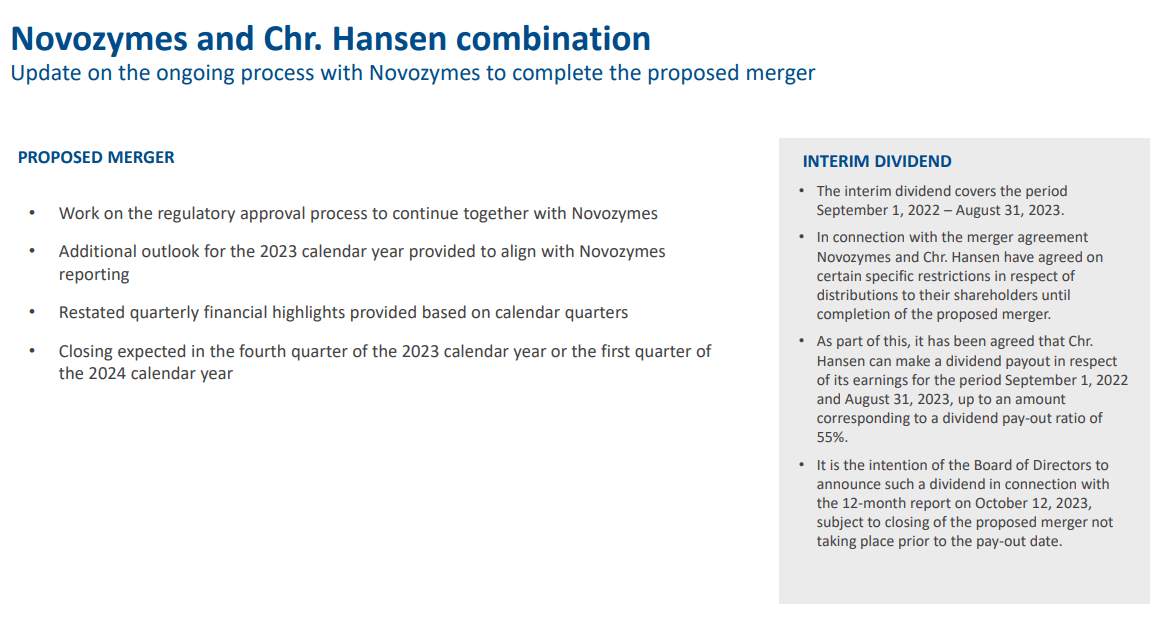

In my recent article, I looked at Christian Hansen, including through the lens of the upcoming merger with Novozymes. Hansen has, with or without this merger, a great appeal as a business.

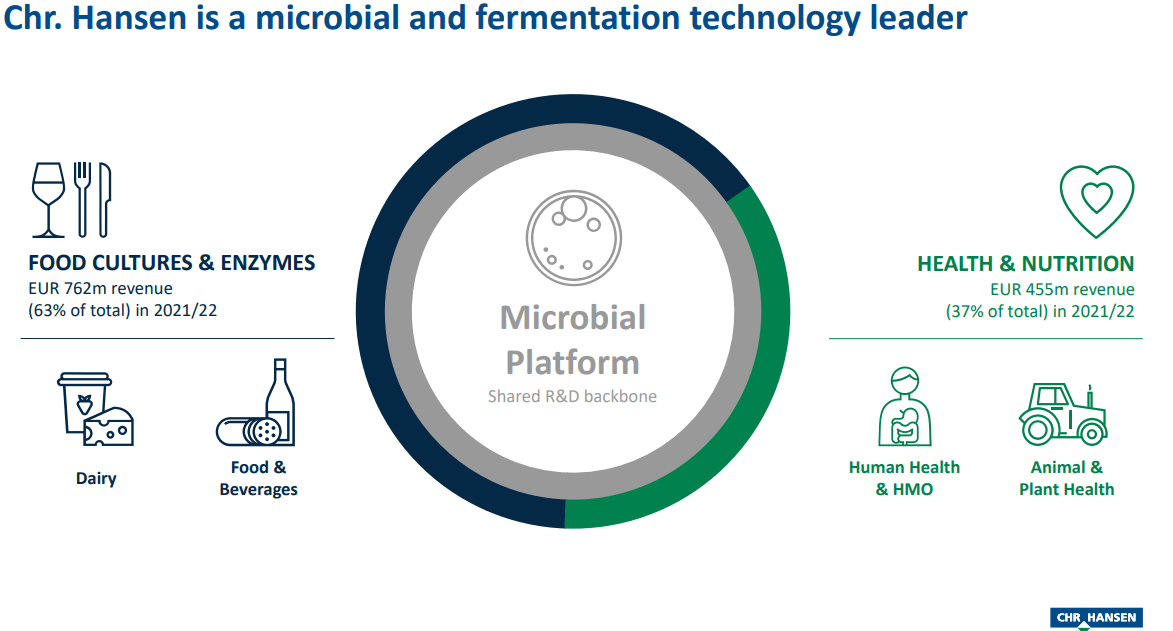

As a global bioscience giant with almost 150 years of history, it has a keystone position in the European food production value chain. It's a producer of enzymes and rennets for the production of cheese-making, as well as various coloring agents, food cultures, and nutritional products. Part of the company's portfolio is less unique or "moated", but large parts of what the company does, that's where this business has a market advantage in terms of scale and market share.

The company develops natural solutions to reduce sugar, food safety and work with the aim of reducing the overall amount of artificial ingredients in the food industry apart from the core areas of cultures and enzymes. Chr. Hansen works to develop natural solutions in order to increase efficiency and industry output as well as, for example, solutions that reduce the required addition of sugar in order to reach a certain level of sweetness. Naturally, such processes and products are very much in line with the overall trajectory of the current food industry.

Chr Hansen IR (Chr Hansen IR)

In my last article , I went through some of the company's basic and fundamental profitability numbers - and how these numbers were extremely impressive, all things considered. A COGS of below 50% is always impressive, but the company combines this with a very lean operating expense model, squeezing very impressive amounts of net margins from every revenue dollar that goes through the business.

The current split is also appealing. In terms of the sales mix, it's around a 63/37 mix of Cultures/Enzymes and Nutrition respectively, and geographically, 36 and 30% go to EMEA and the US, with the remaining split between APAC and Latin America and other segments. As you can see, it's not just a European company - far from it, in fact.

{kind=link}

We also know why the company has underperformed for the last few years, with China being a major exposure for this business. Christian Hansen, like many companies that operate in China, is much more complex than initially expected and communicated in marketing material. Presenting China as an underpenetrated market (at the time) was not wrong - but I've seen and reported in segments not only like consumer staples, but telecom, real estate, and other areas, it turned out to be far more complex - and less profitable - than initially expected.

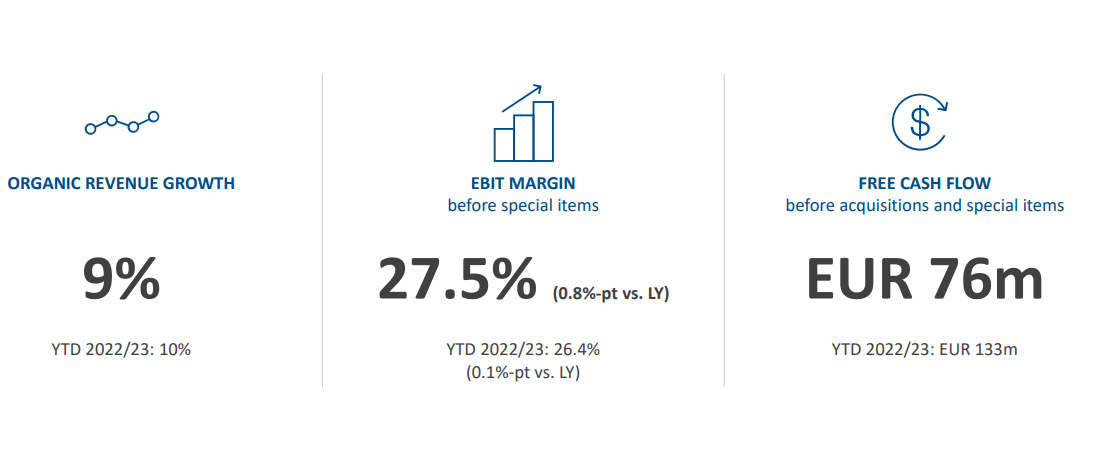

Despite what you see in the recent share price trends, the company is actually doing rather well - at least if we look at the quarterly results .

{kind=link}

Sure, some numbers like FCF are down YoY, but there are reasons for this. My focus is more on the combination of increased top-line and solid margins. The company can achieve this through either a better mix, better sales, or pricing (and some other combinations). Much of this, like with most companies I currently review, is driven by price increases related to inflation.

The company declines for the quarter were seen, unsurprisingly, in APAC geographies, which fell by 2% despite pricing due to negative trends in both China and India specifically, as well as softening markets in Korea.

This in turn was weighed up by growth in EMEA, LATAM and NA, all of which grew either by double digits or close to double digits - again, mostly through pricing initiatives, but also volume growth.

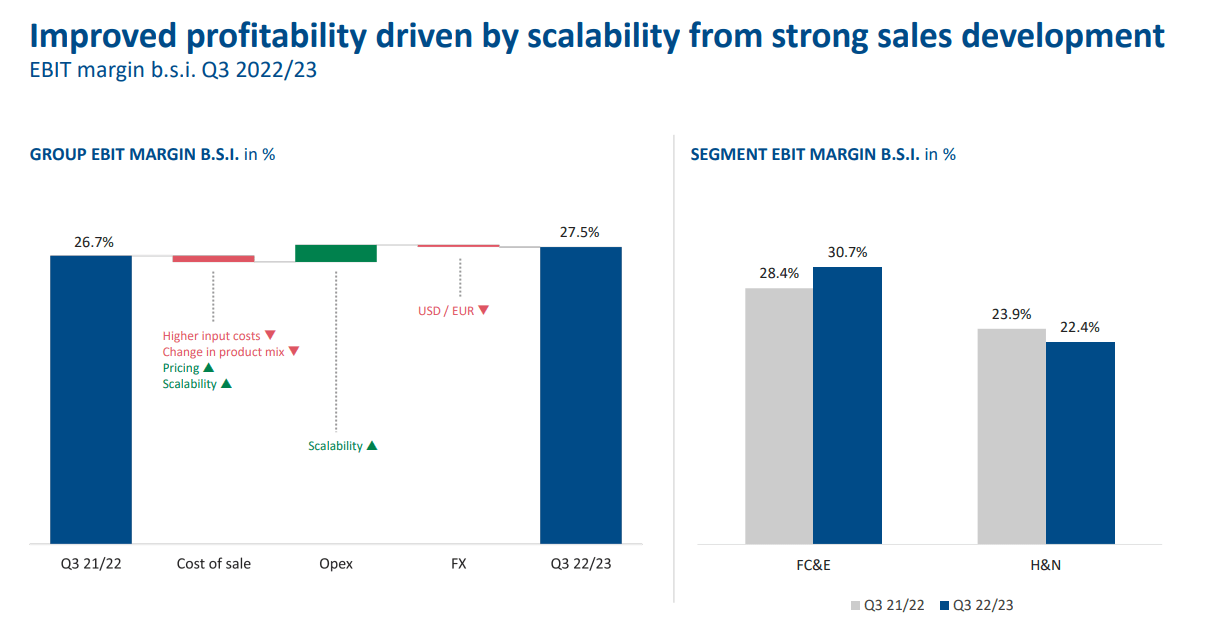

This enables actual profitability improvements for Christian Hansen, completely contrary to the valuation development of the share price.

{kind=link}

The company experienced higher amounts of working capital during the quarter - but due to significant increases in operating profit and taxes, this more than made up for the increase in WC. The company's continued outlook is an overall positive one, with expectations for a double-digit organic revenue growth (or as low as 9%, which isn't low), and an EBIT margin in line with previous years. The fact that FCF, on a full-year basis is set to grow and improve as well cements the positive view we can have on Christian Hansen. This also means that because the company is declining in share price, that this is a move in direct opposition to what is expected of the company in terms of 2023-2025E growth.

And this is always an excellent time to go into an investment.

Then there is the aforementioned merger, which is a solid upside as well.

{kind=link}

On a segment-specific basis, Health & Nutrition is the most volatile segment of the company's operations, while Food culture and enzymes is more stable. However, the group margin trends, due to the sales split, remain very stable with a trough of 24.4%, compared to an average of around 27% for the past 3 fiscal years.

Christian Hansen has everything you'd be looking for in a company, barring a high yield. It has sector-beating profitability, it has scale, it has globalization, it has underlying demographic trends, it has earnings-related upside. All in all, if you can get past the massive premia that you need to accept, this is an investment well worth considering.

Risks? Few structural or fundamental ones. The risks are mostly valuation-related. As we move into a higher interest rate environment with different WACCs and risk-free rates, we need to consider that parts of Europe have had close to ZIRP for almost a decade at this point. This has significantly skewed valuations for some of these quality companies and means that we can't use historical bases as much of a future indicator for how high the company should be trading.

Based on this, I give you my current valuation thesis for the company.

Christian Hansen Valuation - How high can we expect this company to be?

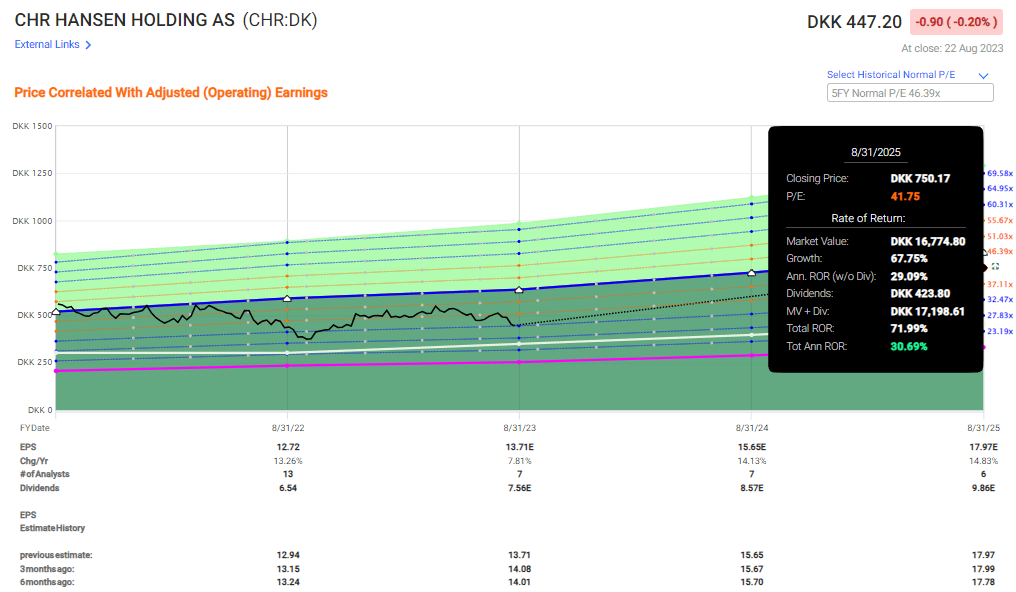

So, Christian Hansen is unfortunately at a very high valuation level despite what can be argued to be a meaningful drop in a relatively short time. We're not back to fall -22 troughs, but we're getting close to it. The company now trades at around 32x P/E, which sounds very high, but needs to be considered in the context of the company usually trading at over 40x. Also, the valuation is completely in contrary to the earnings trends. The company grew in 2022, is expected to grow this fiscal, next fiscal, and the 2025 fiscal.

And because accuracy trends are over 80% accurate if we include earnings beats from the company, there is a high likelihood of such earnings growth materializing, at least as I consider the likelihood.

What does this mean for the valuation?

If we say that Christian Hansen is worth its 40x P/E premium - or even 46x as the 5-year average is, with its 1.57% current yield (which by the way can be considered safe), and the inclusion of Novozymes, then the upside to that 40-41x P/E is around 30% annualized, or 72% RoR to a 41.7x, or around 68% to 41x P/E.

{kind=link}

Of course, this assumes a continuation of the relatively high premium we've seen during significantly different interest rate environments.

I continue to accept the company's premium here - at least some of it in my forecasts. Not the full 40-46x, but rather forecast it closer at 35-37x based on its appeal, market share, safety, and combination with Nzymes. A 37x P/E premium implies a 2025E share price of 662 DKK and an annualized upside of around 23%. This is well above my overall demand of 15% annualized - as is the lower end of my target range of 35x P/E.

In fact, you could go as low as 32x P/E and still annualize almost or just above a 15% annualized RoR, implying in turn a share price of 580 DKK, or 40 DKK below my current official price target of 620 DKK for the company.

S&P Global continues to view the company as a positive potential investment. For the native Danish ticker of CHR, 10 analysts average a low target of 500 DKK up to a high target of 750 DKK/share. This means that the company is currently significantly below even the lowest target for the company. Despite this, only 3 analysts are at "BUY" or similar here. I interpret this as what I am speaking about in this article - hesitation prior to the M&A, as well as to see where exactly this company ends up "settling" in terms of valuation as we move into higher interest rates.

I think forecasting above 40x P/E is responsible - but I think that 35-37x P/E will hold in the long term, given the company's stability and fundamentals. That's why I hold my PT, add more shares to my stake, and continue to be at a "BUY" here - even above that in my article from around a month back, and where the 12% decline justified this update.

Thesis

- Chr. Hansen Holding is a leader in technologies relating to microbial and fermentation, specifically enzymes, and Health/Nutrition. The company has averaged double-digit earnings growth for over 10 years and is usually traded at a high premium akin to some of the highest P/E companies out there.

- In order to invest in the business, you need to accept that high premium and that potential high growth rate outlook, as well as the meager yield of below 2%, currently at ~1.5%.

- Because I accept the premium and forecast the company at above a 30x P/E, I can see a double-digit upside here if the company continues to manage double-digit growth and maintain a PT of around 620 DKK/share.

- That makes this company a "BUY" here, and one of the highest P/Es of any company that I accept.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I will not call the company "cheap" here, but I will say that it has an upside - and for that reason, I give it a "BUY".

For further details see:

Chr. Hansen: Buying More Shares After The 12% Decline