IFF - Chr. Hansen: Still Somewhat Undervalued After Its Outperformance

2023-12-26 15:52:05 ET

Summary

- Chr. Hansen Holding A/S is a Danish company with above-average growth potential in the enzymes business.

- The company recorded strong financial performance with 16% organic revenue growth and double-digit growth in core segments.

- The pending merger with Novozymes is expected to be a game changer for the sector and create a leading global bioscience player.

Dear readers/followers,

In this article, we'll look at Danish company Chr. Hansen Holding A/S ( CRTSF , CHYHY ), which I have covered with solid "BUY" ratings twice before on Seeking Alpha. The last time I covered the company, it was in the early beginnings of a dip - a dip that continued and was for me a reason to continue to "BUY" the company.

This was the right choice. I'm up more than 20% RoR on my investment in this company, and even if you bought at the early part of the dip only in conjunction with my bullish article on the company, you still would have done quite well for yourself in overall returns, in the sense that you would have beat the market quite handily in a short period of time, or less than 6 months.

Christian Hansen RoR (Seeking Alpha)

Christian Hansen is a Danish company with premiumization and low yield but offers above-average growth potential. The company is something as "alchemical" as an enzymes business, which is surprisingly more volatile than you'd expect, but is expected to generate good upside over the next few years.

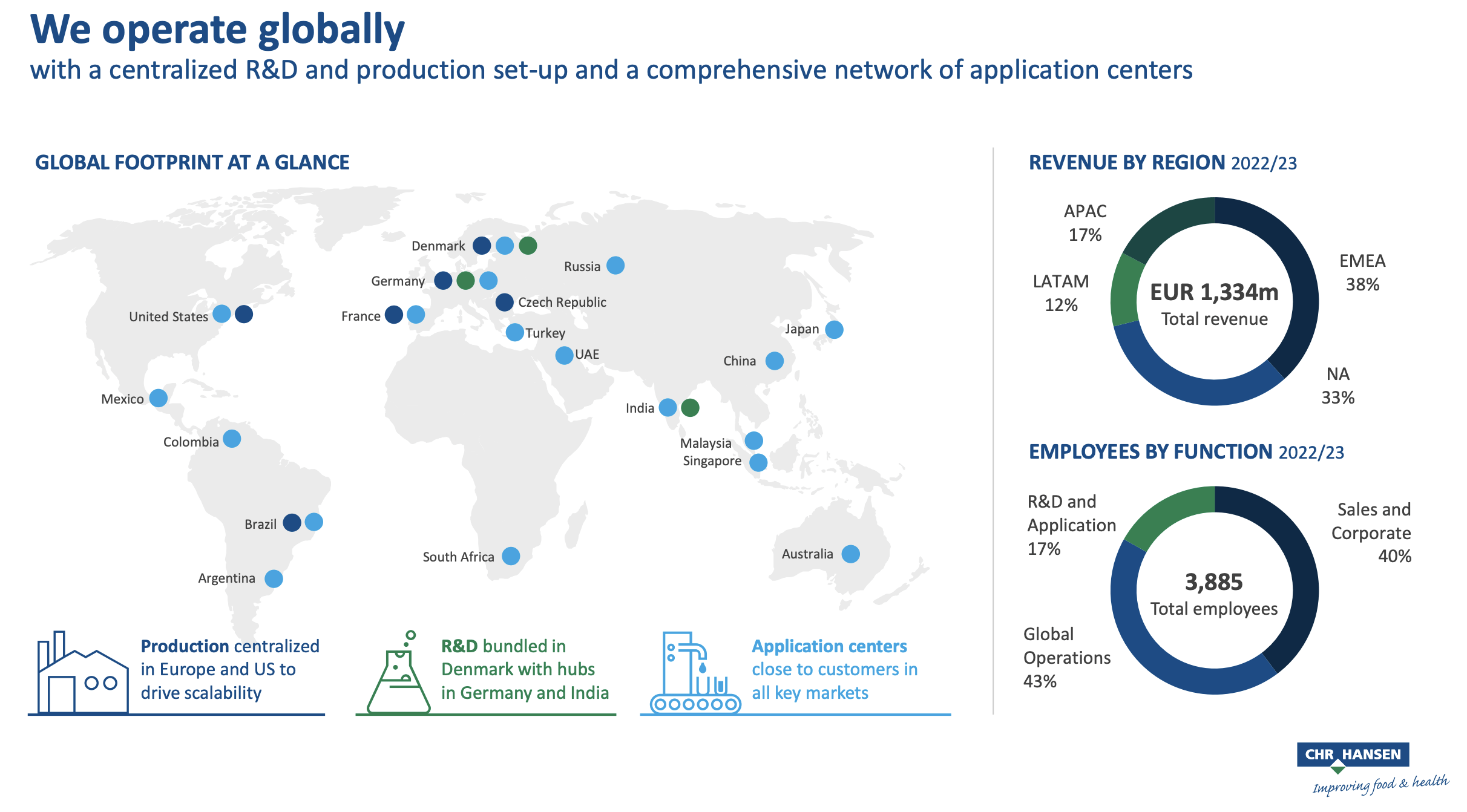

The company we're reviewing has a very strong market position in European Food production and develops natural solutions for a growing and good food industry.

My stake in the company remains comparatively small, but any decline in my stake is exciting because if you manage to buy this business at a low valuation, this could come with a very pleasant overall upside - at least for the long term.

Let's look at recent results and trends.

Christian Hansen - Upside in enzymes continues

The latest set of results we have are around 1.5 months old at this point, with fiscal Q4 2023 coming out in October. The company recorded a strong financial performance in the extended financial year.

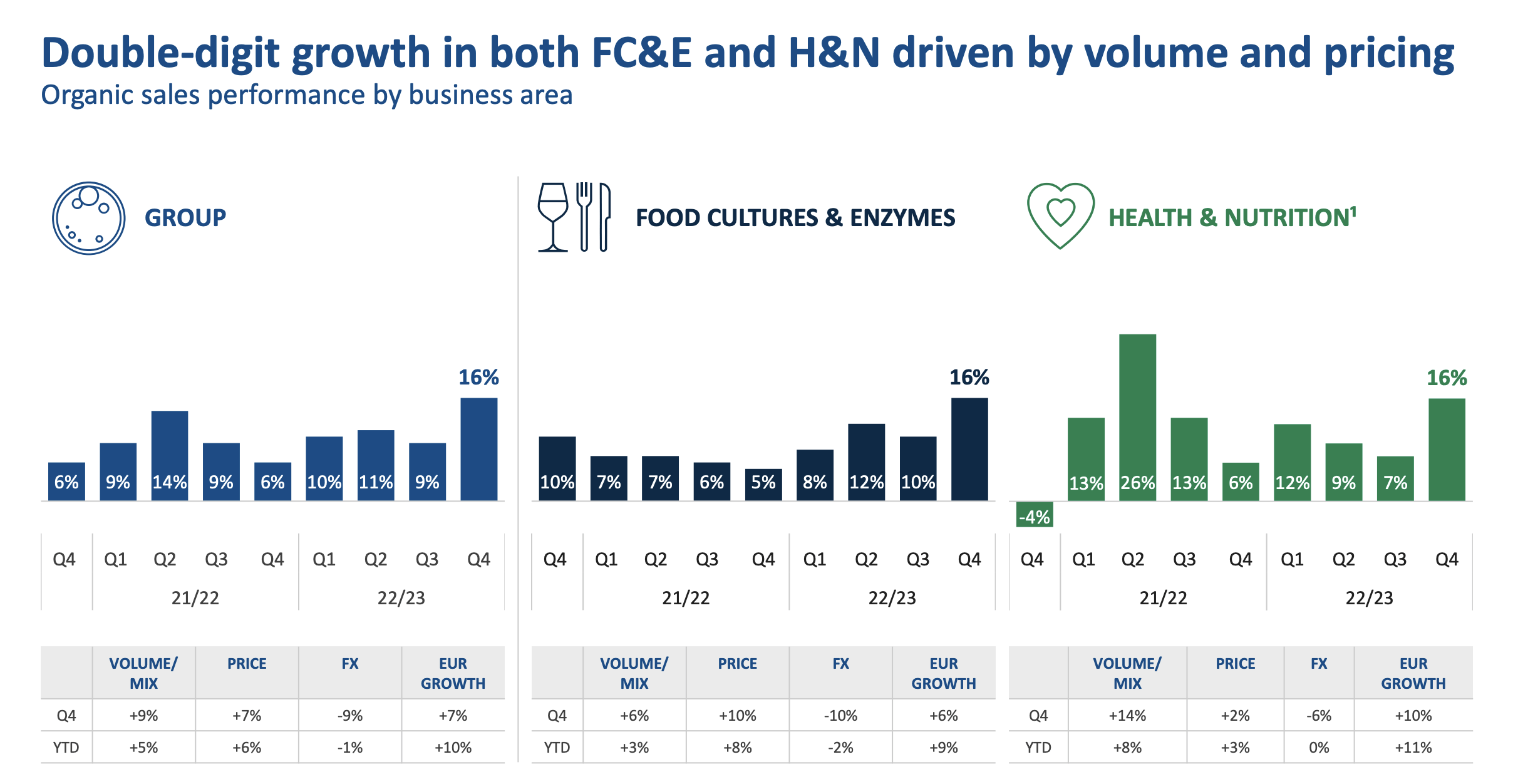

In this case, we're talking about a 16% organic revenue growth with a continued EBIT margin of 28% and free cash flow, or FCF, of almost €70M. This last number was impacted somewhat, but still at a good level.

The company recorded double-digit growth in its core segments, including the Dairy and a new probiotic strain. Much of the growth came from inflation-driven price increases, which saw the company passing along, successfully, much of these to customers.

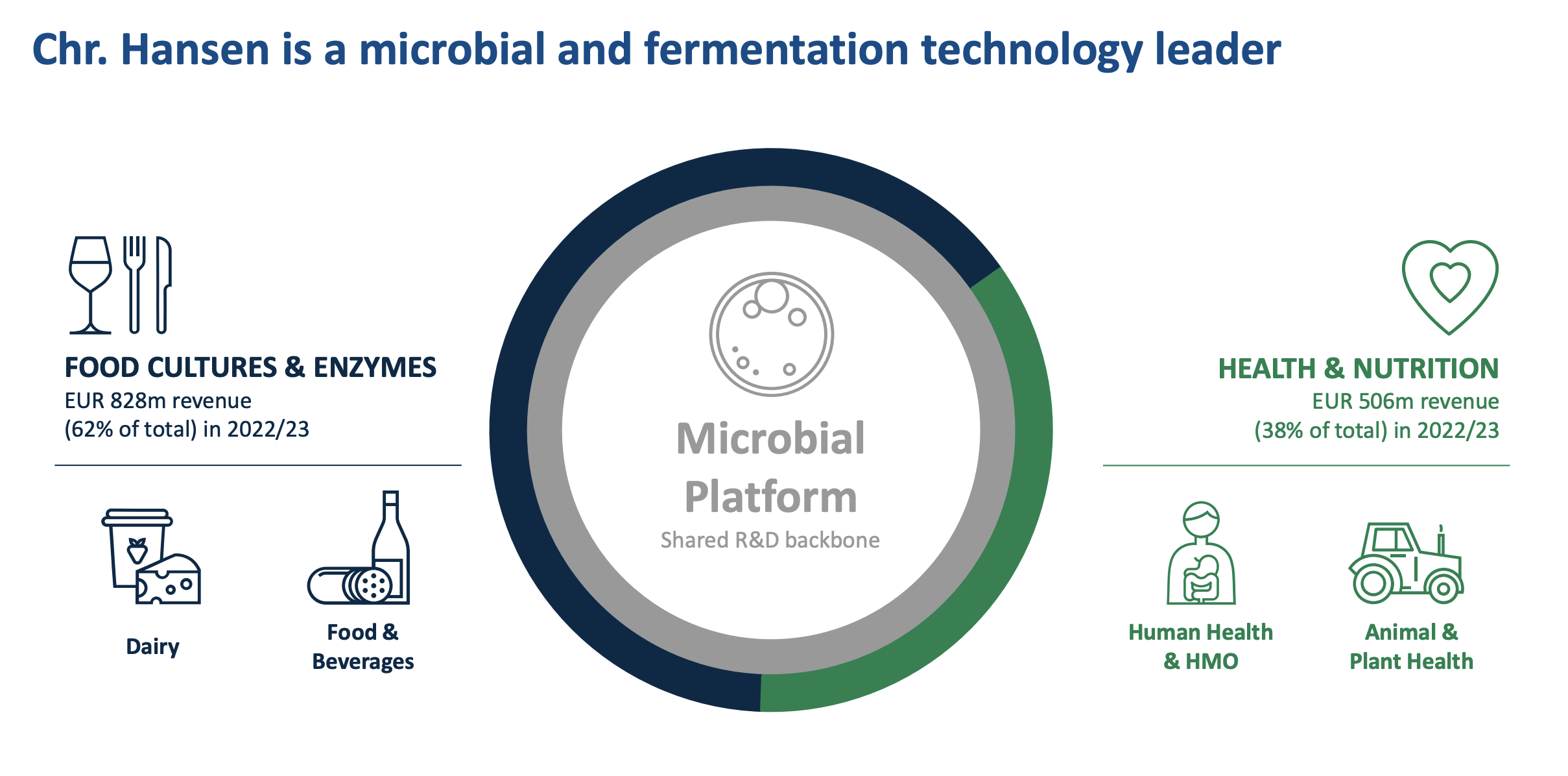

Remember, the company is a play on two sectors - food cultures & enzymes, and Health & Nutrition. Both of these saw impressive trends, with good growth across most of the company's regions.

Chr. Hansen IR (Chr. Hansen IR)

{kind=link}

I also don't want to give the impression that the upside came only from pricing - it's both pricing and organic volume growth in sales, and this is even considering some of the negative FX affecting the company.

Food Cultures and Enzymes remain by far the core and most profitable of the company's sectors. Here, the company manages over 30% of EBIT margin, and on a broad perspective, is one of the best companies in terms of profitability in its sector , that sector being Chemicals (Source: GuruFocus). The company has very conservative leverage, only enhanced slightly by recent M&A's, but still has interest coverage of over 21x, again above average.

The dividend yield continues to be the main problem for investors here. 1.37% isn't much to write home about, even at a relatively safe level.

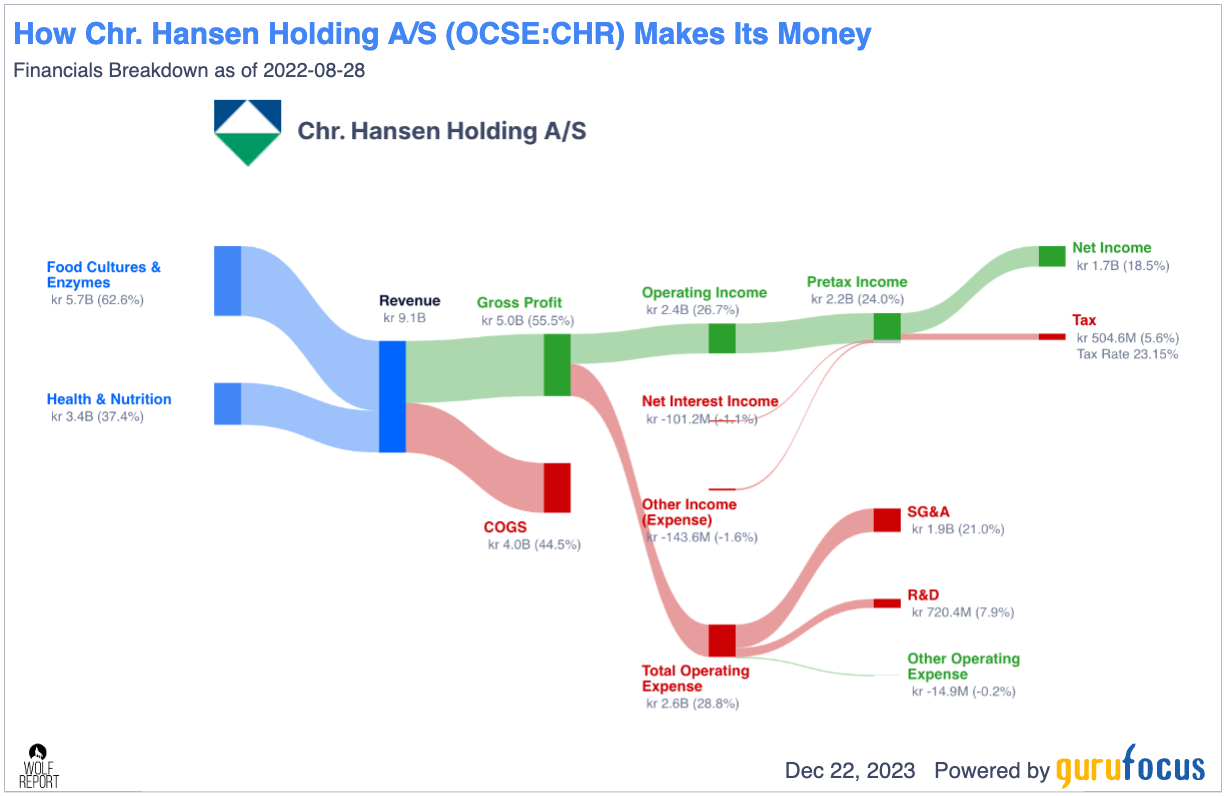

The best thing that can be said for the company is that it has an extremely impressive business model. Take a look at the financial details.

Chr. Hansen Business model (GuruFocus)

{kind=link}

The company also recorded impressive trends in terms of its working capital, with less taxes paid, and the ongoing 12-month forward outlook calls for the company's margins to remain at impressive levels, over 26% for the 2024E period , and FCF recovering to around €200-€300M depending on specific trends here.

Remember also, the pending potential merger with Novozymes, which would be a game changer for this entire sector. On March 30th this year, the merger was approved by the EGM's of the companies with a significant majority - so I view anything left as mere formalities, given that the proposal has already been cleared by the U.S., China, France, Italy, South Africa, Brazil, and Turkey. The completion here is expected this quarter, or the first quarter of 1Q24. The interim dividend has already been paid to shareholders, including myself.

Chr. Hansen IR (Chr. Hansen IR)

{kind=link}

This company, and the proposed merger, is likely going to result in a leading global bioscience player, and one perhaps in the most attractive areas that there is, given that it hasn't much to do with pharma, but with food cultures. This is what forms the appeal to me of investing in this company.

On the other hand, the recent few months have seen an incredible bounce in the company's share price. The company has gone almost nowhere in the last 5 years. The TSR for shareholders that held since 2019 has been negative 3% in total , exclusive of dividends, though the dividend is that very meager 1.2-1.5%.

In order to ensure competitive upside for an investment into Chr. Hansen here, you want to make absolutely sure that you buy it cheap.

And as to that, there is considerable uncertainty at this time. Most of the traditional analysts have firmly raised their fair-value estimates for the company due to the merger with Novozymes. The combined company compared an FV of around 400-500 is now estimated by many to be as high as over 600 DKK/share (Source: Morningstar) due to this merger.

I'm not as sure as some of those analysts here. That's why I am happy I added at under 470 DKK, but may not be adding much more in the absolute near term.

Chr. Hansen IR (Chr. Hansen IR)

{kind=link}

What can be said positively for the company is the presence of a fairly comprehensive moat - the problem is that the entire sector is currently undervalued.

The company's closest relevant competitor is International Flavors & Fragrances (IFF) - while this company has significant comparative uncertainty and a more volatile mix than Chr. Hansen, that company is still vastly more undervalued than this one.

Let's look at the risks and upsides to this company.

Risks & Upside to Christian Hansen

The risks to this company exist. I would argue that the company's underlying growth quality has worsened due to maturing diary markets, and the merger with Novozymes exposes a reliance, perhaps even overreliance on inorganic growth initiatives, which is never a good thing. I don't believe that even with Novozymes, this company can manage a superb and above-average market or sales growth rate, and this will influence the already low dividend growth rate that this company has.

There's also a bit of complexity in terms of marketing to this company. While Chr. Hansen has comprehensive research proving the veracity of its probiotic strains, this still needs to be pushed to consumers, who need to be convinced.

On the other hand, the company is by far the dominant global player in enzymes and diary cultures - and this position will only be enhanced with Novozymes.

Chr. Hansen IR (Chr. Hansen IR)

{kind=link}

I can even put a number on it. The company has 50% of the global market. It has the largest commercially available strain library on earth.

This is not small potatoes and one of the primary reasons I invest in the company.

Any risk to the company long-term is made up for by fundamentals and quality. The only question to my mind left is growth. And this takes us to the company valuation.

Christian Hansen Valuation

If you recall my previous article, I already bumped my price target ("PT") for the proposed merger to 620 DKK/share. This means that I am still at a "BUY" for this business, even though I don't necessarily consider the company to be the strongest potential on the market any longer.

This is owing to the extreme levels of valuation. Chr. Hansen demands a 5-year premium of 44x P/E and even a 20-year of 37x. This is one of the highest still-existing and accepted premiums that I hold in my portfolio. Not even Tomra Systems (TMRAY) gets the benefit of the doubt for this sort of premiumization any longer, and I do not think it is outside the realm of possibility for this company to drop down once again.

So when I say that it's still somewhat undervalued, I mean to its premium.

If you accept its 20-year premium of 37x, then that 620 DKK+ upside is exactly the level you get, but this no longer gives you a 15%+ annualized upside.

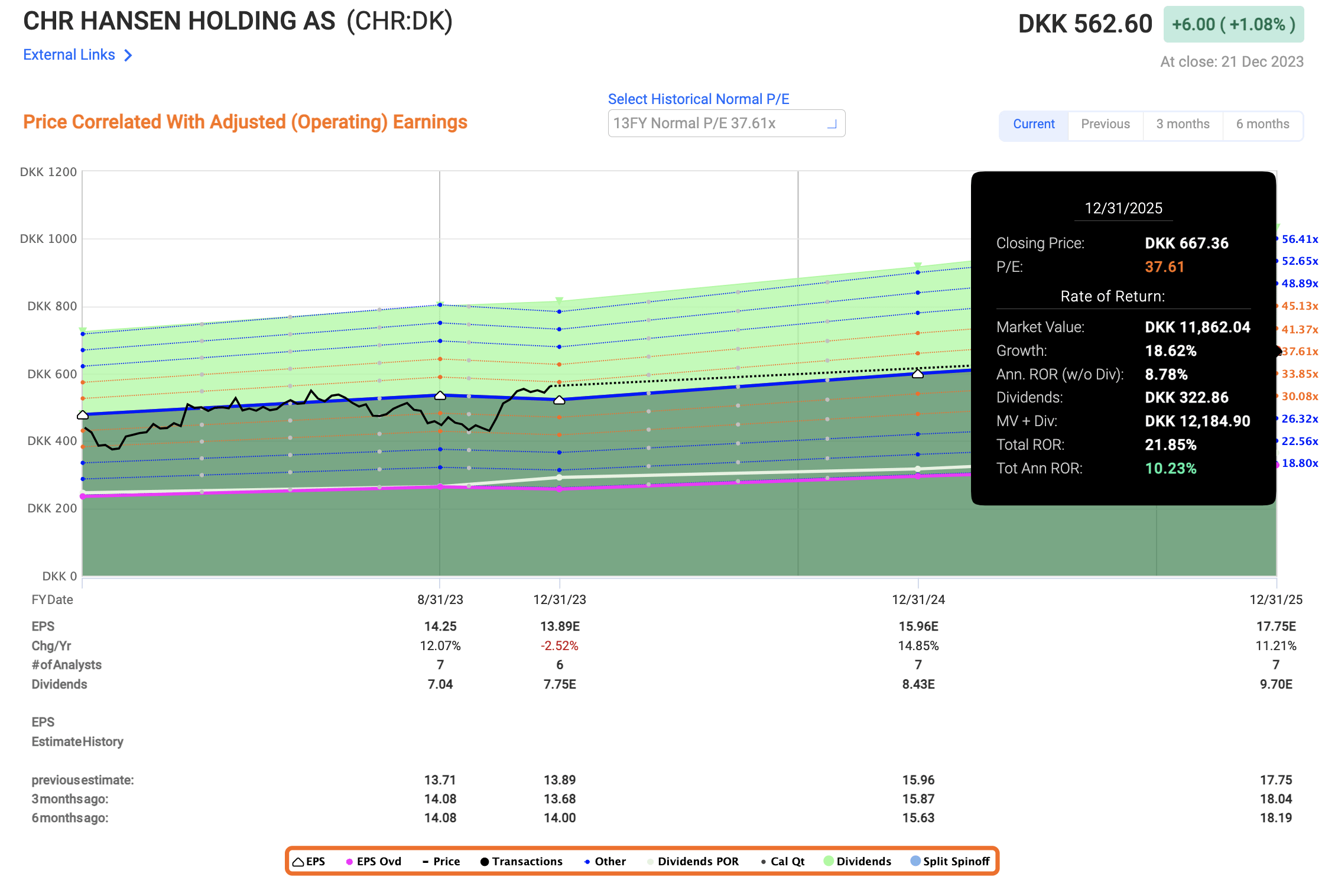

Chr. Hansen Upside (F.A.S.T graphs)

{kind=link}

I don't consider 44x to be "okay" to estimate this company at, but I will give the company allowance for trading at around, 40x, which still gives us around 15% annualized upside. The company is therefore still a "BUY" here and does have an upside.

S&P Global analysts give the company a range starting at 550 and going all the way to 790 DKK, with an average of around 660 DKK. 9 analysts follow the company, but only 2 have the company a "BUY," which is more than it was during the time the company was actually significantly undervalued. Most of the analysts currently following the company have Chr. Hansen at a "HOLD" likely to see the impact and trends once Novozymes is part of the mix.

I would still consider the company to be an attractive prospect here, but I would at the same time not go significantly deep to a 1-3% portfolio position here without seeing more details from Novozymes.

Here is my current thesis for the company.

Thesis

- Chr. Hansen Holding is a leader in technologies relating to microbial and fermentation, specifically enzymes, and Health/Nutrition. The company has averaged double-digit earnings growth for over 10 years and is usually traded at a high premium akin to some of the highest P/E companies out there.

- In order to invest in the business, you need to accept that high premium and that potential high growth rate outlook, as well as the meager yield of below 2%, currently at ~1.5%.

- Because I accept the premium and forecast the company at above a 30x P/E, I can see a double-digit upside here if the company continues to manage double-digit growth and maintain a PT of around 620 DKK/share.

- That makes this company a "BUY" here, and one of the highest P/Es of any company that I accept. The company is less attractive now in December of 2023, but it's still at a level where I can accept this price target and rating for the long term.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversion.

I will not call Chr. Hansen Holding A/S stock "cheap" here, but I will say that it has an upside - and for that reason, I give it a "BUY."

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Chr. Hansen: Still Somewhat Undervalued After Its Outperformance