CHDRF - Christian Dior: Buying LVMH At A Discount

2023-10-23 14:40:26 ET

Summary

- Dior is a holding company whose main value comes from its equity in LVMH.

- LVMH possesses a wide moat that is growing since its products are used to differentiate from people who do not possess them.

- Dior is trading at a discount with respect to its share of LVMH.

Christian Dior (CHDRF) is a French traded company which owns almost 50% of the shares of the luxury conglomerate LVMH, led by the businessman Bernard Arnault. Currently Dior trades at a significant discount with respect to its share of LVMH and may be an interesting option to acquire a stake in the conglomerate at a discount.

Before getting things more complicated, let's take a look at how Dior and LVMH are related. Their history goes back quite some years when Monsieur Arnault began to have an interest in the luxury niche. In a corporate operation he acquired a significant stake in Dior, which now amounts to more than 97% of the float of the holding. In 1988 Arnault, with the financial power provided by the cash flows of Dior (and also by the money of some French bankers), decided to take a 32% stake in the equity of LVMH Moët Hennessy - Louis Vuitton, Société Européenne (LVMHF), creating one of the biggest luxury conglomerates at the moment.

In practice, the company is a holding company that owns a significant position of LVMH's equity. Its financial evolution is then linked to the performance of its main asset, the stake in the luxury conglomerate LVMH. Since Dior is very dependent on what LVMH does, we can take a look at the financial statements of the latter. Over the last decade, the French luxury conglomerate has achieved average gross margins of close to 70% and operating margins of around 22%. Growth in all key metrics has been impressive: sales grew annually at 10.9%, operating income at 13% and free cash flow at 15%. In addition, debt shouldn't be a big concern. The company has a net debt of €28 billion (may seem a bit high) but its effective interest rate is around 2.5%, it is smaller than what the American government has to pay now in the market to sell its debt! Isn't this incredible? Now that we have been over the main metrics, let's dive into the operating activities of the corporation.

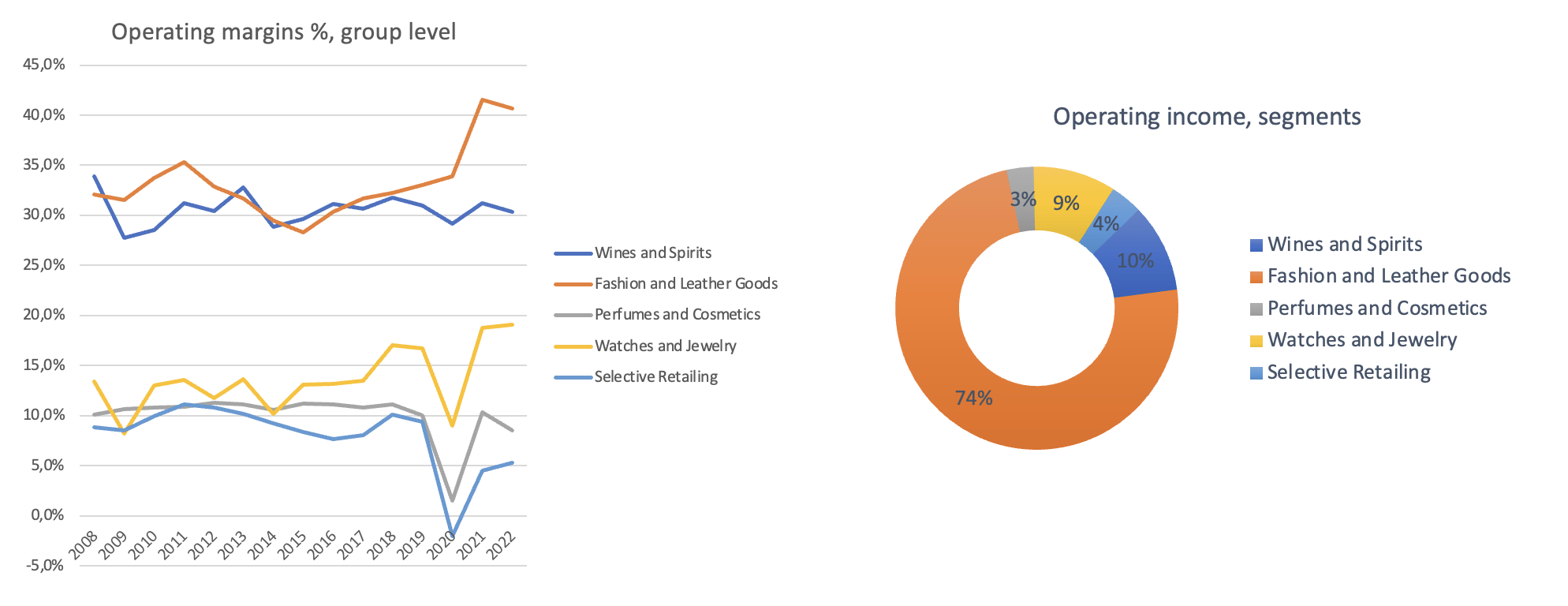

The company reports in five different segments which include sales from Wines & Spirits, Fashion & Leather Goods, Perfumes & Cosmetics, Watches & Jewelry and Selective Retailing. The first division includes iconic brands such as Moët Chandon or Hennessy, which have grown since 2008 at 5% rates and achieved average margins of around 30%. Comparable corporations can be Diageo (DEO) or Pernod Ricard (PRNDY). The second segment has in its portfolio iconic brands such as Louis Vuitton or Dior Couture. Margins have expanded up to 40% and since 2008 growth has been close to 16% per annum. The Perfumes & Cosmetics segment has grown at somewhat lower rates, around 6%, with margins of 10%. The Watches & Jewelry division has reported margins of 19% and annualized growth of 22%, somewhat distorted by the acquisition of Tiffany's in 2020-2021. Finally, Selective Retailing, which includes brands like Sephora, has grown at slower rates as it has been negatively impacted by COVID. In 2020 they made negative margins, now they are at levels of 5%, somewhat below pre-pandemic levels. As long as normalization of travel and restrictions disappear, margins should go back to normal in my view.

{kind=link}

The image above shows the evolution of operating margins since 2008 and the most updated sources of operating income. More than 70% of the profits come from Fashion and Leather Goods, where the company is more specialized and optimization of business processes is higher.

But how does all of this growth and financial power translate into value creation for shareholders?

{kind=link}

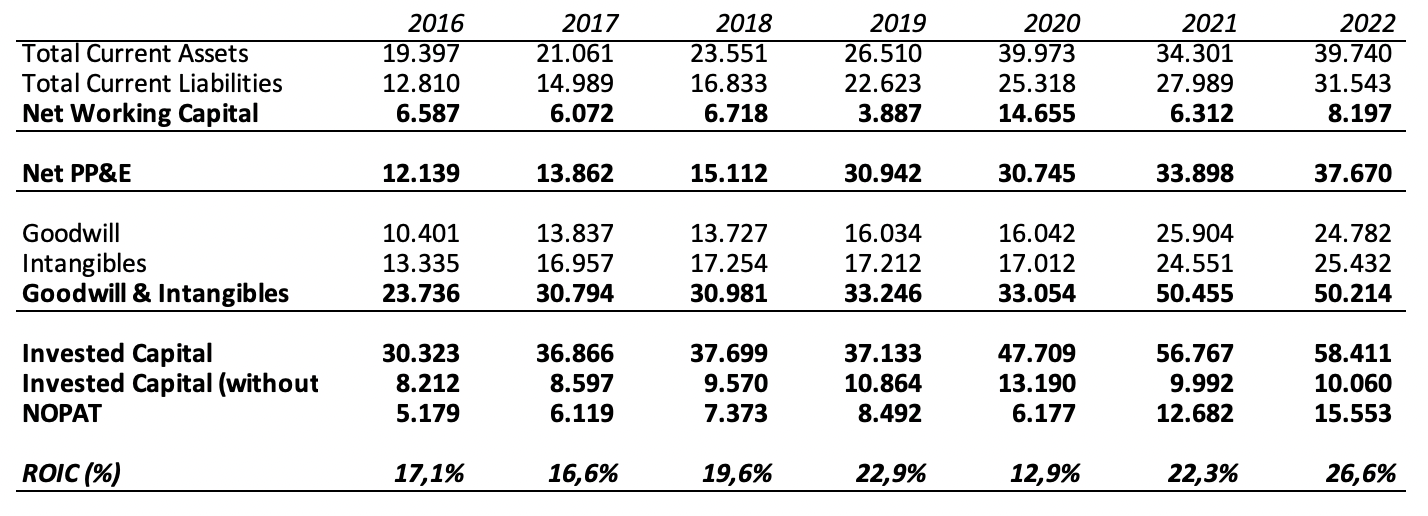

The previous table shows how good LVMH is performing in terms of ROIC, this is, how much profit after tax they generate based on the net value of the assets needed to produce those profits. Since ROIC is above the cost of capital systematically, LVMH is constantly generating value for its shareholders, and Dior is the biggest of them. Since the reinvestment rate (net capex + acquisitions adjusted for changes in working capital) is around 30-40%, the expected organic growth is around 6-8%. If we correct for acquisitions and possible margin improvement, the expected growth can move to ranges between 9-11%, which has been the average return of LVMH shares over the last 30 years. But how can a business that performs so good be maintained in the future? The fundamental laws of economics tell us that high returns should attract competition, and as a result of this the profitability of investments in the sector would sink. Why is this not the case?

LVMH is one of those few companies in which economic laws are the exception and not the rule. The company does not just produce goods, but rather generates desires in people. It may sound strange to your ears, but it is true. Desires for differentiation, desires to have items to distinguish themselves from those who do not have them. Exclusivity in short. And indeed exclusivity is key to understanding why the business works. A product that serves to differentiate oneself, that is scarce and that allows one to mark a level of social status that is inaccessible to many is something that cannot be replicated. For this reason, there are few competitors that can enter this niche. Even if they did enter, they would require years of positioning and development of a product that people may eventually consider differentiating and not a premium item. The risk is too high and the reward too low. The competitive advantage that companies like LVMH possess is that consumers associate their products with differentiation and exclusivity. And this moat is practically indestructible, unless the brand itself decides to do so by sacrificing exclusivity and betting only on growth.

Now that the reader has arrived at this point it would be logical if he or she asked: and why should I buy LVMH via Dior when I can go directly to the Paris Stock Exchange and acquire shares of LVMH in the open market? The key is in the discount. Dior now holds 41% of the share capital of LVMH, around 204.75 million of shares of the conglomerate. The current price of LVMH is around €660, this implies a carried value of €134.6 billion, which is higher than Dior's own market capitalization! Since Dior has 180.41 million of shares, I believe the realized value per share of Dior is at least €746, way above its current price of €632. Although there is always the risk that the holding company will sell the shares, it is highly unlikely that this will happen while the Arnault family controls all of Dior and therefore LVMH.

For further details see:

Christian Dior: Buying LVMH At A Discount