PPRUY - Christian Dior: Slowdown Is Here But Long-Term Attractiveness Sustains

2023-10-11 13:04:48 ET

Summary

- Christian Dior reported organic revenue growth of 14% YoY for the first nine months of 2023, but faces challenges including unfavourable exchange rates and a slowdown in demand.

- Despite this, Dior's parent company LVMH saw a stock price decline, while Dior's stock price increased by almost 5% yesterday.

- With some stabilising in U.S. demand and improved prospects for China, the revenue slowdown might not be significant from here, and the price drop has made its P/E attractive.

Luxury fashion company Christian Dior (CHDRF) (CHDRY) reported its revenues for the third quarter (Q3 2023) yesterday. It's clear from these numbers that after bucking the consumer slowdown in the first half of the year, it's now seeing a drag.

But here's the really interesting development. The CHDRF stock was actually up by almost 5% yesterday. This is in contrast with Dior's parent company LVMH (LVMHF)(LVMUY), which also reported the numbers for the same period yesterday, and was down by over 2%.

The close interrelationship between Dior and LVMH, which I've explained earlier , makes this divergence in share price movements particularly curious. Here I take a closer look at the latest numbers to figure out what they, along with Dior's placement among peers, mean for the stock.

Revenue update

On the face of it, revenue growth is still strong, with 14% year-on-year (YoY) organic growth for the first nine months (9M 2023). This is quite decent, even if it's a come-off from the 20% rise seen for 9M 2022. However, scratch the surface and the challenges begin to appear.

Exchange rates unfavourable

The first challenge is an unfavourable exchange rate, which has dragged down reported growth by 4 percentage points to 10% in the latest 9M. By comparison, the currency effect was positive to the tune of 8 percentage points in 9M 2022, when reported growth was an impressive 28%.

While exchange rate movements are outside any company's control, in so far as they impact a company's earnings, they can't be overlooked. Also, if organic growth had improved instead, the currency effect wouldn't have looked as glaring.

{kind=link}

Q3 2023 sees a sharp slowdown

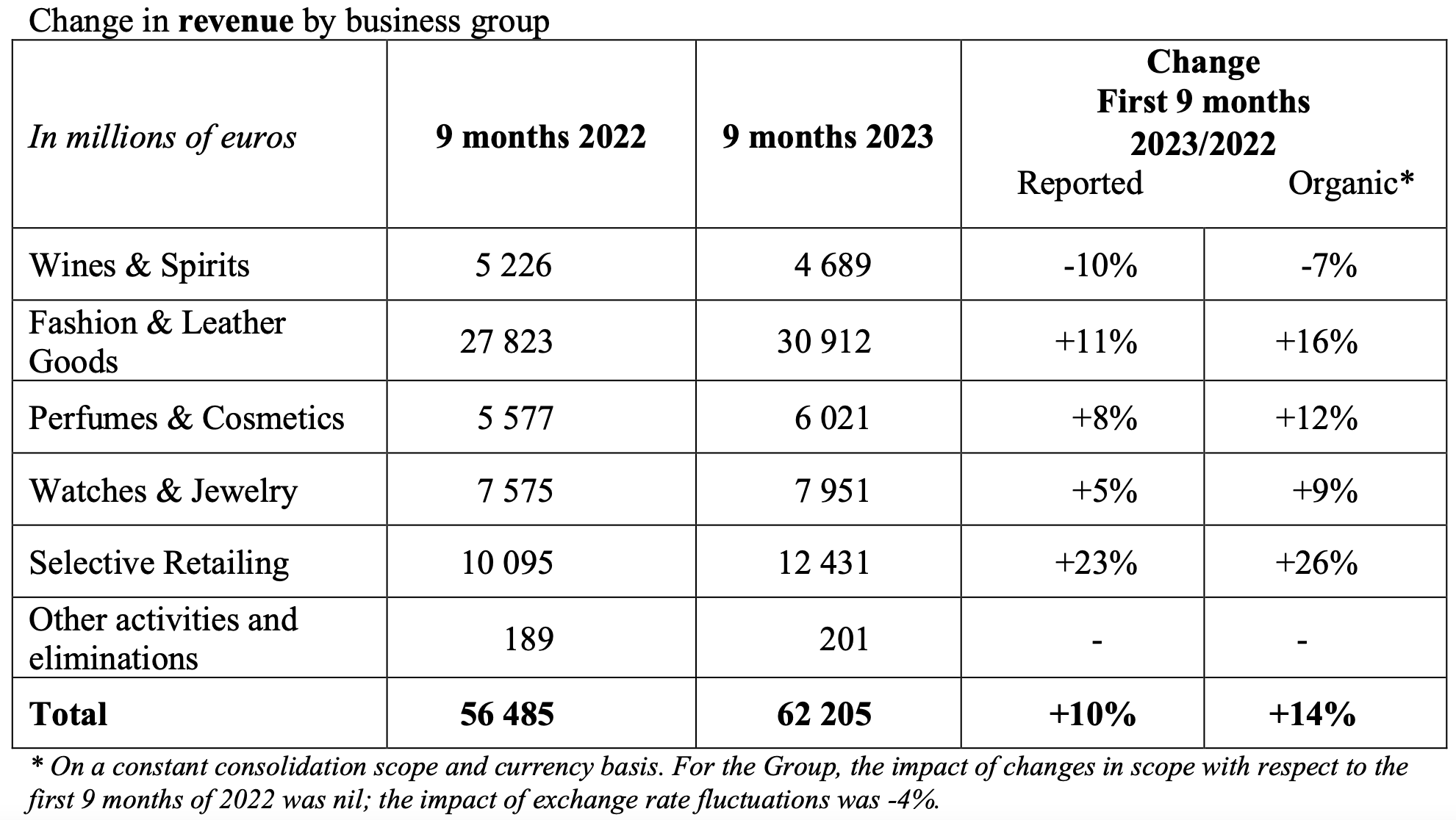

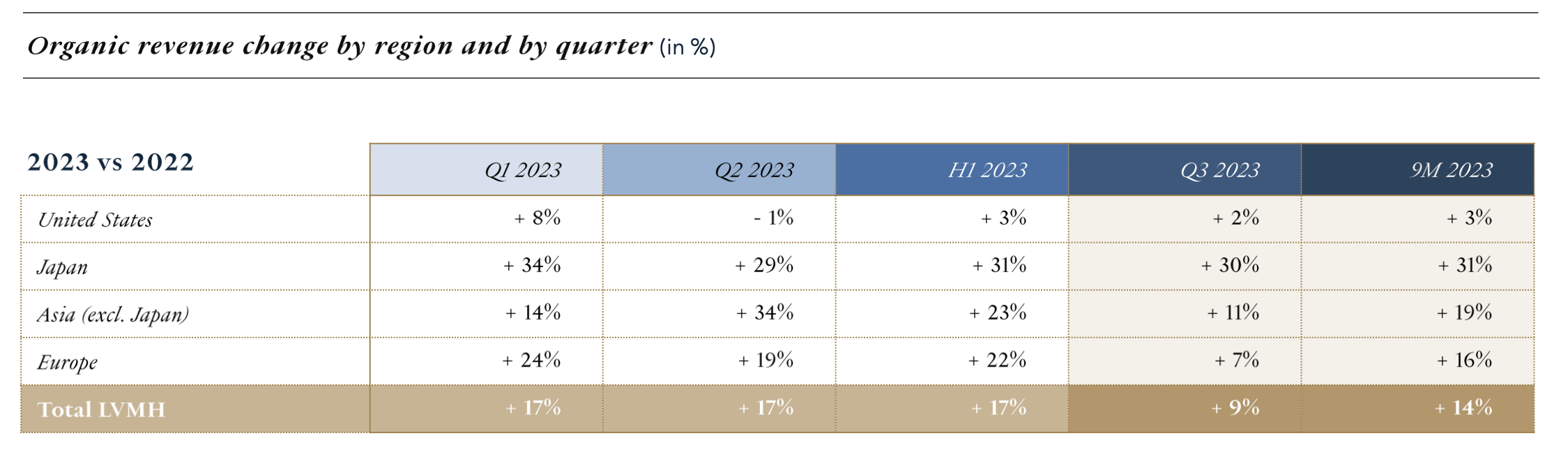

Zooming into the numbers for the latest quarter reflects just how far genuine demand has slowed down. In Q3 2023, organic revenue growth slowed down to 9%, compared to a growth of 17% each during Q1 and Q2, on a broad-based decline across categories, except Selective Retailing. The Wines & Spirits segment has been particularly affected (see table below). There's also an expected slowing down from Q3 2022 when revenues grew by 19%.

Asia and Europe sales slowdown

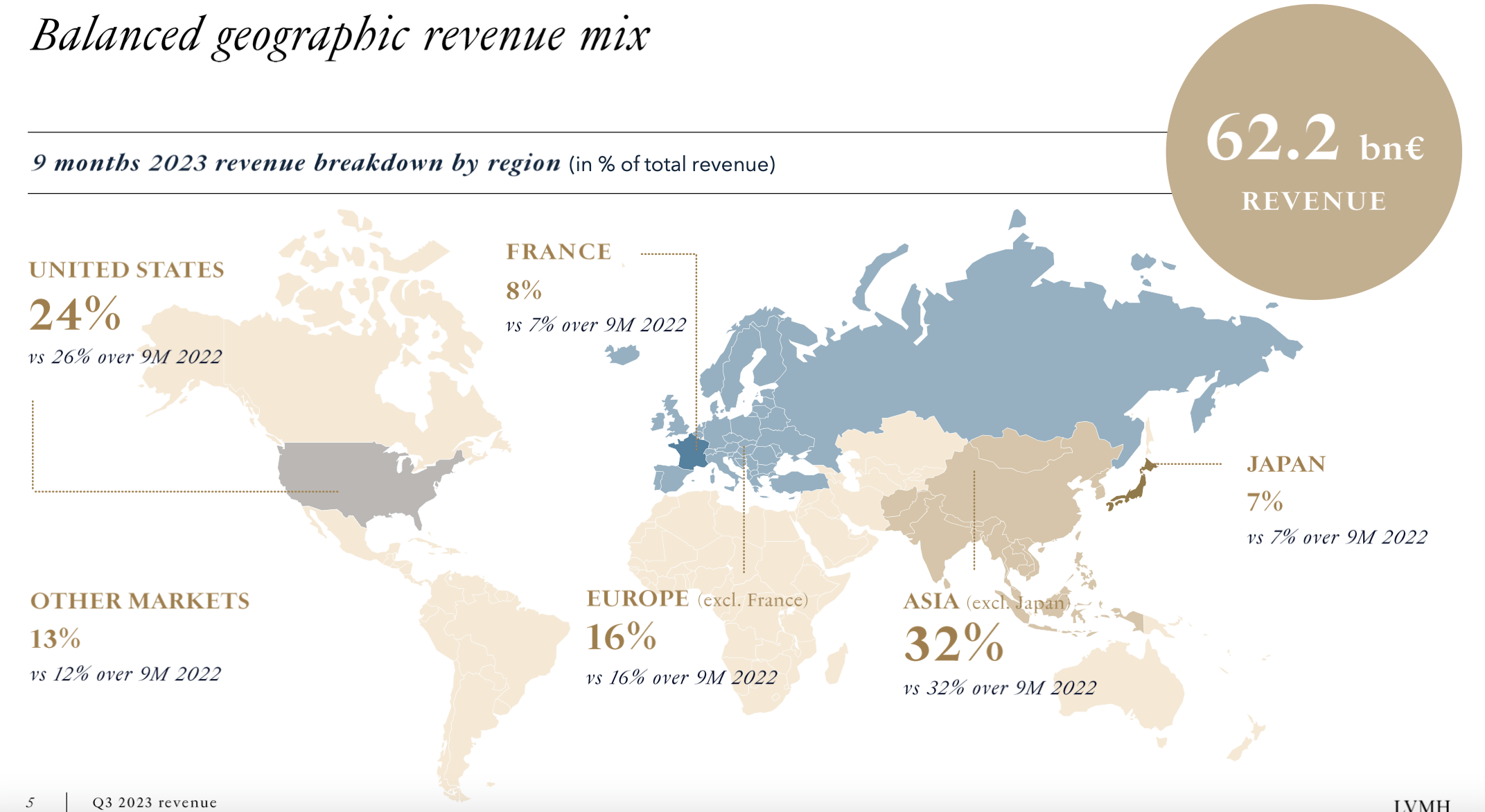

While Dior itself doesn't provide a breakdown of revenues by geography, LVMH does. Considering their revenue numbers are the same, they show the trends for Dior as well. There are two key weak regions visible now.

The first is Asia, where growth has slowed down to just 11%, halving from the first half (H1 2023). More concerning is the fact that the region's softening growth is on a low base. In Q3 2022, it had shown just 6% growth on China's lockdowns. This indicates that the market is indeed cooling off faster than anticipated, and concerns about it might just be on point.

{kind=link}

Next, the Europe market has also seen growth come off to 7%, a third of the H1 2023 rise. Some of this was anticipated on a high base for last year, but warnings of genuine weakening trends in the market have been sounded off recently as well.

It's not all bad

However, the report doesn't necessarily imply that there's more pain in store. There are two reasons why. One, surprisingly, organic growth in the US has picked up a little to 2% after contracting by 1% in Q2 2023. Second, there are now signs of more stabilisation in China's economy as well (read discussion on 'Improved prospects for China' in the link).

This indicates that revenue growth in Asia and the US might not slow down further, even as its European market with a 24% share in revenues could continue to soften.

{kind=link}

The outlook and market multiples

However, in light of the latest come-off, it's essential to relook at the outlook for the full year 2023 now and what it means for market multiples.

Reduced forward estimates

My estimates indicate that in USD terms, revenue growth can slow down to 8.6% in 2023, down from 11.2% for 9M 2023. This is based on the assumption that growth in Q4 2023 remains the same reduced levels as seen in Q3 2023. I've assumed, however, that the net profit margin will stay elevated at the H1 2023 level of 8.3%, considering the softening inflation trends, which can favourably impact costs.

Softening P/E

This results in a forward price-to-earnings (P/E) ratio of 18x for 2023, a slight correction from the 19x last I checked in August. The trailing twelve months [TTM] P/E has declined to 18.7x from 21x in the period, too. Let me put this in perspective.

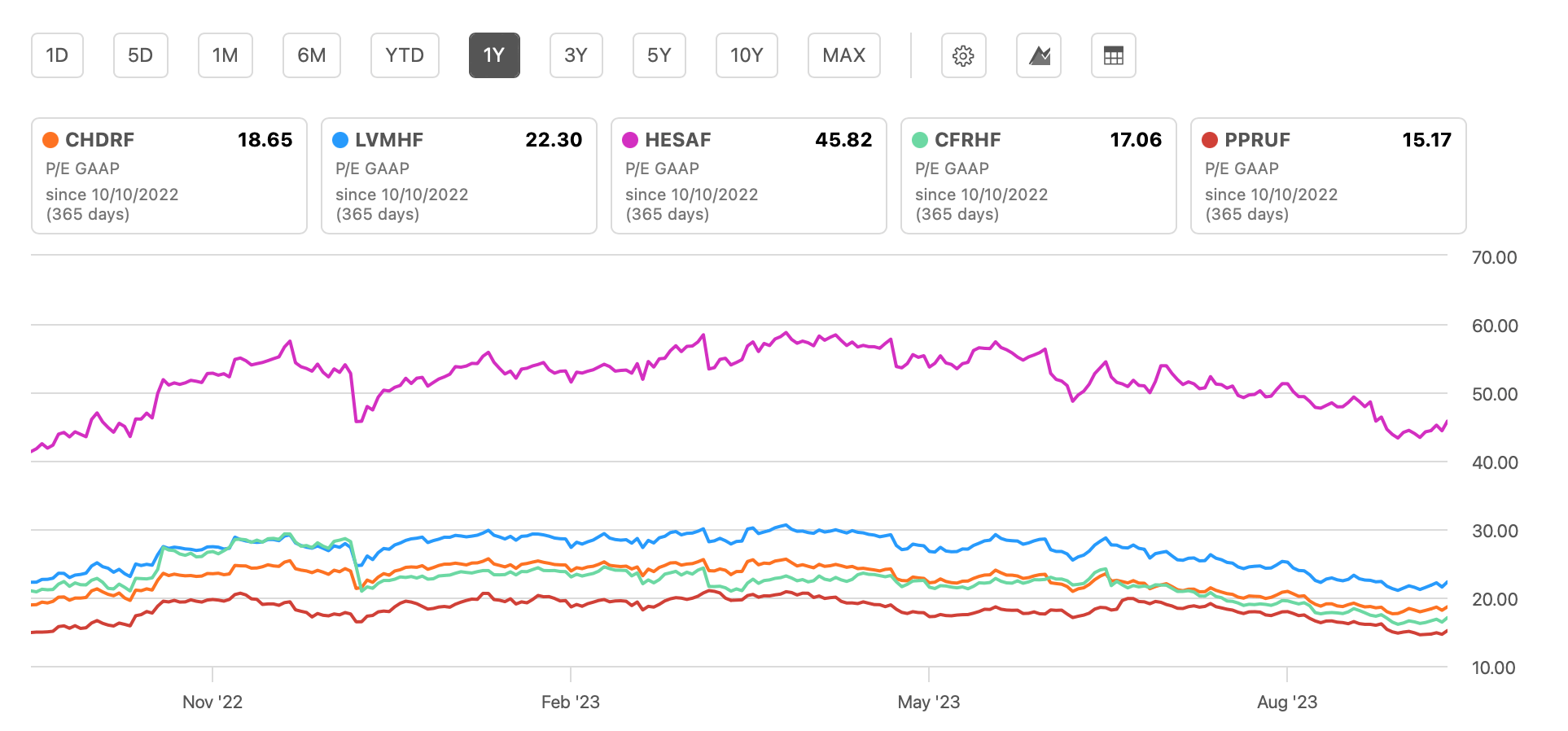

The current TTM P/E is way lower than the median of 29.6x for the 2018-22 period. But here's the real rub. Each time in the past the stock has touched around these levels or lower, it has risen from there (see chart below).

{kind=link}

Comparison with peers

Also, it's worth noting that Dior's TTM P/E is also lower than that of LVMH at 22.3x, which explains why its price continued to rise yesterday even as LVMH fell. The gap between the two can be explained by LVMH being more liquid than Dior, but it still does make the latter more attractive. Particularly now, when Dior's lead against peers like Richemont (CFRHF) and Kering (PPRUF) is far less compared to LVMH (see chart below).

{kind=link}

What next?

Risky as it sounds to maintain a buy on Christian Dior at a time when its price has fallen by 17% in the past six months and revenue growth is slowing down, I think there are very good reasons to Buy it even now.

Its long-term price performance continues to be solid with over 300% rise in the past decade, which improves to 375% when considering total returns. Its current P/E ratio is also at levels that have historically indicated that an uptick is due. The stock also looks competitive compared with LVMH, which is a very similar stock at a higher price.

Even with reduced forward estimates, its forward P/E for the full year 2023 has also improved from the last time I checked. There could be fluctuations over time, but I reckon over the long-term, Dior won't disappoint.

For further details see:

Christian Dior: Slowdown Is Here, But Long-Term Attractiveness Sustains