EAT - Chuy's: Improving EBITDA Margins Should Lead To 50% Potential Upside

Summary

- Chuy's Holdings has successfully improved both sales and EBITDA margins over the past couple of years.

- These improvements have not been reflected in the share price, as Chuy's stock is roughly flat on the year and since its 2017 IPO.

- The improvement in EBITDA margin means that Chuy's Holdings is undervalued compared to peers on an EV/EBITDA basis, so we anticipate a 50% potential upside in the share price from current levels.

Thesis

Chuy's Holdings, Inc. ( CHUY ) is a solid restaurant business that is growing at robust levels and has managed to significantly improve its EBTIDA. It is undervalued compared to peers on an EV/EBITDA business; expect around 50% potential upside in the share price given the improving margins and continued increase in sales growth.

Twitter

Intro

CHUY is a full-service restaurant concept providing a menu of Mexican and Tex-Mex inspired food, founded in Texas but now operating with around 100 restaurants across a number of states. The company currently has an EV of around $600m, and the stock price has been roughly flat on the year, although it has been gradually increasing more recently, up 25% in the past month. On the other hand, the stock price is almost the same as it was when the company IPO'd in 2017 at $22, despite the company growing significantly since.

{kind=link}

Financial Improvements

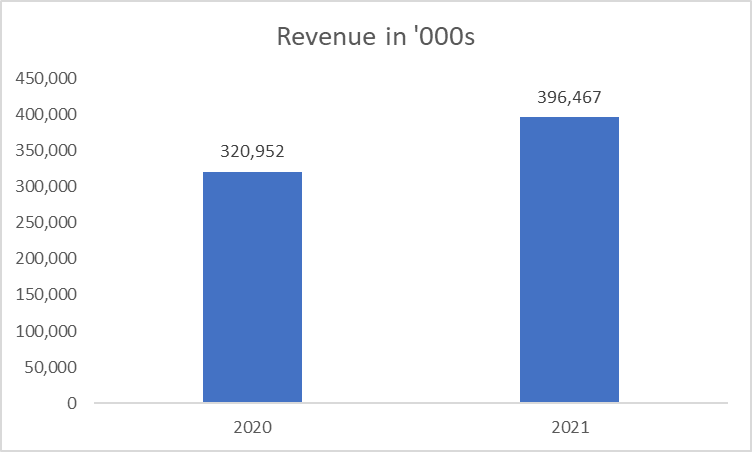

Over the past couple of years, CHUY has managed to greatly improve both sales and margins. Sales grew 24% between the 2020 and 2021 fiscal years, growing from $320m to almost $400m.

{kind=link}

Sales growth has continued in 2022, albeit at a lower growth rate, where sales in the last quarter only grew about 3% compared to the same period a year prior. Despite the slowdown, one could say this is still a reasonable growth rate given that inflation is currently double-digits, and peer-group restaurants have had a lower growth rate in sales according to the latest quarterly report from CHUY.

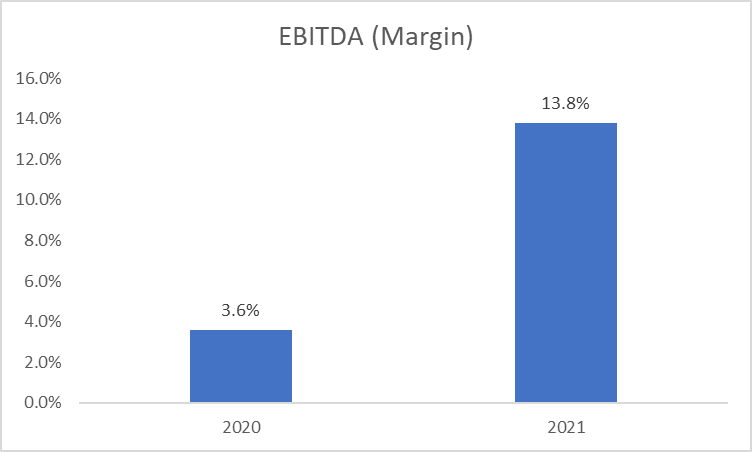

In terms of profits, CHUY significantly improved their bottom line between 2020 and 2021, improving its EBITDA margin from 3.6% to 13.8%.

{kind=link}

This number exceeds peers, where companies like Texas Roadhouse only achieved an 11.5% EBITDA margin and Red Robin Gourmet Burgers only managed around 5%.

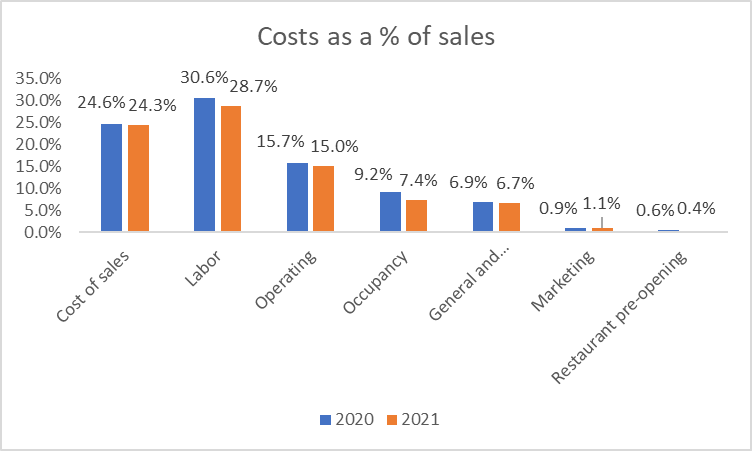

The improvement in EBITDA can be attributed to an increase in revenue as well as an improvement in costs across the board.

{kind=link}

The only costs not to improve are Marketing and Restaurant pre-opening, but these costs are a fraction of the total cost. Improvements were made in labor costs due to sales leverage and a reduction in hourly employees and store management personnel. Significant cost savings were also made elsewhere due to an improvement in the restaurant menu, where the company switched to a limited menu and eliminated the costly complimentary buffet-style foods such as chips or salsa, which led to excessive costs. These cost improvements led to a vital increase in the EBITDA margin.

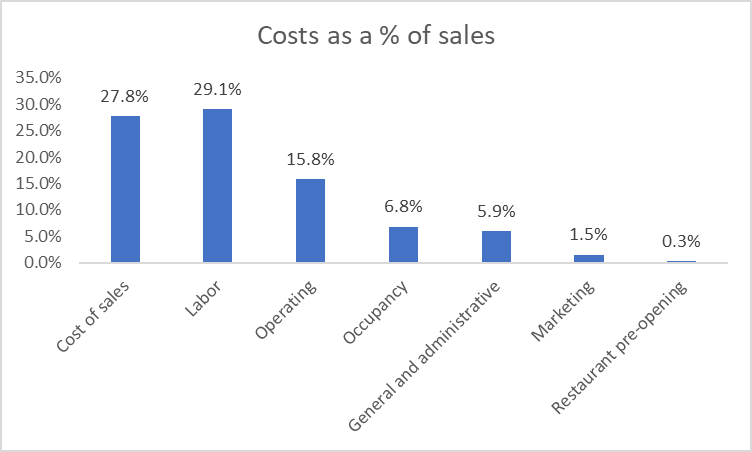

These costs were maintained all the way through to the most recent quarter ending July 2022. Items such as Labor, Occupancy, and G&A improved, but unfortunately operating costs and cost of sales increased. On the other hand, the cost of sales increase was expected to increase substantially given the current economic climate and high input costs, so a higher figure would have been expected and 27.8% is still positive despite the rise.

{kind=link}

However, one thing to note here is that marketing expenses are a little low at 1.5% of sales. Although this has increased from 0.9% in 2020 and 1.1% in 2021, so clearly the company is gradually increasing its marketing budget, this should lead to improved sales (although it much depends on what the marketing strategy is).

Valuation

These improvements in costs, sales, and margins have not been properly reflected in the share price of the company. Investors clearly are not seeing these improvements, and, therefore, the stock remains undervalued.

Looking at a public peer group of restaurant companies of Bloomin' Brands, Inc. (BLMN), Brinker International, Inc. (EAT), The Cheesecake Factory Incorporated (CAKE), BJ's Restaurants, Inc. (BJRI), Red Robin Gourmet Burgers, Inc. (RRGB) and Texas Roadhouse, Inc. (TXRH), CHUY is underperforming in share price but beating on financials. This is the same peer group CHUY uses in their own analysis in their 10-K, illustrating that CHUY's share price has underperformed not only the select peer group but also the indices such as S&P 600 Restaurants and the NASDAQ.

SEC

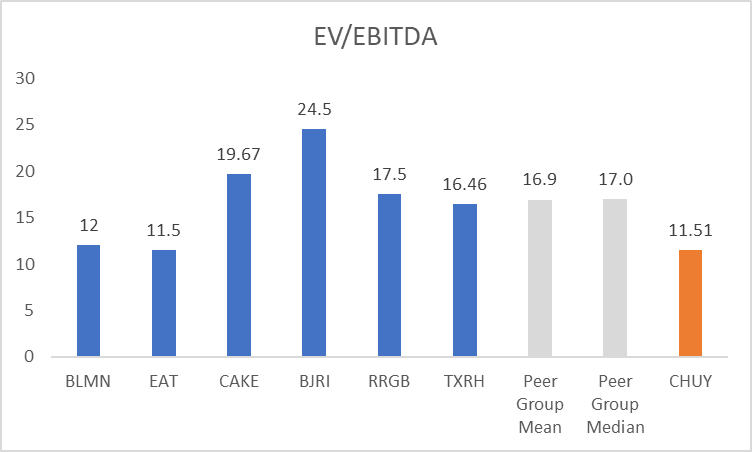

But when we look specifically at valuation ratios, the peer group gives an average EV/EBITDA of around 17, compared to CHUY, which is currently trading at just under 12x EBITDA.

{kind=link}

This indicates that CHUY is undervalued and has a potential upside of around 50% from current levels, and potentially more if improvements are continued in sales growth and cost efficiencies.

Risks

• Foodservice is an industry notorious for its low margins and instability in times of crisis. Given that inflation is substantially high right now, and is expected to stay elevated for a while, we could see input costs for the company continue to rise in the near future, putting pressure on the bottom line and bringing EBITDA margin back down to a much lower level.

• Given that the Fed is raising rates and the base rate is expected to hit between 4 and 5% next year, we could see this have a spillover effect into other costs, such as labor and energy costs, leading to both an increase in the cost of sales and labor costs, again putting pressure on EBITDA margin and adding risk to the current valuation.

Conclusion

In conclusion, CHUY has been successfully improving both their topline and bottom line and has become a strong restaurant brand with 100 outlets across several states, a well-diversified portfolio. These improvements in costs have led to a significant improvement in EBITDA margin, achieving over 13% compared to less than 5% in 2020, but these improvements have not been reflected in the company's share price. This has resulted in CHUY being undervalued compared to peers on an EV/EBITDA basis, leading to a potential upside of around 50% from current levels.

For further details see:

Chuy's: Improving EBITDA Margins Should Lead To 50% Potential Upside