PTY - CIF: Small High Yield CEF From MFS

Summary

- MFS Intermediate High Income is a fixed income closed-end fund.

- The vehicle invests in a portfolio of fixed-rate U.S. high yield bonds.

- The fund has a granular, diversified composition, but has a very small AUM of only $33 million.

- The CEF displays a middle-of-the-road historic performance and significantly lags the gold standards in the HY CEF space.

Thesis

MFS Intermediate High Income (CIF) is a closed end fund from MFS asset management. The fund is on the very small side with only $33 million in assets, however it has been in the market for over two decades. A retail investor needs to be acutely aware of the low volume traded in this name and plan any purchase or exit very carefully. With a 9.5% managed distribution rate and monthly dividends, the fund checks the boxes for the CEF structure.

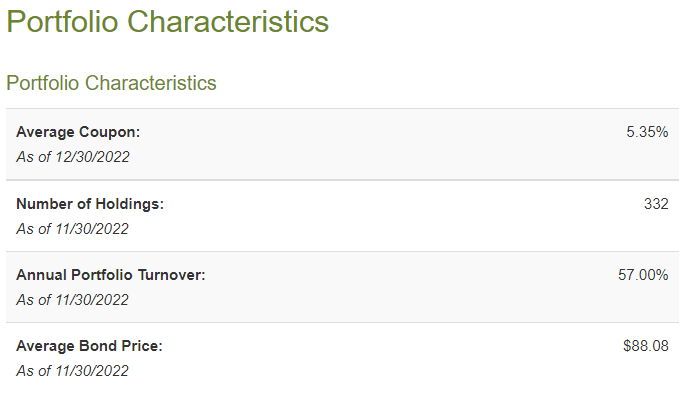

The CEF has current income as its primary objective, and as collateral a portfolio of U.S. high yield bonds. The portfolio has a duration of 5.8 years, and has a very granular build. The fund, however, has a middle of the road to a bottom of the quartile performance. The CEF lags substantially premier HY CEFs in the space, namely PIMCO Corporate & Income Opportunity Fund ( PTY ) and the Credit Suisse Asset Management Income Fund ( CIK ). When we look and analyze a small closed end fund such as CIF we would like to see outperformance, otherwise this fund gets lost in a sea of other names and does not stand-out. Even worse, due to its size it exhibits illiquidity and lacks the appeal of larger funds.

There is nothing wrong with CIF, but there is nothing really good either. Its small size makes it a challenging name to enter / exit, but on the other hand the managers have been successful in keeping its discount to NAV very low via share repurchases.

Analytics

AUM: $33 million

Discount to NAV: -5%

Z-Stat: -1.8

Yield: 9.9%

St Dev (5Y): 12

Sharpe Ratio (5Y): 0.03

Performance

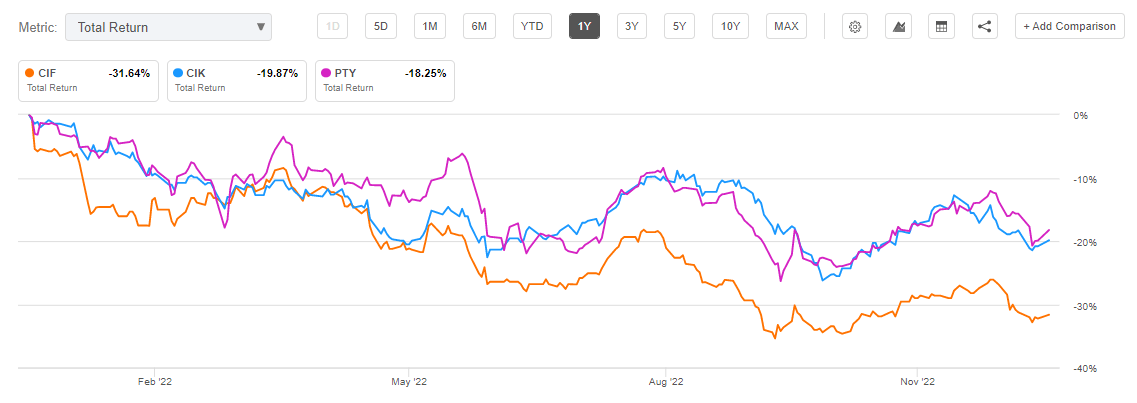

The fund has had a very poor performance in the past year when comparing the name with some of the premier HY CEFs in the space:

{kind=link}

We can see that on a total return basis CIF is down over -30%, while the PIMCO Corporate & Income Opportunity Fund and the Credit Suisse Asset Management Income Fund are down only around -18%. That puts CIF in a lower performing cohort.

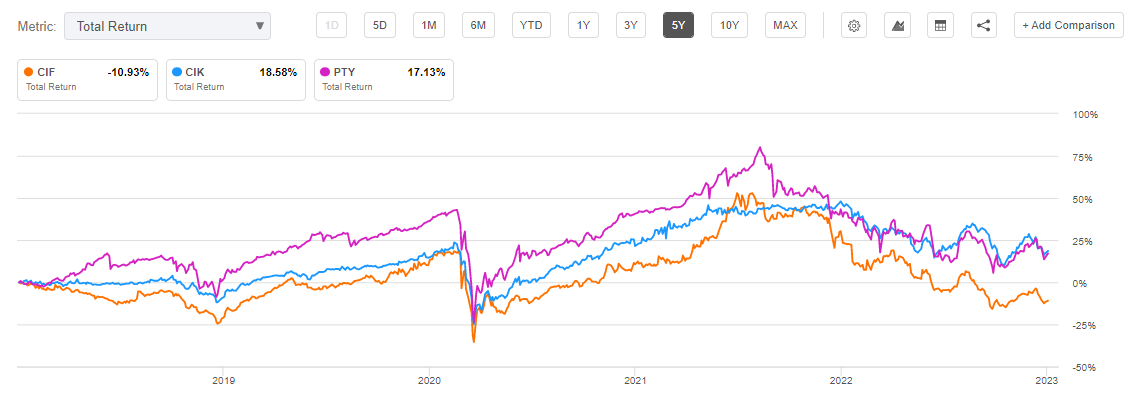

The story is similar on a 5-year basis, where CIF is at the bottom of the performance graph:

{kind=link}

What is most striking though is the fact that the CEF never outperformed its peers in any period of time in the analyzed time-frame.

Holdings

The fund's portfolio is entirely composed of corporate bonds. The vehicle has a run of the mill credit rating composition, with the majority of the names in the 'BB' bracket:

Ratings (Fund Fact Sheet)

The portfolio is granular, with over 100 names in its composition:

{kind=link}

The top names in the portfolio currently are:

Top Holdings (Fund Website)

We can see the CEF having a position in the iShares generic HY ETF.

Premium/Discount to NAV

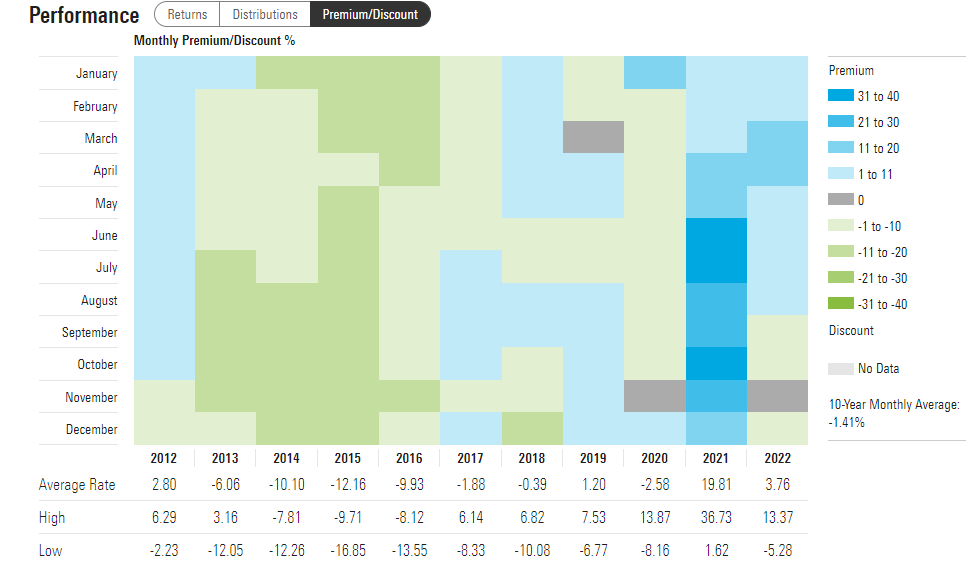

The fund has a mixed performance when it comes to premium / discount to NAV:

{kind=link}

We can see from the historical chart, courtesy of Morningstar, that the CEF alternates between discounts and premiums. We saw a massive premium in 2021 for example when rates were close to zero. We do not think this fund warrants a premium, and we think the low liquidity in the name is responsible for the respective moves. The fund's performance (outside of 2019) puts it in a middle of the pack HY cohort, thus not displaying any redeeming qualities to make this name a premium fund.

The vehicle however has done a number of share repurchases to manage its discount:

{kind=link}

We like this type of corporate action, but clearly the low trading volume can be impacted on an outsized basis by share repurchases. Do not buy this fund at a premium if you want to enter the name. Always wait for a discount and manage the low liquidity aspect.

Conclusion

MFS Intermediate High Income is a small HY CEF. The vehicle has been in the market for over 2 decades, but has an extremely small AUM of only $33 million. The fund is composed of mainly fixed rate U.S. high yield bonds, and its portfolio has a granular build with a middle of the road risk profile. This is not a fund with only 20 bonds and 5 industries, but a truly diversified instrument, despite its size. The vehicle has a lower quartile performance, its total returns paling in comparison with PIMCO Corporate & Income Opportunity Fund or the Credit Suisse Asset Management Income Fund. The only significant outlier is the 2019 total return, which clocks in at an eye watering +43%. The fund is trading at a small discount to net asset value of -5%, but has managed to keep it in check via share repurchases. This fund has a decent build and a decent performance, but is too small. There are liquidity issues (think bid/ask) when one invests in such vehicles. We would like to see MFS merge this fund with another bond fund and create a larger, more liquid vehicle. We are on Hold for this name at the present time.

For further details see:

CIF: Small High Yield CEF From MFS