CTVA - CII: Sustainable 6.66% Yield Potential For Outperformance Over Next 6 Months

2023-06-05 14:44:06 ET

Summary

- Investors today are in desperate need of income to maintain their lifestyles in the face of the rapidly rising cost of living.

- BlackRock Enhanced Capital and Income Fund Inc invests in a portfolio of common stocks and then writes covered call options against the individual stocks to earn a synthetic dividend.

- Despite the CII closed-end fund's description of its strategy, the stock portfolio itself provides very little income for the fund.

- The fund yields 6.66% and this appears to be sustainable due to the fact that option income is repeatable.

- The fund is currently trading at a reasonably attractive valuation today.

There can be little doubt that one of the biggest challenges facing Americans today is the rapidly rising cost of living. This is evidenced by the consumer price index, which purports to measure the price level of a basket of goods that is purchased on a regular basis by an average person. As we can clearly see here, the index has risen by well over the 2% "healthy level" on a year-over-year basis for each of the past twelve months:

{kind=link}

We do see that the rate of price increases is slowing, but as I pointed out in a recent blog post , this is being caused by the falling prices of crude oil and natural gas that we have witnessed over the past few months. When volatile food and energy prices are removed from the index, we see that the annual inflation rate has been little changed over the past several months:

{kind=link}

This has naturally caused people a great deal of budgetary strain, especially those households that possess limited means.

As investors, we are not immune to this as we also purchase food and need money to pay our bills. We do have options available to us that may not be available to everyone, however. After all, we are able to put our money to work for us to earn an income. One of the best ways to do this is to purchase shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are unfortunately not very well followed in the media and many financial advisors are unfamiliar with them. As such, it can sometimes be difficult to obtain the information that we would like to have to make an informed investment decision. This is a shame as these funds offer a number of advantages over open-ended funds and exchange-traded funds. In particular, a closed-end fund is able to use certain strategies that allow it to boost the effective yield of its portfolio well beyond that of anything else in the market.

In this article, we will discuss the BlackRock Enhanced Capital and Income Fund Inc ( CII ), which is one CEF that could be attractive for those that are seeking to earn a substantial level of income from the assets in their portfolios. As of the time of writing, this fund boasts an impressive 6.66% yield, sufficient to allow a $1 million portfolio to earn a bit more than $66,000 per year in annual income. When combined with Social Security, that should be enough to allow a retiree to live a comfortable lifestyle just about anywhere in the nation. I have discussed this fund before, but a few months have passed since that time so naturally several things have changed. This article will focus specifically on these changes as well as provide an updated analysis of the fund's financial condition.

About The Fund

According to the fund's webpage , the BlackRock Enhanced Capital and Income Fund has the stated objective of providing its investors with a combination of current income and capital appreciation. Interestingly, though, this is not specifically stated on the webpage as most BlackRock funds provide. Rather, we have to consult the fact sheet , which describes the fund thusly:

Enhanced Capital and Income Fund, Inc. seeks to provide investors with a combination of current income and capital appreciation. The fund seeks to achieve its investment objective by investing primarily in a diversified portfolio of common stocks in an attempt to generate current income and by employing a strategy of writing (selling) call options on equities in an attempt to generate gains from option premiums.

This fund is therefore a covered call fund, which is not particularly surprising considering that most funds whose names include the word "enhanced" employ some sort of options strategy to boost their effective return. At first, the fact that this fund uses a covered call strategy may worry some risk-averse investors. After all, we have all heard about the inherent risks regarding options. However, covered call strategies are relatively safe to use. This is because the fund already owns the stock that it is writing the option against. The worst-case scenario is that the option will be exercised against the fund and it will be forced to sell some of the stock that it already owns. This is very different from writing a naked call option, as that scenario may require the fund to go out and buy the stock required by the option, potentially paying an enormous price and suffering an enormous loss to do so. If executed correctly, a covered call strategy will never require a fund to realize a capital loss since the option's strike price could be set in such a way that even a forced sale will earn a capital gain. Thus, investors should not have to worry too much about the option-related risk here.

As might be expected from a covered call fund, the BlackRock Enhanced Capital and Income Fund is invested almost entirely in common stock:

CEF Connect

This makes sense as the strategy is to own a common stock and write call options against it. This is a pretty good strategy right now due to the overall uncertainty in the economy. Analysts and investors widely expect the economy to descend into a recession during the second half of 2023. This is being driven by the fact that numerous indicators of manufacturing performance are showing weakness and even the latest jobs reports are coming in weaker than they were a few months ago. This could be expected to result in a market decline over the next few months. The fact that this fund employs a covered call writing strategy helps to limit its losses in such an environment because the collected call premiums offset some of the stock price declines. We saw this in 2022 as the fund outperformed the S&P 500 Index ( SP500 ):

{kind=link}

For comparison purposes, the iShares Core S&P 500 ETF ( IVV ) lost 18.13% in 2022:

{kind=link}

The fund should also outperform during flat markets due to the option premiums collected from its covered call-writing strategy. The only real problem with the strategy is that it caps the potential gains that can be realized from the stock portfolio. This is because the fund will be forced to sell its stock at the strike price of the option. Thus, this fund will probably underperform during a raging bull market. We can see that in the two charts above as the fund underperformed the market in 2019, 2020, and 2021. However, given the fact that a near-term recession is far more likely than a raging bull market given the weakness of the various economic indicators, this is not really a problem that we have to worry about right now. In fact, the market this year has been pretty much flat except for a few technology and AI-related stocks, so this statement has so far proven correct.

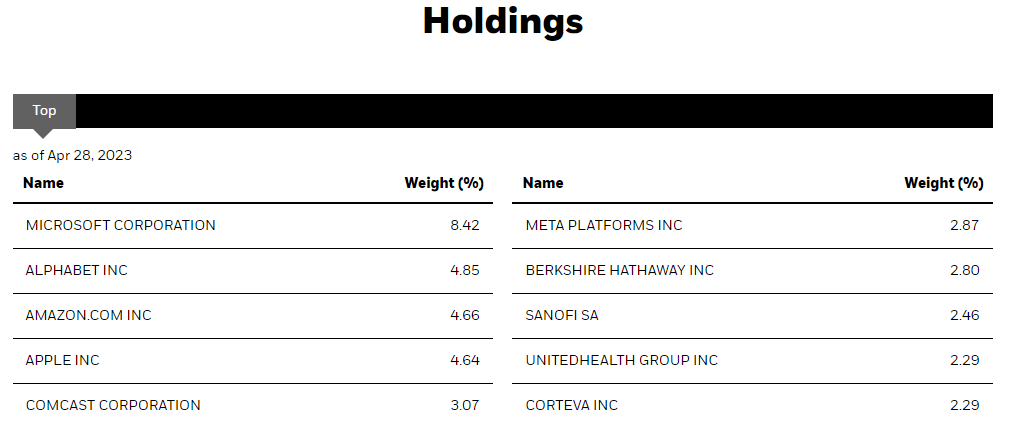

The fact sheet's description of the fund's strategy states that the fund aims to earn current income from the stock portfolio. This implies that the fund will be primarily purchasing dividend-paying common stocks. However, the largest positions in the fund seem to tell a different story. Here they are:

{kind=link}

While some of these companies do, in fact, pay a dividend, there are several on this list that do not. In addition, even some of the stocks that do pay a dividend have such a low yield that they may as well not be paying a dividend at all. We can see that here:

| Company |

| Dividend Yield |

| Microsoft Corporation ( MSFT ) |

| 0.81% |

| Alphabet Inc. ( GOOG ) |

| 0.00% |

| Amazon.com ( AMZN ) |

| 0.00% |

| Comcast Corporation ( CMCSA ) |

| 2.96% |

| Meta Platforms, Inc. ( META ) |

| 0.00% |

| Berkshire Hathaway ( BRK.B ) |

| 0.00% |

| Sanofi SA ( SNY ) |

| 3.73% |

| UnitedHealth Group ( UNH ) |

| 1.32% |

| Corteva ( CTVA ) |

| 1.07% |

As of the time of writing, the S&P 500 Index ( SPY ) yields 1.51% so the only two stocks in the fund's ten largest positions that have a yield exceeding that of the broader market are Comcast and Sanofi. The remainder of the stocks constitutes pretty strange positions for a fund that claims to be seeking current income from its common stock portfolio. While the covered call strategy does allow the fund to earn a synthetic dividend from all of these positions, its description implies otherwise. My guess is that the fund is trying to ensure that its performance is at least somewhat correlated to that of the broader market. As I have pointed out in the past, a substantial proportion of the total gains of the S&P 500 Index over the past fifteen years have come from only a small handful of stocks so any fund would need to hold these stocks to deliver a performance that correlates somewhat to the index. It seems likely that this is one reason for the fund's holdings. Fortunately, all of the stocks that we see above are pretty good from an options perspective so the fund is able to generate solid premium income from them, even if it is not succeeding in its objective of generating current income from the stock portfolio directly.

For the most part, the largest positions in the fund are the same as the last time that we looked at the fund. The sole exception is that Visa ( V ) was removed and replaced with Sanofi. The remainder of the stocks were all among the fund's largest positions a few months ago, but the weightings of many of them have changed significantly. This could easily be explained by one stock outperforming another in the market, though. It is not necessarily a sign that the fund is actively changing its weightings via trading. As such, we might assume that this fund has a fairly low annual turnover. This is certainly true as the fund's current 32.00% turnover is fairly low for an equity closed-end fund. The reason that this is important is that it costs money to trade stocks or other assets, which is directly billed to the shareholders of the fund. This creates a drag on the fund's performance and makes management's job more difficult. After all, the fund's managers will need to earn sufficient excess returns to both cover these costs and still have enough left over to provide a return sufficient to satisfy the shareholders. That is a task that few management teams are able to achieve on a regular basis and it generally results in actively-managed funds underperforming their benchmark indices.

As we have already seen, this one tends to outperform during flat or bear markets but fails to match the index during raging bull markets. This is exactly what we would expect given the fund's strategy. It is nice to see that management is limiting its turnover though, as that should mean that more money is available for the shareholders.

Distribution Analysis

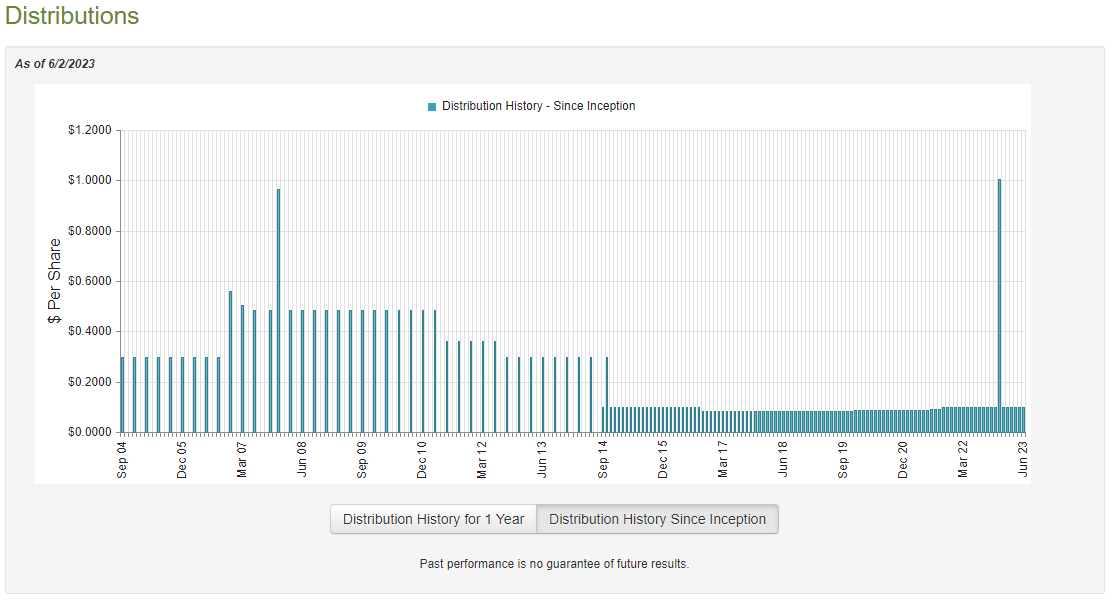

As mentioned earlier in this article, the BlackRock Enhanced Capital and Income Fund has the stated objective of providing current income and current gains to its investors. As is usually the case with closed-end funds, the fund will pay both its income and gains out to the shareholders, which boosts the yield received by the shareholders. As such, it might be expected that this fund will boast an impressively high yield. This is certainly the case as the fund pays out a monthly distribution of $0.0995 per share ($1.194 per share annually), which gives the fund a 6.66% yield at the current price. For the most part, the fund has been reasonably consistent with its payout over time but it has had some variations:

{kind=link}

As we can see, the fund has been increasing its distribution since 2019. That is something that will likely appeal to those investors that are seeking a safe and secure source of income with which to use to pay their bills or otherwise finance their expenses. This is not an unusual situation for a covered call fund, as the covered call strategy is reasonably reliable as an income source. As is always the case though, we want to ensure that the fund can actually afford the distribution that it pays out since we do not want to find ourselves the victims of a distribution cut. This is because a cut would reduce our incomes and almost certainly cause the fund's share price to decline.

Fortunately, we do have a fairly recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on December 31, 2022. As such, this report will not include any information about the fund's performance over the past few months. However, it will still give us a great idea of how it handled the very challenging conditions in the market during 2022. During the full-year period, the BlackRock Enhanced Capital and Income Fund received $10,532,392 in dividends and surprisingly nothing in interest.

When we net out the foreign withholding taxes that the fund had to pay, it had a total investment income of $10,392,441 during the period. The fund paid its expenses out of this amount, which left it with $2,696,846 available for shareholders. As might be expected, this was nowhere close to enough to cover the $92,693,757 that the fund actually paid out in distributions over the course of the year. At first glance, this might be concerning as the fund's net investment income was nowhere close to enough to cover the distributions.

However, the fund does have other methods through which it can obtain the money that it needs to finance the distribution. For example, the premium income that it receives from the covered call writing strategy is not included in net investment income. Neither are capital gains that the fund realizes on the common stock portfolio. However, both of these things do represent money coming into the fund that could be distributed to the investors. Over the full-year period, the fund achieved net realized gains of $100,213,617 but this was more than offset by $211,028,139 net unrealized losses.

Overall, the fund's assets declined by $200,811,433 after accounting for all inflows and outflows. That is certainly concerning, but the fund's capital gains were more than enough to cover the distribution. This is something that is nice to see, particularly since a significant portion of this fund's capital gains is received option premiums, which are generally repeatable over extended periods of time. Thus, the fund's distributions are probably reasonably safe, although we will still want to keep an eye on it to ensure that it makes back the capital losses that it suffered last year.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a sure-fire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the BlackRock Enhanced Capital and Income Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are obtaining the fund's assets for less than they are actually worth. Fortunately, this is the case with this fund today. As of June 2, 2023 (the most recent date for which data is available as of the time of writing), the BlackRock Enhanced Capital and Income Fund has a net asset value of $18.59 per share but the shares currently trade at $17.92 each. This gives the fund's shares a 3.60% discount to net asset value at the current price. That is relatively in line with the 3.86% discount that the shares have had on average over the past month. Thus, the price certainly appears to be reasonable today.

Conclusion

In conclusion, the BlackRock Enhanced Capital and Income Fund appears to be a decent way to earn a high level of income while still maintaining exposure to the stock market. The fund admittedly will underperform during a raging bull, but the second half of the year seems unlikely to bring such an environment given the factors working against such an occurrence. The fund should outperform in a flat or bear market though, which could be nice today. BlackRock Enhanced Capital and Income Fund Inc appears to be able to maintain its current 6.66% yield and boasts a reasonably attractive valuation, so it might be worth considering adding to your portfolio today.

For further details see:

CII: Sustainable 6.66% Yield, Potential For Outperformance Over Next 6 Months