JNK - CIK: Shares Of This Junk Bond CEF Are Trading At An Unjustifiable Price

2023-12-27 08:31:19 ET

Summary

- The Credit Suisse Asset Management Income Fund has a yield of 8.71%, lower than some other funds investing in fixed-income securities.

- The fund's share price has increased by 19.69% since October 9, outperforming major bond indices.

- The fund's distribution yield is 8.71%, but it failed to fully cover its distributions with net investment income, relying on unrealized gains to make up the difference.

- There is a risk that junk bond defaults will increase over the next twelve months despite the impending rate cuts, but this fund appears able to handle that risk.

- The fund's shares have substantially outperformed the portfolio and it looks very expensive right now.

The Credit Suisse Asset Management Income Fund (CIK) is a closed-end fund that income-seeking investors can purchase as a way to achieve their goals. The fund’s 8.71% yield shows that it certainly has a lot going for it in the area of income generation. However, this is a lower yield than is offered in some other funds that are investing in floating-rate securities, junk bonds, and similar forms of debt. That could be due to the fact that junk bonds have gone up fairly rapidly over the past few weeks as investors attempt to front-run the expected federal funds rate cuts next year. This has resulted in a very inverted yield curve that has caused floating-rate securities to have much higher yields than bonds with maturities out into the future, such as most junk bonds. This dynamic has pushed up the price of funds that invest in traditional fixed-rate bonds and naturally pushed down their yields.

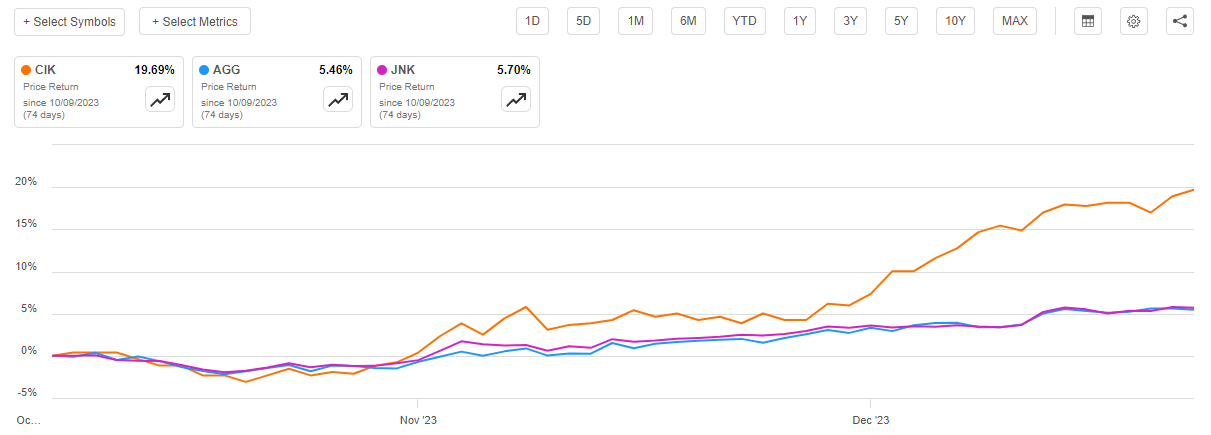

As regular readers may remember, we last discussed the Credit Suisse Asset Management Income Fund in early October. This article was published about a week or two before the bond market turned in earnest and investors started driving yields down and bond prices up. The latter trend has continued to the present day. As such, we might expect that the fund has delivered a very respectable performance for its shareholders since the time that the prior article was published. This is certainly the case, as the fund’s share price is up a whopping 19.69% since October 9:

{kind=link}

As we can clearly see, that drastically outperformed the Bloomberg U.S. Aggregate Bond Index ( AGG ) as well as the Bloomberg High Yield Very Liquid Index ( JNK ). Indeed, this performance difference is enough to suspect that the fund has gotten ahead of itself. After all, there have not been any news releases regarding this fund that have come out over the period. There was certainly nothing that justified that sort of share price appreciation relative to the major indices.

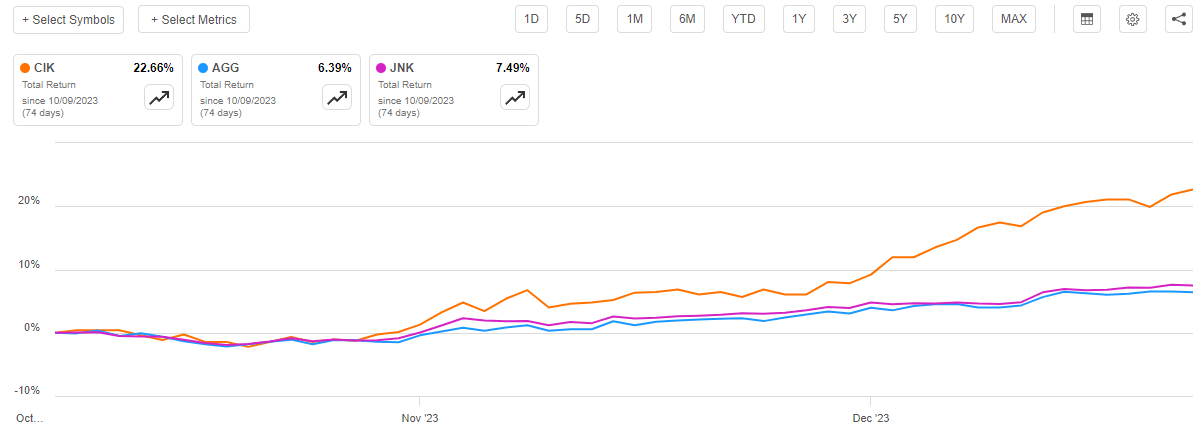

The fund has done even better when we include its distributions in the return analysis. After all, as is the case with most closed-end funds, the Credit Suisse Asset Management Income Fund pays out nearly all of its investment profits to investors in the form of distributions. This results in the actual return being significantly higher than would be reflected simply by looking at the fund’s share price. When we do this, we see that investors in this fund received a very impressive 22.68% over the past two months:

{kind=link}

There are very few securities available in the market today that have delivered a comparable return over such a short period of time. As such, the fund’s recent performance will almost certainly be very appealing to most investors. However, we should investigate it to make sure that its recent performance is justified. After all, if this is just a case of the fund’s share price jumping when its portfolio has not delivered comparable results, then it is unlikely that these gains will hold, and investors purchasing the fund today could end up with losses as the share price falls back to trade in line with the net asset value.

About The Fund

According to the fund’s website , the Credit Suisse Asset Management Income Fund has the primary objective of providing its investors with a very high level of current income while attempting to preserve the value of its principal. This is a very common objective for a fund that invests in fixed-income securities. After all, it is not that difficult to ensure the preservation of principal when investing in these securities. A bond will always pay out its face value at maturity, so anyone who purchases a bond at the face value or less is guaranteed not to lose money unless the issuer of the security defaults. There are, in fact, some funds that simply purchase bonds upon issuance and hold them until maturity. These funds are typically found in retirement accounts sponsored by corporations and are designed for investors who want something that is akin to a savings account at a bank. This fund will not necessarily hold a bond until maturity, as it attempts to earn extra profits by trading bonds and exploiting changes in interest rates, but the concept is the same.

The fund’s website does not provide a great deal of information about the fund’s overall strategy. All it says is:

Under normal circumstances, the Fund will invest at least 75% of its total assets in fixed-income securities, such as bonds, debentures, and preferred stock.

Most of the portfolio invested in U.S. high yield corporate debt, with some exposure to sovereign or corporate debt of developing nations.

As mentioned in my previous article, this strongly suggests that this should be thought of as a junk bond fund. We can see this further by looking at the credit ratings that have been assigned to the securities in the fund. Here is a high-level summary:

Fund Fact Sheet

An investment-grade bond is anything that is rated BBB or higher. As we can clearly see, that only describes 4.94% of the assets that are currently held by the fund. The remainder of the portfolio is invested in debt securities that are considered junk debt. This is something that might be concerning to risk-averse investors, which would apply to many investors who are focused on income generation. After all, we have all heard about the very high risk of losing your money because the issuer of the junk bond defaults.

There is a very real possibility that this risk is increasing due to the fact that interest rates are very close to the highest levels that have been seen so far in the 21st century. According to an article that was published in the Wall Street Journal back in June, junk bond defaults edged up in the first half of 2023. In May 2023, the corporate default rate was 3.4% compared to 3.2% in April. That is still lower than the 4.1% historical default rate, however. Moody’s Investor Service projects that the default rate on junk bonds will continue to increase, peaking at 5.6% in January 2024. From an October 15, 2023, article published by Business Insider:

Moody’s analysts expect the US speculative-grade default rate to peak at 5.6% in January 2024, before easing to 4.6% by August 2024.

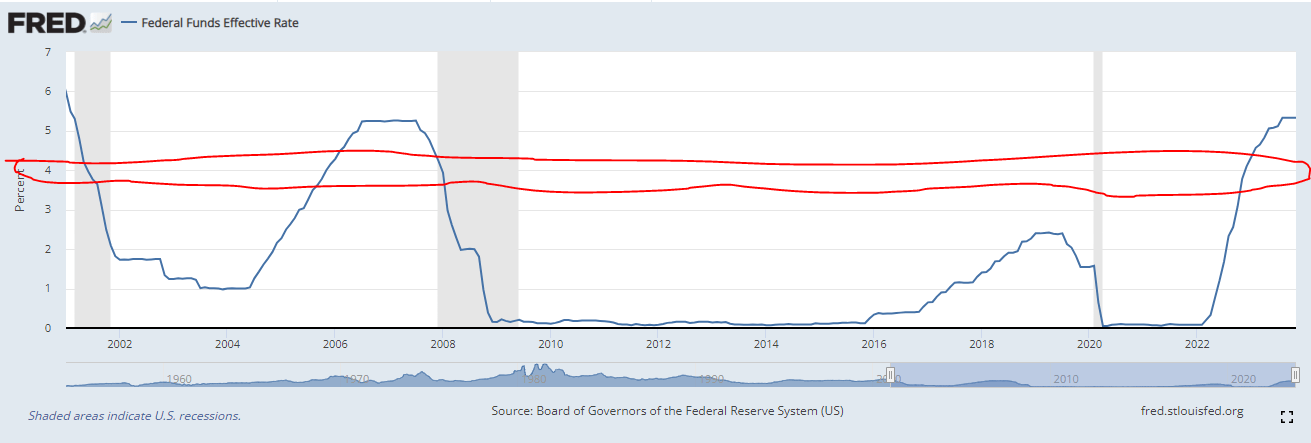

A 4.6% rate would still be well above the historical average for junk bond defaults. Thus, Moody’s analysts seem to expect that the junk bond default rate will remain at levels above the historical average at least through the first half of 2024. However, it will probably remain higher than the 21st century average over the full-year 2024 period. After all, both the market and the members of the Federal Open Market Committee expect that the federal funds rate will finish 2024 well above the average that we saw over most of this century. This chart shows the effective federal funds rate from January 2001 to the present:

Federal Reserve Bank of St. Louis

{kind=link}

I have attempted to circle the range that the market expects the federal funds rate to be at the end of 2024. The membership of the Federal Open Market Committee expects that it will be above this range. My terrible artwork skills aside, we can still see that the federal funds rate will almost certainly remain above the 21st-century average for the next twelve months. This will mean that any junk bond issuer that has to roll over bonds next year will probably have to pay a higher interest rate than they did on the maturing debt. When we consider how many of these companies are barely making enough money to service their existing debt, we can clearly see how the impending increase in interest expenses could push some companies over the edge. If the economy ends up falling into a recession next year, the situation will be even worse.

It is, however, uncertain how accurate Moody’s projection is likely to be. The Business Insider article was published on October 15, 2023, and long-term interest rates have come down considerably since that date. Thus, the actual default rate that we see in 2024 could end up being less than Moody’s projected numbers. This could be especially true if the market continues to hold long-term interest rates very low and makes it easier for speculative-grade companies to refinance. It does still seem likely though that most companies will end up paying higher interest expenses following any debt rollovers and since many of these companies are already pretty close to the edge, those added expenses could push them into financial distress.

That is something that could be concerning to potential investors in the Credit Suisse Asset Management Income Fund. After all, nobody wants to see their risks of loss go up. However, the chart above shows that 71.20% of the fund’s assets are invested in BB-rated and B-rated debt. When we combine that with the 4.94% of its assets that are invested in investment-grade securities, we see that 76.14% of the fund’s assets are invested in B-rated securities or better. According to the official bond ratings scale , companies with these ratings have sufficient financial strength to meet their current obligations even in the event of a short-term economic shock, such as a recession. As such, these companies should be able to avoid defaults in most situations. At the very least, we should not be seeing an outsized number of the companies whose securities are held by the fund defaulting.

In addition to the reasonably high credit ratings of most of the securities in the fund’s portfolio, we also see that it does not have outsized exposure to any individual issuer. Here are the largest positions in the fund's portfolio:

Fund Fact Sheet

As we can see here, the largest position that is held by the fund only accounts for 1.33% of the total portfolio. The yield on any junk bond today is more than enough to erase any losses from a single position very quickly. While it is true that a massive number of defaults in rapid succession could be a risk, that situation would only occur if there were much bigger problems in the economy, so we probably do not need to worry about it too much.

Overall, the biggest risk here is that the market is wrong about the direction of interest rates. As we have discussed in various previous articles, the market is currently pricing 150-basis points of interest rate cuts next year. The Federal Reserve itself states that is unlikely to happen, so there is a risk that bonds will give up some of the gains that they have delivered over the past month or two. That means that anyone buying the fund today might have to eat some capital losses over the next twelve months. That is a risk with any fund investing in fixed-rate bonds though, not just the Credit Suisse Asset Management Income Fund.

Leverage

As is the case with most closed-end funds, the Credit Suisse Asset Management Income Fund employs leverage as a method of boosting the effective yield that it receives from its portfolio. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase junk bonds and similar high-yielding assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. Unfortunately, this strategy is not as effective today as it was two years ago because the difference between the rate at which the fund borrows and the rate that it receives on the purchased assets is narrower than it used to be.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage because that would expose us to an excessive amount of risk. I generally like a fund’s leverage to be under a third as a percentage of its assets for that reason.

As of the time of writing, the Credit Suisse Asset Management Income Fund has leveraged assets comprising 29.76% of its portfolio. This represents a decrease from the 30.95% leverage that the fund had the last time that we discussed it. That is a good sign as it generally means that the fund is reducing its overall leverage and our risk.

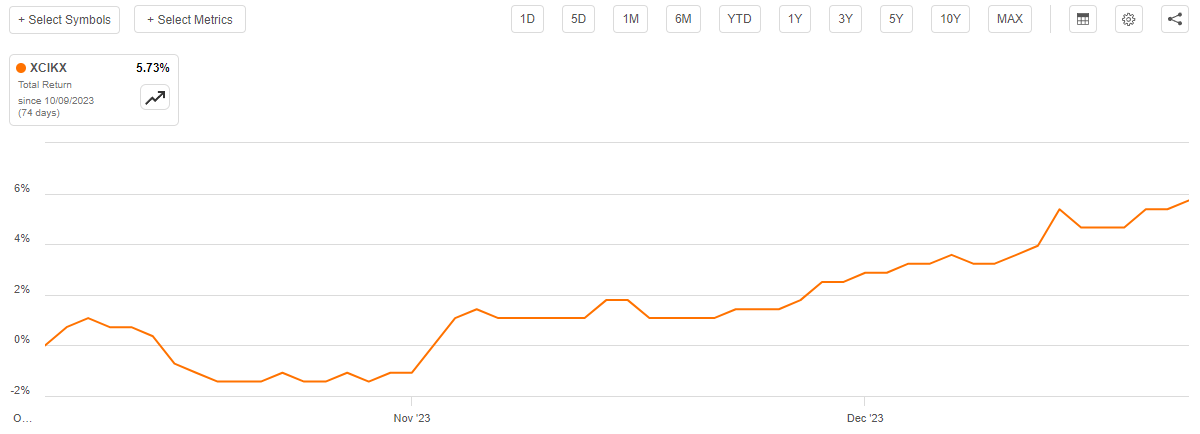

As might be expected, the reason for this decreased leverage is that the fund’s net asset value increased the last time that we discussed it. As we can see here, the fund’s net asset value is up 5.73% from the date that the previous article was published:

{kind=link}

That is curious since this is a lot less than the fund’s share price has gone up over the same period. That could suggest that the strength in the fund’s share price recently is completely unjustified. We will discuss that in more detail later in this article.

For now, the important thing is that the fund’s portfolio is valued at a higher level than it was the last time that we discussed the fund. This had the effect of decreasing the fund’s leverage. After all, if the fund’s leverage remained static but the portfolio is now larger then it would result in the fund having a lower level of leverage.

As was the case the last time that we discussed the fund, its current level of leverage represents a reasonable balance between risk and reward. As such, we should not need to worry too much about the fact that the fund is employing leverage.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Credit Suisse Asset Management Income Fund is to provide its investors with a very high level of current income. In pursuance of this objective, the fund invests primarily in a portfolio of junk bonds. The defining characteristic of junk bonds is that they have remarkably high yields, which are intended to compensate investors for the high risk of defaults associated with these securities. As of the time of writing, the Bloomberg High Yield Very Liquid Index has a yield-to-maturity of 7.78%, which is lower than it used to be, but it is still higher than most other things in the market today. The fund collects the payments that it receives from the securities in the portfolio and borrows money to allow it to collect payments from more bonds than it could with solely its own equity capital. The fund pools all of these payments together with any profits that it manages to collect by trading appreciated bonds prior to maturity, then pays the money out to its shareholders after subtracting its own expenses. We might expect that this would give the fund a very high yield.

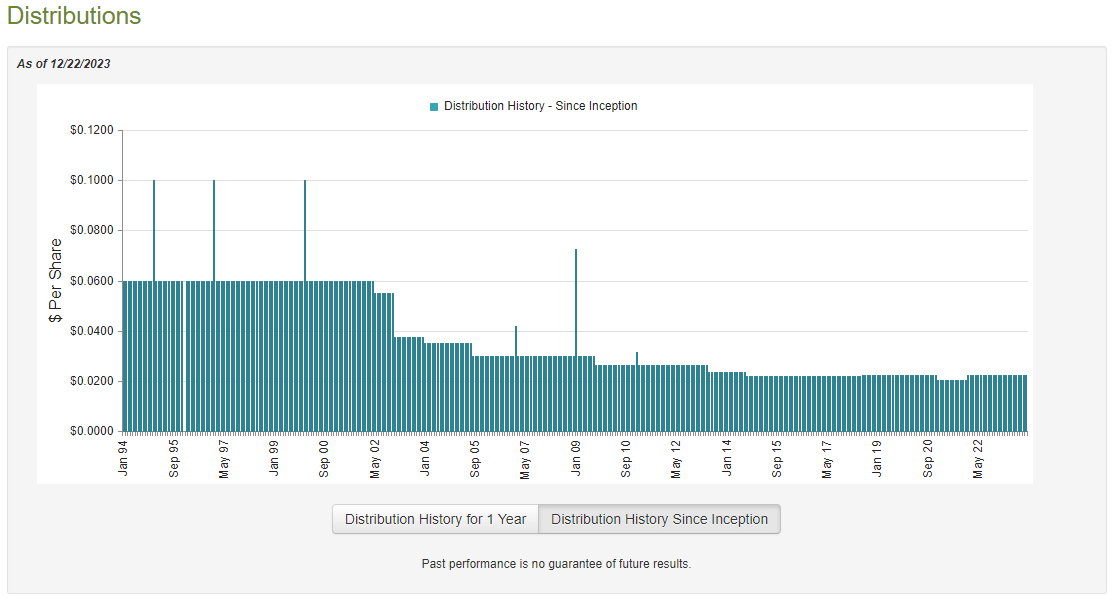

This is certainly the case, as the Credit Suisse Asset Management Income Fund pays a monthly distribution of $0.0225 per share ($0.27 per share annually). This gives it an 8.71% yield at the current share price. That is substantially less than the 10.42% yield that the fund had the last time that we discussed it, which is rather disappointing. It is also somewhat less than some other junk bond funds manage to deliver today. However, the fund still has a higher yield than the broader index as a whole and it yields more than most things that trade in the public markets. The fund has unfortunately not been particularly consistent with respect to its distribution over the years:

{kind=link}

As we can clearly see, the fund’s distribution has varied considerably over its lifetime, although it has been more consistent than many other fixed-income funds since the middle of the last decade. However, the fund’s long-term history might still prove to be a turn-off for some investors who are seeking to earn a consistent level of income from the assets that are in their portfolio. This is one of the few fixed-income funds that did not cut its distribution in response to the 2022 shift in monetary policy that caused bond prices to decline and bond funds to suffer large losses. We should investigate why the fund was able to accomplish a feat that so many of its peers failed to accomplish as we do not want it to be maintaining a distribution that it cannot actually afford and destroying its net asset value in the process.

Fortunately, we have a somewhat recent financial report that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2023. This report is perhaps not as recent as would be ideal due to the fact that the bond market has been volatile since the end date of the report. After all, bond prices fell dramatically over the summer as the market began to price in the fact that interest rates may indeed be “higher for longer.” This trend reversed around the middle of October, and bond prices have been increasing since that time. As such, the fund experienced periods during which it undoubtedly took some losses and had the opportunity to make some gains. This report will provide us with no insight into how it handled these two very different situations, and we will, unfortunately, have to wait a few months for the fund to release its annual report in order to see how it handled the volatility.

During the six-month period, the Credit Suisse Asset Management Income Fund received $8,690,617 in interest from the assets in its portfolio. It had no dividend income but did manage to earn $31,614 in securities lending profits. This gives the fund a total investment income of $8,722,231 during the period. The fund paid its expenses out of this amount, which left it with $6,452,067 available for the shareholders. That was, unfortunately, not enough to cover the $7,106,023 that the fund paid out in distributions over the period. It did manage to get pretty close, but it is still discouraging that the fund failed to fully cover its distribution out of net investment income. That is something that we would normally prefer to see with a debt fund like this one.

With that said, there are other methods through which the fund can obtain the money that it needs to cover the distribution. For example, it might have been able to exploit the changes in bond prices that accompany interest rate swings. Fortunately, it did have some success at this task during the period. The fund reported net realized losses of $9,765,520 but these were more than offset by $15,871,925 net unrealized gains. Overall, the fund’s net assets increased by $5,484,972 over the period after accounting for all inflows and inflows. Thus, the fund did manage to fully cover its distributions.

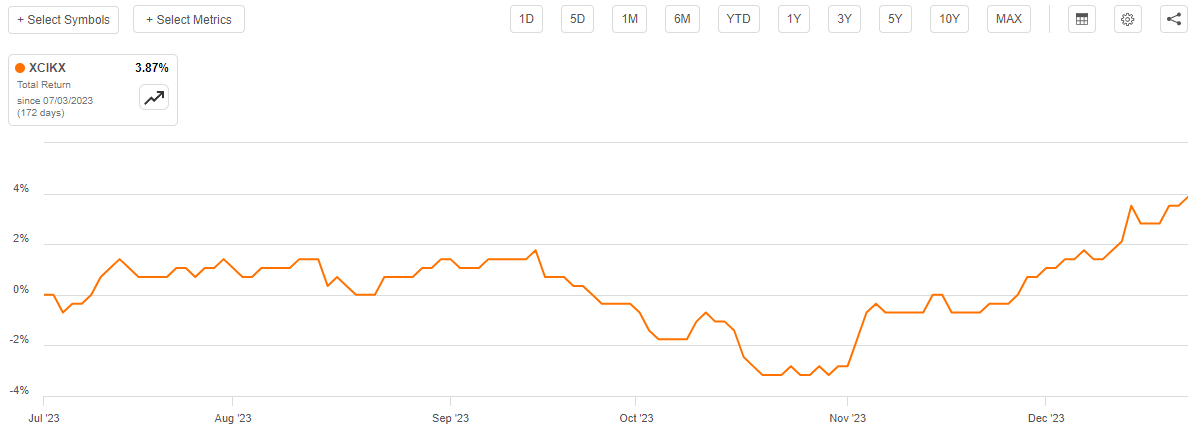

However, the fund was only able to cover the distributions by using its unrealized gains. It did not have sufficient net investment income and net realized gains to cover the payout. As everyone reading this is well aware, unrealized gains can be very quickly erased in a market correction, so they are not a dependable way of covering a distribution. Fortunately, in this case, it seems to be okay. As we can see here, the fund’s net asset value per share has increased by 3.87% since July 1, 2023:

{kind=link}

This strongly suggests that the fund has managed to fully cover all of the distributions that it has paid out since the end date of the most recent report with a substantial amount of money left over. Thus, the distribution is probably okay, and the fund should not need to cut the distribution in the near future.

Valuation

As of December 22, 2023 (the most recent date for which data is currently available), the Credit Suisse Asset Management Income Fund has a net asset value of $2.95 per share, but the shares currently trade for $3.10 each. That is a 5.08% premium on net asset value. This is substantially above the 4.02% discount that the shares have had on average over the past month. It also suggests that the fund’s shares have gotten ahead of themselves since this fund normally trades at a much cheaper price. Potential investors may want to wait until the premium fades and the shares once again trade at a discount before purchasing shares.

Conclusion

In conclusion, the Credit Suisse Asset Management Income Fund is a good junk bond fund that has gotten a bit too much attention recently from the market. The shares have been driven up far beyond any justifiable level, as there is no real reason for this fund to trade at a premium to the net asset value. It would be best to wait until the fund becomes available at a discount before buying in. It is certainly not a bad fund though, and could certainly prove to be a reasonable way to play junk bonds once the price drops.

For further details see:

CIK: Shares Of This Junk Bond CEF Are Trading At An Unjustifiable Price