CIK - CIK: This Underfollowed Junk Bond Fund Is Actually Pretty Good

2023-10-09 18:14:43 ET

Summary

- Credit Suisse Asset Management Income Fund, Inc offers a high level of income with a 10.42% yield, but that yield is not impressive compared to other income-focused closed-end funds.

- The fund has outperformed the Bloomberg U.S. Aggregate Bond Index this year by quite a lot.

- The fund invests heavily in junk bonds but has a diversified portfolio to mitigate default risk.

- There is the potential for interest rates to rise more as oil prices could reignite inflation, but the Fed will probably stand pat until next year.

- The fund did cover its distribution in the first half of the year, but only because of unrealized gains. It is uncertain the degree to which it will realize these gains.

Credit Suisse Asset Management Income Fund, Inc. ( CIK ) is a closed-end fund, or CEF, that advertises itself as a solution for those investors who are looking to generate a high level of income from their portfolios. It does this reasonably well, as is evidenced by its current 10.42% yield. This is a substantially higher yield than that possessed by most other assets in the market, although it is not especially impressive compared to other income-focused closed-end funds.

The fund’s performance so far this year has been reasonably strong, which is actually rather surprising considering that the rising interest rate environment has been punishing most assets that make yield an important part of their overall investment thesis. As we can see here, investors who purchased the fund back at the start of the year are now up 9.50%, which is shy of the 12.67% total return of the S&P 500 Index ( SP500 ) but considerably better than the loss that bond investors ( AGG ) took over the period:

{kind=link}

This is actually fairly surprising considering that the Credit Suisse Asset Management Income Fund is actually a bond fund itself. As such, we will want to investigate how exactly this fund has managed to outperform the Bloomberg U.S. Aggregate Bond Index by such a considerable margin. This article will seek to accomplish this task. In addition, we will attempt to determine if buying this fund could make sense for an income-focused investor today.

About The Fund

According to the fund’s website , the Credit Suisse Asset Management Income Fund has the primary objective of providing its investors with a high level of current income while still ensuring the preservation of capital. That is a very reasonable objective considering that 96.74% of the fund’s portfolio is invested in bonds:

CEF Connect

Bond funds frequently state that they have the preservation of principal as one of their objectives. This makes a lot of sense, too, as bonds are one of the only securities in the market in which an investor can have a very high degree of confidence that they will not lose money. After all, bonds pay their entire face value at maturity, so an investor who holds a bond over its entire life will not lose money unless the issuer of the security defaults. Default risk can generally be managed by simply holding a large number of bonds from different issuers, in order to ensure that any individual issuer only accounts for a very small percentage of the fund.

This fund uses that strategy to great effect. According to the fund’s fact sheet , which is dated August 31, 2023, the Credit Suisse Asset Management Income Fund has a total of 220 issuers represented in its portfolio. Of this total, the largest issuer only accounts for 1.33% of the portfolio:

Fund Fact Sheet

The largest issuer here is GEMS MENASA Cayman, which is unfortunately difficult to investigate. It is, in fact, not easy to find much information about the company at all. Fitch recently produced a positive outlook on the company’s debt. Based on Fitch’s report, it sounds as if the company is a private school operator in Dubai. Bloomberg has a different description :

GEMS MENASA Cayman Ltd/GEMS Education Delaware LLC is set up as a dual issuer and operates as a special purpose entity. The Company was formed for the purpose of issuing debt securities to repay existing credit facilities, refinance indebtedness, and for acquisition purposes.

It, therefore, appears that this company is basically something that is intended to raise debt financing from the American and international capital markets for the benefit of a private school operator in Dubai. While this may seem sketchy at first, this is actually something that is quite common to allow companies to access capital markets that otherwise may be difficult for them to access or as a method of limiting liability. The positive outlook from Fitch should give us a certain amount of confidence that the debt is not overly risky, although it does still have a B rating, which is considered a speculative grade. Even in the event of a default, we can still see that it only represents 1.33% of the portfolio so a full default here would not have a noticeable impact on the fund. In fact, the interest payments alone from the other securities in the portfolio will more than offset the full loss that the fund would incur should GEMS MENASA or anything else in its portfolio default. Thus, investors do not really have too much to worry about here.

As might be expected from the speculative-grade rating of the fund’s largest position, the Credit Suisse Asset Management Income Fund invests heavily in junk bonds. We can clearly see this by looking at the weightings assigned to all of the securities that comprise the fund’s portfolio. Here is a high-level summary:

Fund Fact Sheet

A junk bond is anything rated BB or lower. As can be clearly seen here, that is 95.19% of the portfolio. This may be concerning to some investors, despite the discussion that we just had about the fund’s overall diversification as a protection against default losses. However, we can see that 70.87% of the bonds in the fund have a BB or a B rating, which are the two highest possible ratings for junk bonds. This is good because the official bond ratings scale states that bonds with a BB or a B rating are issued by companies that have sufficient financial capacity to carry their existing debt. These companies should also be able to carry their debt through a short-term economic crisis, although a long-term crisis may pose problems. Fortunately, long-term crises are quite rare. When we combine this with the fund’s diversification and low weighting to any individual asset, we can conclude that we probably do not really need to worry too much about default risk. The biggest risk here would be something that affects every security in the fund at the same time, such as changing interest rates.

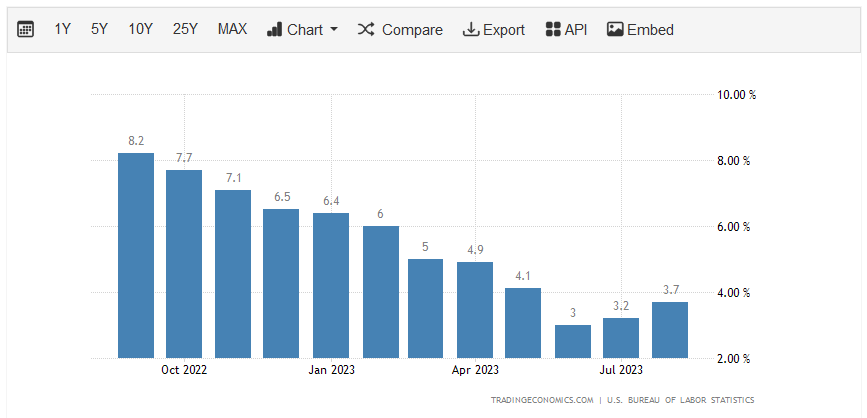

The future of interest rates is something that is uncertain right now. A majority of the members of the Federal Open Market Committee, which is the governing body that sets the federal funds rate, expect that the federal funds rate will be at 5% to 5.25% at the end of 2024. That would mean a 25-basis-point cut sometime next year. However, there is no certainty that this will be the case. One big reason for this is that inflation is trending in the wrong direction. As we can see here, the year-over-year change in the headline consumer price index increased in both July and August:

{kind=link}

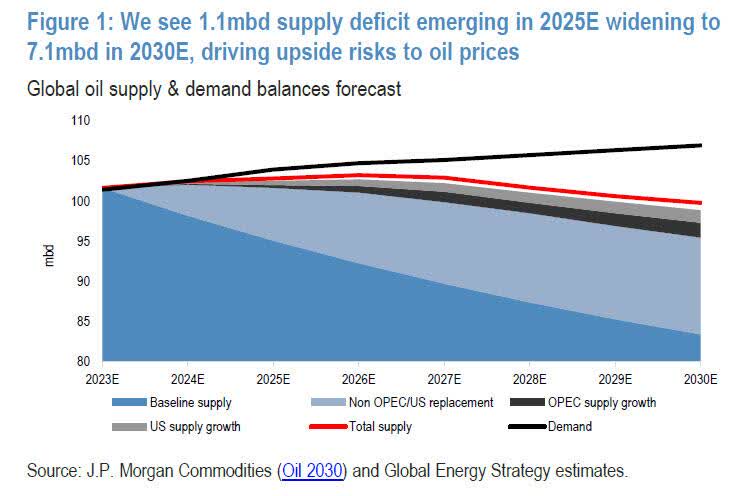

It remains to be seen what September’s number will show, but at the moment inflation appears to be trending in the wrong direction. As I pointed out in numerous articles recently that went out to subscribers to Energy Profits in Dividends, this is due to oil prices going up over the past few months. That looks quite likely to be a long-term trend due to the energy industry in aggregate substantially underinvesting in production capacity over the past decade. Analysts at JP Morgan currently project that the world will have a 1.1 million barrel per day deficit in 2025 and a 7.1 million barrel per day deficit of crude oil production relative to demand:

Zero Hedge/Data from JP Morgan Chase

{kind=link}

This is likely to pressure oil prices upward and thus have a negative impact on the inflation numbers. This could be a very real problem as we approach the latter half of 2024 and force the Federal Reserve’s current predictions of an interest rate cut next year to be incorrect. In addition, I have been seeing a number of predictions from various analysts that suggest that the economy will not experience anything close to a “soft landing.” In fact, a recession (if not a severe one) looks more likely and if that is the case, then the central bank may cut rates.

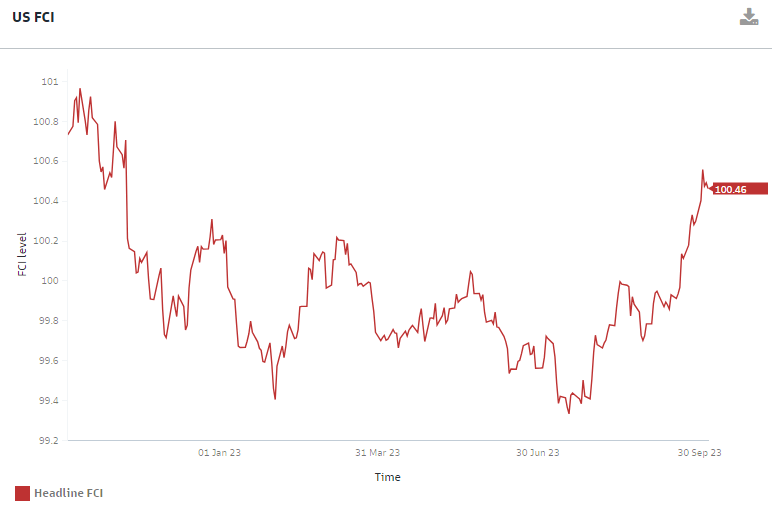

In short, there are currently too many factors at play to make an accurate prediction as to the future direction of interest rates. As such, it is difficult to determine where this fund might be in a year or two. However, it does seem rather unlikely that the central bank will actually raise rates again this year. This is mostly due to the increase in U.S. Treasury yields over the past two months. This has rapidly increased the financial conditions index:

{kind=link}

The sharp increase that we see in this index has had the effect of cooling the economy, which is exactly the goal that the Federal Reserve hopes to achieve when it raises interest rates. Thus, the market has basically done the job of hiking rates and greatly reduced the need for the Federal Reserve to raise rates once more this year. This development has prompted analysts at Rabobank and Goldman Sachs to expect that the central bank will stand pat for the remainder of this year while it evaluates the impact that the current situation has on the economy. This is a viewpoint that has been publicly shared by a few top officials at the various Federal Reserve banks, although Chairman Powell has made no public comment on this development at the time of writing.

Leverage

One of the defining characteristics of closed-end funds is that they typically use leverage as a method of boosting their effective yields. The Credit Suisse Asset Management Income Fund is no exception to this. I explained how this works in various previous articles. To paraphrase myself:

In short, the fund borrows money and then uses that borrowed money to purchase junk bonds and similar high-yielding assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. Unfortunately, this strategy is not as effective today as it was two years ago because the difference between the rate at which is fund borrows and the rate that it receives on the purchased assets is narrower than it used to be.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage because that would expose us to an excessive amount of risk. I generally like a fund’s leverage to be under a third as a percentage of its assets for that reason.

As of the time of writing, the Credit Suisse Asset Management Income Fund has leveraged assets comprising 30.95% of its portfolio. This is lower than many other debt funds, which is a sign that this fund is probably not using an excessive amount of debt. Rather, it appears that it is striking a reasonable balance between risk and reward. While it is certainly true that the fund will have more risk than one using no leverage, such a fund would also almost certainly have a lower yield. For the most part, everything should be okay here as long as you can accept a bit more volatility than a comparable index fund would possess.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Credit Suisse Asset Management Income Fund is to provide its investors with a high level of current income. In pursuance of that objective, the fund invests its assets in a variety of junk bonds, which will naturally have significantly higher yields than less risky assets. The fund then borrows money to purchase even more bonds that provide it with income in excess of what the fund can obtain solely by using its equity. It then collects all payments made by the bonds in the portfolio, as well as any capital gains that it manages to realize by trading the bonds, and pays the money out to its shareholders, net of its own expenses. Given the nature of what this bond invests in, we can expect that this would result in the fund possessing a fairly high distribution yield.

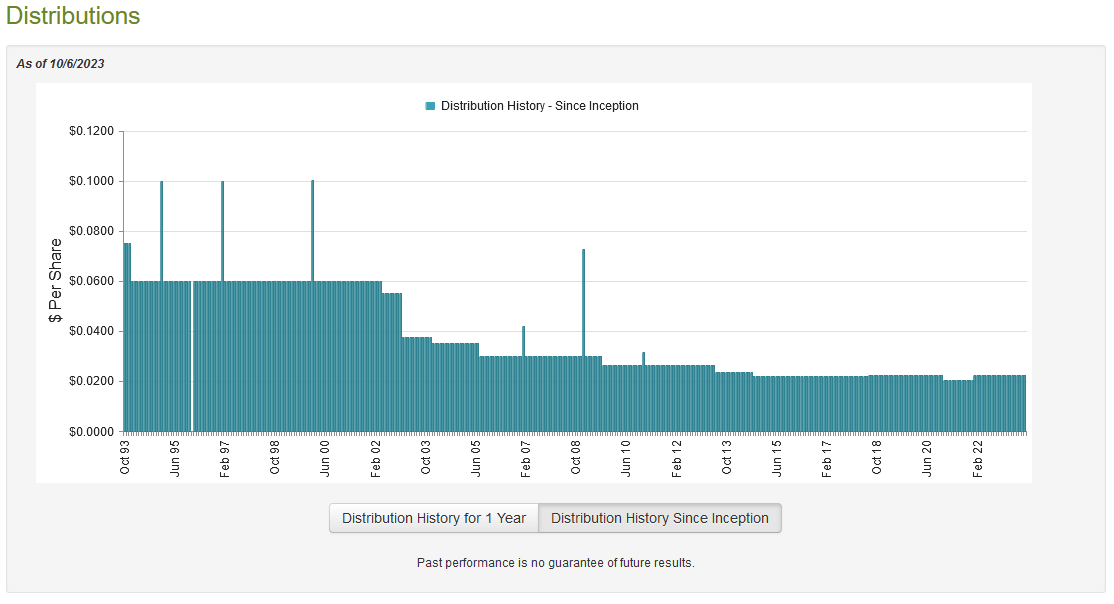

This is certainly the case as the Credit Suisse Asset Management Income Fund pays a monthly distribution of $0.0225 per share ($0.27 per share annually), which may not seem like much but it is sufficient to give the fund a 10.42% yield at the current price. The fund’s long-term distribution history, unfortunately, leaves a great deal to be desired but it has actually done pretty well since the financial crisis in 2007:

{kind=link}

Overall, this distribution history may not be particularly appealing to anyone who is seeking to earn a safe and consistent income from their portfolios. However, the fund’s distribution has been reasonably stable for most of the past decade, especially for a bond fund. That alone is quite nice, although it does raise some questions about how this fund was able to accomplish a feat that very few other funds have managed to accomplish.

Naturally, the fact that this fund has been able to provide a more stable distribution than many other funds means that we should investigate the methods through which it is obtaining the money to pay the distribution. After all, we do not want to be the victims of a distribution cut that reduces our incomes and almost certainly causes the share price to decline.

Fortunately, we do have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is nice as it covers the first half of this year, which was generally a pretty optimistic and strong one for bonds. Investors generally expected that the Federal Reserve would rapidly pivot and begin cutting interest rates as early as the second half of this year, so they were bidding up bonds and by extension driving yields down. The fact that they were bidding up bonds may have provided the fund with the opportunity to obtain a certain amount of capital gains by selling appreciated securities into the optimistic market.

During the six-month period, the Credit Suisse Asset Management Income Fund received $8,690,617 in interest and $31,614 in securities lending income. Surprisingly, the fund reported no dividends, not even from money market funds. In total, it reported an investment income of $8,722,231 before taxes and other expenses. The fund naturally paid its expenses out of this amount, which left it with $6,452,067 available for shareholders. This was, unfortunately, not enough to cover the $7,106,023 that the fund actually paid out during the period, although it did get pretty close. However, it still could be concerning considering that we usually like a fixed-income fund to be able to fully fund its distribution out of net investment income.

With that said, the fund does have other means through which it can obtain the money that it needs to cover the distribution. For example, the fund might have been able to sell some of its appreciated bonds into the favorable market and realize some capital gains. Unfortunately, the fund had mixed results in this task. During the six-month period, the fund reported net realized losses of $9,765,520 but these were more than offset by $15,871,925 net unrealized gains. Overall, the fund’s net assets increased by $5,484,972 during the period after accounting for all inflows and outflows. As such, it technically did manage to cover the distributions, but this only happened because of its unrealized gains. As everyone reading this is likely aware, unrealized gains can quickly vanish in a market correction so there is no guarantee that this distribution coverage will remain. Overall, I would feel more comfortable if this fund had sufficient net investment income and net realized gains to cover its distributions. It did still manage to do better than many other fixed-income closed-end funds, though.

Valuation

As of October 6, 2023 (the most recent date for which data is currently available), the Credit Suisse Asset Management Income Fund has a net asset value of $2.79 per share but the shares only trade for $2.60 each. This gives the fund’s shares a 6.81% discount on net asset value at the current price. This is not nearly as attractive as the 8.48% discount that the shares have had on average over the past month, so it might be best to wait for a market correction before buying in. The shares are still trading for less than intrinsic value though, so it is not necessarily a problem buying at the current price.

Conclusion

In conclusion, the Credit Suisse Asset Management Income Fund is a reasonably good junk bond fund that currently trades at an attractive valuation. The fund enjoys a substantial amount of diversification that should ensure that the overall default risk is low here, which is a necessity when investing in junk bonds. There is still interest rate risk, of course, but right now we probably will not see the Federal Reserve raise rates, but of course, rates might still go up in the market due to the insatiable demand for cash from the Federal Government.

Overall, the biggest problem with Credit Suisse Asset Management Income Fund is that it was not able to cover its distribution solely out of net investment income during the first half of the year, so it is uncertain how sustainable its payout actually is. I am not anticipating a distribution cut at this time, though.

For further details see:

CIK: This Underfollowed Junk Bond Fund Is Actually Pretty Good